Your wallet’s probably stuffed with payment options these days. Credit cards, mobile apps, crypto, buy-now-pay-later schemes-the types of digital payments available have exploded, and honestly, it’s getting confusing.

Your wallet’s probably stuffed with payment options these days. Credit cards, mobile apps, crypto, buy-now-pay-later schemes-the types of digital payments available have exploded, and honestly, it’s getting confusing.

At Web3 Enabler, we’ve put together this guide to cut through the noise. Whether you’re a business owner choosing payment systems or just curious about what’s actually out there, we’ll walk you through the real options, the trade-offs, and what’s actually worth your attention.

Traditional Digital Payment Methods

Cards Still Rule (But They Cost You)

Credit and debit cards remain the backbone of online shopping and in-store transactions. 92% of shoppers used a digital payment method in the last year. Cards work, people trust them, and merchants accept them everywhere. But here’s the catch: per-transaction processing fees add up fast. Banks take a cut every single time you swipe, and those percentages compound across thousands of transactions. If you run a business, those fees directly impact your margins.

Bank Transfers and ACH: The Cheap Alternative

Bank transfers and ACH payments exist for scenarios where speed matters less than cost. They’re dirt cheap compared to cards-ACH payments cost pennies per transaction. This makes them perfect for recurring subscriptions, invoicing, or high-volume operations where cost savings matter more than instant settlement. Settlement takes longer (sometimes days), but the financial advantage justifies the wait for many businesses.

Mobile Wallets and P2P Apps Are Winning

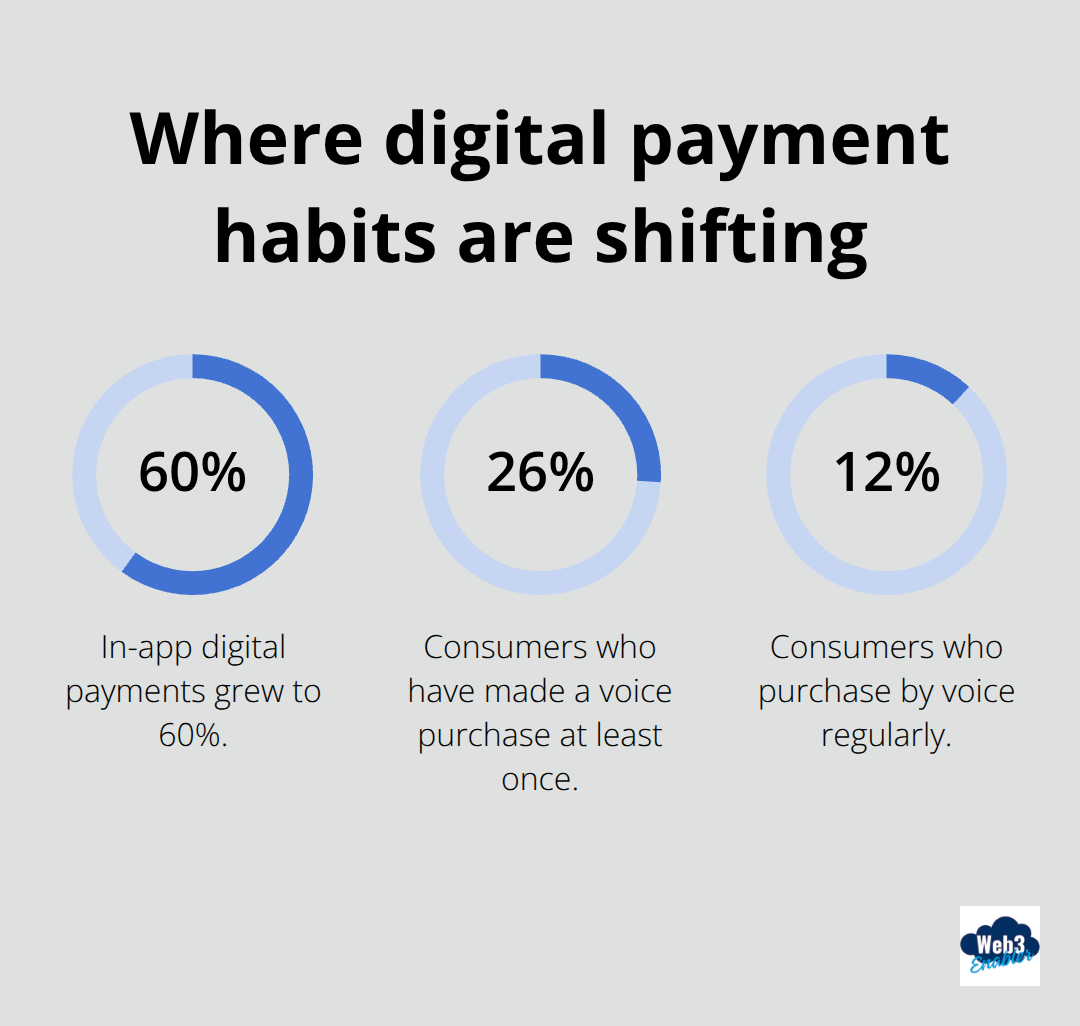

Digital wallets like Apple Pay, Google Pay, and Samsung Pay have quietly become massive. In-app digital payments grew to 60%, while customers appreciate the lower friction and smoother experience compared to physical cards. P2P payment apps like Venmo and Cash App started as friend-to-friend tools but now work at checkout too. Voice payments represent the outlier here-26% of consumers have made a voice purchase at least once, with 12% doing it regularly (Voicebot and Rain Agency). It’s niche, but it signals where convenience heads next.

Building Infrastructure That Handles Multiple Methods

The real strategic question for businesses isn’t whether to accept these methods individually-it’s whether your payment infrastructure can handle multiple methods simultaneously without chaos. You need a POS system or payment gateway that supports the mix you actually want to offer. Security isn’t optional either. Tokenization replaces sensitive card data with encrypted tokens, PCI DSS compliance is mandatory for anyone touching card information, and two-factor authentication should be standard. The infrastructure exists to do this right, but too many businesses cut corners.

Settlement Speed and Fee Structures Matter More Than You Think

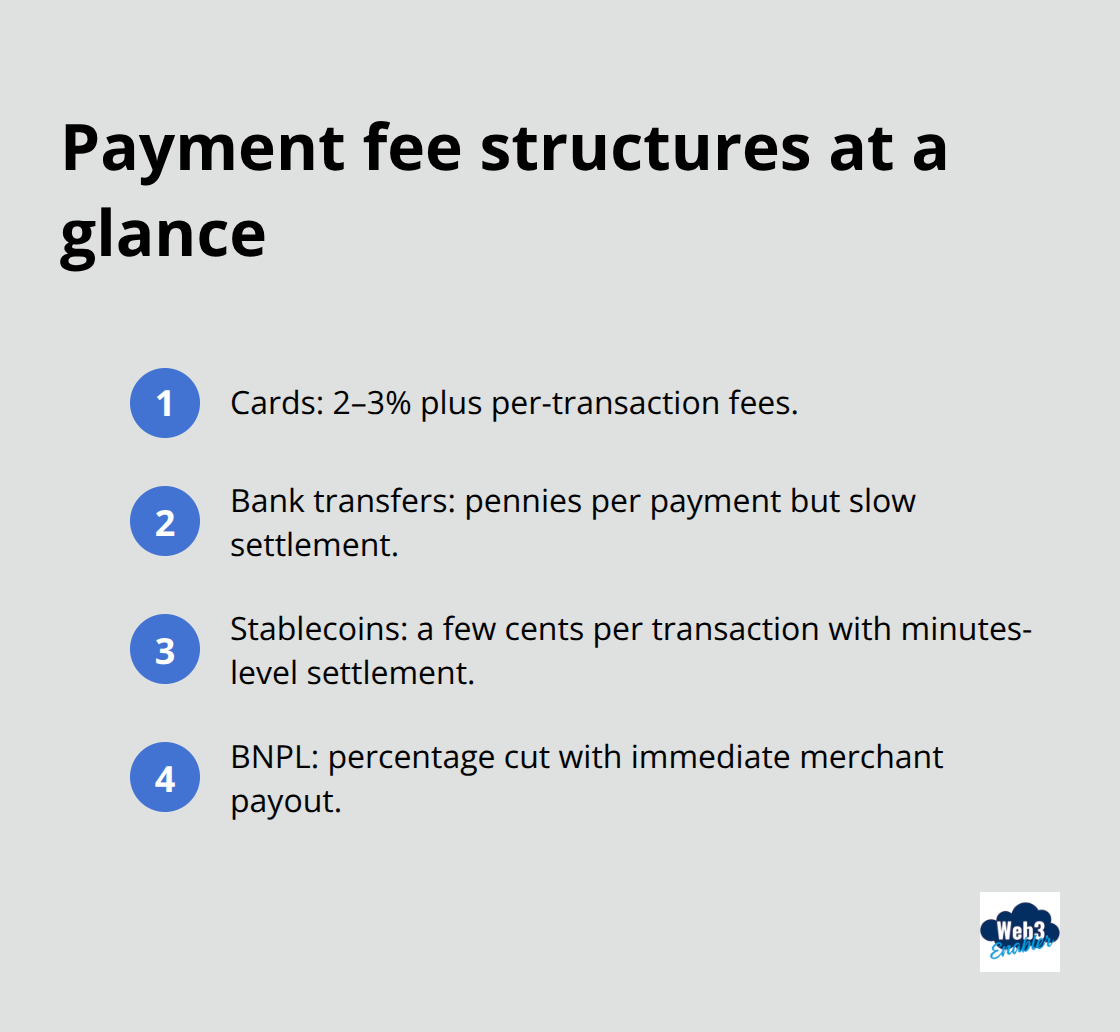

Processing times directly affect your cash flow. Cards settle in days, bank transfers take even longer, but mobile wallets and modern payment platforms move money faster. That difference between same-day and three-day settlement changes your operations. Fees pile up differently too-credit card processing typically runs 2-3% plus per-transaction fees, while bank transfers might be flat fees or nearly free depending on your bank. Buy Now Pay Later services like Affirm and Klarna give merchants full payment upfront minus their cut, shifting the installment burden to the BNPL provider instead of your business.

These traditional methods still dominate because they work. But they’re not the only game in town anymore. Emerging payment solutions built on blockchain rails are starting to challenge the old guard with faster settlement, lower costs, and global reach that traditional systems simply can’t match.

Emerging Digital Payment Solutions

Stablecoins Challenge Traditional Settlement Speed

Stablecoin payments have moved from crypto niche to serious infrastructure. Global crypto transaction volume topped $10.6 trillion in 2024, up 56 percent year-over-year, with stablecoins doubling in circulation between 2023 and 2025 according to Stripe. Global stablecoin circulation hit 307 billion dollars in November 2025, growing above 50 percent annually. This isn’t hype-merchants and businesses actively choose faster settlement over traditional banking rails. Stablecoins like USDC maintain 1-to-1 value against the dollar while settling in minutes instead of days. Cross-border crypto payments cost only a few cents per transaction regardless of location, obliterating the margin-crushing fees that cards impose. Stripe now processes stablecoin payments alongside traditional methods, and over 15,000 businesses worldwide accept crypto. Settlement completes in minutes, reducing chargeback risk once confirmed on-chain, and merchants expand into regions with currency instability or limited banking infrastructure without currency conversion delays.

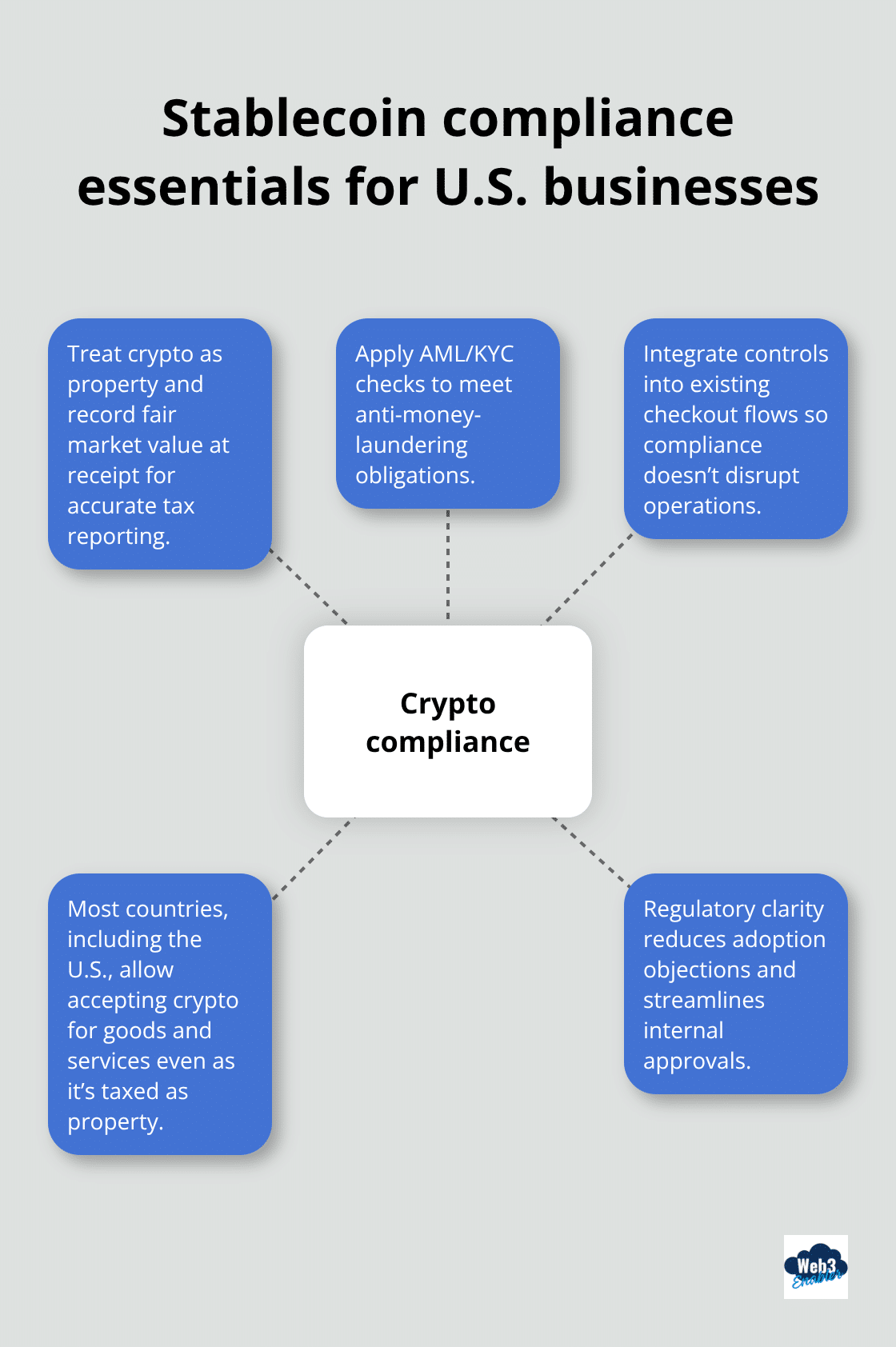

Compliance Keeps Stablecoin Payments Legitimate

You still need compliance when accepting stablecoins. Treat crypto as property for tax purposes, log fair market value at receipt, and follow AML/KYC rules. The infrastructure exists to integrate this seamlessly into existing checkout flows, so compliance doesn’t require reinventing your operations. Most countries (including the US) permit accepting crypto for goods and services legally, though crypto remains taxed as property rather than legal tender.

This regulatory clarity removes the biggest objection many businesses had just two years ago.

BNPL Shifts Risk Away From Merchants

Buy Now Pay Later services like Affirm, Klarna, and Afterpay shifted the payment friction away from merchants entirely. Merchants receive full payment upfront minus the BNPL provider’s cut, meaning you don’t front money while customers pay installments. This works exceptionally well for high-ticket items where customers hesitate at checkout due to price. The downside: BNPL providers take their margin, and you lose some control over customer relationships since the financing company owns that interaction.

CBDCs Remain Limited for Global Commerce

Central Bank Digital Currencies represent a different beast entirely-government-backed digital currencies designed to modernize domestic payments and improve settlement efficiency. They exist, but global interoperability remains limited, making them less relevant for cross-border commerce right now. The real shift happening is that blockchain-based payments excel where traditional systems fail: cross-border transfers, platform-based ecosystems, and programmable payments that execute automatically based on conditions.

How Blockchain Payments Actually Work

A blockchain payment flows from a signed transaction through broadcast, consensus, block formation, and on-chain settlement with increasing finality over confirmations. This push-based model eliminates chargebacks but requires senders to verify recipient details before sending, making user experience critical. Stablecoins serve as the dominant asset class for on-chain payments due to predictable value and fast settlement. Native cryptocurrencies remain volatile and less ideal for retail, while tokenized fiat and regulated digital cash serve as compliant, familiar settlement assets on blockchain rails. The infrastructure supporting these payments-wallets, bridges, and liquidity pools-underpins modern digital payment rails, enabling faster settlements than traditional finance can match. This foundation sets the stage for understanding which payment method actually fits your business needs and where the real competitive advantages lie.

What Actually Costs More and What Saves You Money

Security Protects Your Bottom Line

Security matters more than most businesses realize, but it doesn’t have to mean expensive overhauls. Tokenization replaces sensitive card data with encrypted tokens before it ever touches your systems, which dramatically reduces your liability if data gets breached. PCI DSS compliance is mandatory for anyone processing card information, and honestly, the compliance frameworks exist specifically to prevent the costly disasters that happen when businesses skip this step. Two-factor authentication costs almost nothing to implement yet stops most fraud cold. The real expense isn’t security infrastructure-it’s what happens when you ignore it. A single data breach costs companies millions in remediation, legal fees, and lost customer trust. That’s not theoretical. That’s why financial institutions and payment processors obsess over security standards that seem excessive until you’re the one explaining to customers why their data got stolen.

Settlement Speed Changes Your Cash Flow

Speed and convenience sound vague until you measure them against your actual cash flow. Cards settle in days, sometimes longer depending on your bank, which means you fund operations on money that hasn’t actually arrived yet. Stablecoins settle in minutes, which changes everything for businesses operating on tight margins. That difference between waiting three days and receiving funds in an hour compounds across thousands of transactions. Mobile wallets reduce checkout friction measurably-customers complete purchases faster when they don’t have to hunt for their card or type in lengthy payment information. The convenience factor directly correlates with conversion rates. Lower friction means fewer abandoned carts.

Fee Structures Determine Your Real Profitability

Credit cards charge 2-3 percent plus per-transaction fees that accumulate relentlessly. Bank transfers cost pennies but take forever. Stablecoin payments cost a few cents per transaction regardless of whether you send money across town or across borders, with settlement times measured in minutes instead of days. BNPL services charge you a percentage cut, but merchants receive full payment immediately instead of waiting for installment collections.

The fee structure you choose determines your actual profitability, not just your stated margins.

The Math Behind Payment Method Choices

A business moving high transaction volumes can save thousands monthly by optimizing payment methods. That’s not speculation-that’s the math that drives over 15,000 businesses to accept crypto payments already. The hard truth about costs: you need to calculate what each payment method actually costs you after fees, settlement delays, and operational overhead. Most businesses discover that their “standard” payment mix (typically card-heavy) costs far more than alternatives they never considered. Stablecoin infrastructure now integrates into existing checkout flows, so switching doesn’t require rebuilding your entire operation. The competitive advantage goes to businesses that measure their actual costs and adapt their payment mix accordingly.

Final Thoughts

Payment methods have fundamentally shifted, and the types of digital payments available now span traditional rails, blockchain-based settlement, installment financing, and government-backed currencies. Five years ago, your options were cards, bank transfers, or maybe a digital wallet if you were early. Today, that explosion of choice isn’t noise-it’s competition forcing the old guard to move faster and cheaper. Over 15,000 businesses worldwide now accept crypto payments because the math works, not because they’re betting on hype.

Choosing the right payment solution depends on three concrete factors. First, measure your actual costs across methods-cards, bank transfers, stablecoins, and BNPL all have different fee structures and settlement timelines. Second, understand your customer base, since high-volume operations benefit from cheap settlement like stablecoins or ACH, while retail businesses with price-sensitive customers might prioritize BNPL to reduce checkout friction. Third, evaluate whether your infrastructure can handle multiple payment types simultaneously and whether your team understands compliance requirements for each method.

The competitive advantage goes to businesses that treat payment methods as strategic choices rather than fixed constraints. Stablecoins will continue capturing cross-border and high-volume transactions because they’re faster and cheaper, cards remain dominant for retail because customers trust them, and BNPL grows for high-ticket purchases. If you’re ready to explore how blockchain-based payments fit your operation, Web3 Enabler provides Salesforce-native solutions that connect stablecoin payments directly into your existing systems without requiring a complete infrastructure rebuild.