Your business sends money across borders constantly. Yet you’re still stuck with wire fees that sting, settlement times that drag on for days, and zero visibility into where your cash actually is.

We at Web3 Enabler built USDC remittance solutions directly into Salesforce because your payment infrastructure shouldn’t feel like it’s from 2005. When you can move money in minutes instead of days-and cut fees by half-your bottom line notices immediately.

Why Your Money Moves at Bank Speed, Not Internet Speed

Traditional remittances operate on a system designed for the 1970s, which explains why your international payments crawl. A typical wire transfer costs between 1% and 6% in fees, according to G20 data, while remittance corridors average over 3% per transaction. When you move money for payroll, vendor payments, or customer settlements across borders, those percentages compound fast. A $100,000 payment to a contractor in Mexico or the Philippines costs you $3,000 in fees alone, before you factor in the currency spreads banks slip in quietly. That’s not a rounding error-that’s real cash leaving your business for no value in return.

The Settlement Time Trap

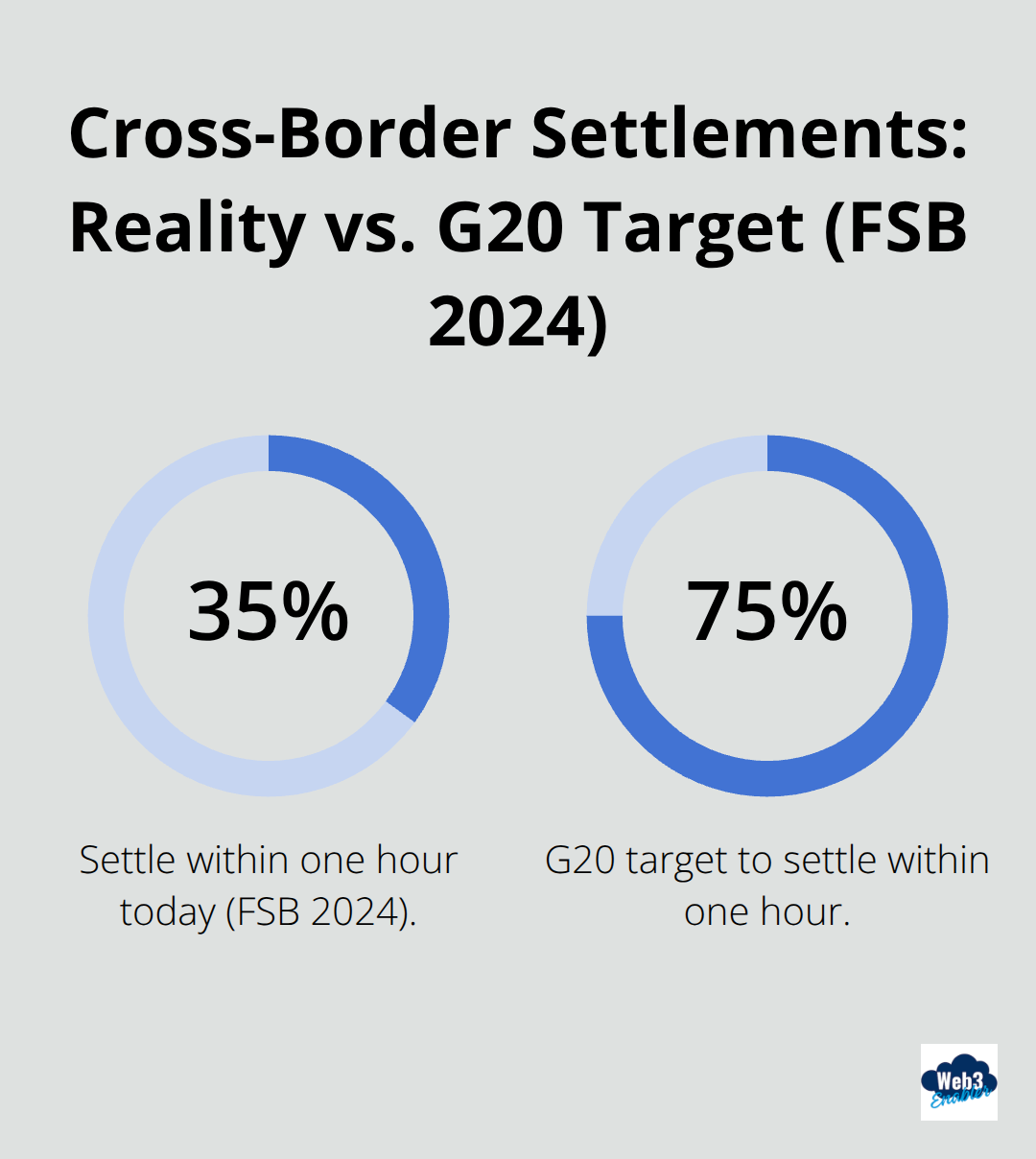

Settlement times reveal the real problem. Traditional correspondent banking takes three to five business days minimum, often stretching longer when weekends or holidays interrupt the chain. Your payment leaves your account immediately, but the recipient doesn’t see funds for days. This creates a cash flow nightmare for businesses operating globally. A 2024 assessment from the Financial Stability Board noted that only 35% of retail cross-border payments settle within one hour, despite G20 targets demanding 75% by now. Your business must pre-fund accounts in multiple currencies just to keep operations moving, tying up capital that could work elsewhere.

Meanwhile, banks control whether your payment moves fast or slow, and they have zero incentive to speed things up because slower settlements justify higher fees.

The Layered Fee Structure

Banks bundle costs so opaquely that most businesses never calculate the true damage. You pay an outgoing wire fee, a correspondent bank fee, a receiving bank fee, currency conversion spreads, and sometimes even a fee just to confirm the payment went through. That $100,000 payment actually costs the recipient less than $97,000 due to this layering. Emerging markets suffer worse-stablecoins already serve payments and payroll across 15 countries, with adoption strongest in regions where traditional fees make remittances economically painful. Your vendors in these regions lose purchasing power to fees before they ever touch the money.

Why Banks Defend the Status Quo

Banks justify these costs by citing risk, compliance, and infrastructure expenses, but those arguments collapse when you realize blockchain networks settle transactions in minutes for pennies. The real reason they maintain this system is simple: opacity protects margins. Stablecoins like USDC eliminate the middlemen who profit from delay and complexity. When you can move value directly on a blockchain, you remove the correspondent banks, currency desks, and settlement intermediaries that each extract their cut. This isn’t theoretical-the BVNK report shows that over $300 billion in stablecoin activity already flows through payments and payroll channels, proving that businesses and workers actively choose faster, cheaper rails when they’re available.

The question isn’t whether blockchain remittances work. The question is whether your business will modernize its payment infrastructure before your competitors do. Building remittance solutions directly into your existing systems-like Salesforce-lets you capture these savings without ripping out your entire tech stack.

How Stablecoins Actually Work in Cross-Border Payments

The Blockchain Settlement Advantage

Stablecoins cut through the banking middleman problem with brutal simplicity. Instead of your payment bouncing through correspondent banks in New York, London, and Manila while each institution extracts fees, USDC moves directly on blockchain networks in minutes. The technical reason is straightforward: stablecoins are digital representations of value that settle on decentralized ledgers without requiring permission from any bank. When you send USDC from your account to a vendor in Brazil, that transaction hits the blockchain immediately, and the recipient converts it to Brazilian real within hours rather than waiting three to five business days.

The cost difference is staggering. A typical USDC transfer costs a few cents in network fees, versus the 3% to 6% you’d pay through traditional banking channels. For a $100,000 payment, that’s the difference between spending $5 and spending $5,000. This isn’t speculation about future potential-the BVNK 2026 Stablecoin Utility Report documents over $300 billion flowing through stablecoin payment and payroll channels across 15 countries, with adoption strongest in emerging markets where traditional remittance fees make cross-border transfers economically brutal.

Why USDC Dominates Global Payments

USDC specifically dominates this space because it combines institutional credibility with practical availability. Issued by Circle and fully backed by US dollar reserves, USDC trades on every major blockchain network including Ethereum, Solana, and Polygon, meaning your payment routes through whatever network offers the lowest fees that day. More importantly, USDC maintains a 1:1 peg to the US dollar, eliminating volatility concerns that plague other crypto assets-your vendor receives exactly the value you sent, with no surprise price swings between transaction and settlement.

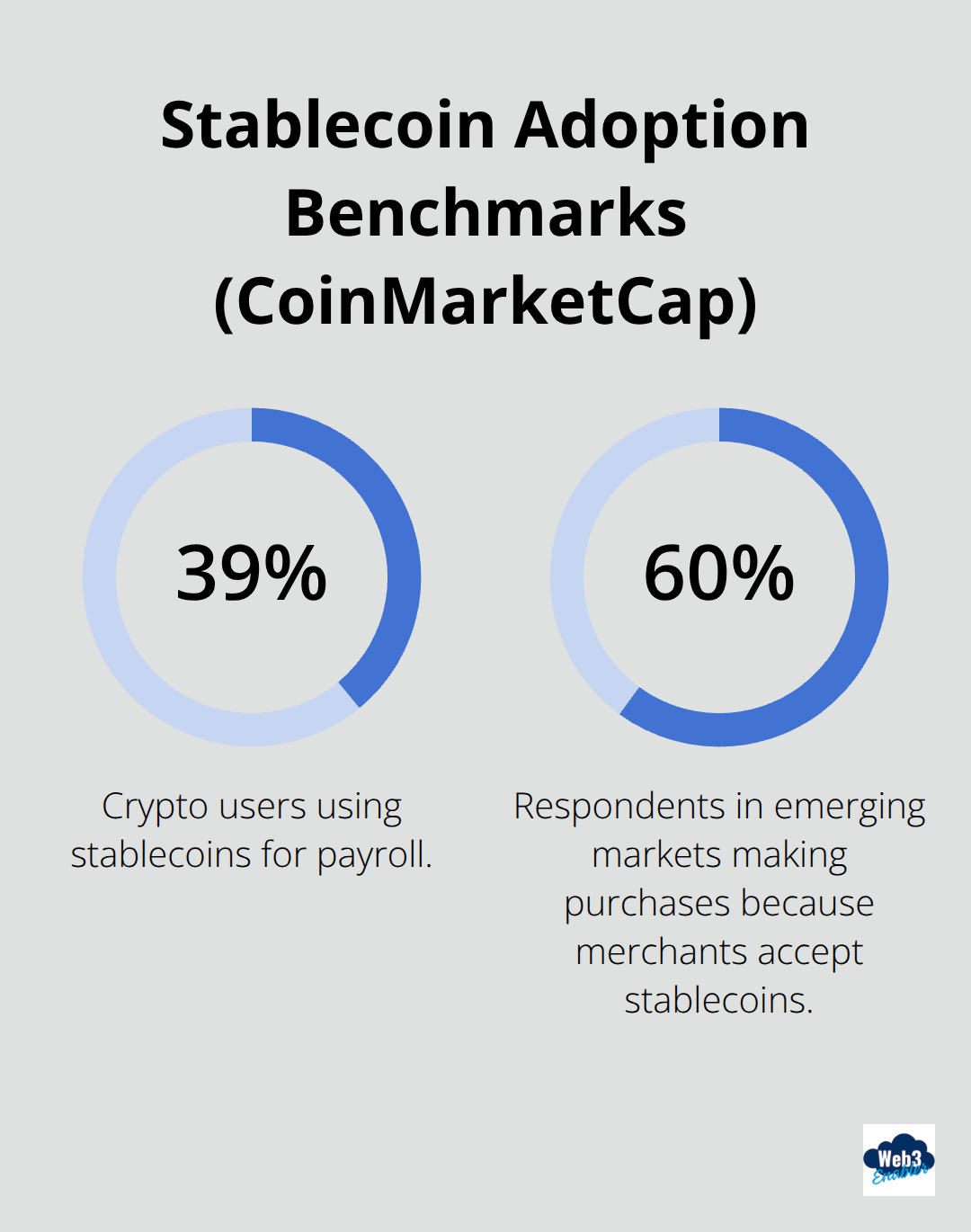

The ecosystem supporting USDC has matured rapidly. Major institutions like BlackRock now hold Circle equity, and stablecoin adoption in payroll already covers 39% of crypto users globally according to CoinMarketCap research, proving that real businesses trust USDC for mission-critical payments. Over half of respondents in a CoinMarketCap study made purchases specifically because merchants accepted stablecoin payments, with adoption rising to 60% in emerging markets.

Real-Time Visibility and Compliance Integration

When you build remittance infrastructure directly into systems like Salesforce, you gain real-time visibility into settlement status, automatic reconciliation against invoices, and compliance controls that traditional wire transfers never provided. A vendor payment that would normally take five days and cost thousands in fees now settles overnight for pocket change, and your finance team sees the transaction status in the same CRM interface they use daily.

This integration transforms how your business handles international payments. Your team no longer tracks remittances across separate banking portals, email confirmations, and spreadsheets. Instead, payment status flows directly into your existing workflows, reducing manual work and eliminating the delays that plague traditional systems. The compliance layer embeds automatically, capturing transaction records and verification data without requiring your team to manage separate audit trails.

Building these payment rails directly into your existing infrastructure means your business captures stablecoin’s speed and cost advantages without abandoning the systems your team already knows. This is where the real modernization happens-not by replacing Salesforce, but by extending it to handle cross-border payments the way the internet was designed to move value.

How to Actually Integrate USDC Into Your Salesforce Workflows

Your Salesforce instance already knows everything about your customers, invoices, and payment schedules. The missing piece is connecting that data to blockchain settlement rails so payments move at internet speed instead of banking speed. Web3 Enabler provides 100% Salesforce Native solutions specifically to solve this problem without forcing your team to learn crypto terminology or abandon the systems they use daily. When you integrate USDC remittance directly into Salesforce, your payment workflows stop being separate from your business operations and start being part of them.

Stop Managing Payments in Three Different Systems

Most businesses handle cross-border payments across banking portals, email confirmations, and spreadsheets that never talk to each other. Your accounts payable team initiates payments in one system, your finance team tracks them in another, and your compliance team scrambles to document everything afterward. This fragmentation creates delays, audit nightmares, and no visibility into where money actually sits during settlement.

When you integrate remittance infrastructure into Salesforce, your payment status lives in the same interface where your team manages customer records, invoices, and vendor relationships. A $50,000 vendor payment that traditionally takes five business days and costs $2,500 in fees now settles overnight for under $10, and your accounting team sees the settlement confirmation in the same CRM where they initiated the payment. You send USDC to a vendor in Mexico, that transaction appears directly in their customer record, automatically reconciles against the invoice it paid, and creates an immutable audit trail without your team doing extra work.

Compliance Automation Replaces Manual Gatekeeping

Cross-border payments trigger compliance requirements that most businesses handle through manual review processes, email chains, and external compliance platforms. Your team must verify vendor identity, screen against sanctions lists, document transaction purpose, and maintain records that regulators might request years later. These steps add days to settlement timelines and create bottlenecks that make faster payments feel risky.

When you integrate USDC remittance into Salesforce, compliance controls embed directly into the payment workflow rather than existing as separate checkpoints. The system automatically screens beneficiaries against current sanctions lists before payment execution, captures KYC verification data that satisfies regulatory requirements across multiple jurisdictions, and maintains transaction records on an immutable ledger that auditors can verify instantly. Smart contracts encode your specific compliance rules so that payments execute only when all conditions are met, eliminating manual approval delays that slow traditional wires. A multinational business sending payroll to distributed teams across 12 countries no longer needs to maintain separate compliance documentation for each corridor or wait for manual review before each payment. Instead, the system automatically applies the appropriate regulatory framework based on payment destination, verifies all conditions are satisfied, and executes settlement within hours while actually strengthening your compliance posture because everything is documented and verifiable rather than buried in email threads.

Connect Every Payment Network Your Business Actually Uses

Global payment infrastructure fragmented long ago. Your business might use correspondent banking for some corridors, SWIFT GPI for others, and emerging market payment networks for regions where traditional banking barely functions. Rather than forcing you to choose one system, Salesforce-native remittance infrastructure connects to whatever payment networks serve your specific corridors. USDC trades on Ethereum, Solana, and Polygon, meaning your payment can route through whichever blockchain offers the lowest fees that day while your team never thinks about network selection.

For corridors where local currency requirements exist, the system integrates with liquidity providers who convert USDC to Brazilian real, Philippine peso, or Mexican peso at transparent rates that beat traditional FX spreads. A business sending vendor payments across Latin America, Southeast Asia, and Africa no longer needs separate banking relationships or payment infrastructure for each region. Instead, USDC remittance infrastructure handles all corridors through a single integration that your Salesforce team manages from one dashboard. The cross-border payments market continues to expand, and that growth will favor infrastructure that handles multiple corridors efficiently rather than forcing businesses to maintain separate systems for each region.

FAQ: USDC Remittance in Salesforce

How much can my business save on international wire fees with USDC?

Traditional cross-border wires typically cost between 1% and 6% in total fees when accounting for wire charges and currency spreads. For a business moving 10 million dollars annually, those fees can reach 600,000 dollars. By switching to USDC remittance rails, those costs can drop to as little as 5,000 dollars because you eliminate the layers of correspondent banks and intermediary currency desks.

How does USDC settlement speed compare to traditional correspondent banking?

While traditional bank transfers often take three to five business days to settle—longer if interrupted by holidays or weekends—USDC settles in minutes. This speed allows your business to avoid the settlement time trap, meaning you no longer have to tie up capital or pre-fund accounts in multiple currencies just to keep international operations moving.

Is USDC remittance compliant with current 2026 regulations?

Yes. Regulatory frameworks like the CLARITY Act have provided the oversight necessary for institutional adoption. When integrated directly into Salesforce, the system automatically screens beneficiaries against sanctions lists and captures KYC data. Every transaction is recorded on an immutable ledger, creating a permanent audit trail that is much easier for auditors to verify than fragmented banking portals and email threads.

Do I need to use external crypto platforms to manage these payments?

No. Web3 Enabler offers 100% Salesforce Native solutions. This allows your accounts payable and finance teams to initiate, track, and reconcile international payments without ever leaving the CRM. All payment data lives in the same customer or vendor records you already manage, ensuring your infrastructure stays unified rather than fragmented across different systems.

Which blockchain networks are used for these remittances?

USDC is available across multiple major networks including Ethereum, Solana, and Polygon. A Salesforce-native integration can automatically route payments through whichever network offers the lowest fees and fastest speeds on that specific day. This ensures your business captures the best possible rates without requiring your team to have deep technical knowledge of blockchain infrastructure.

Final Thoughts

Your business has paid for slow, expensive cross-border payments because that’s how banking worked when your infrastructure was built. But the infrastructure has changed-stablecoins like USDC now process over $300 billion annually through payment and payroll channels, proving that faster, cheaper settlement is operational reality your competitors already use. For a business moving $10 million annually across borders, USDC remittance Salesforce solutions cut your fees from $600,000 to $5,000 while settling in hours instead of days.

Institutional adoption accelerates rapidly as BlackRock holds Circle equity, Morgan Stanley files for Bitcoin and Solana ETFs, and regulatory frameworks like the CLARITY Act arrive to clarify oversight. These developments signal that blockchain infrastructure becomes corporate infrastructure, not that crypto becomes mainstream. The businesses that integrate stablecoin rails into their existing systems now will operate at a cost and speed advantage that competitors struggle to match as adoption spreads.

Web3 Enabler provides 100% Salesforce Native solutions that connect blockchain settlement directly to your existing workflows without forcing your team to abandon the systems they already know. Start with one corridor where cost savings are most obvious, prove the model works, then expand to other regions-the infrastructure is ready and your competitors are moving.