Your international payments are stuck in the 1990s. Wire transfers take days, fees eat into margins, and tracking money across borders feels like solving a puzzle with missing pieces.

We at Web3 Enabler built a USDC payments workflow that changes this. Settlements happen in minutes instead of days, costs drop dramatically, and your customer data stays perfectly synced throughout the process.

Why USDC Actually Saves Money

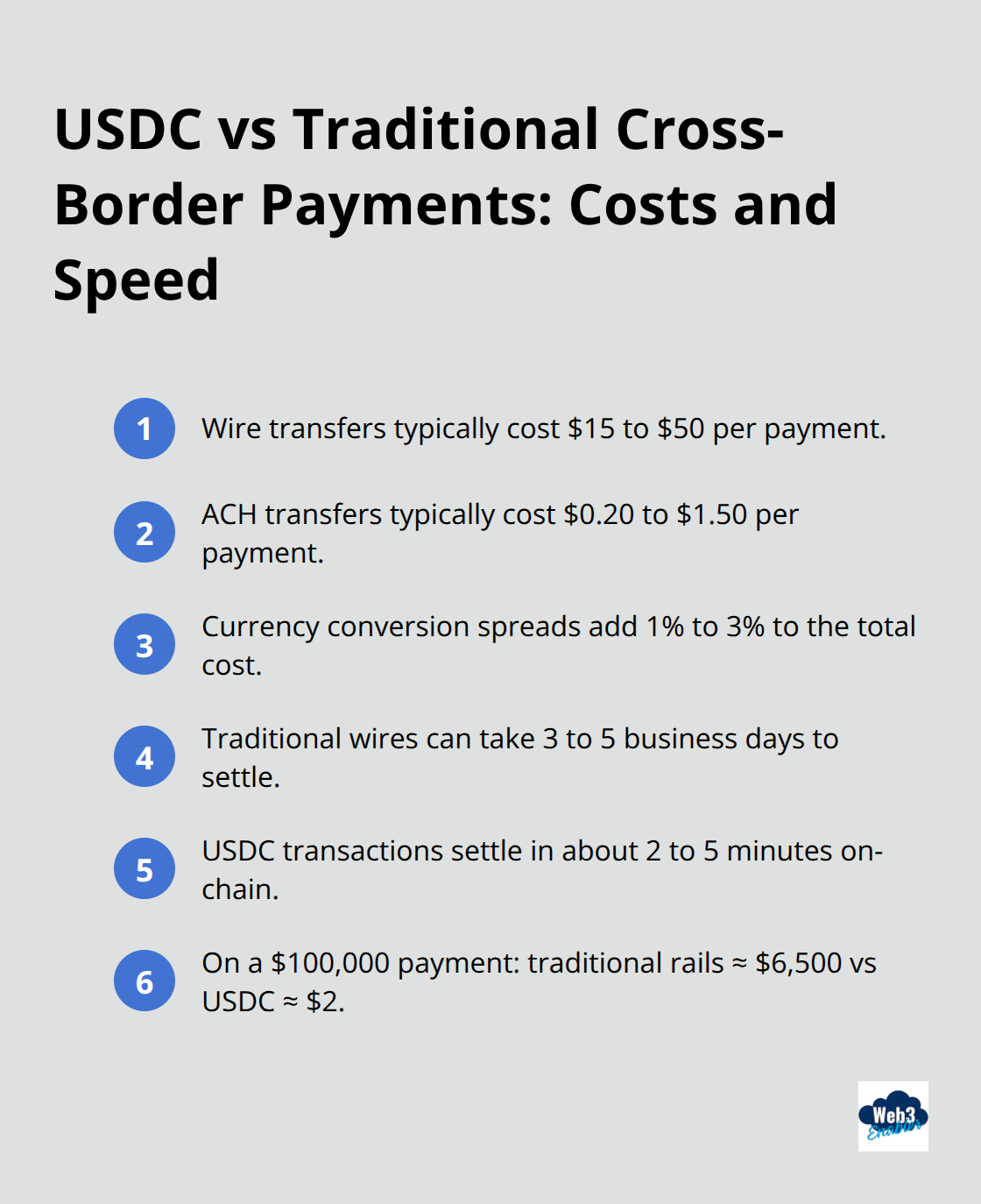

Traditional cross-border payments cost far too much. A wire transfer runs $15 to $50, ACH transfers cost $0.20 to $1.50, and that’s before hidden expenses pile on. Currency conversion spreads add another 1-3%, and if your payment gets stuck in correspondent banking, you wait 3-5 business days while your money sits idle.

Remittances average 6.5% in total costs per transaction. USDC settlements, by contrast, cost just a few cents in network fees and settle in 2-5 minutes on Ethereum or other blockchains. For a $100,000 international payment, traditional rails cost you roughly $6,500 in fees and delays. USDC costs you about $2. That’s not hyperbole-that’s math.

Speed Compounds Across Your Operations

Speed matters because your cash flow depends on it. When you send money via wire, it vanishes into the banking system for days. With USDC, settlement becomes instant and final within minutes. This speed compounds when you manage global operations. If you pay international vendors, process global payroll, or handle marketplace payouts across multiple regions, those minutes add up fast. Your treasury team no longer needs to pre-fund regional wallets or maintain cash buffers in multiple countries. USDC enables just-in-time transfers, meaning you move money exactly when you need it, not days before. For businesses processing hundreds of payments monthly across borders, this cuts working capital requirements significantly and improves cash flow predictability.

Compliance Integrates, Not Complicates

The compliance conversation around stablecoins has shifted dramatically. USDC is fully regulated and issued by Circle with a 1:1 reserve backing every token. KYC and AML requirements still apply, but they integrate into your existing workflows rather than creating parallel processes. This matters because auditors want traceable, transparent transactions, and blockchain delivers exactly that. Every USDC transfer creates an immutable record, down to the second, with full visibility into who paid whom and when. No more chasing down wire confirmations or reconciling bank statements manually. The emerging regulatory framework (including the GENIUS Act in the US and MiCA in the EU) pushes stablecoin issuers toward bank-like standards, which benefits users like you. Your money becomes safer, more transparent, and more compliant than before.

What Happens Next in Your Workflow

Now that you understand why USDC payments make financial sense, the real question becomes how to actually implement them. Your existing systems-your CRM, your ERP, your treasury software-don’t need to be ripped out and replaced. Instead, they connect to USDC infrastructure through APIs and integrations that sit on top of what you already use. The next section shows you exactly how to build this workflow within Salesforce, automating settlement processes while keeping your customer data perfectly synced throughout the entire transaction.

Building Your USDC Payment Workflow in Salesforce

Connect USDC Without the Technical Headaches

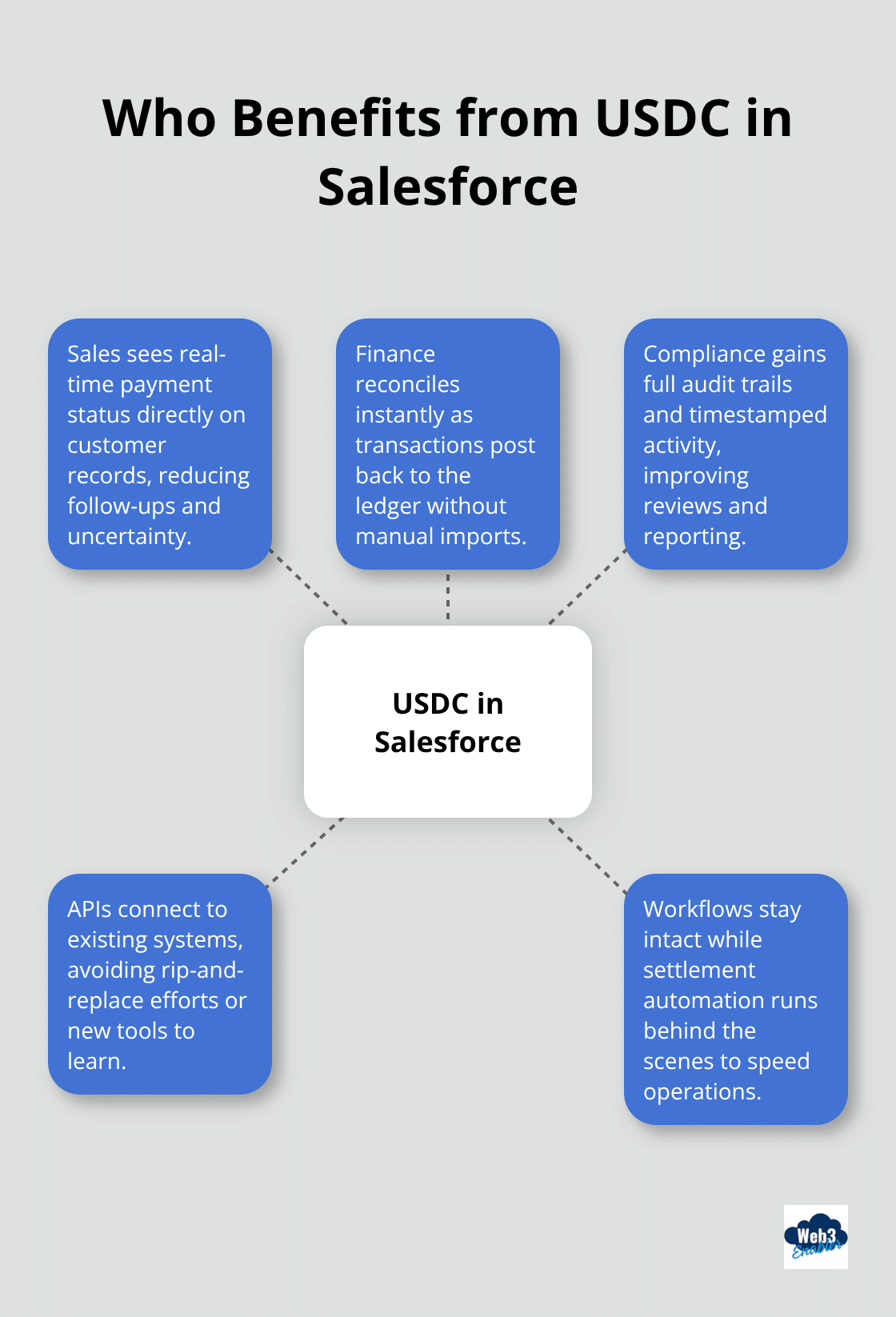

Connecting USDC to your Salesforce environment sounds technical, but the reality is straightforward. Your payment acceptance lives inside Salesforce, where your customer records already sit. When a customer pays in USDC, the transaction data flows directly into your existing customer database. Your sales team sees the payment status in real time. Your finance team reconciles it instantly. Your compliance team has full audit trails without extra work.

The integration works because it respects your existing workflows instead of forcing you to build new ones around blockchain.

Start Small, Scale Smart

Start with a single use case, like paying international vendors or processing marketplace payouts. Don’t try to move everything to USDC on day one. Choose one payment scenario where speed and cost savings matter most, then build from there. Institutional stablecoin infrastructure is mature enough for serious business use, with 55 financial institutions enrolled in Circle Payments Network. This maturity means you can test USDC payments in a low-risk environment before expanding across your entire operation.

Automate Settlement Processes End-to-End

Settlement automation is where USDC really flexes. Traditional payments require manual intervention at multiple points: approval workflows, payment initiation, confirmation, reconciliation. USDC settlements compress this into a single automated process triggered by your existing business logic. Modern Treasury’s stablecoin feature processes USDC payments in 2 to 5 minutes compared to 1 to 3 business days for ACH, all while costing only network fees rather than $15 to $50 per wire transfer.

Your ERP system can trigger payments when delivery confirmations hit your database. Your payroll system can execute global payroll in minutes instead of coordinating across multiple banks. Your treasury team sets guardrails like per-merchant limits, daily spend caps, and approval thresholds, then lets automation handle execution. This isn’t about removing human oversight. It’s about removing the tedious manual steps that slow everything down.

Scale With Proven Infrastructure

That scale means infrastructure is stable and proven. Your compliance team still owns KYC and AML requirements, but those integrate into your payment setup once, not repeated for every transaction. Address whitelisting, dual approvals for high-value transfers, and detailed audit logs become part of your standard operating procedure.

Settlements happen 24/7/365, which matters when your business operates globally and your vendors don’t work on your timezone. This always-on capability eliminates the coordination headaches that plague traditional banking. Your money moves when you need it to move, not when bank hours align.

Sync Customer Data Throughout the Transaction

Every USDC transfer creates an immutable record with full visibility into who paid whom and when. No more chasing down wire confirmations or reconciling bank statements manually. Your customer data stays perfectly synced throughout the entire process because the payment system and your CRM speak the same language. This synchronization eliminates duplicate data entry, reduces reconciliation errors, and gives your team a single source of truth for every transaction.

The next section shows you real-world examples of how businesses are actually using USDC to cut payment times from days to minutes and what those cost savings look like across different industries.

Real-World Examples of USDC Automation

Technology Companies Cut Vendor Payments from Days to Minutes

Technology companies discovered USDC settlements first. Instead of waiting 3-5 business days for wire transfers to clear, they send USDC and watch funds arrive in minutes. A software firm paying developers across 12 countries reduced payment processing time from 72 hours to 4 minutes per transaction.

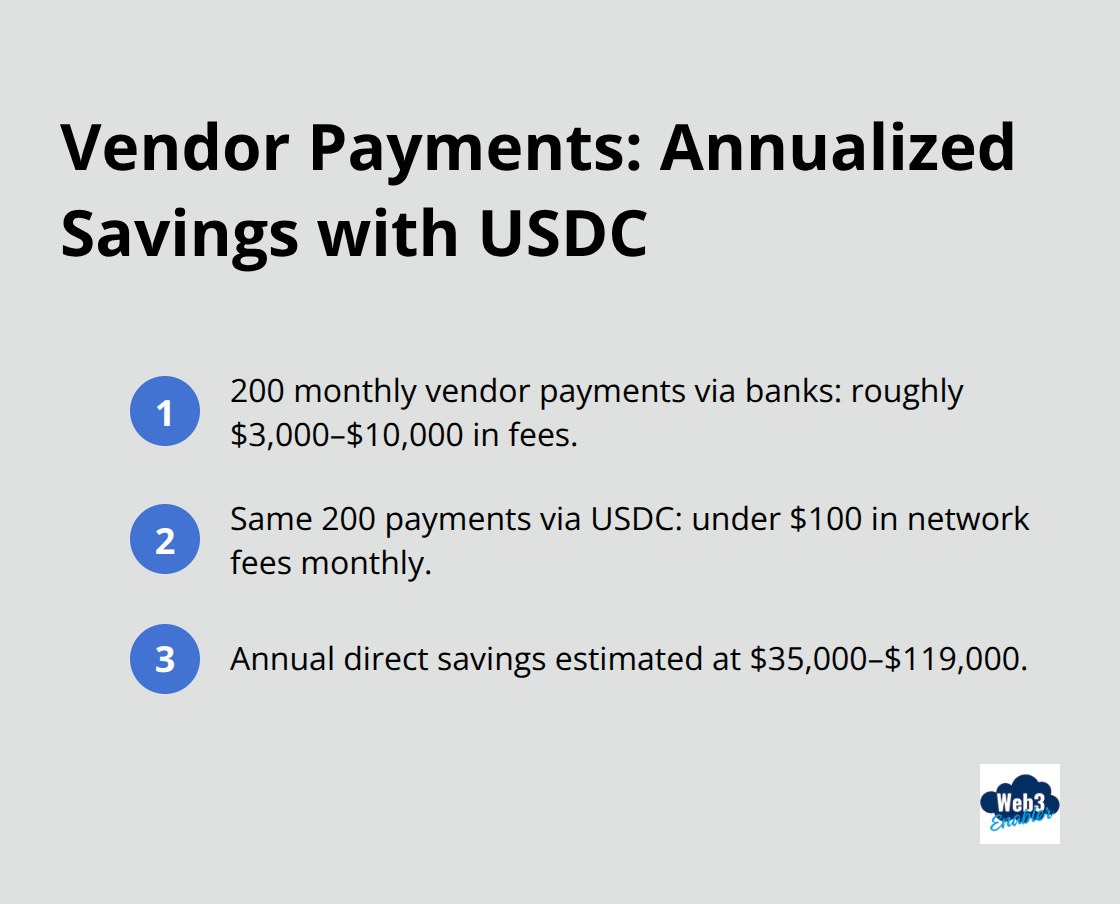

That speed compounds quickly. Processing 200 international vendor payments monthly costs roughly $3,000 to $10,000 in fees through traditional banking, plus the working capital cost of money sitting in transit. The same 200 payments in USDC cost under $100 in network fees. Over a year, that saves $35,000 to $119,000 in direct costs.

Intuit embedded USDC into its platform because businesses demanded faster settlement for real-time payments. Finance teams set up a payment in their existing system, it settles in USDC, and the money arrives instantly. No blockchain wallet management required. No technical expertise needed.

Visa now allows settlement using USDC through its network, signaling that major payment infrastructure treats stablecoin settlements as standard business practice.

Global Payroll Systems Eliminate Regional Bank Accounts

Companies paying remote teams across multiple continents historically maintained separate bank accounts in each region, pre-funding them monthly and absorbing currency conversion costs averaging 1-3%. USDC payroll automation eliminates this entirely.

A design agency paying 45 contractors across 18 countries moved to USDC payroll settlement and cut processing overhead by roughly 60%. Payments that once required coordinating across multiple banks now happen automatically on a schedule. Contractors receive funds 24 hours faster than traditional banking allows.

The finance team spends zero time managing correspondent banking relationships or currency hedging. Settlement happens 24/7/365, which matters when your business operates globally and your vendors don’t work on your timezone.

Marketplace Operators Solve Seller Payout Delays

Marketplace operators handling seller payouts discovered USDC automation solved their biggest operational headache. A peer-to-peer commerce platform paying 10,000 sellers monthly faced constant complaints about settlement delays. Traditional ACH transfers took 1-3 business days, and international sellers waited longer.

The company deployed USDC payouts and cut settlement time to 2-5 minutes. Seller satisfaction improved dramatically because payment uncertainty disappeared. Sellers knew exactly when funds arrived instead of checking bank accounts repeatedly.

The platform’s operations team reduced manual reconciliation work by 70% because USDC transactions create immutable records with zero ambiguity. Cost savings proved substantial too. At $0.50 average network fee per transaction versus $0.20-$1.50 for ACH plus $15-$50 for international wires, the math heavily favors USDC for cross-border payments.

The platform processed roughly 50,000 seller payouts monthly. USDC cost them $25,000 annually in network fees. Traditional banking would have cost $100,000 to $300,000 in fees plus operational overhead.

Treasury Teams Gain Real-Time Visibility Across Entities

Treasury teams managing multi-entity fund transfers found USDC created unprecedented visibility. A financial services company with subsidiaries across Europe, Asia, and North America historically struggled with real-time cash position reporting. Money moved through correspondent banking channels with opacity and delays.

USDC settlement provided instant, auditable transfers with transparent on-chain records. The treasury team gained real-time visibility into exactly where funds sat across all entities. Cash flow forecasting became accurate instead of probabilistic.

They eliminated the need to maintain excess cash reserves in multiple jurisdictions because USDC enabled just-in-time transfers. This isn’t fringe technology anymore. Institutional capital flows through USDC settlements because the speed and cost advantages are undeniable.

Final Thoughts

USDC payments aren’t theoretical anymore-they work right now in real businesses, cutting costs and accelerating operations that moved at banking speeds for decades. Your organization loses money every day you stick with traditional cross-border payments, as wire fees, currency spreads, and multi-day settlement delays compound into thousands of dollars annually. USDC settlements cost cents instead of dollars and finish in minutes instead of days, making the financial case undeniable.

Getting started requires no rip-and-replace of your existing systems. Your Salesforce environment, your ERP, and your treasury software all stay exactly where they are while you layer a USDC payments workflow on top through APIs that respect your current processes. Start with one use case where the pain cuts deepest-vendor payments, global payroll, or marketplace payouts-then measure results and expand. The infrastructure has matured: Circle’s network includes 55 financial institutions with 74 more under review, Visa settled transactions using USDC, and Intuit embedded it into their platform.

What happens next depends on your timeline and ambition. Some organizations move to USDC payments within weeks while others take months to build governance frameworks and compliance controls, yet both approaches work because USDC scales with your comfort level. Explore what Web3 Enabler can do for your organization if you’re ready to move faster and spend less on international payments.

FAQ: USDC Payments Workflow

Is USDC legally recognized for business payments in 2026?

Yes. Following the enactment of the GENIUS Act in July 2025, USDC is classified as a “permitted payment stablecoin” in the U.S. This federal framework mandates 1:1 reserve backing and monthly audits, giving CFOs the regulatory certainty needed to treat USDC as a standard financial rail rather than a crypto experiment.

How much can a business save by switching from Wires to USDC?

Traditional international wires typically cost between $15 and $50 per transaction, plus 1–3% in hidden currency conversion spreads. In contrast, USDC settlements on Layer-2 networks or the Circle Payments Network (CPN) cost only a few cents in gas fees. For a $100,000 global payment, a business can save over $6,000 in total fees and liquidity delays.

Does using USDC require our team to manage private keys?

Not necessarily. While some firms choose self-custody, most enterprises use custodial APIs from providers like Stripe or Modern Treasury. These platforms handle the technical “heavy lifting”—including key management and blockchain connectivity—allowing your team to interact with USDC through a familiar dashboard or CRM interface.

How does USDC integrate with Salesforce or our ERP?

USDC workflows are designed to be “invisible” to the end user. Through REST APIs, a USDC payment can automatically trigger a status update in Salesforce, reconcile an invoice in your ERP, and log the transaction in your accounting software simultaneously. This eliminates the manual “puzzle-solving” often required to track traditional cross-border wires.

Can we use USDC for global payroll without regional bank accounts?

Absolutely. One of the primary use cases in 2026 is just-in-time payroll. Instead of pre-funding dozens of local currency accounts weeks in advance, companies hold USDC centrally and execute payouts that settle in minutes. Contractors receive funds instantly and can convert them to local currency on their own schedule via integrated on-ramps.