The digital payment landscape is shifting fast, and two major players are fighting for dominance: tokenized deposits and stablecoins. Both promise to revolutionize how businesses handle money, but they’re built on completely different foundations.

We at Web3 Enabler see companies getting confused about which solution fits their needs. The tokenized deposits vs stablecoins debate isn’t just technical jargon – it’s about choosing the right financial infrastructure for your business future.

What Exactly Are Tokenized Deposits

Tokenized deposits put your traditional bank deposits on blockchain rails. Think of them as digital twins of the money that sits in your corporate account, but with superpowers. JPMorgan’s JPM Coin has proven these aren’t just experimental toys anymore, with stablecoins projected to reach $500–750 billion in the coming years.

Major banks like Citi and JP Morgan already use tokenized deposits for real-time liquidity management across different countries and currencies. These digital representations maintain all the regulatory protections you expect from traditional banking.

Banks Maintain Full Control

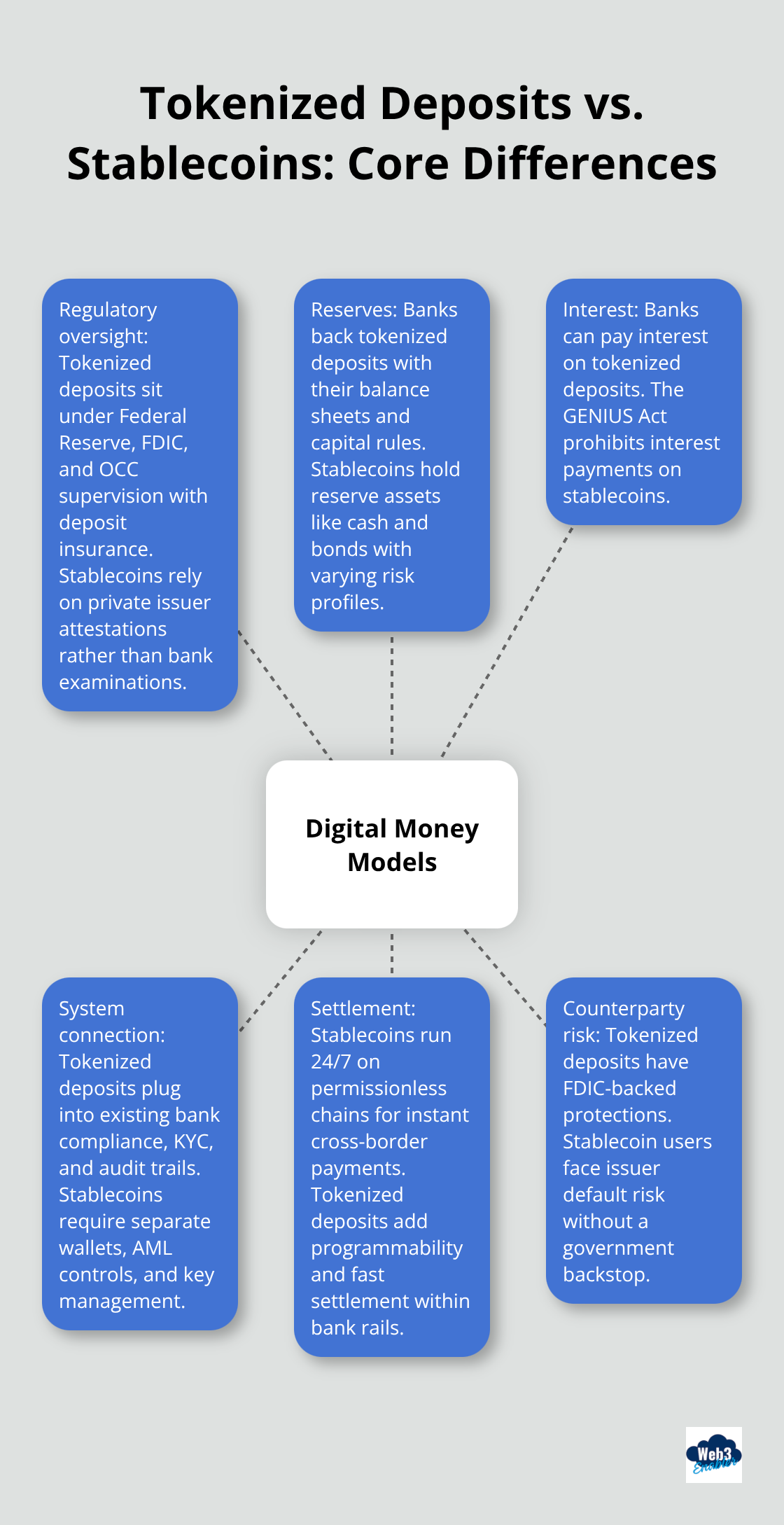

The biggest difference from other digital currencies? Your bank still holds your actual cash. When you receive tokenized deposits, the bank creates a blockchain representation of your account balance. This means you deal with the same regulatory protections and deposit insurance you’ve always had.

No mysterious offshore entities or algorithmic mechanisms back these deposits. Your corporate treasurer can sleep soundly because the Federal Reserve still watches over these funds. Banks can even pay interest on tokenized deposits (unlike stablecoins where the GENIUS Act specifically prohibits interest payments).

Direct Banking System Connection

Tokenized deposits plug directly into your current banking infrastructure. Your compliance processes, KYC requirements, and audit trails remain intact. The blockchain layer adds programmability and instant settlement capabilities without disruption to your established relationships.

This makes tokenized deposits perfect for businesses that need blockchain benefits but can’t abandon traditional oversight. Corporate finance teams love this approach because they avoid the regulatory headaches that come with cryptocurrency holdings on their balance sheets.

While tokenized deposits offer familiar banking comfort, stablecoins take a completely different approach to digital money.

What Makes Stablecoins Different

Stablecoins flip the script on traditional digital payments. They operate as cryptocurrencies that maintain stable value through asset backing. Unlike tokenized deposits that rely on bank infrastructure, stablecoins like USDT and USDC exist independently on blockchain networks.

Tether’s USDT leads with over $176 billion in circulation, while Circle’s USDC has reached $74 billion according to recent market data. These private companies issue digital tokens backed by cash reserves and government bonds, but they operate outside traditional bank oversight.

Private Companies Control the Money Supply

Circle and Tether don’t need bank licenses to issue billions in digital currency. They maintain reserves through trust structures and publish monthly attestations about their asset backing. USDC focuses on transparency with 100% backing in cash and short-term government bonds, while USDT includes riskier commercial paper in its reserves.

This creates a fundamental difference from tokenized deposits where regulated banks guarantee the underlying funds. The GENIUS Act specifically prohibits stablecoins from interest payments, which makes them less attractive for corporate treasury management compared to interest-bearing bank deposits.

Global Payment Networks Without Bank Infrastructure

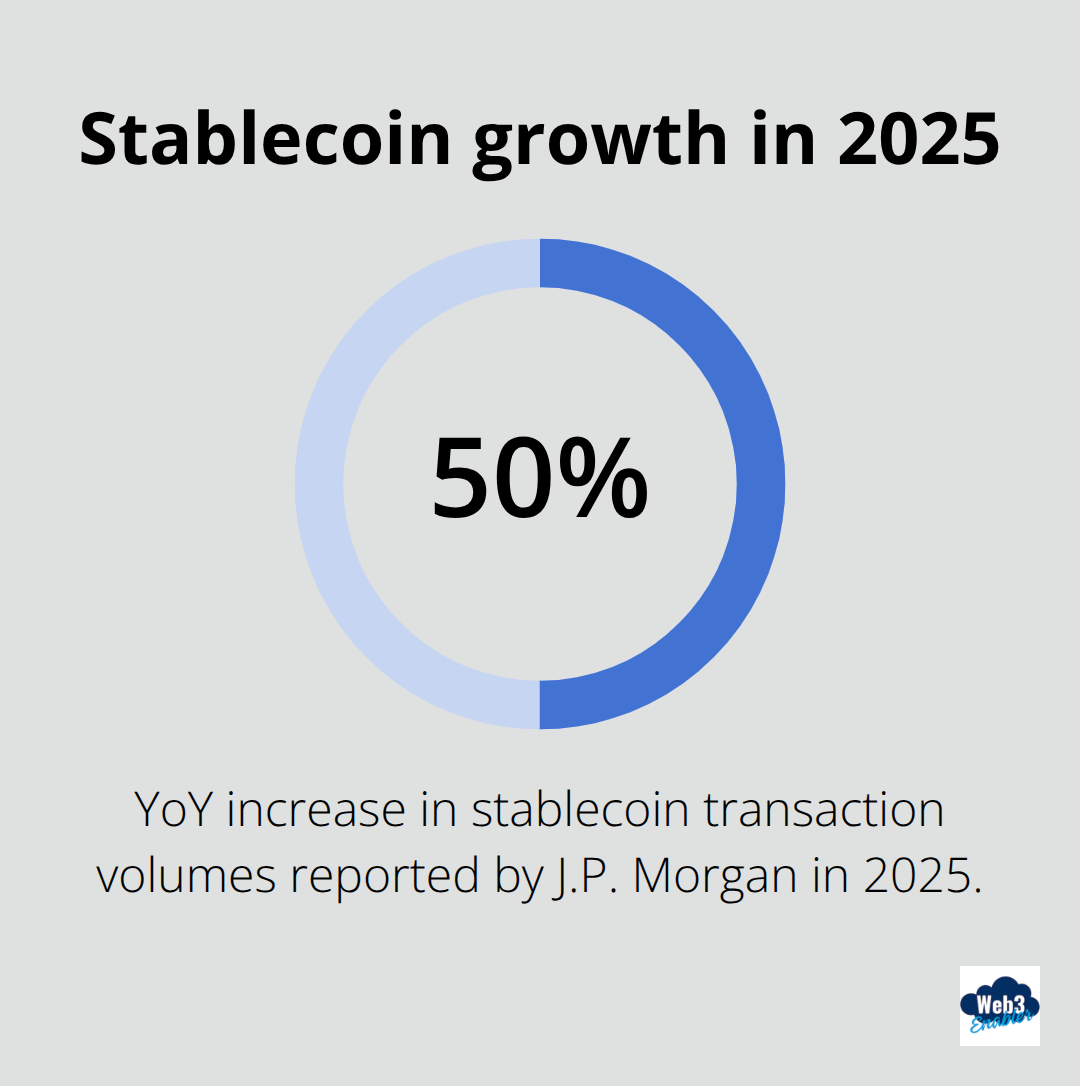

Stablecoins operate 24/7 across permissionless blockchains like Ethereum and Solana. They enable instant cross-border payments without correspondent bank delays. J.P. Morgan reported a 50% year-over-year increase in stablecoin transaction volumes in 2025, driven by businesses that seek faster international settlements.

Companies can send $10 million to suppliers in emerging markets within minutes rather than days through traditional wire transfers. However, this speed comes with compliance challenges since businesses must handle their own KYC processes and anti-money laundering requirements (without bank intermediaries that manage regulatory oversight).

These fundamental differences in structure and operation create distinct advantages and challenges that businesses must weigh carefully.

Where Do They Actually Differ

The regulatory gap between tokenized deposits and stablecoins creates vastly different risk profiles for corporate finance teams. Tokenized deposits fall under traditional bank oversight where the Federal Reserve, FDIC, and OCC maintain supervision through established bank examination processes. Your corporate deposits remain protected by the same deposit insurance and capital requirements that govern regular bank accounts.

Stablecoins operate under the Payment Services Act framework where private companies like Circle and Tether self-attest their reserve status through monthly reports rather than bank examinations. The GENIUS Act prohibits stablecoins from interest payments, which makes them less attractive for treasury management compared to interest-bearing tokenized deposits that banks can offer.

Reserve Standards Tell the Real Story

JPM Coin operates with fractional reserve practices where JPMorgan holds actual customer deposits and creates blockchain representations backed by the bank’s full balance sheet. Circle maintains USDC reserves in cash and short-term government bonds with monthly attestations from Grant Thornton, while Tether’s USDT includes commercial paper and corporate bonds that carry credit risk.

This means tokenized deposits benefit from bank capital requirements and stress tests, while stablecoin holders depend entirely on private company reserve management. Corporate treasurers face different counterparty risks: bank failure protection through FDIC insurance versus stablecoin issuer default risk with no government backstop.

System Connection Complexity Varies Dramatically

Tokenized deposits plug directly into current corporate bank relationships where your compliance procedures, audit trails, and KYC processes remain intact. Companies can leverage programmable features while they maintain established credit lines, foreign exchange services, and cash management tools from their primary bank.

Stablecoins require businesses to build separate compliance infrastructure for cryptocurrency assets, implement their own anti-money laundering procedures, and manage private key security without bank intermediaries. The operational burden shifts entirely to corporate teams who must handle wallet management, blockchain transaction oversight, and regulatory reports that banks typically manage for tokenized deposits (creating significant internal resource demands).

Final Thoughts

The tokenized deposits vs stablecoins decision comes down to your risk tolerance and operational priorities. Corporate finance teams that value regulatory certainty and bank relationships choose tokenized deposits. These solutions integrate with current compliance frameworks while they add blockchain programmability.

Stablecoins attract businesses that prioritize speed and global reach over traditional oversight. Companies in emerging markets or those that need 24/7 settlement capabilities often pick stablecoins despite the extra compliance burden. EY predicts stablecoins will account for over 5% of global payments by 2030 (while banks offer more tokenized deposit services to compete).

Your choice depends on specific operational needs and strategic goals. Treasury departments that want interest-bearing digital assets favor tokenized deposits, while companies that need permissionless global payments lean toward stablecoins. We at Web3 Enabler help businesses navigate these decisions through our Salesforce-native blockchain solutions that support both payment types within corporate infrastructure.