Accepting SEPA to Brazil payments sounds straightforward until you hit the reality: correspondent banking delays, FX volatility, and reconciliation nightmares. Most companies struggle because they treat European and Brazilian payment rails the same way.

We at Web3 Enabler built this guide to show you exactly how to move EUR into Brazil, convert to BRL, and keep your ledgers clean in Salesforce. You’ll learn the practical steps that actually work.

SEPA and Brazil: Two Completely Different Payment Worlds

Understanding SEPA’s Unified Infrastructure

SEPA payments operate within a unified European infrastructure where 36 countries share standardized rails, minimal friction, and settlement within hours or seconds. A SEPA transfer from France to Germany moves through a single regulatory zone with harmonized compliance rules, predictable fees under €0.50, and next-day settlement as standard. SEPA Instant transfers settle in under 10 seconds under EU Regulation 2024/886, but that speed vanishes the moment you cross the Atlantic.

Brazil operates on entirely different infrastructure. Domestic payments run through PIX, which settled 37.6 billion transactions in 2024 and processes transfers 24/7 in seconds with near-zero fees for individuals. When a European customer sends you EUR via SEPA, that payment arrives at a European bank account, not directly into Brazil. With Blockchain Payments and Virtual-on-ramps, that bank account can send stablecoins like USDC directly to your wallet. That wallet can even off-ramp, via PIX, directly to your Brazilian bank account.

The EUR-to-BRL Conversion Problem

You then face a separate problem: converting EUR to BRL and moving the funds across borders through correspondent banking, which introduces delays, multiple intermediaries, and FX volatility that don’t exist within SEPA’s closed ecosystem. A correspondent banking route from Europe to Brazil typically involves your European bank, one or more intermediary banks, and finally a Brazilian bank, with each hop adding 1–3 business days and fees ranging from €15 to €50 per transaction.

When a customer sends you a SEPA payment, the EUR lands in your European account first. You cannot receive SEPA directly into a Brazilian bank account because SEPA operates only within the European economic area. Your European bank then initiates a separate cross-border wire to Brazil, converting EUR to BRL at whatever rate your bank offers, which typically includes a 1–3% FX spread above the interbank rate.

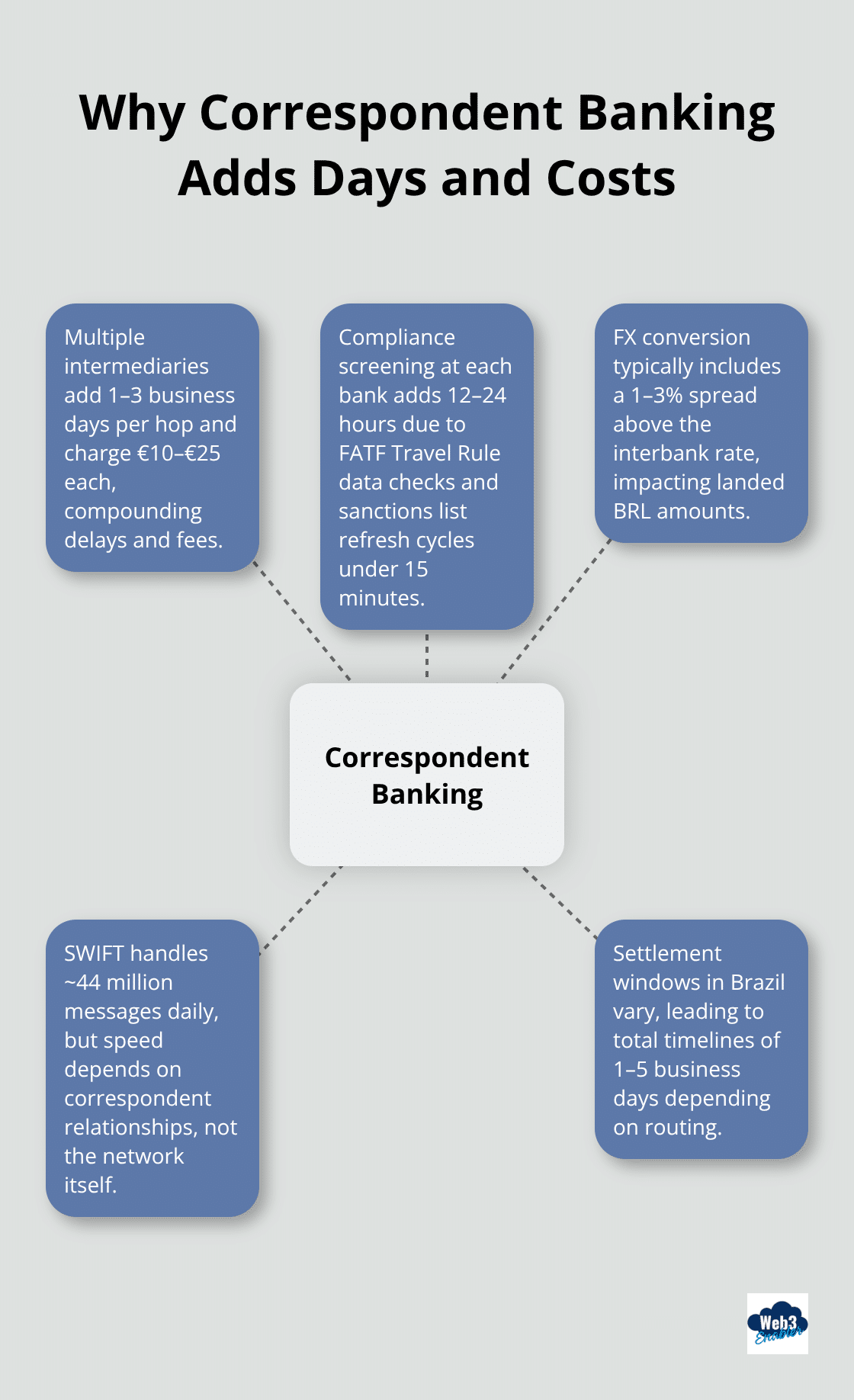

Settlement in Brazil takes 1–5 business days depending on correspondent bank routing and whether the Brazilian receiving bank participates in faster clearing windows. Most correspondent routes still rely on SWIFT, which processes roughly 44 million messages daily but doesn’t guarantee speed. Real-time payment visibility is rare in this flow, meaning you won’t know if funds arrived until settlement completes.

With Stablecoin solutions, the costs per transactions is pennies, and the on-ramp and FX charges are usually fractions of a percent.

European customer sends EUR to an on-ramp bank account, EUR is converted to USDC, USDC is sent to your wallet, and the USDC is off-ramped into your bank account.

Why Correspondent Banking Adds Days and Costs

Correspondent banking is the standard method for cross-border transfers between Europe and Brazil because no single bank operates in both regions with full settlement capability. Your European bank sends the SEPA-initiated wire to a correspondent bank in the US or Europe that has a relationship with a Brazilian bank, which then credits your final destination account. Each correspondent takes a fee, typically €10–€25, and adds processing time.

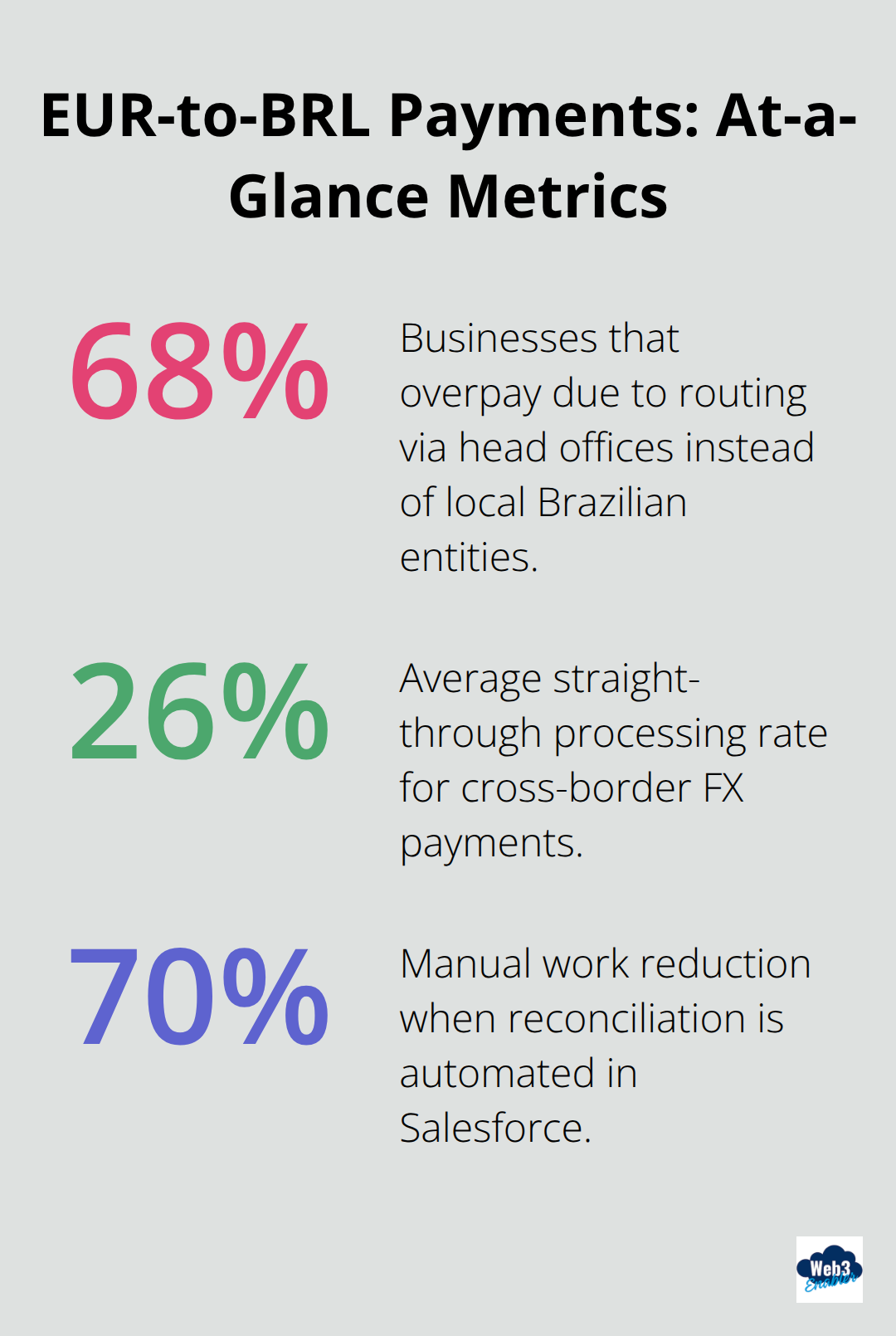

The FATF Travel Rule requires complete originator and beneficiary information across all hops, and compliance screening at each correspondent adds another 12–24 hours because banks must screen customer details against 215+ sanctions regimes with list refresh cycles under 15 minutes. About 68% of businesses report paying unnecessarily high fees because they route payments through head offices instead of local entities in Brazil, according to FXC Intelligence 2025.

Maintaining Separate Operational Workflows

Companies accepting SEPA into Brazil must maintain separate operational workflows: one for SEPA receipt in Europe and another for FX conversion and BRL settlement. The straight-through processing rate for cross-border FX payments averages 26%, according to LexisNexis 2024 data, meaning 74% of transactions require manual intervention, delays, or exception handling.

If you have a local BRL account in Brazil, routing directly to that account reduces intermediaries, but you still face the FX conversion decision: convert in Europe before sending, or receive USD and convert in Brazil. Conversion in Europe locks in a rate immediately but may be unfavorable. Conversion in Brazil delays the rate lock until settlement arrives, exposing you to FX movement but potentially capturing better rates if BRL strengthens. Neither option is free.

Stablecoins solve all of this with fast, near instantaneous low-fee payments.

Moving Forward with Cross-Border Payments

The correspondent route is not optional-it’s the only way to move EUR from Europe to Brazil at scale-but understanding its mechanics helps you negotiate better fees and timing with your banks. This complexity is exactly why setting up proper FX conversion processes and settlement timelines requires careful planning, which we’ll address in the next section.

Building Your EUR-to-BRL Corridor

Managing FX Conversion Timing and Rates

FX conversion timing and rate management are the second critical variable. You face two core decisions: convert EUR to BRL in Europe before sending, or receive funds in a holding currency and convert in Brazil. Converting in Europe locks in a rate immediately through your European bank’s FX desk, typically at a 1–3% spread above the interbank rate, but you lose optionality if BRL strengthens between conversion and settlement.

Converting in Brazil delays the rate lock until funds arrive (usually 2–5 business days later), exposing you to FX movement but potentially capturing better rates. The straight-through processing rate for cross-border FX payments averages only 26% according to LexisNexis 2024, meaning most transactions require manual intervention or exception handling, which compounds delays.

Try locking the rate at the moment the customer commits to payment, not when settlement completes. Ask your European bank for a forward FX contract that fixes the EUR-to-BRL rate for 5–10 business days, giving you certainty while the correspondent route executes. This costs slightly more than spot conversion but eliminates the risk that your margin evaporates during settlement delays.

Accelerating Settlement Through Local Rails

Settlement timelines in Brazil typically run 1–5 business days depending on correspondent routing and whether the receiving bank participates in faster clearing windows. Most correspondent routes still rely on SWIFT messaging without real-time visibility, so you won’t know if funds arrived until settlement is confirmed. Regulatory requirements add complexity: the FATF Travel Rule requires complete originator and beneficiary information across all correspondent hops, and EU Regulation 2024/886 mandates daily customer-level screening for EU-originated sanctions compliance.

If your Brazilian receiving bank participates in PIX, you can request that the correspondent convert to BRL and then push funds through PIX for immediate final settlement, which accelerates the last mile to seconds instead of days. This requires coordination with both your European bank and your Brazilian bank, but it has become increasingly standard practice for payments over €10,000.

Once funds settle in your Brazilian BRL account, you need visibility into the transaction status and the ability to reconcile across your ledger systems. The next section covers how to track these payments in real time and automate reconciliation workflows within Salesforce Financial Services Cloud, ensuring your finance team stays informed throughout the entire EUR-to-BRL journey.

Tracking EUR-to-BRL Payments in Real Time

Blockchain Payments, with Revenue Cloud and Sales Cloud Addons

Mapping SEPA Payments to Salesforce Payment Objects

With Blockchain Payments, your European on-ramp is in your client’s name. They KYC and Virtual On Ramp are created in your Salesforce Org but on behalf of the Client, with information attached to their account. When they sent a EUR SEPA payment, it reaches this on-ramp account that is then on-ramped to stablecoins, USDC, USDT, or EURC.

Those Virtual On-ramps have a target wallet, and the stablecoins are directed to that target wallet. The target wallet is a walled belonging to your company. As soon as their currency is on-ramped, it is directed to you and you have received the payment.

With a liquidation wallet, those stablecoins are automatically sold and off-ramped to your bank account. Via PIX, you receive Brazilian Real in your bank account.

The whole project is automated, ith the entire data flow stored in Salesforce, easily reportable and auditable.

Automating Settlement and Reconciliation Workflows

When payment arrives in your wallet, the information, including the Payment record is created in Salesforce. Via Flow, Zapier, or Mulesoft, this information is pushed to your Brazilian ledger with the converted BRL amount, settlement timestamp, and fees deducted. Your reconciliation process then starts with data already aligned across geographies.

Building Immutable Audit Trails for Compliance

Audit trail creation happens automatically through Salesforce’s Change Data Capture feature, which logs every update to Payment records, including who changed what, when, and why. This creates an immutable record that satisfies regulatory examination requirements for cross-border transaction documentation. Every correspondent screening decision, FX rate adjustment, and settlement confirmation appears in the audit trail, giving compliance teams the evidence they need during regulatory reviews.

Separating FX P&L from Operational Performance

For multi-currency transactions, store the spot FX rate, forward contract rate (if used), and settlement rate all within the Payment record so your finance team can analyze FX P&L separately from operational P&L. This separation gives management visibility into whether your FX strategy actually protects margins or erodes them. You can then adjust your forward contract strategy based on actual performance data rather than guessing.

Accelerating Month-End Close with Automated GL Posts

Assign each Payment record to a specific GL account code for BRL receipts in Brazil, and configure an automated GL post that fires the moment reconciliation completes. This eliminates the manual journal entry step entirely and accelerates your month-end close by 2–3 days. Your finance team no longer waits for settlement confirmation to begin close procedures; the system posts to GL automatically once matching completes and discrepancies are resolved.

Final Thoughts

Direct correspondent relationships with your European bank save €15–€25 per transaction and eliminate unnecessary intermediary delays that most companies accept without question. Lock your FX rate forward rather than converting at settlement, protecting your margin from BRL volatility during the 2–5 day correspondent window. Automate your reconciliation in Salesforce Financial Services Cloud instead of tracking payments across spreadsheets and email confirmations, reducing manual work by 70% and accelerating month-end close by 2–3 days.

Stablecoins make this fast, easy, and lower cost.

Blockchain Payments makes stablecoins easy.