Your business probably sends money across borders or handles payments in ways that feel stuck in the 1990s. USDC payments offer a faster, cheaper alternative that actually works in the real world.

We at Web3 Enabler have watched companies waste time and money on traditional payment rails. This guide walks you through the entire USDC payments process-from setup to settlement-so you can move money like it’s 2026.

What USDC Actually Is

USDC is a stablecoin-a digital token pegged 1:1 to the US dollar and backed by audited reserves. Unlike Bitcoin or Ethereum, which swing wildly in price, USDC stays flat. You send $100 USDC today and the recipient gets exactly $100 worth tomorrow, not $87 or $156. This stability matters because businesses need predictable prices, not casino dynamics. USDC lives on blockchains like Ethereum, Solana, and Stellar, which means it moves without banks, wire delays, or middlemen taking cuts.

How USDC Stacks Up Against Traditional Crypto

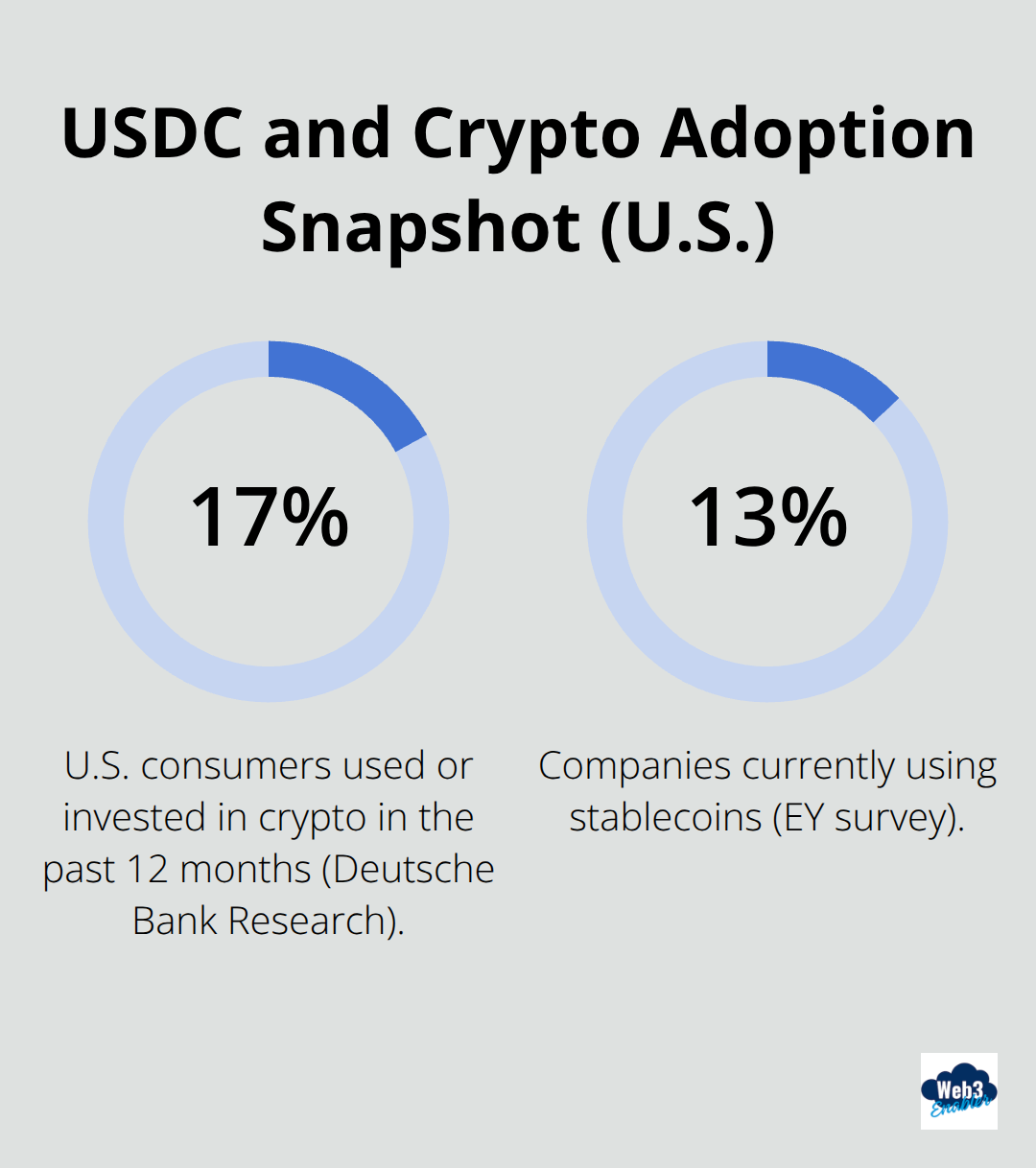

Deutsche Bank Research found that 17% of US consumers have already used or invested in crypto in the past 12 months, but adoption among corporations is still climbing. An EY survey revealed only 13% of companies currently use stablecoins, yet more than 50% expect to adopt within 6 to 12 months. That gap between early movers and everyone else is where real advantage lives right now.

USDC differs fundamentally from Bitcoin or Ethereum because it maintains a fixed price. Traders speculate on crypto volatility; businesses need payment certainty.

Why USDC Beats Your Current Payment Setup

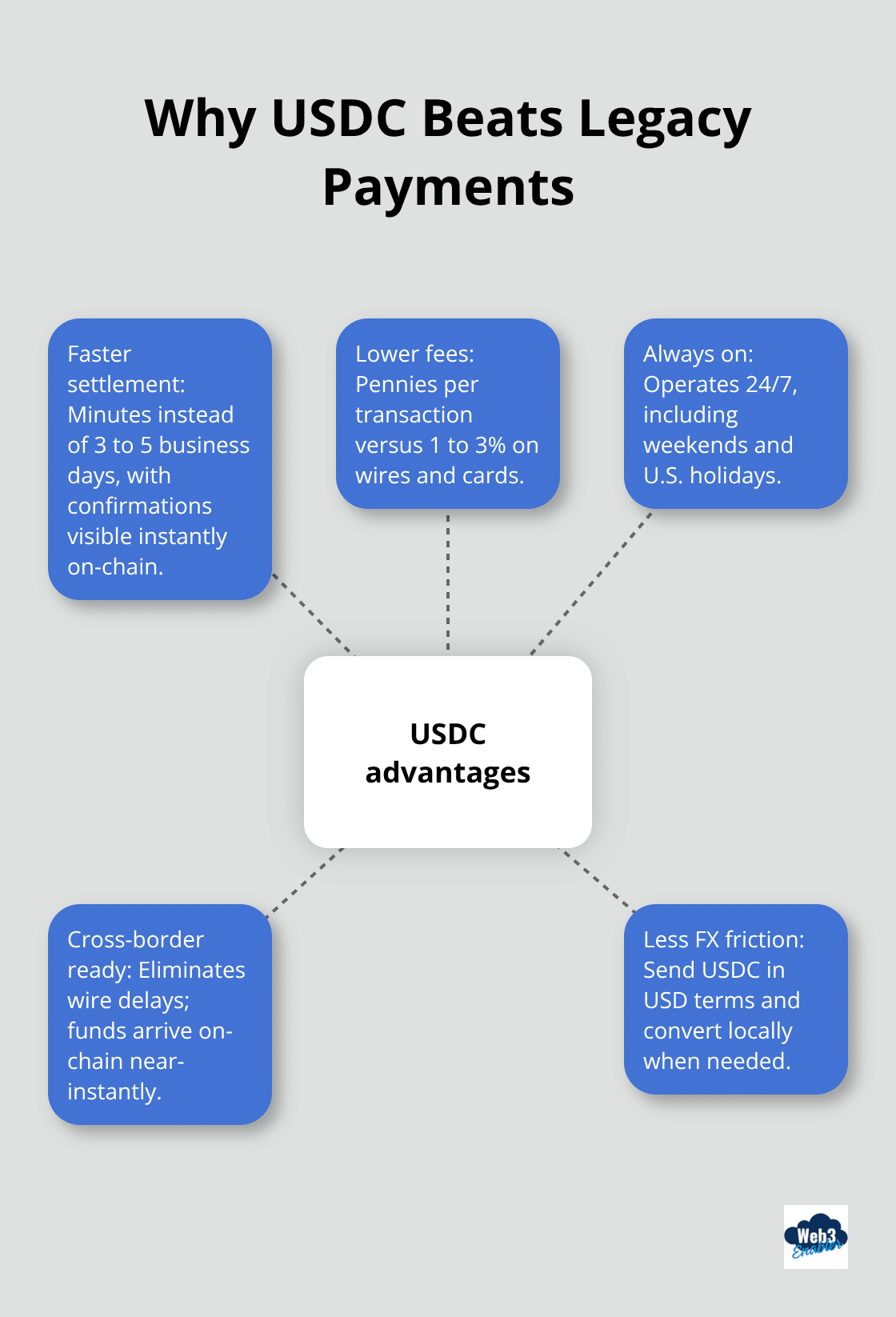

Your business probably uses ACH transfers, wire services, or international payment platforms that take 3 to 5 business days and charge 1 to 3% in fees. USDC settles in minutes, costs pennies, and works 24/7-even on weekends and holidays when banks are closed. For cross-border B2B payables, that speed matters. A company paying contractors in Southeast Asia no longer waits for the wire to clear; the payment arrives instantly on-chain.

Stablecoins also sidestep currency conversion friction. Instead of converting USD to local currency through multiple intermediaries, you send USDC directly and let the recipient convert at their preferred exchange. Ernst & Young’s surveys suggest that stablecoins may account for 5–10% of cross-border payment value by 2030 ($2.1–$4.2 trillion), and early adopters already capture operational wins. One practical advantage: USDC works in regions with weak banking infrastructure. A business paying suppliers in high-inflation countries can use stablecoins to bypass local currency risk entirely. The recipient holds USD-equivalent value instead of watching their local currency erode.

The Compliance Reality You Actually Need to Know

USDC isn’t a regulatory free-pass. The GENIUS Act, passed in July 2025, established clear rules: issuers must maintain 1:1 reserves, undergo audits, and comply with anti-money laundering controls like traditional financial institutions. Circle, the company behind USDC, holds national trust charters and follows strict reserve practices. That transparency matters for your business because it means USDC has institutional backing, not some mystery issuer.

When you accept USDC payments, you take responsibility for basic KYC-knowing who your customer is-just like with wire transfers. If you use a provider like Stripe, they handle the compliance heavy lifting; if you accept payments directly into your wallet, you need your own controls. The regulatory landscape keeps tightening, which actually works in your favor. Established issuers with proper oversight become the default, and fly-by-night stablecoins get squeezed out. For your business, that means choosing Circle-backed USDC over untested alternatives is the practical move.

Now that you understand what USDC is and why it matters, the next step involves actually getting it into your business operations-which means integrating it with your existing systems without blowing up your current setup.

Getting USDC Into Your Systems Without Breaking Anything

Start With Your Current Setup

Integrating USDC payments into your existing business infrastructure sounds like a technical nightmare, but the reality is far simpler than you’d expect. Most companies don’t need to rip out their current systems; they add USDC alongside them. If you use Stripe, you’re already halfway there-Stripe Payments accepts stablecoins and settles directly to your fiat balance, meaning your accounting team sees normal USD deposits without touching blockchain infrastructure. For businesses running on Salesforce, Web3 Enabler provides 100% Salesforce Native solutions that plug directly into your existing workflows, letting you accept USDC payments and track them in the same CRM your sales team already uses daily.

The integration approach depends on your risk tolerance. High-volume merchants often choose a payment processor that handles the on-chain complexity; smaller operations or those with technical teams might accept USDC directly into their own wallets and manage the conversion themselves. Direct wallet acceptance means faster settlement-you skip the processor’s fee layer entirely-but you own the custody responsibility.

Move Fast With Real-World Proof

Early movers are already capturing operational wins. One DeFi protocol manages roughly $30,000 monthly across cloud infrastructure using stablecoin cards funded from USDC holdings, avoiding traditional wire delays entirely. Testing matters more than the choice itself-spin up a test transaction on Stellar or Solana, watch it settle in seconds, then decide whether your business needs that speed advantage.

Build Compliance Into Your Foundation

Compliance and security aren’t obstacles; they’re the foundation that lets you move fast without legal headaches. The GENIUS Act, passed in July 2025, treats stablecoin issuers like Circle as federal financial institutions, which means they follow the same AML and KYC rules as banks. Your business responsibility is straightforward: know your customers and maintain audit trails. If a customer sends you USDC, you link their wallet address to their identity just like you’d verify a wire transfer.

Circle holds national trust charters and undergoes regular audits-you’re not trusting a startup, you’re trusting an entity with Federal Reserve oversight. For direct stablecoin acceptance, maintain records of every transaction, monitor sanctions lists using tools like Chainalysis or TRM Labs, and document customer identity.

Many businesses use middleware providers like Stripe or Fireblocks that handle this automatically, charging a small fee in exchange for compliance infrastructure you don’t have to build yourself. The regulatory landscape tightens every quarter, but that works in your favor-fly-by-night stablecoins get squeezed out, and established players like USDC become the only sensible choice.

Protect Your Keys and Transactions

Security best practices are equally practical: never hold private keys in hot wallets exposed to the internet, use hardware wallets or custody providers for amounts above your daily operating threshold, and enable multi-signature controls so no single person can move large sums. One technical practice that works across blockchains: use atomic transactions on Stellar or similar networks, which guarantee that both your merchant payment and any platform fee execute together or fail entirely-no partial transfers that leave money stranded.

If you accept USDC from customers, rotate receiving wallet addresses monthly and audit your transaction logs quarterly against your accounting records. Most security breaches happen not from blockchain vulnerabilities but from sloppy key management or phishing attacks targeting employees, so train your team to treat wallet access like root server access.

With your systems integrated and security locked down, the actual payment workflow becomes straightforward-and that’s where the real speed advantage shows up.

How USDC Payments Actually Move Through Your Business

Initiating a USDC Payment

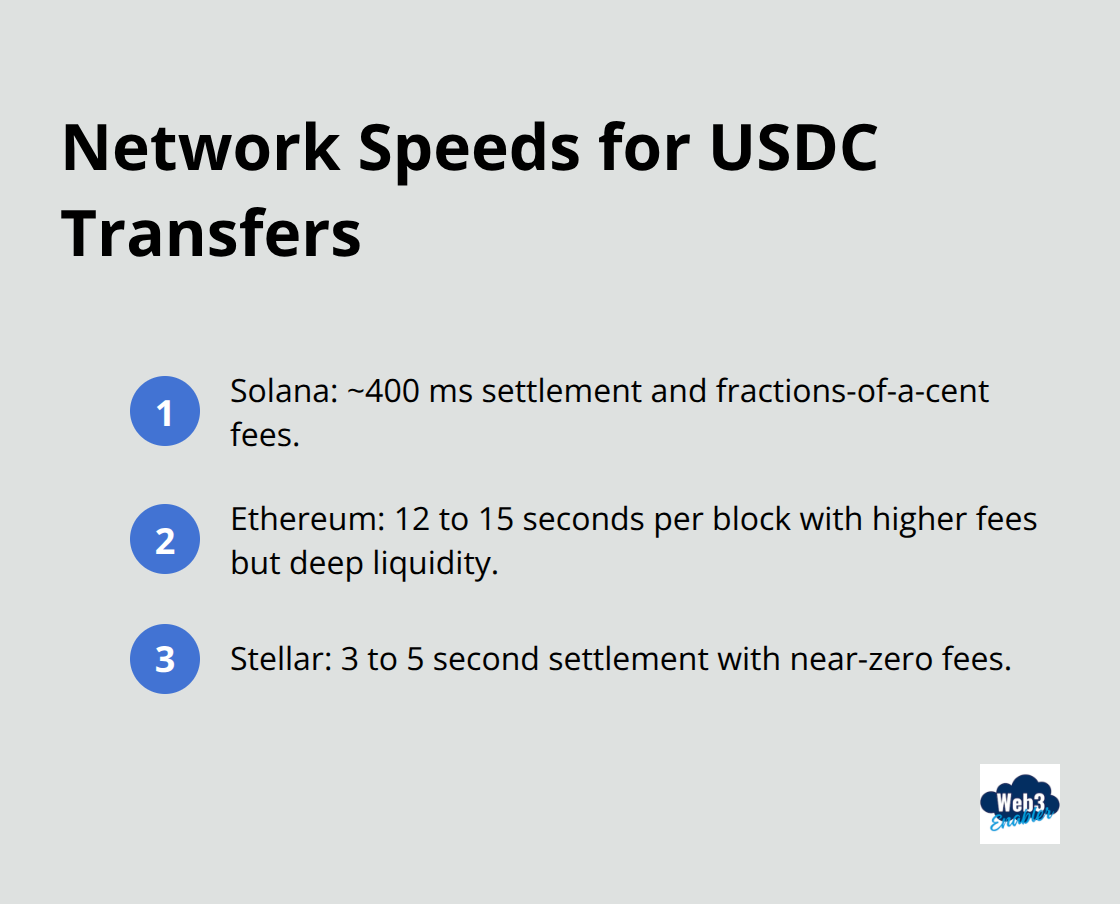

A USDC payment starts the moment someone initiates a transfer from their wallet or payment interface. The payer specifies the recipient’s wallet address, the amount in USDC, and which blockchain they’re using-Ethereum, Solana, or Stellar each have different speed and cost profiles. Solana settles transactions in roughly 400 milliseconds and costs fractions of a cent, making it ideal for high-volume operations. Ethereum takes 12 to 15 seconds per block and costs slightly more, but offers the deepest liquidity and integration with existing DeFi infrastructure. Stellar, designed specifically for payments, processes transactions in 3 to 5 seconds with near-zero fees, making it the practical choice for B2B cross-border flows.

Once the payer submits the transaction, it enters the blockchain’s mempool-essentially a waiting room where validators check that the sender actually owns the USDC and has sufficient balance. This verification happens automatically; no bank teller reviews it.

Confirmation and Finality

Within seconds to minutes depending on the network, validators confirm the transaction and add it to a new block. At this point, the payment is final. Unlike wire transfers that banks can reverse days later, USDC transactions are irreversible once confirmed-which means accuracy matters on the front end, not the back end. The moment a transaction confirms on-chain, both parties see it instantly. Your accounting system should reflect this immediately rather than waiting for a three-day clearing period.

Settlement Options for Your Business

If you use Stripe or a similar processor, they handle the on-chain settlement and automatically deposit USD into your business bank account within 24 hours, giving you the speed benefit without blockchain complexity. For direct wallet acceptance, you own the settlement timing-you can convert USDC to fiat on an exchange like Kraken or Coinbase within minutes if you need immediate USD, or hold USDC in your treasury if you’re paying vendors who accept it.

Reconciliation and Accounting Integration

The reconciliation piece is where most businesses stumble, but it’s actually straightforward if you approach it systematically. Every USDC transaction generates a transaction hash-a unique identifier on the blockchain-that you can cross-reference with your accounting records. Tools like Xero and QuickBooks now integrate with blockchain data providers, allowing you to automatically match on-chain transactions to invoice records without manual entry. One DeFi protocol managing $30,000 monthly across cloud infrastructure uses this approach: they fund virtual cards from their USDC treasury, and the card provider automatically reconciles expenses against their wallet activity.

Building Your Audit Trail

Treat blockchain transactions like any other payment method-document the wallet addresses of your counterparties, timestamp every transfer, and audit monthly against your general ledger. If you accept USDC from customers, maintain a record linking each wallet address to the customer’s legal identity for compliance purposes (this protects you if regulators ask questions and makes tax reporting straightforward when accountants need to calculate gains or losses on currency conversion).

FAQ: Moving to USDC Payments in 2026

What is the GENIUS Act, and how does it protect my business?

The GENIUS Act (passed July 2025) was the watershed moment for stablecoins in the U.S. It established that issuers like Circle must maintain 1:1 reserves in liquid U.S. treasuries and cash, subject to federal audits. For your business, this means USDC is no longer a “crypto experiment”—it is a federally regulated financial instrument. You get the speed of a blockchain with the institutional safety of a national trust.

How fast do USDC payments actually settle compared to a bank wire?

Traditional SWIFT or ACH transfers are limited by banking hours, holidays, and the “hand-off” between intermediary banks, often taking 3–5 days. USDC is 24/7/365.

- Solana: Settles in roughly 400 milliseconds.

- Stellar: Processes in 3–5 seconds.

- Ethereum: Takes about 15 seconds. In short: your recipient can have spendable funds before you’ve finished typing the “payment sent” email.

Do I need to manage private keys to accept USDC?

Not necessarily. While “direct wallet acceptance” gives you the most control and lowest fees, many businesses prefer custodial or hybrid solutions. If you use a processor like Stripe or a Salesforce-native tool like Web3 Enabler, the complexity is abstracted away. You can accept USDC from a client, and the system can automatically convert it to USD and deposit it into your bank account, so your finance team never has to touch a “seed phrase.”

What are the actual cost savings on a $100,000 international payment?

Traditional international wires typically involve a $30–$50 flat fee plus a 1% to 3% currency conversion markup. On $100,000, you’re losing between $1,000 and $3,050. With USDC on a network like Solana or Stellar, the network fee is less than $0.01. Even with a small off-ramp fee to convert back to local fiat, your total cost is usually under 0.1% to 0.5%, saving your business thousands of dollars per transaction.

How does USDC reconciliation work inside Salesforce?

This is where Web3 Enabler shines. Every USDC transaction generates a unique on-chain hash. Our integration maps that hash directly to your Salesforce records (Opportunities, Invoices, or Accounts). Because the blockchain is an immutable ledger, the reconciliation is “auto-verified”—the system confirms the funds arrived at the exact block height and updates the status in your CRM in real time, eliminating manual spreadsheet matching.

Final Thoughts

USDC payments process fundamentally changes how your business moves money across borders and time zones. Settlement happens in minutes instead of days, compliance builds in from the start rather than after the fact, and the GENIUS Act actually works in your favor by eliminating sketchy issuers and leaving Circle-backed USDC as the institutional standard. Companies paying global teams, managing cross-border B2B payables, or operating in high-inflation regions already capture real operational advantages.

Starting requires far less effort than you’d expect. If you use Stripe, stablecoin payments integrate without touching your existing infrastructure; if you want direct wallet acceptance, test a small transaction on Solana or Stellar first and watch it settle in seconds. The compliance piece isn’t optional, but it’s straightforward: know your customers, maintain audit trails, and use established providers like Circle.

The decision matters less than taking action. Early movers already capture competitive advantage, and waiting another year means watching your competitors settle payments faster and cheaper than you do. We at Web3 Enabler help businesses connect blockchain technology to existing systems without ripping out infrastructure, and our Salesforce Native solutions let you accept USDC payments and track them in the CRM your team already uses daily-explore how Web3 Enabler can accelerate your adoption.