Cross-border blockchain payments are reshaping how money moves globally, cutting through the friction that has defined remittances for decades. Traditional systems still charge families 5–7% in fees while taking days to settle, a reality we at Web3 Enabler see changing rapidly.

Cross-border blockchain payments are reshaping how money moves globally, cutting through the friction that has defined remittances for decades. Traditional systems still charge families 5–7% in fees while taking days to settle, a reality we at Web3 Enabler see changing rapidly.

Blockchain technology offers a direct path: faster settlement, lower costs, and genuine transparency. This post examines how distributed ledger systems are dismantling barriers and what compliance frameworks make them viable for real-world use.

Why Traditional Cross-Border Payments Still Cost Families Thousands

The Correspondent Banking Bottleneck

The infrastructure moving money across borders today was built for a different era. When a family in the Philippines sends $200 to relatives in the US through traditional banking channels, the money passes through correspondent banking in multiple countries, each taking a cut and adding processing time. The World Bank projects the real-time payments market will grow at 35.5% annually through 2030, yet most remittances still move through systems designed for batch processing. Families lose 5–7% to fees before the money even arrives, and settlement takes multiple business days. Banks justify these costs by pointing to compliance overhead, but the reality is simpler: the system is inefficient, and no single institution has incentive to modernize it.

Fragmentation Across Borders Slows Everything Down

The fragmentation across borders makes this worse. A transfer from Singapore to Thailand might use PayNow and PromptPay, two domestic instant payment systems that have begun connecting through Project Nexus, a BIS-led initiative linking instant payment systems across India, Malaysia, Philippines, Singapore, and Thailand. Yet the moment funds need to move outside these corridors, the speed advantage disappears. Regulatory requirements differ wildly-what counts as acceptable KYC documentation in one jurisdiction may trigger additional review in another. Currency conversion happens multiple times, often at rates hidden within bank spreads.

Manual Processes Create Compliance Delays

Enterprise clients report spending weeks on compliance reviews for straightforward cross-border transactions, while manual reconciliation across multiple banking systems creates audit nightmares. The competitive advantage in cross-border payments has already shifted from who owns the payment rails to who can orchestrate liquidity and settlement across multiple rails, according to analysis from DBS. This means the old model-relying on a single correspondent bank pathway-no longer works for speed or cost.

Why Blockchain Offers a Different Path Forward

Businesses moving capital internationally now face a choice: accept the friction and expense of traditional banking, or find systems that bypass these inefficiencies entirely. Blockchain technology removes intermediaries, settles transactions in minutes rather than days, and creates immutable records that simplify compliance. The next section examines how distributed ledger systems actually solve these problems in practice.

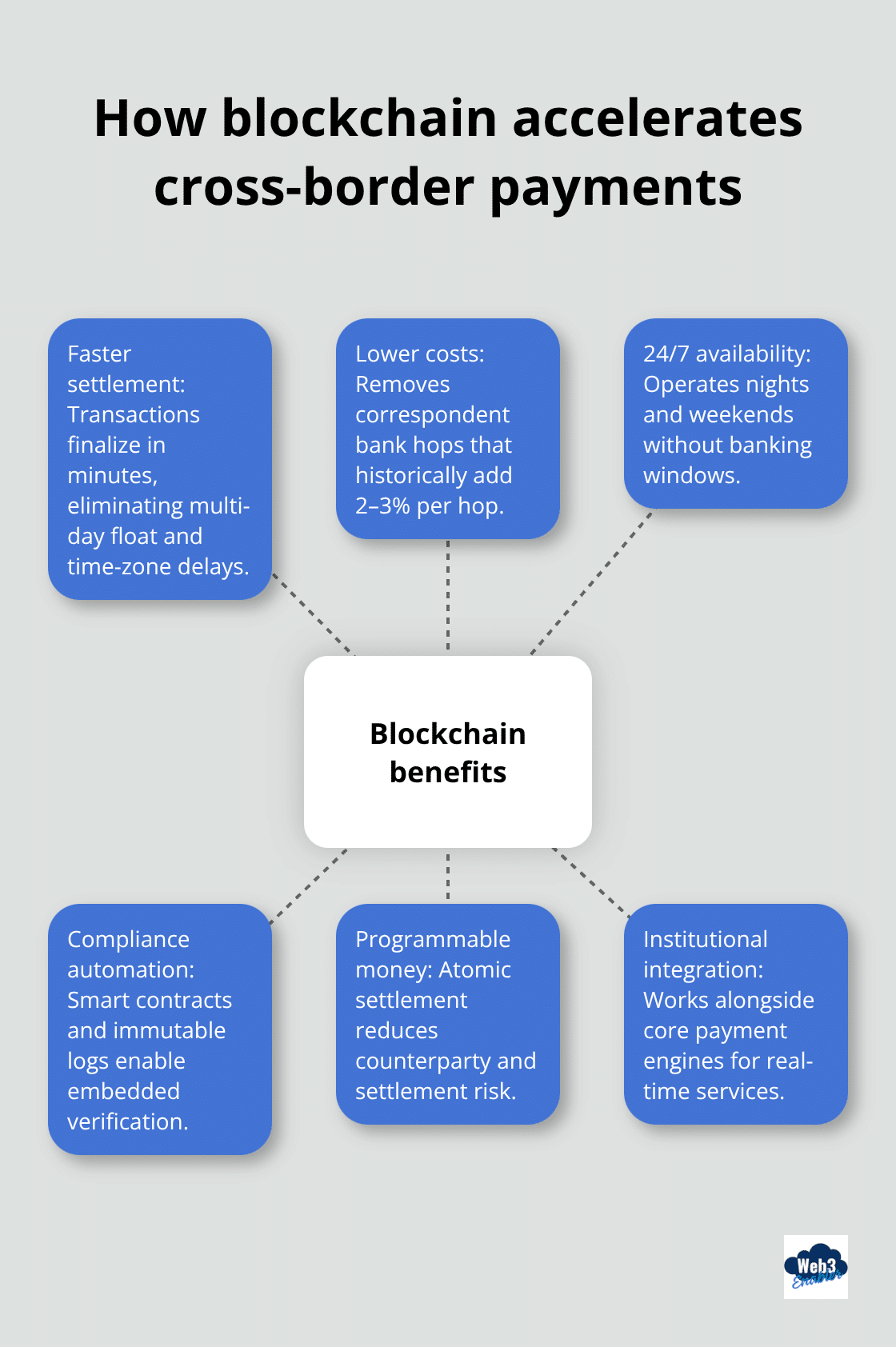

How Blockchain Cuts Through the Remittance Mess

Blockchain removes the intermediary chain that makes traditional remittances expensive and slow. When a sender in the US initiates a stablecoin transfer to a recipient in the Philippines, the transaction settles on a distributed ledger in minutes, not days. DBS reports a nearly threefold year-over-year increase in cross-border QR transactions using blockchain rails, demonstrating that speed translates directly into adoption. The mechanics are straightforward: tokenized money moves as programmable assets on an immutable ledger, eliminating correspondent banks that historically charge 2–3% per hop. A 2025 analysis found that blockchain-enabled stablecoins reduced cross-border transaction costs significantly, with settlement times under 10 minutes in most cases. This matters because a family sending $500 monthly to relatives now pays substantially less than traditional methods. The cost difference compounds over time, freeing capital for families and enterprises alike. Financial institutions like DBS have launched blockchain-enabled services delivering instant, 24/7 real-time payments via permissioned blockchains integrated with core payment engines, proving that institutional-grade infrastructure works at scale.

Settlement Without Waiting for Banking Hours

Traditional payments pause at night and weekends due to correspondent banking windows and time-zone delays. Blockchain operates continuously. A transaction initiated Friday evening in Manila settles instantly on a shared ledger accessible to both sender and receiver, regardless of local banking hours.

This eliminates the multi-day float that banks historically exploited for internal gains. Tokenized deposits and stablecoins enable atomic settlement-both sides of the transaction confirm simultaneously on the ledger, removing settlement risk. The World Bank projects cross-border payments will exceed $250 trillion by 2027, yet most of that volume still moves through batch systems. Institutions adopting blockchain for corridors like Singapore-to-India or Philippines-to-US report that real-time settlement compresses working capital cycles by 3–5 days on average, freeing capital that would otherwise sit frozen in transit. For SMEs sending regular payments to suppliers or contractors abroad, this timing improvement directly improves cash flow and reduces reliance on overdraft facilities.

Compliance Becomes Embedded, Not Bottlenecked

The industry is shifting from post-event compliance to embedded verification within the payment itself. AI-based screening, inline anomaly detection, and immutable audit trails execute during transaction processing rather than hours or days after. Smart contracts on blockchain automate fund movements under predefined conditions-a remittance to a sanctioned jurisdiction automatically blocks, while transfers meeting risk thresholds trigger real-time alerts to compliance teams. This reduces false positives that plague manual review systems. Project Nexus, the BIS-led initiative connecting instant payment systems across India, Malaysia, Philippines, Singapore, and Thailand, demonstrates how standardized compliance frameworks across borders eliminate the regulatory whiplash that currently delays transfers. Institutions implementing blockchain-based compliance report 60–70% reductions in manual review time while maintaining or improving detection accuracy. The immutable ledger creates an audit trail that satisfies regulators without requiring separate reconciliation systems, directly addressing the manual reconciliation nightmare that enterprise clients currently face.

Why Institutional Adoption Accelerates the Shift

The competitive advantage in cross-border payments has already shifted from who owns the payment rails to who can orchestrate liquidity and settlement across multiple rails. This shift explains why major financial institutions now test and deploy blockchain solutions. When DBS launched blockchain-enabled services integrated with core payment engines, the bank proved that distributed ledgers work alongside existing infrastructure rather than replacing it. Institutions gain the ability to offer clients faster settlement, lower costs, and transparent transaction records-all without abandoning their current systems. This hybrid approach removes the false choice between innovation and stability, making blockchain adoption practical for risk-averse financial organizations. As more institutions connect their blockchain infrastructure to shared ledgers, liquidity pools deepen and settlement becomes faster across more corridors. The network effects compound: each new institution joining increases the value for all participants, accelerating the transition away from correspondent banking bottlenecks.

The shift toward embedded compliance and real-time settlement creates new opportunities for businesses that can integrate blockchain infrastructure with their existing operations. The next section examines how stablecoins and regulatory frameworks make this integration viable at scale.

Stablecoins and Compliance Move Blockchain Payments into Production

Stablecoins transformed from speculative assets into operational infrastructure for cross-border remittances. In 2025, the majority of major cross-border payments companies launched stablecoin-based solutions, with USDC and USDT competing as the primary USD-pegged options. The Clarity for Payment Stablecoins Act, signed into law on July 18, 2025, removed regulatory uncertainty that previously blocked institutional adoption, and CEOs of major US banks immediately signaled interest in stablecoin corridors for enterprise payments. This shift matters because stablecoins enable faster, lower-cost cross-border transfers compared to traditional payment methods. A family sending $500 monthly through a stablecoin rail now pays significantly less in fees than through correspondent banking. Stablecoins settle on blockchain in minutes while maintaining fiat value, removing both the speed penalty of traditional banking and the volatility risk of speculative cryptocurrencies. DBS and other institutional players integrated stablecoin settlement directly into their core payment engines, proving the infrastructure works at institutional scale. When selecting a stablecoin corridor, prioritize liquidity depth and regulatory clarity in both sending and receiving jurisdictions. USDC offers broader geographic coverage through Circle’s partnerships, while USDT maintains higher volume on many corridors. Both serve different use cases, and financial institutions increasingly offer both options to clients rather than betting on a single standard.

How Compliance Automation Removes Remittance Delays

Embedded compliance within blockchain payments addresses the regulatory fragmentation that currently blocks cross-border transactions. Traditional systems require manual KYC verification, sanctions screening against OFAC and EU lists, and beneficial ownership documentation-processes that add 5–15 business days to settlement. Blockchain systems execute these checks inline through smart contracts before funds move, creating immutable records that satisfy regulatory audits without separate reconciliation. The shift from post-event compliance to real-time embedded verification reduces false positives because structured data on blockchain eliminates the free-text fields and transliteration errors that plague manual screening. Project Nexus demonstrates this in practice: standardizing compliance requirements across India, Malaysia, Philippines, Singapore, and Thailand removed the regulatory whiplash that previously delayed transfers between these corridors. Enterprise clients implementing blockchain-based compliance report that manual review time drops significantly. The immutable audit trail on blockchain creates a complete record of who initiated the transaction, where funds came from, and where they went-information that regulators increasingly demand but that traditional banking systems struggle to provide without expensive data consolidation. Financial institutions must implement robust governance upfront: establish clear KYC procedures aligned with FATF Recommendation 16, maintain centralized compliance data across jurisdictions, and use machine learning to detect anomalies in transaction patterns rather than relying on rule-based systems that generate excessive false positives.

Building Enterprise Payment Infrastructure That Scales

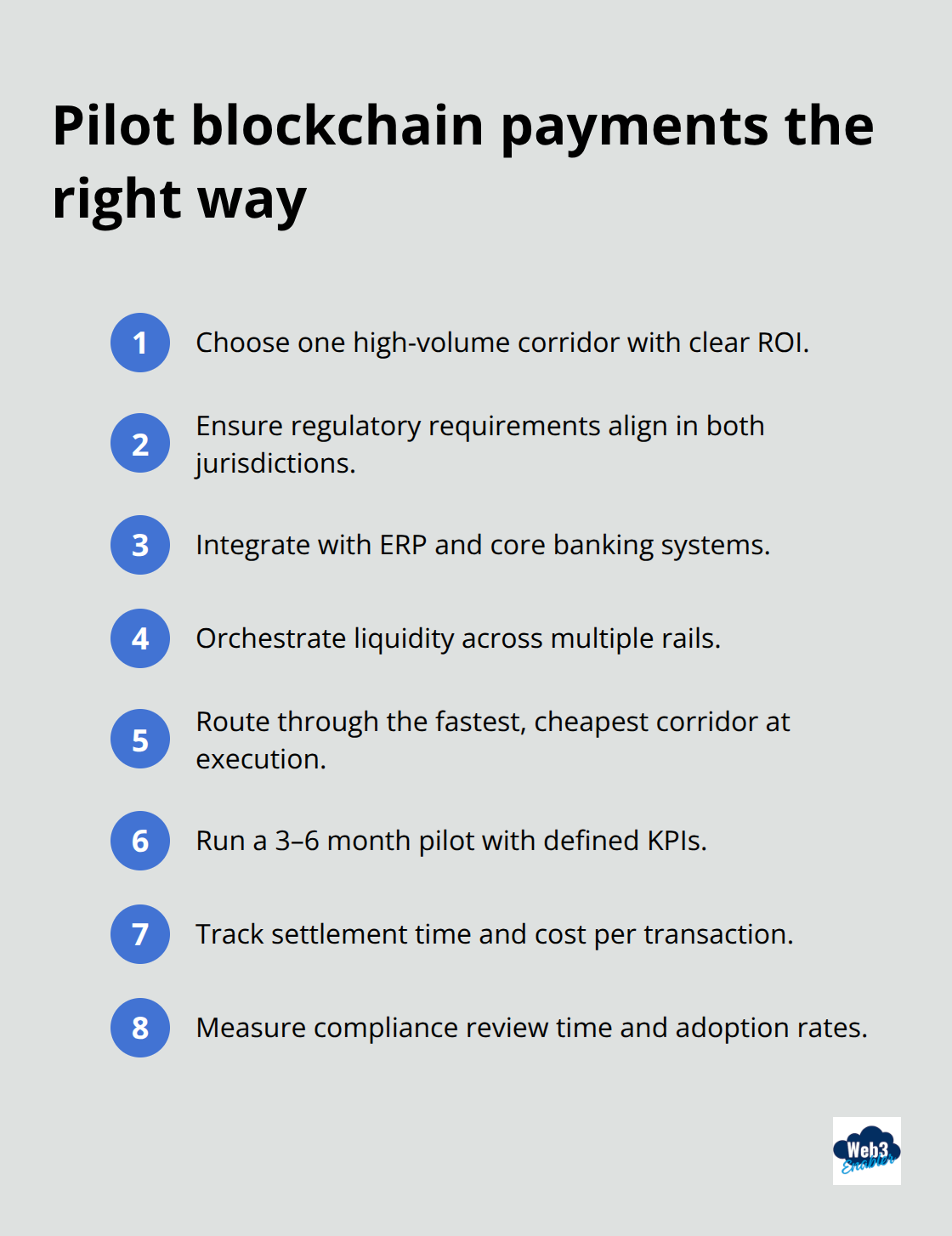

Enterprise solutions for cross-border payments require more than stablecoin connectivity-they demand integration with existing ERP systems, liquidity management across multiple corridors, and the ability to scale from pilot to millions of transactions without proportional increases in compliance staff. Institutions that treat blockchain as a parallel system rather than integrated infrastructure consistently fail at scale because compliance, reconciliation, and operational risk management remain fragmented. The competitive advantage now flows to institutions that orchestrate liquidity across multiple payment rails simultaneously, routing transactions through the fastest and cheapest corridor available at execution time. A financial institution managing payments to 50 countries needs real-time visibility into liquidity, FX rates, and regulatory requirements across each corridor-information that traditional banking systems provide days after settlement. Blockchain-native infrastructure provides this visibility in real time, enabling finance teams to optimize settlement timing and currency conversion strategy. Start with a single, high-volume corridor where ROI is clear and regulatory requirements are aligned. Singapore-to-India or Philippines-to-US payments show clear cost reduction compared to correspondent banking, making these corridors ideal pilots. Run the pilot for 3–6 months with clear KPIs: measure settlement time reduction, cost per transaction, compliance review time, and customer adoption rates.

Only after validating these metrics should institutions expand to additional corridors. The technical architecture matters less than integration with existing systems-a blockchain solution that requires separate reconciliation, compliance review, and customer interfaces adds operational complexity rather than reducing it. Solutions that integrate directly with core banking systems, ERP platforms, and compliance tools win because they reduce the total cost of operations while improving speed.

Final Thoughts

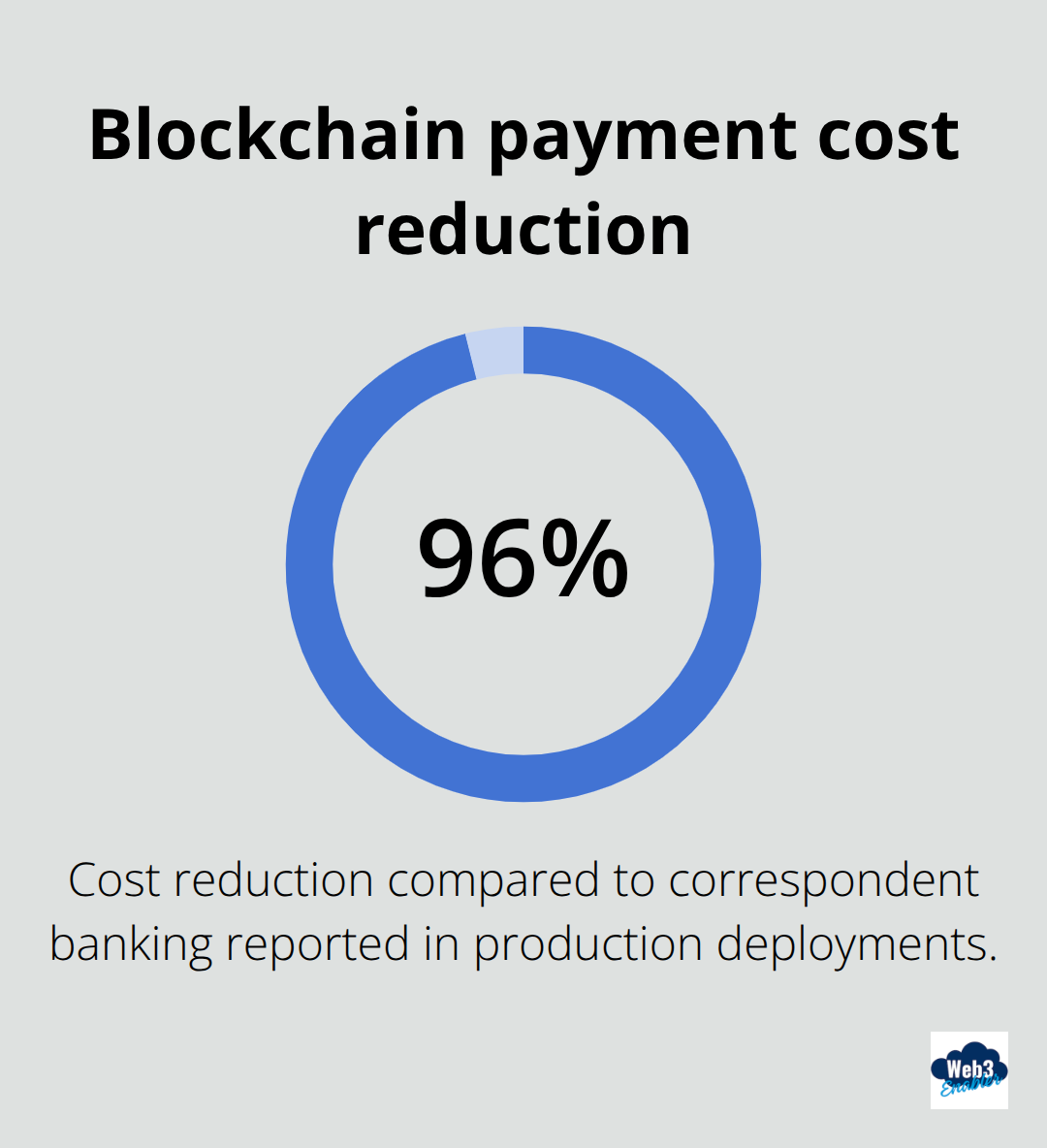

Cross-border blockchain payments have moved beyond pilot phase into operational reality, with institutions reporting settlement times under 10 minutes and cost reductions up to 96% compared to correspondent banking. Embedded compliance verification within blockchain transactions addresses the regulatory fragmentation that has blocked remittances for decades, while immutable audit trails satisfy regulatory requirements without separate reconciliation systems. Real barriers remain-regulatory harmonization across jurisdictions stays incomplete, and achieving instantaneous atomic swaps across currencies requires universal trust that does not yet exist.

Stablecoin corridors now offer clear ROI on high-volume payment routes like Singapore-to-India or Philippines-to-US, making the opportunity immediate for businesses ready to move beyond correspondent banking bottlenecks. Start with a single corridor, measure settlement time reduction and cost per transaction over 3–6 months, then expand to additional routes as your team gains confidence with the infrastructure. Financial advisors gain new value by providing clients visibility into blockchain payment options and helping them optimize settlement timing across multiple corridors.

We at Web3 Enabler help organizations integrate blockchain infrastructure directly with Salesforce and core banking systems, enabling stablecoin payments and compliance automation without requiring separate platforms. Web3 Enabler provides the infrastructure to connect cross-border blockchain payments with your existing operations when your organization is ready to scale beyond traditional banking constraints.

Frequently Asked Questions About Cross-Border Blockchain Payments

These FAQs explain how cross-border blockchain payments work for remittances, how fees and settlement times compare to traditional rails, and what compliance requirements make them viable in real-world use.

What are cross-border blockchain payments?

Cross-border blockchain payments move value internationally using a distributed ledger, often via stablecoins. Instead of routing through multiple correspondent banks, funds transfer wallet-to-wallet on-chain with verifiable settlement records.

Why do traditional remittances still cost 5–7% in fees?

Fees come from multiple layers: correspondent bank charges, payment provider fees, FX spreads, and receiving bank fees. When a transfer passes through several intermediaries, each layer can add cost and delay.

How does blockchain reduce remittance fees?

Blockchain reduces fees by eliminating intermediary hops and enabling direct settlement on a shared ledger. With stablecoins, value transfer can avoid repeated FX conversions and reduce processing overhead.

How fast are blockchain remittances compared to bank transfers?

Traditional cross-border transfers often take days due to batching, cut-off times, and correspondent routing. Blockchain transfers can confirm in minutes (or faster depending on the network) and operate 24/7, including weekends and holidays.

Why are stablecoins used instead of volatile cryptocurrencies?

Stablecoins are designed to track fiat value, which makes them more practical for remittances and business payments. They combine faster settlement with lower price volatility than assets like BTC or ETH.

Are blockchain payments compliant with KYC and AML requirements?

They can be, but compliance depends on how the payment flow is implemented. Production-grade solutions typically include identity verification, sanctions screening, transaction monitoring, and audit-ready records tied to counterparties and purpose of payment.

What compliance frameworks matter most for cross-border blockchain payments?

Most programs align to standard financial crime controls: KYC, sanctions screening (for example OFAC lists where applicable), AML monitoring, and travel-rule style requirements where required. The key is embedding these checks into the workflow instead of treating them as after-the-fact steps.

Do blockchain payments provide better transparency than traditional remittances?

Yes. On-chain transactions produce a timestamped, verifiable trail that both sender and receiver can confirm. This reduces “where is my money” uncertainty and supports stronger auditability when paired with compliant customer data.

What are the main risks with cross-border blockchain payments?

Common risks include operational mistakes (sending to the wrong address), regulatory differences by jurisdiction, liquidity constraints in certain corridors, and vendor controls. Strong governance, verified payment instructions, and monitored rails reduce these risks.

How should a business start using cross-border blockchain payments?

Start with one high-friction corridor where fees and settlement delays are clearly painful, define success metrics (cost per transfer, settlement time, exceptions rate), and expand only after the process is repeatable with controls and reporting in place.

How does Web3 Enabler support cross-border blockchain payments?

Web3 Enabler connects blockchain payment activity to enterprise workflows so teams can manage settlement status, records, and audit trails inside Salesforce rather than juggling external tools. This helps reduce reconciliation effort and improves visibility across payment operations.