Digital currency is reshaping how we think about money, but most people still scratch their heads when asked for a clear digital currency definition.

We at Web3 Enabler see businesses wrestling with this shift daily. The good news? It’s not as complicated as the tech bros make it sound.

This guide breaks down everything you need to know about digital money without the jargon overload.

What Exactly Is Digital Currency

Digital currency is electronic money that exists only in digital form, without physical bills or coins. Think of it as the evolution of money from metal coins to paper bills to numbers on a screen. The global cryptocurrency market has reached approximately $4.12 trillion as of September 2025, with over 35,186 different types of digital currencies available. Unlike the digital numbers in your bank account that represent physical dollars, true digital currencies exist independently of traditional banks and operate on distributed networks.

The Real Difference From Your Bank Account

Your online bank shows digital representations of physical money, but digital currencies are native digital assets. When you transfer $100 through your bank app, that money still relies on central banks, takes 1-5 business days to settle, and costs institutions an average of $6 million per data breach (according to IBM’s 2024 Cost of a Data Breach Report). Digital currencies settle in seconds to minutes, operate 24/7 without bank holidays, and use cryptographic security instead of centralized systems. Cross-border payments through traditional banks cost 4-6% in fees, while blockchain-based digital currencies can cost as little as 0.1% to 2%.

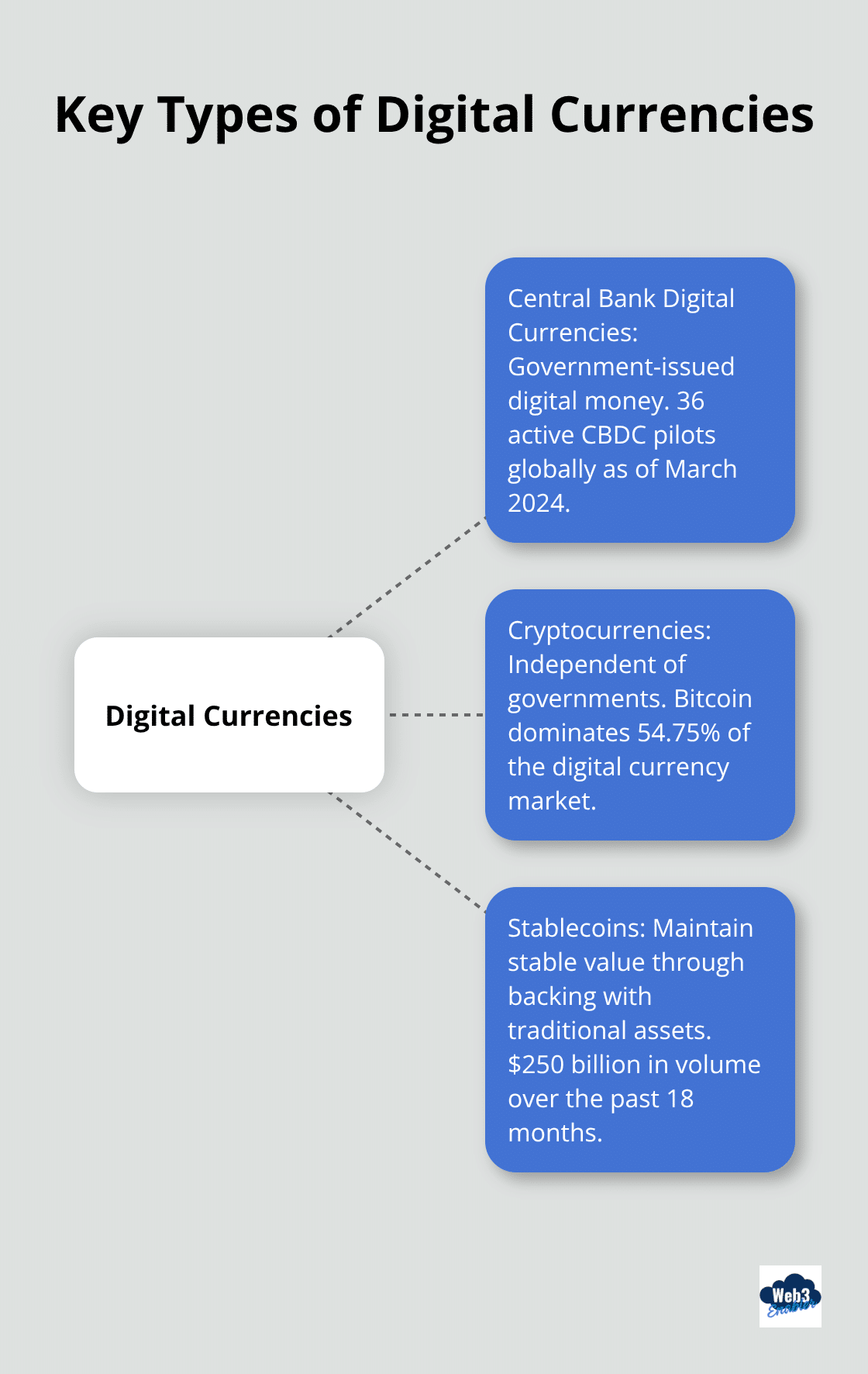

Three Types That Actually Matter

Central Bank Digital Currencies represent government-issued digital money, with countries like Jamaica, Nigeria, and The Bahamas already launching their versions. As of March 2024, there are 36 active CBDC pilots globally. Cryptocurrencies like Bitcoin, which dominates 54.75% of the digital currency market, operate independently of governments. Stablecoins have surged to $250 billion in volume over the past 18 months because they maintain stable value through backing each digital token with traditional assets like US dollars, which makes them practical for business transactions without the wild price swings that make headlines.

How These Digital Assets Function

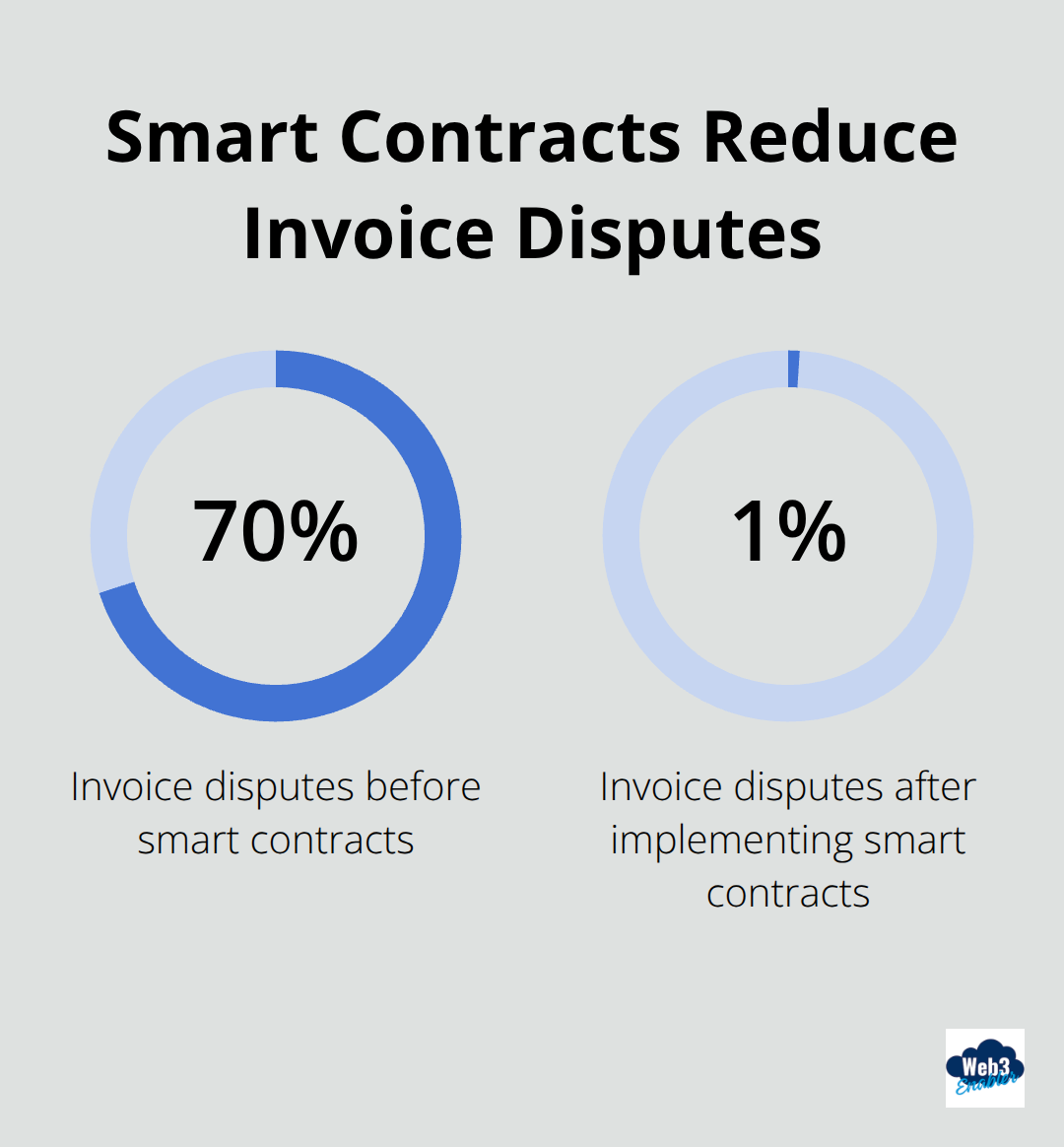

Digital currencies operate through distributed networks rather than single institutions. Each transaction gets verified through consensus mechanisms that prevent fraud and double-spending. The immutable nature of blockchain transactions leads to near-zero chargebacks, which improves transaction reliability significantly. Smart contracts can automate payment processes (Walmart Canada reduced invoice disputes from 70% to 1% through this technology). This automation removes intermediaries and reduces costs while maintaining security through cryptographic verification.

Now that you understand what digital currency is, let’s explore the technology that makes it all possible.

How Does Digital Currency Actually Process Transactions

Digital currency transactions move through blockchain networks that verify each payment through distributed consensus rather than central authorities. When you initiate a digital currency transfer, the network broadcasts your transaction to thousands of nodes that validate the payment details, check account balances, and confirm authenticity through cryptographic signatures. Bitcoin’s network currently processes transactions at 851 exahashes per second, while Ethereum maintains security through over 35.7 million staked ETH across more than one million validators. This distributed verification eliminates the single points of failure that plague traditional systems (where IBM reports financial institutions face an average of $6 million per data breach).

Digital Wallets Store Your Access Keys

Digital wallets don’t actually store currencies but manage the cryptographic keys that prove ownership of digital assets on the blockchain. Hot wallets connect to the internet for convenient transactions but carry higher security risks, while cold wallets remain offline for maximum protection of larger assets. Each wallet creates unique addresses for payment receipt, and private keys must remain secure since anyone with access can control the associated funds. Professional wallet solutions offer multi-signature requirements, where multiple parties must approve transactions (banks like JPMorgan use this to reduce loan approval times by 30 percent through automated verification processes).

Security Through Mathematical Proof

Digital currencies achieve security through advanced cryptography rather than institutional trust. Each transaction creates an irreversible mathematical proof that becomes permanently recorded across the distributed network, which makes retroactive changes virtually impossible without majority network control. The Bank of England’s pilot programs demonstrate that blockchain implementations can yield up to 70 percent savings on cross-border payments while they maintain superior security compared to traditional correspondent networks. Hash functions convert transaction data into unique digital fingerprints, and any attempt to alter transaction details produces completely different fingerprints that the network immediately rejects.

Transaction Speed Beats Traditional Systems

Traditional payment systems take 1-5 business days to settle, but digital currencies complete transactions in seconds to minutes around the clock. Cross-border payments through banks cost 4-6% in fees, while blockchain-based transfers cost as little as 0.1% to 2%. The immutable nature of blockchain transactions leads to near-zero chargebacks, which improves transaction reliability significantly compared to traditional payment methods that banks struggle to secure.

While the technology handles transactions efficiently, businesses need practical ways to integrate these payment systems into their operations.

What Are the Real Benefits and Risks

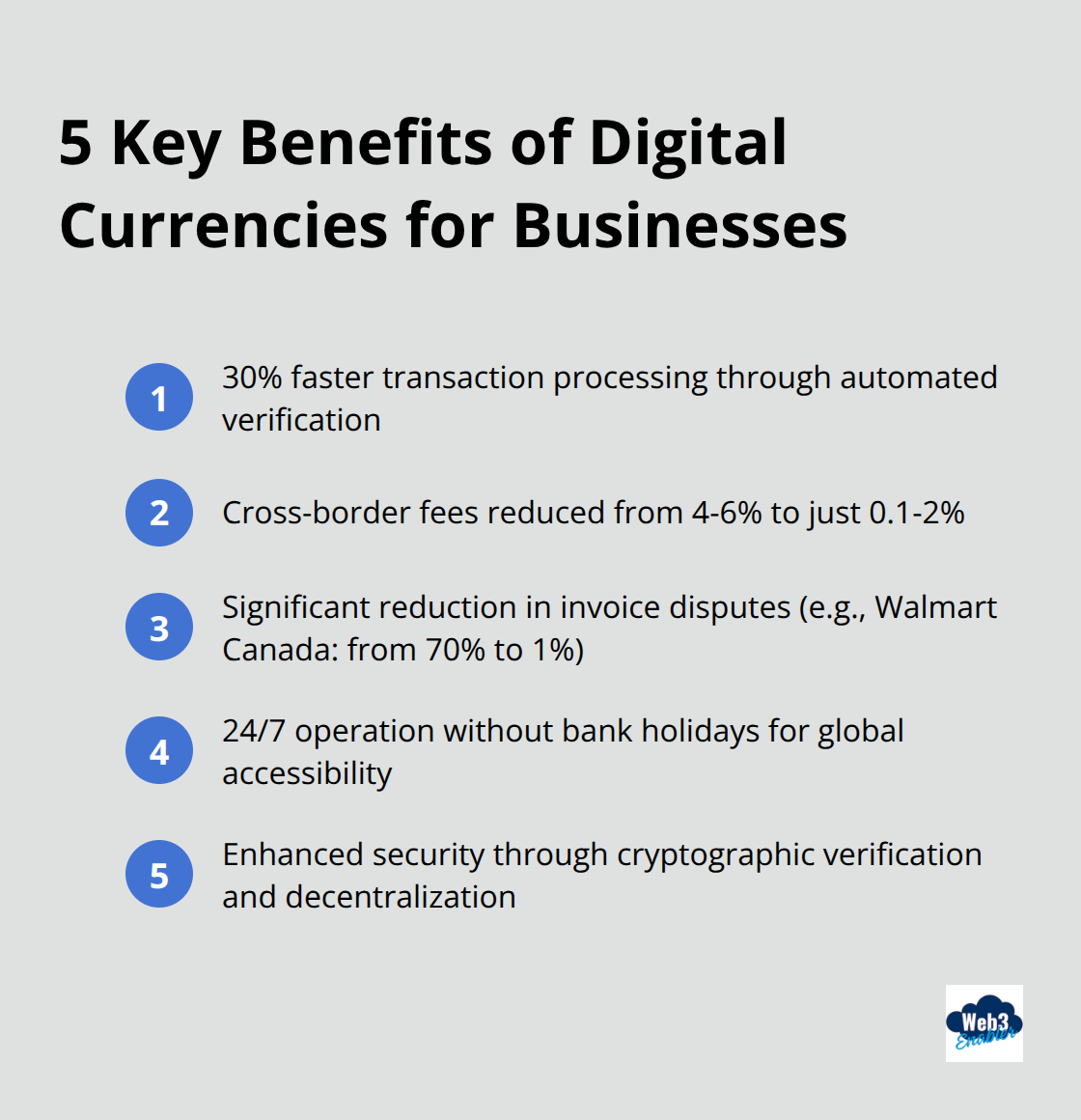

Digital currencies deliver measurable business advantages that traditional payment systems cannot match. While businesses explore crypto adoption, consumer concerns about data privacy and security remain significant, with 70% of respondents in Deloitte’s 2025 survey expressing worries about digital services. Businesses that use blockchain payment solutions report 30% faster transaction processing through automated verification, while cross-border fees drop from 4-6% to just 0.1-2%. The NOWPayments platform supports over 300 cryptocurrencies with fees of only 0.5% per transaction compared to traditional processors. Smart contracts eliminate manual processes and reduce disputes significantly – Walmart Canada cut invoice disputes from 70% to 1% through automated payment verification. Stablecoin volumes reached $250 billion in the past 18 months because they provide price stability while they maintain the speed and cost advantages of digital currencies.

Security Challenges Demand Professional Management

Digital currency adoption faces legitimate security concerns that businesses must address proactively. The decentralized nature eliminates single points of failure but transfers responsibility to individual users and organizations. Private key management becomes critical since lost keys mean permanently inaccessible funds with no recovery mechanism. Professional wallet solutions with multi-signature requirements and cold storage protocols mitigate these risks, but implementation requires technical expertise. However, 2023 data from Chainalysis shows illicit cryptocurrency transactions accounted for only 0.34% of total volume (which demonstrates that security concerns often exceed actual risks when proper protocols are implemented).

Regulatory Landscape Shifts Toward Clarity

The regulatory environment for digital currencies stabilizes as governments recognize their economic potential. President Biden’s Executive Order initiated national strategy development for digital currencies, while the Federal Reserve researches CBDC implementation to improve payment system efficiency. Market structure bills under Senate discussion aim to clarify regulatory roles and reduce the current enforcement-heavy approach. Exchange-traded funds for cryptocurrencies are expected to gain approval, potentially increasing institutional investment significantly. Forward-thinking businesses that engage proactively with evolving compliance requirements gain competitive advantages over those who wait for complete regulatory certainty.

Implementation Costs Vary Across Solutions

Traditional payment systems cost financial institutions an average of $6 million per data breach, while blockchain eliminates single points of failure through decentralization. Initial setup costs for digital currency integration range from simple payment processors to complex enterprise solutions. The broader blockchain technology market projects expansion from $31 billion in 2024 to over $390 billion by 2030 (reflecting its increasing importance across industries). McKinsey predicts stablecoin usage will rise to $2 trillion by 2028, which showcases major growth trajectory for digital currencies in business applications.

Final Thoughts

Digital currency adoption accelerates as businesses recognize practical advantages over traditional payment systems. Deloitte reports that 40% of large companies plan to accept crypto payments within the next two years, while stablecoin volumes reached $250 billion in the past 18 months. The digital currency definition continues to evolve from speculative asset to legitimate business tool, with McKinsey predicting stablecoin usage will rise to $2 trillion by 2028.

The regulatory landscape shifts toward clarity as governments develop frameworks that support innovation while maintaining security. Exchange-traded funds for cryptocurrencies expect approval, potentially increasing institutional investment significantly. The broader blockchain technology market projects expansion from $31 billion in 2024 to over $390 billion by 2030 (reflecting massive industry growth potential).

Smart businesses choose the right implementation partner to navigate this transformation successfully. Web3 Enabler provides Salesforce Native blockchain solutions available on the AppExchange, which enables businesses to accept stablecoin payments and send global payments faster within existing corporate infrastructure. The question isn’t whether digital currencies will reshape business payments, but how quickly your organization will adapt to this inevitable shift.