Fiat collateralized stablecoins have become the backbone of digital payments, offering businesses a bridge between traditional finance and blockchain technology. These digital assets maintain their value by backing each token with real-world currency reserves.

Fiat collateralized stablecoins have become the backbone of digital payments, offering businesses a bridge between traditional finance and blockchain technology. These digital assets maintain their value by backing each token with real-world currency reserves.

We at Web3 Enabler see companies increasingly turning to stablecoins for faster, cheaper international transfers and streamlined payment processes. The market has exploded to over $150 billion in total value.

What Makes Fiat Collateralized Stablecoins Actually Stable

Think of fiat collateralized stablecoins as the responsible adults in the crypto playground. While Bitcoin swings wildly between $30,000 and $70,000, these digital assets stick stubbornly to their $1.00 target. The secret? Each token gets backed by actual dollars that sit in real bank accounts. Circle maintains reserves in cash and short-term U.S. Treasury bonds to back USDC, while Tether claims over $100 billion in reserves for USDT.

The Dollar-for-Dollar Promise

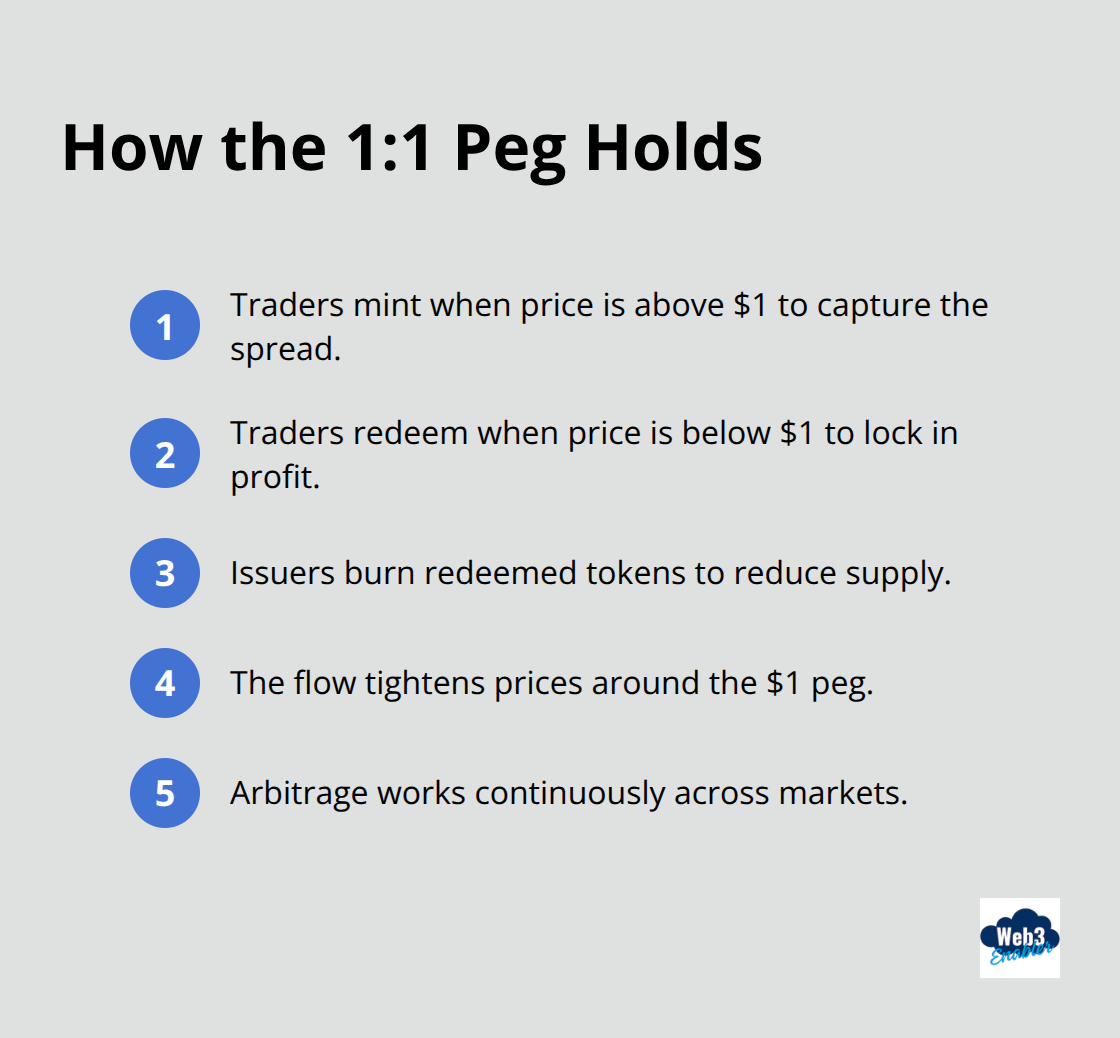

The mechanics are simple. Issue one token, deposit one dollar. Want to cash out? Burn the token, get your dollar back. This 1:1 reserve creates what economists call price stability through arbitrage. When USDC trades at $1.01, smart traders buy dollars, mint new USDC, and pocket the difference. When it drops to $0.99, they buy cheap USDC and redeem it for full dollars. This constant pressure keeps prices tight around the $1 peg.

Why Traditional Crypto Falls Short

Regular cryptocurrencies like Bitcoin derive value from speculation and adoption. No reserves, no assets, just pure market sentiment. Algorithmic stablecoins tried to maintain stability through code and failed spectacularly when TerraUSD collapsed in May 2022 (wiping out $60 billion). Commodity-backed stablecoins like PAX Gold work but face storage costs and liquidity issues.

The Fiat Advantage

Fiat-collateralized stablecoins win because dollars are liquid, widely accepted, and governments actually want people to use them. The Federal Reserve reported that stablecoin transaction volumes hit $14 trillion in 2024, which proves businesses prefer predictable value over crypto volatility.

Now that you understand how these digital dollars maintain their stability, let’s examine which players dominate this massive market and what sets them apart.

Major Fiat Collateralized Stablecoins in the Market

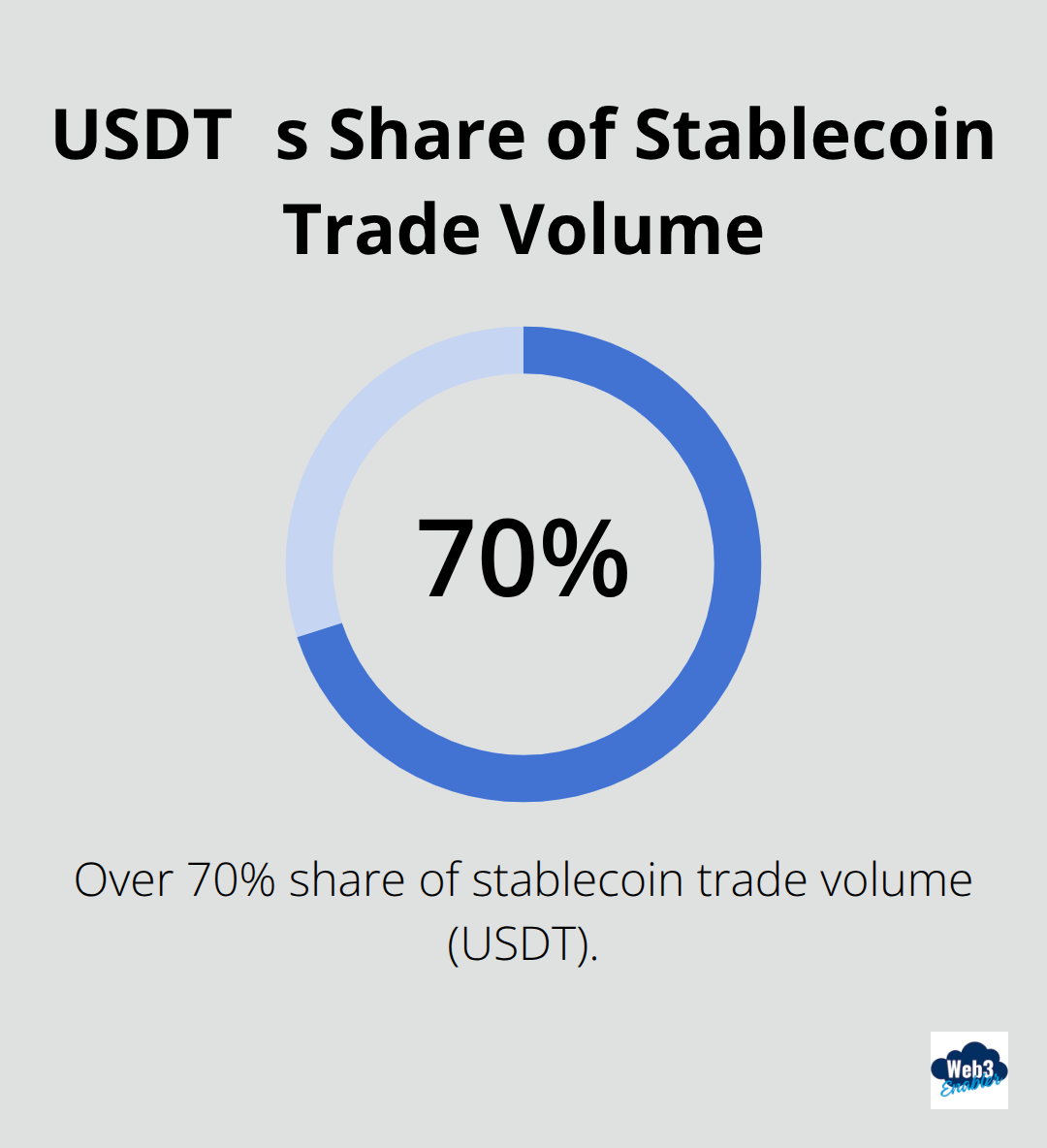

Tether dominates with USDT that commands over 70% of stablecoin trade volume despite constant regulatory scrutiny. The Commodity Futures Trading Commission fined Tether $41 million in 2021 for false claims about full dollar reserves, yet USDT remains the go-to choice for crypto exchanges worldwide. Tether processes roughly $50 billion in daily transactions but publishes reserve attestations quarterly rather than monthly audits. This opacity creates risk for businesses that require transparent financial instruments.

Circle Takes the Transparency Crown

Circle positions USDC as the compliance-first alternative with monthly attestation reports from Grant Thornton and reserves held exclusively in cash and short-term U.S. Treasury bonds. USDC holds the second-largest market share at roughly $30 billion in circulation. Circle went public through a SPAC merger and maintains bank partnerships with major institutions like Silvergate and Signature Bank. For businesses that prioritize regulatory compliance, USDC offers clearer audit trails and institutional-grade transparency that traditional finance teams actually understand.

The Supporting Cast Worth Your Attention

PayPal launched PYUSD in August 2023, backed by dollar deposits and short-term Treasuries, and targets mainstream adoption through its 400 million user base. Binance USD faced regulatory pressure and Circle stopped the creation of new BUSD tokens in February 2023. First Digital USD emerged as a Hong Kong-regulated alternative, while Gemini Dollar provides New York state oversight. These smaller players compete on specific features like geographic compliance or institutional custody (but lack the network effects that make USDT and USDC practical choices for most business applications).

Market Share Reality Check

The numbers tell a clear story about market concentration. USDT processes more daily volume than Visa’s entire payment network, while USDC captures most institutional demand from regulated businesses. The remaining stablecoins fight for scraps in a winner-take-all market where liquidity and acceptance matter more than technical features or regulatory promises.

These market dynamics create both opportunities and risks that businesses must weigh carefully when they consider stablecoin adoption for their payment systems.

Benefits and Risks of Fiat Collateralized Stablecoins

Cost Savings That Actually Matter

Stablecoins cut international transfer costs significantly compared to traditional banking fees, which saves companies thousands on cross-border payments. PayPal reported that businesses using PYUSD reduce settlement times from 3-5 days to minutes, while Visa processes $12 trillion annually compared to USDT’s $18 trillion in 2024 transaction volume. Companies like Shopify and Microsoft accept USDC payments because stablecoins eliminate chargeback fraud that costs merchants $31 billion yearly (according to Nilson Report data). The 24/7 settlement capability means businesses receive payments instantly rather than wait for banking hours, and programmable features allow automatic payment splits between vendors without manual intervention.

Regulatory Maze Requires Expert Navigation

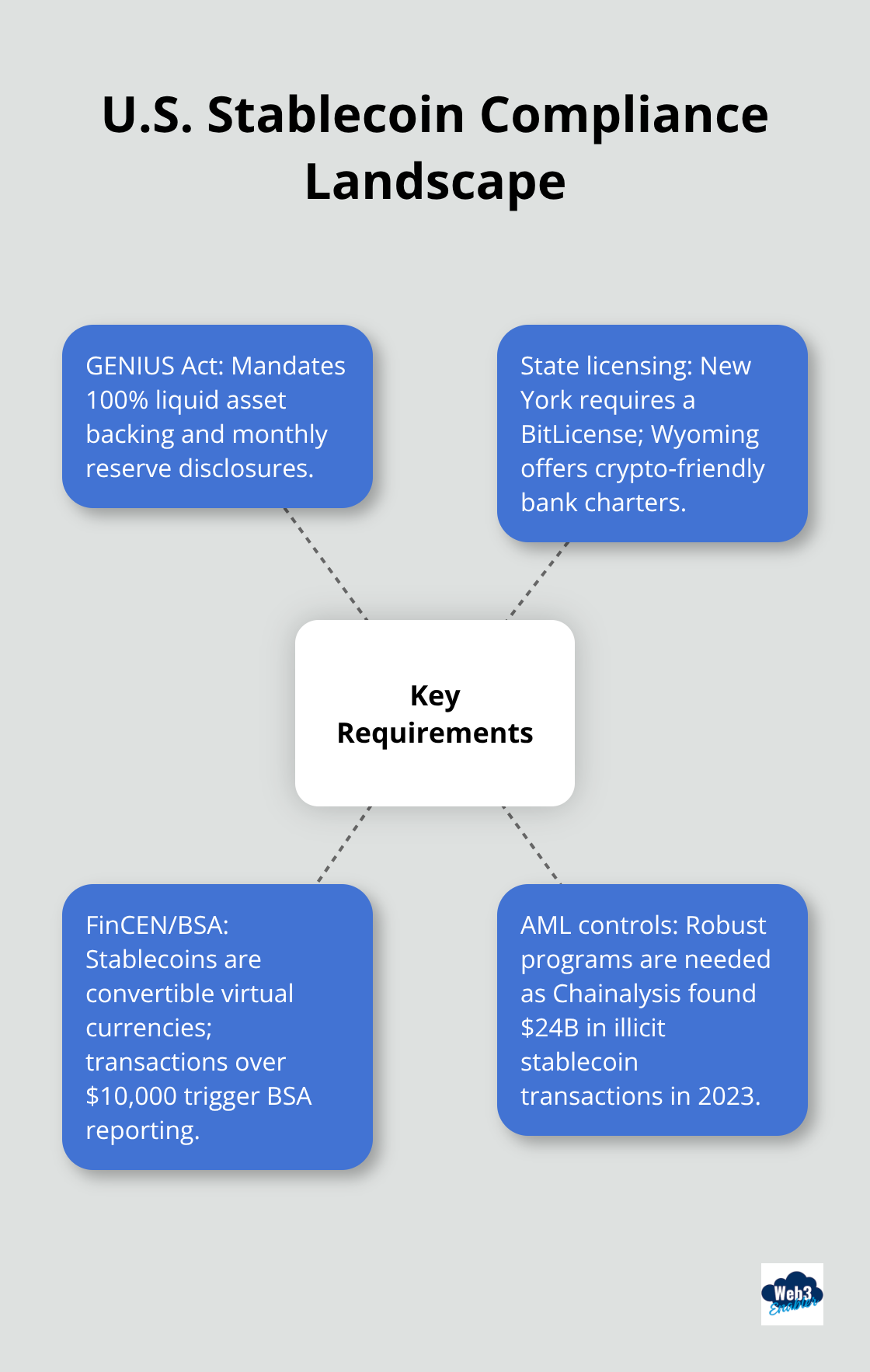

The GENIUS Act requires stablecoin issuers to maintain 100% liquid asset backing and monthly reserve disclosures, but businesses must still navigate state money transmission laws that vary wildly. New York requires a BitLicense for any stablecoin activity, while Wyoming offers crypto-friendly banking charters that traditional states reject. FinCEN classifies stablecoins as convertible virtual currencies, which triggers Bank Secrecy Act reporting requirements for transactions over $10,000. Companies need robust AML programs because Chainalysis found $24 billion in illicit stablecoin transactions during 2023, which makes compliance monitoring essential for institutional adoption.

Risk Management Beats Wishful Thinking

Depegging events like USDC’s temporary drop to $0.87 in March 2023 during Silicon Valley Bank’s collapse show that even regulated stablecoins face liquidity crises. Circle froze $3.3 billion in USDC reserves at SVB, which proved that traditional banking risks still apply to digital assets. Tether’s opacity around reserve composition creates counterparty risk that businesses can mitigate through diversification across USDC and regulated alternatives. Smart treasury management means companies hold multiple stablecoin types, maintain traditional banking relationships for compliance, and implement automated redemption triggers when stablecoins trade below $0.98 to limit downside exposure.

Final Thoughts

Fiat collateralized stablecoins have reached a tipping point where businesses can no longer ignore their potential. The $255 billion market represents more than experimental technology – it signals a fundamental shift in how companies handle payments and treasury management. Major corporations from Shopify to Microsoft already accept stablecoin payments, while traditional financial institutions like Bank of America enter the market through partnerships and custody services.

The regulatory landscape solidifies with frameworks like the GENIUS Act that provide clear guidelines for issuers and businesses. This clarity removes much of the uncertainty that previously kept enterprises on the sidelines. Companies that adopt stablecoins now gain competitive advantages through faster settlements, lower fees, and global payment capabilities that traditional banks cannot match.

For businesses ready to explore stablecoin integration, start with small pilot programs that use regulated options like USDC. Establish compliance frameworks that address AML requirements and implement treasury policies for digital assets alongside traditional cash reserves (Web3 Enabler offers solutions that integrate stablecoin payments directly into existing business processes). The question is not whether fiat collateralized stablecoins will become mainstream business tools, but how quickly your company can adapt to this new financial reality.