Crypto payments are reshaping how businesses operate across the Middle East, but navigating this landscape requires more than enthusiasm-it demands clarity on regulations, technical setup, and practical execution.

We at Web3 Enabler have created this guide to help you understand exactly what’s needed to accept Middle East crypto payments, from compliance requirements in the UAE and Saudi Arabia to real-world implementation across e-commerce, hospitality, and real estate.

Legal and Regulatory Framework for Crypto Payments in GCC and Levant

The regulatory environment across the GCC has shifted dramatically toward structured frameworks rather than blanket prohibitions. UAE’s Virtual Assets Regulatory Authority (VARA) established clear licensing pathways for crypto service providers, making it the most accessible market in the region for businesses accepting digital payments. Saudi Arabia’s Central Bank (SAMA) runs fintech sandboxes that allow controlled crypto experiments, signaling openness to innovation within defined boundaries. Bahrain’s Central Bank licensed crypto exchanges directly-the Bank of Bahrain and Kuwait’s partnership with Binance Bahrain embeds crypto-as-a-service into banking apps through white-label APIs. This shift means you operate within frameworks designed to protect both businesses and customers, not in legal gray zones. The practical implication is straightforward: partner only with payment processors licensed or registered under these authorities. A processor with VARA registration in the UAE carries legal weight and reduces your exposure to frozen funds or compliance violations.

Evaluating Payment Partner Credentials

When you evaluate payment partners, request proof of licensing and regulatory standing before integration. The cost of compliance upfront is far lower than the cost of regulatory action afterward. Ask your processor for documentation of their regulatory status in each jurisdiction where you operate. Processors that hesitate to provide this information should raise immediate red flags. You can verify VARA registrations through the UAE’s official registry, and you can confirm SAMA sandbox participation through public announcements. This due diligence takes hours but protects your business from months of disruption.

What Levant Markets Require

The Levant presents a more fragmented picture than the GCC, with no unified regulatory body governing crypto payments. However, this does not mean operating there is impossible. Lebanon’s banking crisis has created demand for crypto-based alternatives, though the legal status remains ambiguous. Jordan and the Palestinian territories lack explicit crypto regulations but also lack explicit prohibitions, creating a de facto tolerance for non-bank crypto activity. Egypt’s Central Bank has cautiously permitted crypto transactions for remittances, recognizing the practical need for alternative payment channels. The practical approach in Levant markets is to focus on remittances and cross-border transfers rather than domestic commerce. These corridors have documented demand and regulatory acceptance.

Stablecoin Corridors and Custody Standards

Use regulated stablecoin corridors like USDT and USDC, which operate across most Levant jurisdictions without triggering banking restrictions. Work with custodians holding international licenses (Fireblocks, BitGo, or Crassula) rather than local operators with unclear standing. For AML and KYC compliance, implement travel rule adherence through your payment processor to meet international standards, even where local rules remain undefined. This positions you ahead of future regulation rather than behind it.

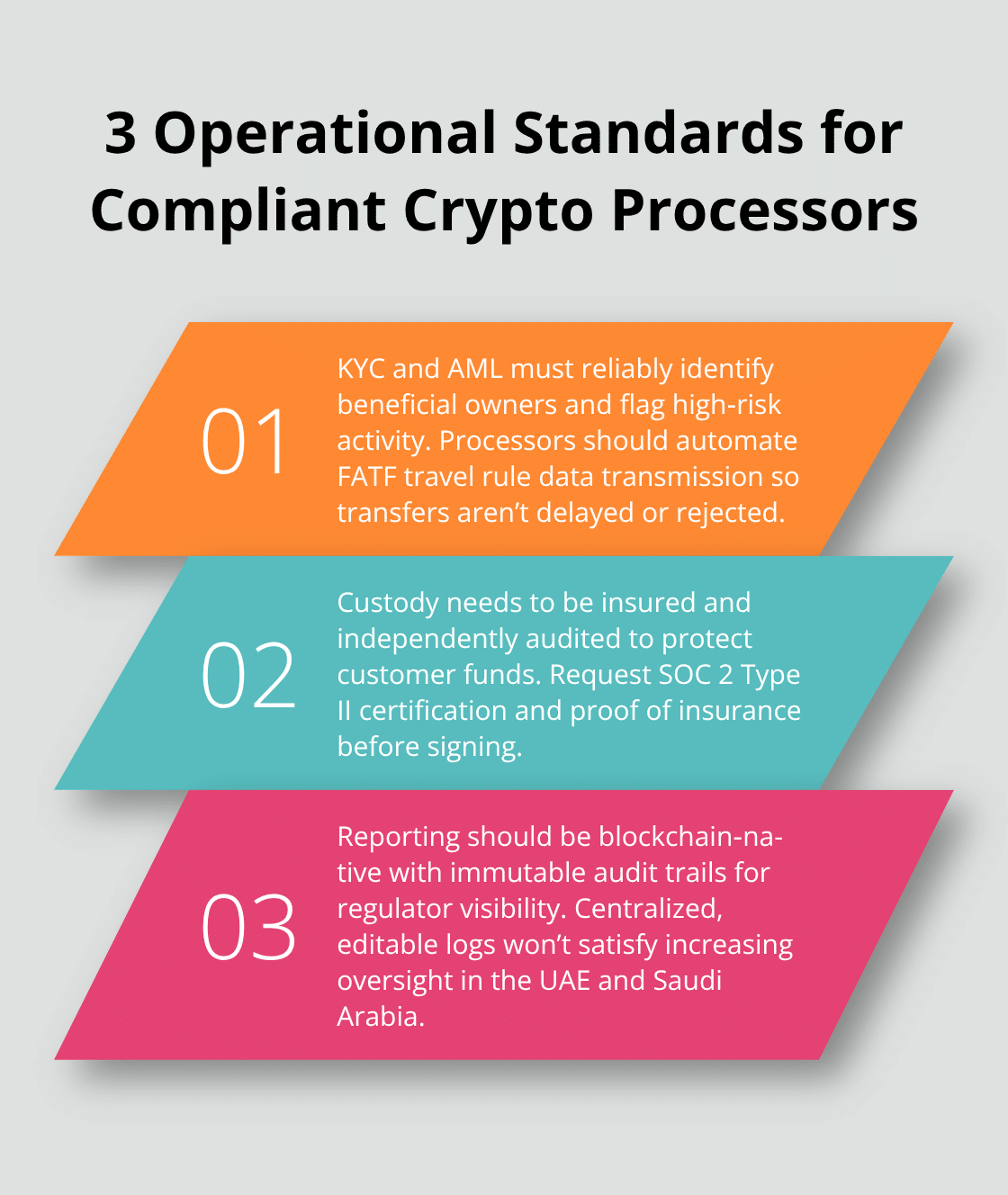

Three Operational Standards That Separate Compliant Processors

Regardless of jurisdiction, three operational standards separate compliant processors from risky ones. First, KYC and AML controls must be robust enough to identify beneficial ownership and flag high-risk transactions. The Financial Action Task Force (FATF) travel rule, which requires crypto providers to transmit customer information on transfers above certain thresholds, is now enforced across regulated GCC markets. Your payment processor must handle this automatically or your transactions will face delays or rejection. Second, custody arrangements must be insured and audited.

A processor holding customer funds without insurance or independent security audits is a liability, not a service. Request SOC 2 Type II certification and proof of insurance coverage before you sign contracts. Third, transaction reporting and audit trails must be blockchain-native and tamper-proof. Regulators in the UAE and Saudi Arabia increasingly demand real-time visibility into crypto flows. Processors using centralized databases rather than immutable ledgers will struggle to satisfy these demands.

Moving From Compliance to Implementation

When you integrate with a payment partner, verify these three elements directly-do not assume compliance from marketing claims. Once you confirm that your processor meets these standards, you can move forward with technical setup. The next chapter covers how to select stablecoin partners and connect them to your existing business systems.

Building Your Crypto Payment Stack

Select the Right Stablecoin for Your Market

USDT and USDC dominate Middle East payment corridors because they operate across UAE, Saudi Arabia, and Levant markets without triggering banking restrictions. USDT recorded $13.3 trillion in transaction volume in 2025, making it the most liquid option for merchants converting to fiat quickly. When you choose between them, prioritize the one your processor supports natively-switching between stablecoins mid-transaction introduces delays and conversion costs that erode margins.

Verify that your processor settles USDT or USDC directly to your bank account in AED, SAR, or JOD within 24 hours, not to a third-party wallet requiring additional steps. This matters because a two-day settlement cycle costs you cash flow and introduces price volatility exposure. Ask your processor for their settlement SLA in writing and confirm they maintain liquidity pools in your target currency.

Processors without dedicated liquidity in regional markets often route through international exchanges, adding 2-4 business days and eating into your margins.

Connect Crypto Payments to Your Business Systems

Integration with your existing systems must happen through APIs, not manual reconciliation. If your processor requires you to manually match transactions or export CSVs for accounting, that processor is built for small merchants, not growing businesses. Your payment gateway must connect to your e-commerce platform, accounting software, and inventory system automatically.

Most GCC-focused processors now offer Shopify and WooCommerce plugins, but if you use custom infrastructure, demand API documentation that shows real-time transaction webhooks, wallet balance queries, and automated invoice generation. This integration eliminates the friction that slows down scaling.

Automate Currency Conversion and Settlement

Implement auto-conversion on incoming crypto to your preferred stablecoin or fiat currency immediately upon receipt-do not hold customer payments in volatile assets. This protects your revenue from price swings and simplifies tax reporting. Set conversion thresholds so that payments above a certain amount convert instantly while smaller transactions batch hourly to reduce blockchain fees.

For fiat settlement, establish a direct connection between your processor and your local bank account. The Central Bank of Bahrain, SAMA, and UAE regulators now permit licensed crypto providers to maintain fiat corridors directly, eliminating the need for intermediaries. Confirm that your processor holds a banking license or has a banking partner explicitly authorized in your jurisdiction-processors without this infrastructure will experience account freezes during regulatory changes.

Verify Custody and Banking Infrastructure

Fireblocks and Crassula both operate licensed corridors in the UAE and Saudi Arabia, while smaller processors often route through third-party banks that can cut service without notice. Request proof that your processor maintains insured custody arrangements and direct banking relationships in your operating markets. A processor that cannot show you these connections will create operational risk when regulatory pressure increases or market conditions shift.

The infrastructure you build now determines whether you scale smoothly or face constant disruptions. Once you confirm that your payment stack handles settlement reliably, you can focus on the specific industries where crypto payments unlock the most value-starting with e-commerce, where transaction speed and lower fees create immediate competitive advantages.

Real-World Applications Across Industries

E-Commerce: Lower Fees and Faster Checkouts

E-commerce merchants in the UAE saw transaction abandonment rates drop by 8-12% when they added crypto payment options, according to adoption surveys from regional fintech operators. This matters because the average cart value in Middle Eastern e-commerce ranges from $80–$200, and payment friction directly erodes margins. When a customer encounters a crypto checkout that settles to your AED or SAR account within hours rather than days, they complete the transaction. Shopify merchants accepting USDT in Dubai reported 15% higher conversion rates from international customers who prefer crypto over credit cards due to lower fees and faster processing.

The reason is mechanical: crypto payments bypass payment processor markups that typically run 2.5–3.5% for cards, reducing your effective cost per transaction to under 0.5%. For high-volume e-commerce, this difference compounds quickly. Place your crypto payment option prominently on your checkout page-not buried in an accordion menu-because customers who know they can pay in crypto often seek it out deliberately. Use real-time price feeds to display prices in both AED and USDT, updating every 30 seconds so customers see exact amounts before confirming. This transparency prevents disputes over exchange rates.

Hospitality: Accelerated Cash Flow from International Guests

Hospitality operators in Saudi Arabia discovered a different advantage: crypto payments from international guests eliminate currency conversion delays that typically add 2–3 business days to settlement. A hotel in Riyadh processing $50,000 in weekly bookings from overseas visitors gains access to that cash 48 hours faster when guests pay in USDC instead of wire transfers. This accelerated cash flow matters more in hospitality than in most sectors because seasonal demand creates sharp fluctuations in working capital needs.

Implement crypto payment acceptance at your booking engine level, not just at the front desk. Guests booking through your website should see crypto as a payment method option during checkout, reducing friction compared to asking them to pay in crypto upon arrival. This integration at the point of sale captures international customers who actively prefer crypto for its speed and cost advantages.

Real Estate: Capital Efficiency Through Instant Settlement

Real estate transactions represent the largest opportunity but also the most complex implementation. A property developer in Dubai selling units worth $300,000–$500,000 each faces settlement delays of 5–7 business days through traditional banking, during which exchange rates shift and buyer confidence weakens. When you accept stablecoin payments for real estate, you eliminate this uncertainty. The transaction settles in hours, and your developer can immediately redeploy capital into new construction or hold USDC as a stable asset without currency risk.

However, real estate requires additional compliance: you must document the buyer’s identity through enhanced KYC procedures, ensure the property sale complies with local real estate regulations, and maintain audit trails showing the transaction on-chain. Work with a licensed crypto payment processor that offers white-label solutions specifically for real estate, not generic payment gateways. Processors like Crassula and Fireblocks provide transaction reporting templates designed for real estate firms, making regulatory reporting straightforward.

Matching Infrastructure to Your Business Model

The key across all three sectors is matching your crypto payment infrastructure to the specific pain point you solve: e-commerce benefits from reduced fees and faster checkout, hospitality gains from accelerated settlement and international guest convenience, and real estate unlocks capital efficiency through instant transactions. Your choice of stablecoin, settlement currency, and processor should reflect which pain point matters most to your business model.

Final Thoughts

Accepting Middle East crypto payments requires three concrete actions: verify your payment processor holds regulatory licenses in your operating jurisdiction, automate currency conversion to stablecoins or fiat within hours of receipt, and implement robust KYC and AML controls that meet FATF travel rule standards. These steps eliminate the compliance uncertainty that stops most businesses from moving forward. The regulatory environment in the UAE, Saudi Arabia, and Bahrain has shifted decisively toward structured frameworks-VARA licensing, SAMA sandboxes, and Central Bank of Bahrain crypto exchange approvals create pathways that did not exist two years ago.

Risk mitigation starts with processor selection. Request SOC 2 Type II certification, proof of insurance coverage, and direct banking relationships in your target markets before you sign contracts. Processors without these credentials will create operational friction when regulatory pressure increases or market conditions shift.

Your next step depends on your business model. E-commerce merchants should integrate crypto payment plugins into their checkout flow within 30 days and measure conversion rate impact, while hospitality operators should pilot crypto acceptance with international booking channels to capture faster settlement. We at Web3 Enabler help businesses at scale connect blockchain transactions directly to their existing infrastructure, enabling faster and cheaper global payments that settle in seconds-explore how Web3 Enabler integrates crypto payments into your business systems to accelerate your implementation timeline and reduce operational complexity.

FAQs About Accepting Crypto Payments in the Middle East

Is it legal to accept crypto payments in the UAE?

It can be, but “the UAE” is not one rulebook. Dubai has a dedicated virtual assets regulator for most of Dubai, while DIFC and Abu Dhabi have their own financial regulators. Your first step is identifying which regulator applies to your entity and payment flow, then choosing a payment partner that is licensed or otherwise authorized for the activity you are doing. Treat this as a compliance project, not a plugin install.

How do I verify a crypto payment processor is licensed in Dubai?

Ask for written proof of their licensing status and cross-check it against the regulator’s public register. Confirm whether they are fully licensed or only operating under an in-principle approval, and confirm the exact activities covered by that authorization, for example custody, brokerage, exchange, or payment services. If a provider will not share documentation, treat that as a red flag.

Can businesses accept crypto payments in Saudi Arabia?

Saudi Arabia is cautious on crypto activity and expectations can differ depending on the use case and the regulator involved. If you want to accept crypto for goods and services, do not assume it is permitted just because you can technically process it. Work only with partners that can clearly explain the approvals they operate under, and consider controlled pilots where appropriate rather than full rollout on day one.

How is Bahrain different for crypto payments?

Bahrain has an established framework for crypto-asset service providers and has granted licenses to firms operating under that framework. For merchants, that usually means you should select a payment partner that is properly licensed or regulated for the services they provide, and confirm how settlement to fiat will occur, which bank rails they use, and what audit and reporting you will receive.

What should businesses know about Jordan, Lebanon, and Egypt before accepting crypto?

Rules vary widely. Jordan enacted a virtual assets law in 2025 that creates a licensing framework and allows the central bank to authorize virtual assets for payment purposes under specific regulations. Lebanon is often described as a gray area where activity may exist but banking access and formal protections can be limited. Egypt has warned against dealing in cryptocurrencies and restricts activity without approval. If you operate in multiple countries, design your payment stack so corridors can be enabled or disabled by jurisdiction.

Should I accept USDT or USDC for Middle East crypto payments?

Both are widely used stablecoins in the region. The practical choice is the stablecoin your processor supports natively with the cleanest settlement path to your target currency, for example AED or SAR, and the strongest compliance tooling. Confirm liquidity, conversion spreads, supported chains, and whether you can lock pricing at checkout to avoid short-window volatility. Pick one primary rail for your main corridor, then expand once operations are stable.

What are the KYC, AML, and Travel Rule requirements for crypto payments?

In regulated environments, your payment partner should handle KYC and AML checks and support Travel Rule information sharing when required. You still need internal controls, including policies for sanctions screening, high-risk customer reviews, and record retention. Ask how originator and beneficiary data is transmitted between providers, what thresholds trigger enhanced due diligence, and what happens when Travel Rule data is missing or unverifiable.

How do I protect revenue from crypto volatility?

Do not hold customer payments in volatile assets. Use automatic conversion so incoming payments convert immediately into a stablecoin or fiat, based on your treasury policy. Define thresholds so large payments convert instantly, while smaller payments can batch to reduce network fees. Make sure the processor can provide an auditable trail for conversions, timestamps, and rates used.

How do refunds and disputes work with crypto payments?

Crypto transfers are typically push-based and generally final, so you need a clear merchant-led refund process instead of relying on chargebacks. Define whether refunds are issued in the same stablecoin, a different stablecoin, or fiat to a bank account. Document how you will verify identity for refunds, handle partial refunds, and manage FX or network fee differences so customer support is consistent.

How should I integrate crypto payments with Shopify, WooCommerce, and accounting?

Use integrations that produce clean, automated records. Your gateway should offer plugins for common platforms and robust APIs for custom stacks, including real-time webhooks for payment status, invoice generation, and settlement updates. In accounting, you want each payment mapped to an order, fees separated, conversions recorded, and exports compatible with your ERP or general ledger. If you are reconciling via spreadsheets, you are not ready to scale.