International payments move at a snail’s pace. Companies wait days for funds to settle across borders, while hidden fees and multiple intermediaries eat into margins.

We at Web3 Enabler have seen how cross-border settlement automation changes the game. Blockchain payments eliminate the middlemen, compress timelines from days to minutes, and give finance teams real visibility into their cash flow.

Why Global Payments Still Get Stuck in the Old System

The Correspondent Banking Bottleneck

Traditional banking relies on a correspondent banking network that passes money hand-to-hand across borders. Each handoff introduces delay. The Federal Reserve’s wire system processes payments in batches, not continuously, which means a payment initiated at 3 p.m. on Friday won’t move until Monday morning. The Financial Stability Board reported in 2025 that nearly one-fifth of cross-border payment corridors still exceeded 3% in costs, well above the G20 target of 1% or less.

That gap exists because legacy infrastructure was designed for a different era. When a company in Frankfurt sends funds to a supplier in Singapore, the money touches at least four or five banks along the way. Each one takes a fee, applies currency conversion spreads, and holds the payment for a day or more while they batch and reconcile. Traditional bank transfers take 3-5 business days for domestic payments, while international transfers crawl along for up to 10 business days, even though the underlying technology could move the money in seconds.

Manual Processes Compound the Delays

The human overhead compounds the problem significantly. Bank staff manually verify account details, cross-check compliance rules, and reconcile transactions across incompatible systems. One study from J.P. Morgan on real-time payments found that traditional fraud controls designed for slower settlement timelines fail completely in instant payment environments because they run after the transaction completes, not before. The damage occurs before anyone can stop it.

The Eurosystem noted that two-thirds of euro area card transactions still flow through non-European providers, forcing cross-border dependencies that add friction and cost. Compliance checks happen at every stage, creating redundancy and delay.

Hidden Costs That Silently Erode Margins

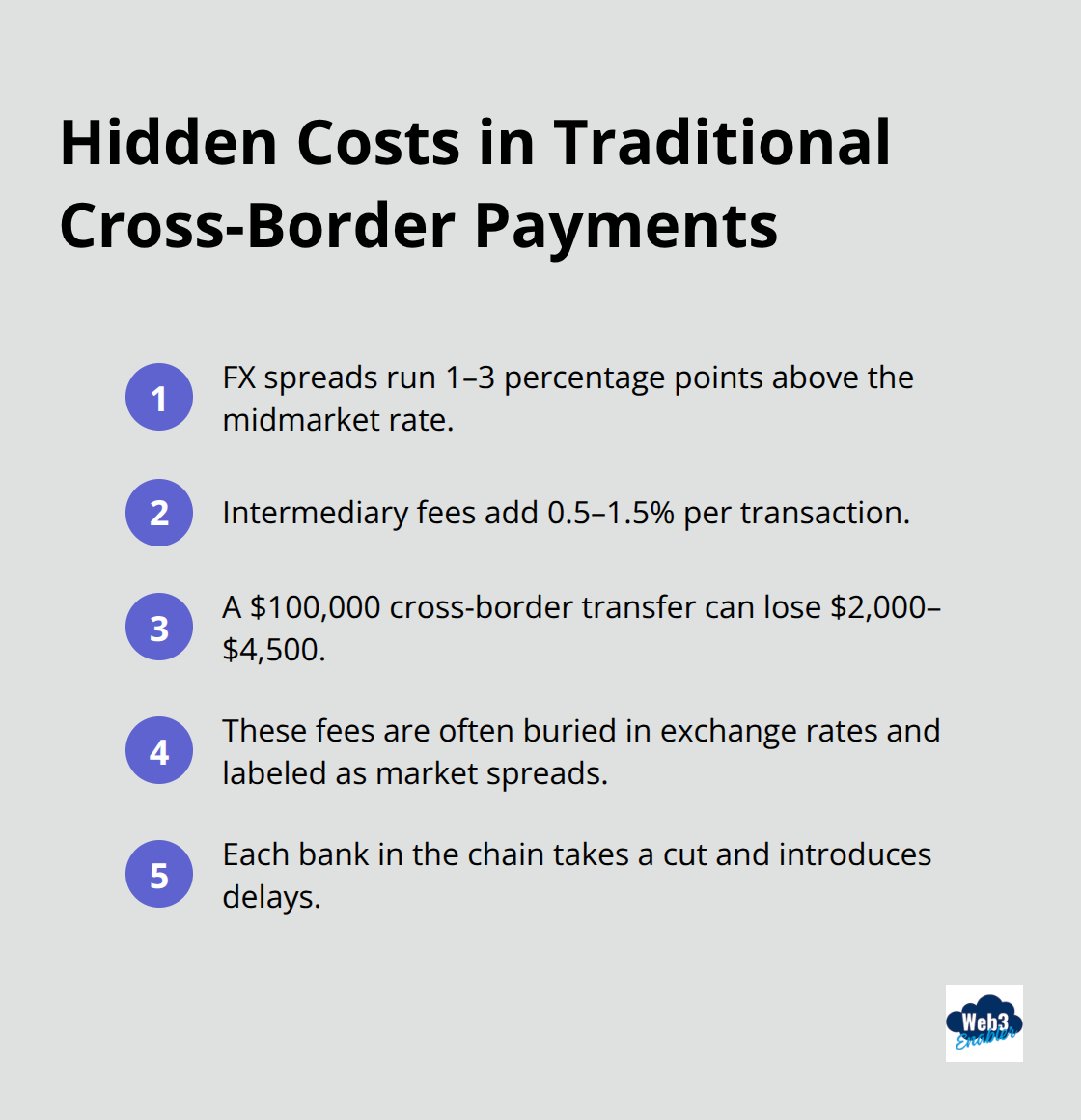

Hidden costs pile up without visibility. Currency conversion spreads can run 1 to 3 percentage points above the midmarket rate. Intermediary fees add another 0.5 to 1.5% per transaction. A company moving $100,000 internationally can lose $2,000 to $4,500 in fees and conversion costs alone.

Finance teams rarely see these costs broken down because they’re buried in exchange rates and labeled as market spreads. The real issue is structural. Traditional infrastructure requires trust between institutions that don’t know each other, so every bank in the chain demands its cut and its control point.

Why the System Persists Despite Its Flaws

The system works, but it works slowly and expensively. Companies have accepted this as normal because alternatives didn’t exist. That acceptance has ended. Blockchain payments now offer a path forward that eliminates intermediaries, compresses settlement timelines, and gives finance teams the visibility they need to optimize cash flow and reduce operational risk.

How Blockchain Payments Eliminate the Settlement Bottleneck

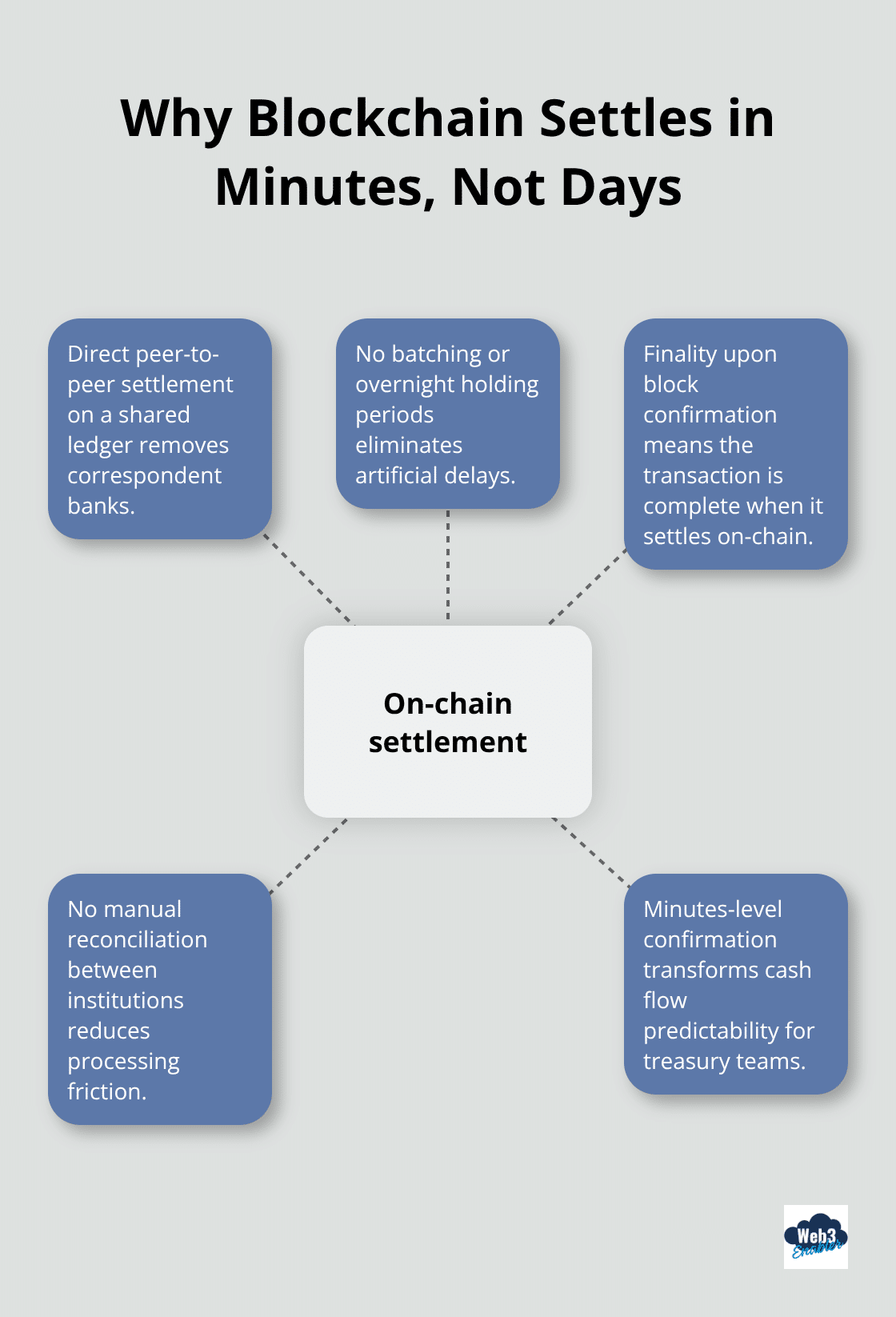

Blockchain payments work fundamentally differently from correspondent banking. Instead of routing money through a chain of intermediaries, transactions settle directly between parties on a shared ledger. When a company sends stablecoin payments across borders, the transaction confirms in minutes, not days. Blockchain achieves this speed because there is no batching, no overnight holding periods, and no manual reconciliation steps between institutions. The transaction becomes final the moment it settles on-chain.

For treasury teams managing global operations, this shift from days to minutes transforms cash flow predictability and liquidity planning. A supplier in Hong Kong no longer waits ten days to receive payment from a buyer in Amsterdam. Settlement happens in real time, which means accounting teams close books faster and finance leaders see accurate liquidity positions without guessing how many payments are in flight.

Real-Time Visibility Transforms Finance Operations

The second advantage is visibility. Traditional wire transfers disappear into the correspondent banking system, leaving finance teams blind until the payment lands in the destination account. Blockchain transactions are immutable and auditable at every step. When a payment settles on-chain, it leaves a permanent record that shows exactly when the transaction occurred, which wallet received it, and the precise amount transferred. This transparency eliminates reconciliation delays. Instead of waiting for bank statements to arrive and manually matching transactions, finance teams see settlement confirmation instantly and can reconcile accounts in real time. For companies with hundreds of international payments monthly, this reduces manual exception handling from hours of work per day to nearly zero. Treasury teams also gain better control over currency risk. Stablecoin payments eliminate FX conversion spreads because the value is fixed at issuance. A company paying in USDC sends exactly the dollar equivalent agreed with the counterparty, with no hidden conversion costs eating into the transaction.

Intermediaries Disappear, Costs Plummet

Removing intermediaries directly reduces fees. A traditional international payment involves correspondent banks, currency exchanges, and clearing houses, each taking a cut. Blockchain payments eliminate most of these touchpoints. Instead of losing 1 to 3 percentage points to currency conversion and another 0.5 to 1.5% to intermediary fees, companies pay only the network fee to settle on-chain, typically a fraction of a cent per transaction. For a company moving $5 million monthly across borders, the annual savings from lower fees alone can reach $50,000 to $100,000. Add faster cash flow and reduced treasury staff time, and the business case becomes compelling. Organizations like financial institutions managing high-volume settlements see the biggest impact.

Salesforce Integration Unlocks Operational Efficiency

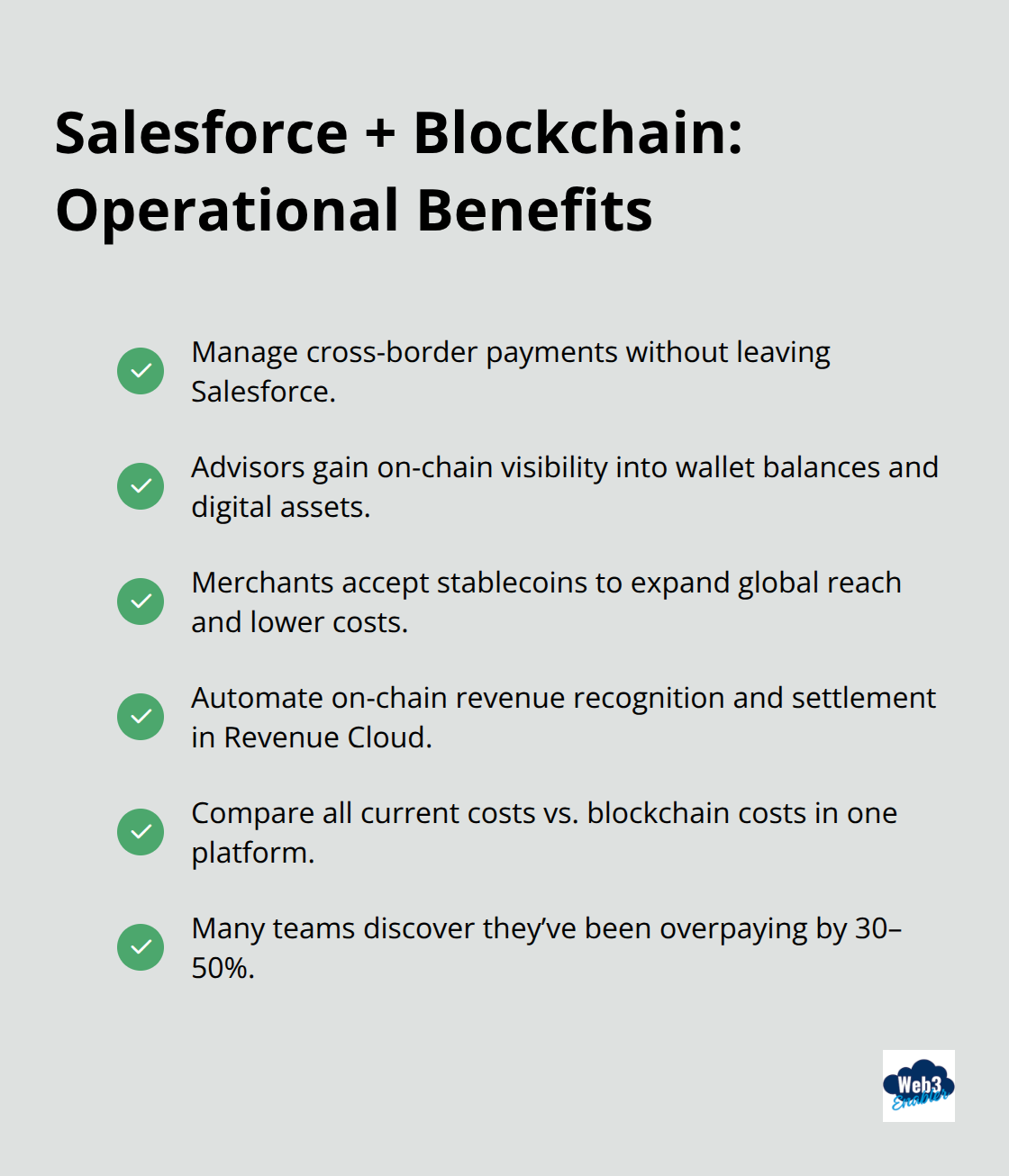

Web3 Enabler brings blockchain settlement directly into Salesforce, enabling finance teams to manage cross-border payments without leaving their CRM. Within Financial Services Cloud, advisors gain on-chain visibility into client wallet balances and digital asset positions, delivering more informed guidance. Commerce Cloud merchants accept stablecoins for e-commerce transactions, expanding global reach while lowering payment processing costs. Revenue Cloud users automate on-chain revenue recognition and settlement, unlocking new efficiencies for global billing and treasury management. This integration means finance teams calculate their current cross-border costs (all fees, currency spreads, and staff time spent on reconciliation) and compare that against blockchain settlement costs within a single platform. Most discover they are overpaying by 30 to 50% for the privilege of slow, opaque transactions.

The real impact emerges when finance teams move beyond cost savings and examine how blockchain settlement transforms their entire payment workflow. Real-world impact on financial operations shows exactly how this modernization plays out across treasury departments, liquidity management, and institutional settlement practices.

How Cross-Border Settlement Automation Transforms Treasury Operations

Immediate Cash Flow Improvements

Finance leaders managing global operations face a stark reality: their current settlement process wastes millions annually while keeping them blind to cash position. Blockchain settlement fixes this. When a multinational company shifts even 30% of cross-border payments to blockchain rails, cash flow improves measurably. A $500 million annual payment volume moving 30% through stablecoins saves roughly $150,000 to $300,000 in fees and currency spreads yearly. More importantly, the company compresses its cash conversion cycle by 5 to 7 days because payments settle in minutes instead of waiting for correspondent banks to batch and process. That compression alone frees up working capital that treasury teams can redeploy. For a company with $2 billion in annual revenue, a 5-day improvement in cash conversion translates to $27 million in freed-up liquidity. Finance teams that adopt blockchain settlement gain this advantage before competitors do, and they keep it because moving back to correspondent banking becomes unthinkable once teams experience real-time visibility and instant reconciliation.

Operational Efficiency and Staff Productivity

The second transformation happens in treasury operations itself. Traditional payment workflows require treasury staff to track payments across multiple banking platforms, wait for settlement confirmations, and manually reconcile against accounting records. Blockchain eliminates this friction because every transaction creates an immutable, auditable record that settles instantly. A global financial institution processing 10,000 cross-border payments monthly saves roughly 200 hours of manual reconciliation work per month (approximately 2,400 hours annually) when moving to blockchain settlement. That frees compliance and operations teams to focus on higher-value work instead of chasing payment status.

Salesforce Integration for Real-Time Visibility

Web3 Enabler brings blockchain settlement directly into Salesforce, enabling finance teams to manage cross-border payments without switching platforms. Revenue Cloud users automate settlement and revenue recognition, compressing month-end close from days to hours. Financial Services Cloud advisors see client wallet balances and stablecoin positions in real time, enabling more accurate portfolio guidance and faster decision-making. Commerce Cloud merchants accepting stablecoins reduce payment processing costs by 40% to 60% compared to traditional card networks and wire transfers. These operational gains compound across departments and geographies.

Instant Dispute Resolution

The hidden benefit emerges in dispute resolution. Blockchain transactions are immutable and timestamped, so disagreements about payment amounts or timing resolve instantly by checking the on-chain record. Traditional banking requires weeks of back-and-forth between institutions to investigate discrepancies. Blockchain eliminates that entirely, reducing friction between trading partners and accelerating settlement finality.

Final Thoughts

Cross-border settlement automation transforms how finance teams operate globally by delivering three immediate wins: faster cash flow that frees working capital, lower costs that compound annually, and real-time visibility that eliminates reconciliation delays. A company moving even 30% of cross-border volume through blockchain rails recovers hundreds of thousands in annual savings while compressing cash conversion cycles by days. Treasury staff reclaim time spent on manual tracking and dispute resolution, redirecting effort toward strategic liquidity management instead of operational firefighting.

Modernizing payment infrastructure matters because the old system was designed for a different era. Correspondent banking worked when alternatives didn’t exist, but it no longer serves companies competing in global markets where speed and transparency drive competitive advantage. Finance leaders who delay this transition accept unnecessary costs and operational friction that competitors are already eliminating, and the business case is quantifiable: lower fees, faster settlement, reduced staff overhead, and improved cash position visibility.

Start by calculating your current cross-border costs across all fees, currency spreads, and internal labor, then compare that against blockchain settlement costs within a unified platform. Web3 Enabler brings cross-border settlement automation directly into Salesforce, enabling finance teams to manage international payments without switching systems or disrupting existing workflows. Begin with a single payment corridor, measure the impact against your baseline costs, then scale across geographies as your team gains confidence in the new infrastructure.

FAQ: Cross-Border Settlement Automation

Why is traditional correspondent banking so slow and expensive?

Traditional banking relies on a “hand-off” system where money moves through multiple intermediary banks. Each bank must manually reconcile the transaction, apply its own currency conversion spread (often 1-3%), and charge a fee. This legacy infrastructure was designed for a non-digital era, resulting in the 3–10 day settlement cycles seen today.

How do stablecoins like USDC eliminate international “middlemen”?

Stablecoins operate on public or permissioned blockchains that serve as a shared ledger. Instead of five banks verifying a single transfer, the blockchain confirms the transaction once. This allows a company in Frankfurt to send funds to Singapore in minutes, bypassing the batch processing and overnight holds of the traditional Federal Reserve wire system.

What is the typical ROI for switching to blockchain-based settlement?

Most mid-market companies moving at least 30% of their international volume to blockchain rails see positive ROI within 60–90 days. This comes from reducing intermediary fees (saving $15,000+ monthly on high-volume corridors) and compressing the “Cash Conversion Cycle” by 5–7 days, which frees up significant working capital.

How does Salesforce integration help with “Instant Reconciliation”?

By bringing blockchain data into Financial Services Cloud or Revenue Cloud, every on-chain transaction is automatically recorded as an immutable audit trail. Finance teams no longer have to manually match bank statements to invoices; the system recognizes the unique transaction hash and updates the account balance in real time.

Is blockchain settlement compliant with 2026 global financial standards?

Yes. 2026 standards, influenced by the Financial Stability Board’s 2025 report, encourage the use of regulated stablecoins and “Virtual On-Ramps” that maintain full KYC/AML transparency. By using a native Salesforce integration, your compliance team can view the entire chain of custody—from the US payer to the international recipient—within a single, auditable dashboard.