Cash is becoming a relic. Customers expect to tap, click, and pay-and businesses that don’t offer digital payments are leaving money on the table.

Cash is becoming a relic. Customers expect to tap, click, and pay-and businesses that don’t offer digital payments are leaving money on the table.

The increase in digital payments isn’t just a trend; it’s a business necessity. At Web3 Enabler, we’ve seen firsthand how companies that modernize their payment systems cut costs, speed up transactions, and gain valuable customer data.

Why Companies Are Actually Making the Switch

The Customer Expectation Has Already Shifted

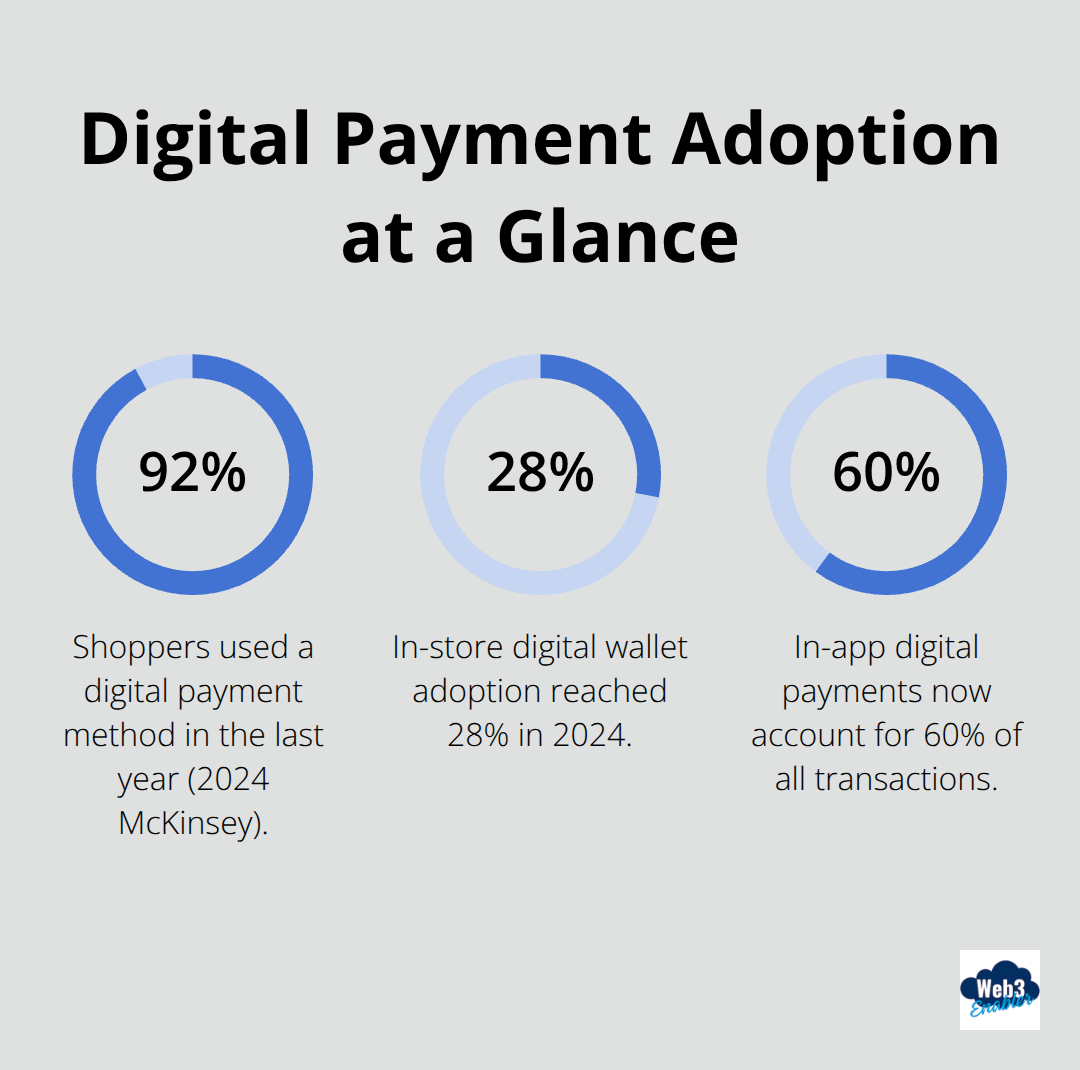

92 percent of shoppers used a digital payment method in the last year, according to 2024 McKinsey data-your customers have already voted with their wallets. In-store digital wallet adoption jumped from 19 percent in 2019 to 28 percent in 2024, and in-app digital payments now account for 60 percent of all transactions. This isn’t a niche preference anymore; it’s the baseline expectation.

Contactless and mobile payments have become so normalized that offering only cash or card processing feels outdated. Customers tap their phone, scan a QR code, or use their preferred wallet without thinking twice. Businesses that haven’t adapted actively frustrate their audience and lose sales to competitors who have.

The Math Works in Your Favor

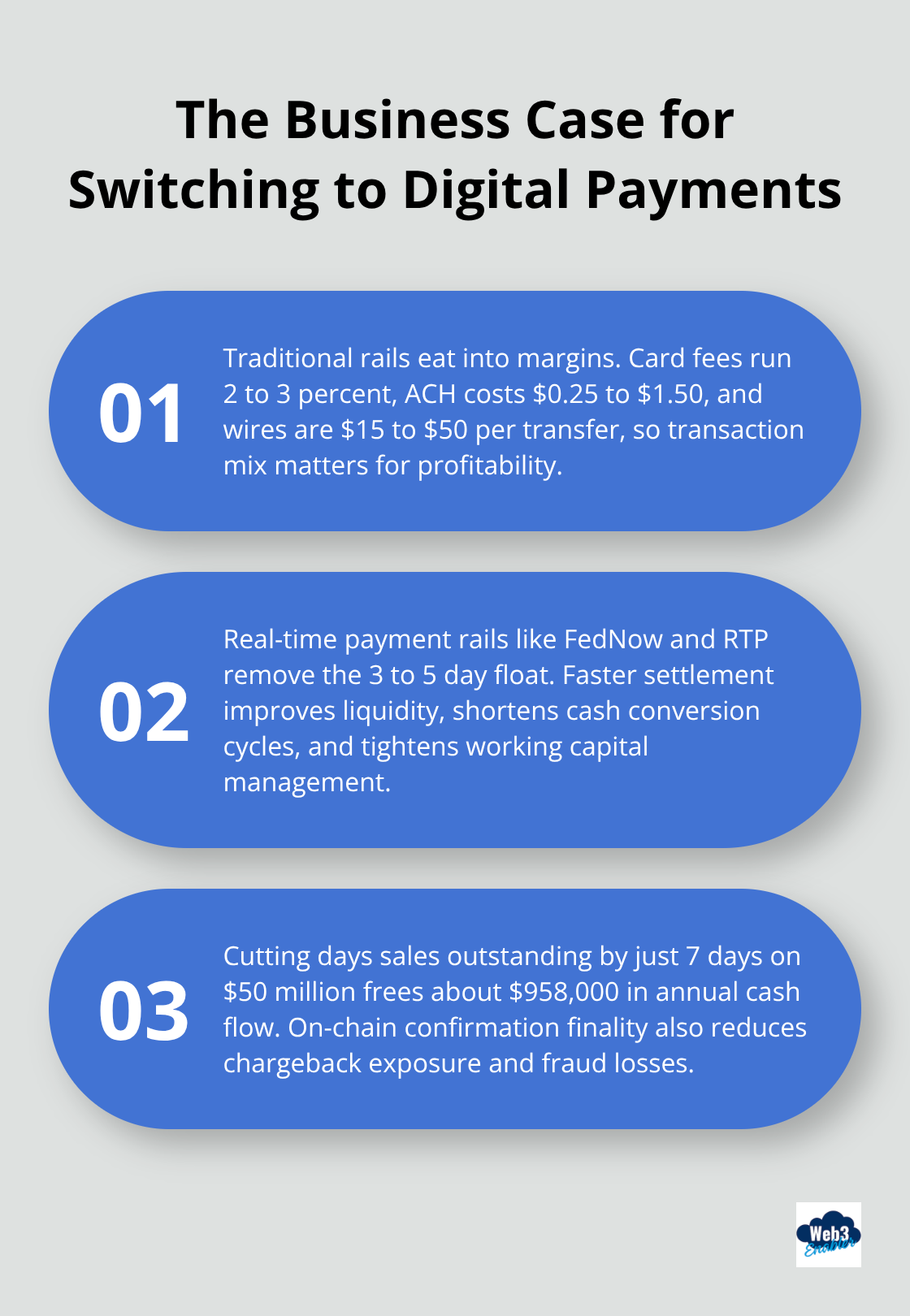

Traditional payment methods carry real costs that add up fast. Credit and debit cards consume 2 to 3 percent in fees, ACH transfers run 25 cents to $1.50 per transaction, and wire transfers cost $15 to $50 each. Real-time payment rails like FedNow and RTP eliminate the traditional 3 to 5 day float in B2B payments, meaning your cash stops sitting trapped in settlement limbo.

A 7-day reduction in days sales outstanding on $50 million in revenue unlocks approximately $958,000 in annual cash flow-that’s money sitting in your account instead of your customers’. Digital methods also dramatically reduce chargeback risk because on-chain confirmations are final, cutting fraud exposure significantly.

The Hidden Multiplier Effect

Automating even 50 percent of payment processing and shifting 60 percent of transactions to zero-fee rails saves a typical $50 million company roughly $1.175 million in year one (about $425,000 in labor costs and $750,000 in transaction fees). That translates to approximately 280 percent ROI.

Digital payments also unlock something less obvious but equally valuable: enhanced data collection. Your system automatically logs customer behavior, purchase frequency, and preferences without extra effort. This data asset informs inventory decisions, marketing campaigns, and customer retention strategies in ways cash transactions never could.

The shift from traditional to digital payments isn’t optional-it’s a direct path to faster cash, lower expenses, and smarter business decisions. Now that you understand why the change matters, the next step involves building the infrastructure to make it happen.

Building Your Payment Stack

Choose a Provider That Fits Your Business

Picking the wrong payment infrastructure is like choosing the wrong foundation for a house-everything built on top gets wobbly. You need a provider that handles multiple payment methods, integrates smoothly with your existing systems, and doesn’t require a PhD to set up. Stripe processes around 1,700 transactions per second and supports 125+ payment methods across borders, making it a solid starting point for most businesses. Square works well if you’re running a retail operation with both online and in-person sales, offering unified commerce without juggling separate platforms. For B2B companies handling recurring invoices and complex payment flows, Paystand consolidates payments with real-time AR/AP dashboards and zero-fee network options. Your choice depends on your transaction volume, customer base, and whether you need advanced features like subscription management or international payouts. Test the integration with your current systems before committing-a provider that plays nicely with your ERP or CRM saves months of headaches later.

Deploy the Right Hardware and Payment Methods

NFC-enabled terminals are now table stakes; digital wallets are increasingly popular for in-store payments. QR code payments cost almost nothing to implement and work instantly in quick-service environments, speeding up lines and reducing friction. Accept mobile wallets like Apple Pay and Google Wallet alongside cards-this covers roughly 60 percent of in-app digital payment preferences. Try three to five payment methods rather than supporting everything at once. This approach reduces complexity while covering 90 percent of customer preferences.

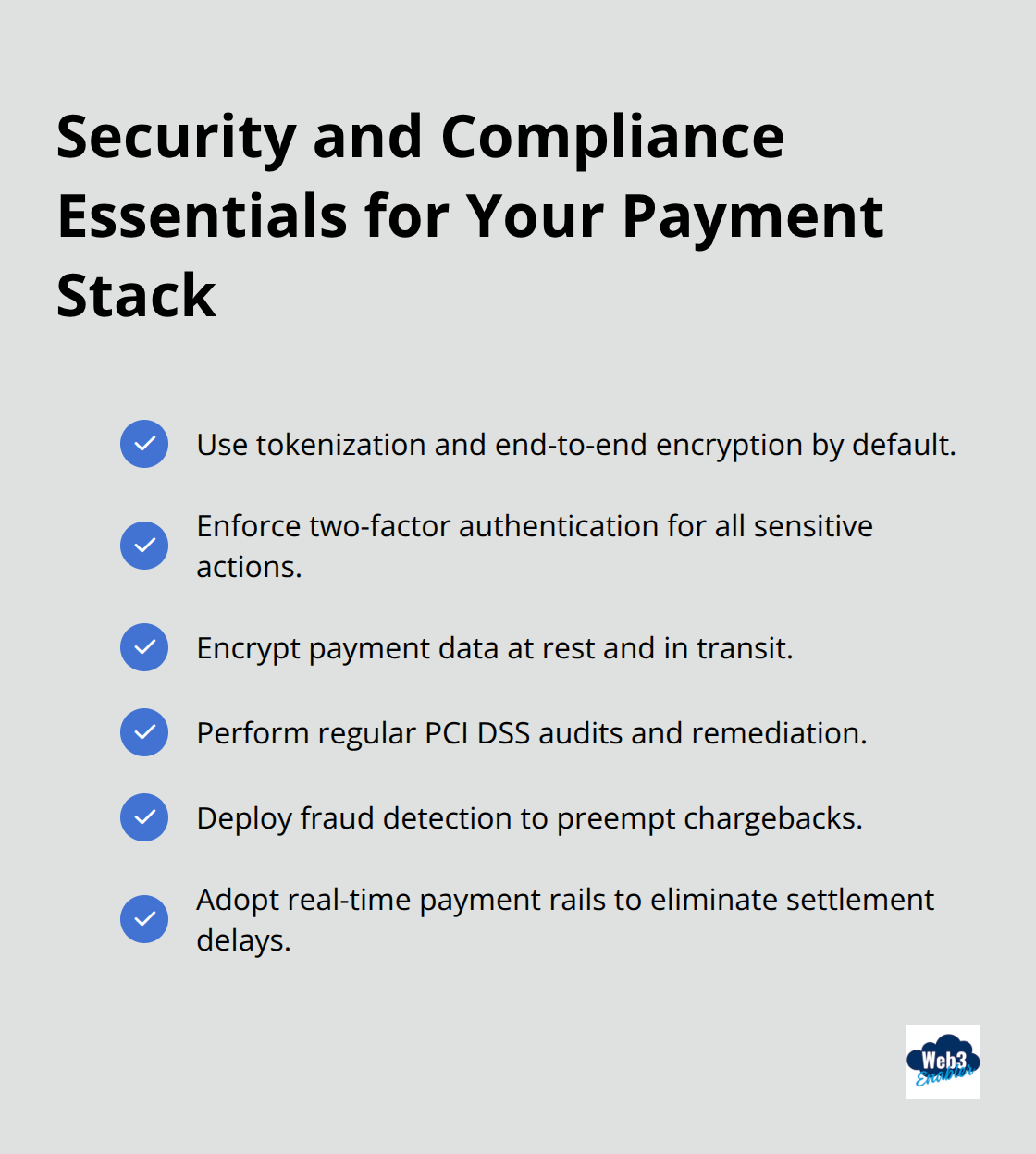

Lock Down Security and Compliance

Tokenization and encryption aren’t optional extras; they’re mandatory. PCI DSS compliance requires two-factor authentication, encrypted data storage, and regular security audits. Fraud detection tools flag suspicious patterns before they become chargebacks, which cost merchants $15 to $100 per incident beyond the disputed amount. Real-time payment rails eliminate settlement delays entirely, meaning funds hit your account immediately instead of sitting in processing queues.

Train Your Team on Payment Operations

Your staff needs to understand the actual mechanics: how to process refunds, handle payment failures, and troubleshoot customer wallet issues. Spending a week upfront on training prevents weeks of customer support headaches later. When your team knows how payments flow through your system, they handle edge cases faster and keep customers happy.

With your infrastructure in place and your team ready to operate it, the next challenge involves getting customers to actually use these new payment options. That’s where strategy comes in.

Getting Customers to Actually Switch

Target Your Early Adopters First

The infrastructure sits ready, but adoption doesn’t happen automatically. You need a deliberate strategy to shift customer behavior from comfortable payment habits to your new digital options. Start with your highest-value customer segments rather than pushing digital payments to everyone at once. Travelers, remote workers, and subscription customers already expect frictionless digital payment flows, so they become your early adopters. This focused approach builds momentum without overwhelming your team or confusing your broader customer base.

Create Real Incentives, Not Empty Promises

Offer a genuine incentive for switching, not just vague convenience talk. A 2 percent discount for digital wallet payments or a small cashback reward on stablecoin transactions creates immediate motivation. Affirm and Klarna report that offering buy-now-pay-later options increases average order value by 20 to 30 percent, so if your customer base skews younger or price-sensitive, bundling BNPL alongside traditional methods captures sales you’d otherwise lose. The key involves testing which incentives resonate with your specific audience rather than copying what competitors do.

For B2B companies, the incentive looks different: faster payment processing, automated invoice matching, and real-time visibility into payment status matter more than discounts. Companies offering self-service payment portals see 40 percent faster payment collection because customers pay on their own schedule without waiting for support.

Eliminate Friction at Checkout

Your checkout experience makes or breaks adoption. Every friction point kills conversions. QR code payments work brilliantly for in-person retail because they’re instant and require zero hardware changes. For online businesses, one-click checkout using saved wallet information cuts abandonment rates significantly. Mobile wallet integration through Apple Pay or Google Wallet means customers complete transactions in seconds without typing card numbers.

Your team needs to monitor payment failures and understand why customers drop off at checkout. If 5 percent of transactions fail on a specific payment method, that signals a need to troubleshoot or remove it. This data-driven approach prevents customers from abandoning digital payments out of frustration.

Train Staff to Handle the Transition

Staff training goes beyond mechanics; your team needs to confidently explain why digital payments benefit customers, handle edge cases when payments fail, and troubleshoot wallet connection issues without frustrating customers. A customer who experiences a payment failure and encounters a confused employee reverts to slower payment methods entirely.

Invest in clear documentation and monthly refresher training, especially when you add new payment methods. The ROI compounds quickly because well-trained staff reduce support tickets, speed up problem resolution, and prevent customers from abandoning digital payments out of confusion or poor service.

Final Thoughts

The increase in digital payments isn’t coming-it’s already here, and your competitors are moving fast. You’ve seen the numbers: 92 percent of shoppers expect digital options, real-time payment rails eliminate settlement delays, and a modest 7-day improvement in cash flow unlocks nearly $1 million annually for a $50 million company. The math is undeniable, and waiting costs you money every single day.

Your implementation roadmap stays straightforward. Pick a provider that handles multiple payment methods without complexity, deploy NFC terminals and mobile wallet support, lock down security with tokenization and fraud detection, and train your team to operate the system confidently. Start with early adopters-travelers, remote workers, subscription customers-rather than forcing digital payments on everyone simultaneously, and create genuine incentives that motivate the switch.

A typical $50 million company saves roughly $1.175 million in year one through payment automation and zero-fee rails, plus you unlock customer data that informs inventory decisions and marketing strategies in ways traditional methods never could. Web3 Enabler provides Salesforce-native solutions that connect blockchain technology directly to your existing systems, enabling faster global payments and compliance without the complexity. Your customers have already voted with their wallets-the only question left is whether you’ll answer.