Financial institutions are moving tokenized assets from theory into production. Custody workflows, compliance tracking, and real-time settlement now happen on-chain, but only when your systems can handle the complexity.

We at Web3 Enabler built tokenization financial services solutions directly into Salesforce, so your team manages every stage-from issuance through settlement-without leaving your existing platform.

What Tokenization Actually Means for Your Business

Regulatory Clarity Removes Adoption Barriers

Tokenization converts real-world assets into digital representations on a blockchain. For financial institutions, this means transforming bonds, treasuries, real estate, private equity, and money market funds into programmable tokens that settle in hours instead of days. The SEC’s joint statement from January 28, 2026 clarified that tokenized securities remain securities under federal law regardless of whether ownership is recorded on-chain or off-chain, removing ambiguity that previously blocked institutional adoption. This regulatory clarity matters because your compliance team can treat tokenized assets within existing securities frameworks rather than building parallel processes.

Production Custody Relationships Are Live Today

Tokenized treasuries already move through custody workflows at major institutions. Coinbase Custody supports tokenized treasuries and charges about 50 basis points annually with a $500,000 minimum balance. Fidelity Digital Assets targets traditional institutional clients with tokenized treasury and fund custody using cold storage, HSM multi-person approvals, and SOC 1/2 audits. These are not experimental pilots anymore-they are production custody relationships handling real client assets.

Three Operational Shifts Drive Immediate Value

The practical impact for your organization comes down to three operational shifts. First, settlement speed accelerates dramatically. Anchorage Digital reports that roughly 90% of transactions settle under 20 minutes because tokens move on-chain without intermediaries. Second, your compliance team gains permanent, auditable records.

Every token transfer creates an immutable on-chain record that feeds directly into your reporting systems, eliminating reconciliation delays between your custodian and your internal ledgers. Third, you operate beyond traditional market hours. Tokenized assets move 24/7, which means your treasury and capital markets teams execute settlement and movement outside 9-to-5 windows.

Capital Treatment Aligns With Existing Frameworks

The FDIC, OCC, and Federal Reserve issued joint guidance on March 5, 2026 confirming that tokenized securities qualify as financial collateral for capital rule purposes and that blockchain type-permissioned versus permissionless-does not affect capital treatment. Your risk and capital teams can integrate tokenized assets into existing collateral frameworks without rewriting your capital adequacy models.

Tokenization Adoption Accelerates Across the Industry

Broadridge’s 2026 Digital Transformation study found that 54% of firms report moderate to large investments in tokenization and digital asset infrastructure, signaling that tokenization is no longer a competitive edge-it becomes table stakes. Your institution needs custody integration, real-time on-chain visibility, and automated reconciliation to move tokenized assets through your systems without manual intervention. The next section explores how financial institutions manage token custody and security across the entire asset lifecycle.

Managing Custody and Token Movement Through Complete Lifecycle

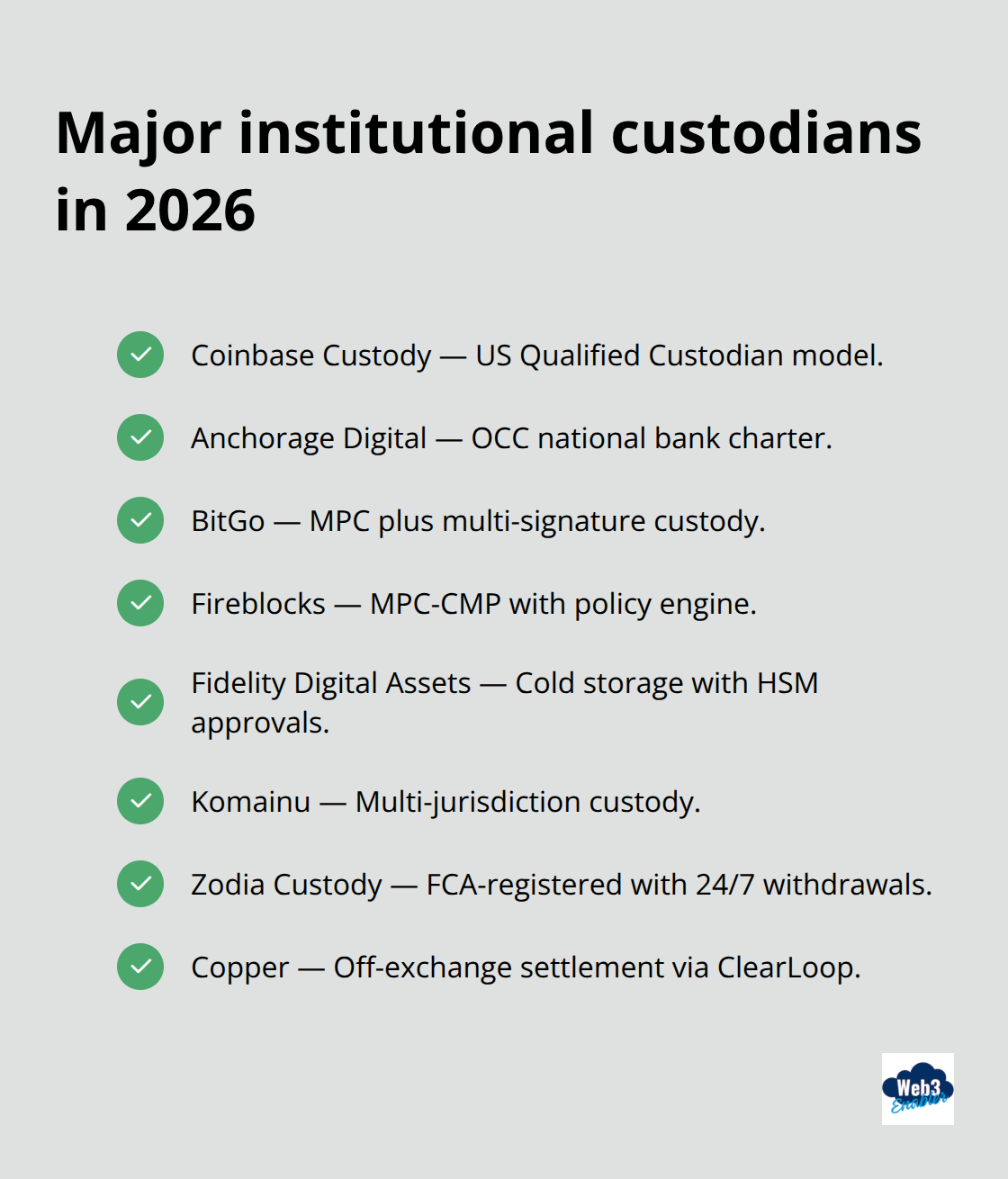

Eight Major Custodians Shape Your Token Infrastructure

Your institution’s custody provider handles the security infrastructure, but your internal systems must track every stage of the token lifecycle in real time. Eight major institutional custody providers dominate the market as of 2026: Coinbase Custody, Anchorage Digital, BitGo, Fireblocks, Fidelity Digital Assets, Komainu, Zodia Custody, and Copper. Each offers different strengths. Coinbase Custody provides a regulated US Qualified Custodian model with vault-based security and supports hundreds of assets including tokenized treasuries. Anchorage Digital, holding an OCC national bank charter, settles roughly 90% of transactions under 20 minutes and uses biometric approvals for enhanced security. BitGo combines MPC with multi-signature custody for over 1,500 assets and charges 20–25 basis points on USD balances with insurance up to $250 million. Fireblocks layers MPC-CMP architecture with a policy engine supporting approximately 1,200 assets including tokenized securities, with enterprise pricing starting around a few thousand dollars annually. Fidelity Digital Assets targets traditional institutional clients with cold storage, HSM multi-person approvals, SOC 1/2 audits, and a regulated US framework plus its native FIDD stablecoin. Komainu specializes in multi-jurisdiction custody with on-chain segregation across dozens of blockchains using MPC and HSM technology. Zodia Custody, backed by Standard Chartered, Northern Trust, SBI, NAB, and Emirates NBD, operates with FCA registration and offers 24/7 instant withdrawals. Copper differentiates through off-exchange settlement via ClearLoop across 50+ exchanges using a 3-entity MPC model and provides tokenized money market fund custody with comprehensive crime insurance up to $500 million. Your choice depends on which assets you tokenize, your geographic footprint, and whether you need native blockchain integration or traditional custody with token representation.

Most major custodians now offer insurance coverage: Coinbase maintains a $320 million crime policy, BitGo insures up to $250 million, and Copper protects up to $500 million, so your institution’s assets remain protected against custody-related losses.

Four Stages Define Token Movement

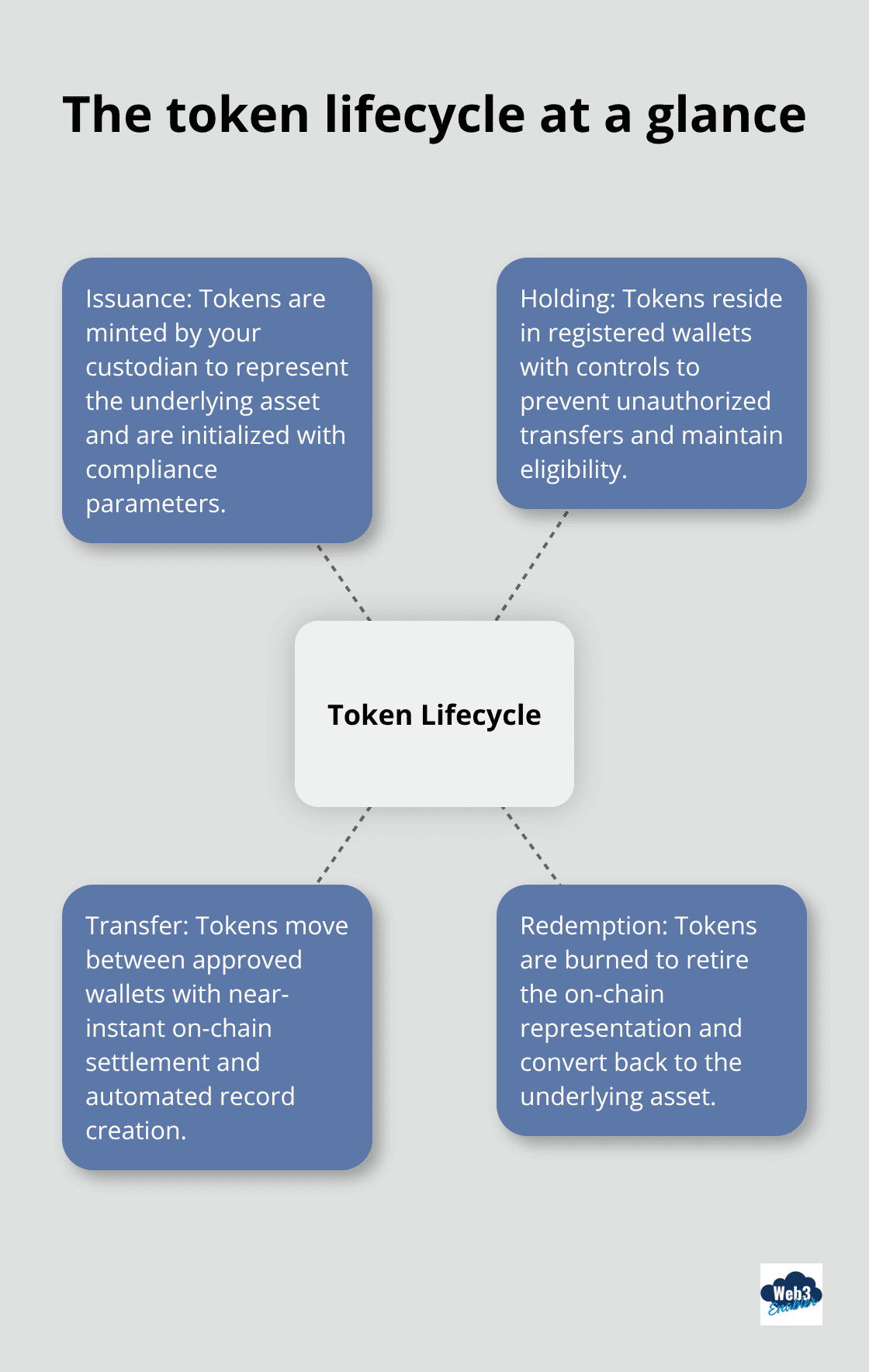

Your custody relationship feeds directly into token lifecycle management within your systems. A token moves through four distinct stages: issuance, where your custodian mints tokens representing the underlying asset; holding, where tokens sit in registered wallets paired with compliance controls to prevent unauthorized transfers; transfer, where tokens move between wallets and settlement occurs on-chain within minutes rather than days; and redemption, where tokens burn to retire the representation and convert back to the asset.

Between issuance and redemption, smart contracts enforce distribution controls that specify who can receive, hold, or transfer tokens, supporting your compliance requirements without manual intervention.

Real-Time Synchronization Eliminates Reconciliation Delays

When a token transfers on-chain, the transaction must automatically sync to your internal systems, creating an immutable audit trail that your compliance team pulls for reporting without manual reconciliation. This integration matters because your custodian manages security and on-chain custody, but your internal systems must maintain synchronized records. If your custodian settles a tokenized treasury position in 20 minutes but your internal reconciliation takes three days, you lose the operational advantage. Real-time synchronization between custody on-chain records and your internal objects eliminates this gap, allowing your treasury team to execute settlement decisions immediately and your compliance team to report positions with zero lag.

Web3 Enabler integrates token lifecycle visibility directly into Salesforce Financial Services Cloud, giving your compliance, operations, and treasury teams real-time visibility into token positions, transfer history, and settlement status without leaving the CRM. When a token transfers on-chain, the transaction automatically syncs to Salesforce native objects, creating an immutable audit trail that your compliance team pulls for reporting without manual reconciliation.

Compliance Controls Embed Into Smart Contracts

Your compliance framework now extends into the token itself. Smart contracts enforce distribution controls that prevent unauthorized transfers before they occur on-chain, rather than catching violations after settlement. This shift moves compliance from a post-trade review function to a pre-trade control mechanism. Your compliance team defines rules once in the smart contract, and every subsequent token transfer respects those rules automatically. This approach reduces manual compliance overhead and eliminates the risk of settlement occurring before your team catches a violation.

The next section explores how on-chain visibility feeds directly into your compliance and reporting workflows, transforming how your institution tracks, audits, and reports tokenized asset positions.

Compliance and Reporting for Tokenized Assets

Regulatory Frameworks Treat Tokenized Securities as Securities

Regulatory frameworks now treat tokenized securities as securities under federal law regardless of whether ownership records sit on-chain or off-chain, according to the SEC’s joint statement from January 28, 2026. This means your compliance team applies existing securities regulations to tokenized assets without building parallel processes. The FDIC, OCC, and Federal Reserve confirmed on March 5, 2026 that tokenized securities qualify as financial collateral under capital rules, and blockchain type-permissioned or permissionless-does not affect capital treatment. Your institution’s custody provider handles the security layer, but your internal systems must track every transaction for audit trail purposes.

Speed Demands Real-Time Synchronization

When tokenized treasury positions settle rapidly, your compliance and operations teams need synchronized records immediately. Manual reconciliation between on-chain custody records and your internal ledgers destroys this speed advantage. The SEC’s framework distinguishes between issuer-sponsored tokenized securities, where the issuer integrates blockchain into the master securityholder file, and third-party tokenized securities, where custodians tokenize existing securities and create crypto assets representing entitlements. Your custody relationship determines which model applies. Coinbase Custody, Fidelity Digital Assets, and other major custodians now provide tokenized asset custody with SOC 1/2 audits and crime insurance, but your institution remains responsible for demonstrating that token transfers comply with securities laws and internal policies.

Smart Contracts Enforce Compliance Before Settlement

This responsibility means your internal systems must enforce distribution controls before settlement occurs on-chain rather than catching violations afterward. Smart contracts embedded in tokens prevent unauthorized transfers automatically, moving compliance from post-trade review to pre-trade enforcement. Your compliance team defines rules once in the smart contract, and every subsequent token transfer respects those rules without manual intervention. This approach reduces manual compliance overhead and eliminates the risk of settlement occurring before your team catches a violation.

On-Chain Visibility Transforms Audit Trails and Reporting

On-chain visibility transforms how your compliance team generates audit trails and reporting without manual intervention. When a token transfers on-chain, the transaction creates an immutable record that feeds directly into your internal systems, eliminating the three-to-five-day reconciliation cycle that traditional settlement requires. Your compliance team pulls audit reports from these synchronized records, showing exactly when tokens moved, who held them, and whether transfers respected distribution controls. This real-time auditability matters because regulators expect institutions to demonstrate continuous compliance monitoring, not periodic reconciliation.

Web3 Enabler integrates token lifecycle visibility directly into Salesforce Financial Services Cloud, syncing on-chain transactions to native Salesforce objects automatically. When a token transfers, the transaction appears in your CRM without manual data entry, creating an immutable audit trail your compliance team accesses for reporting without leaving Salesforce. Automated reconciliation between on-chain records and internal objects eliminates the operational burden of matching custody statements to your ledgers. Your compliance team configures reconciliation rules once within Salesforce, and the system flags discrepancies automatically rather than requiring manual spreadsheet comparisons.

Integrated Platforms Eliminate Reconciliation Delays

Institutions that separate custody systems from internal reporting infrastructure struggle with reconciliation delays and audit gaps. Your compliance team gains permanent visibility into client positions, transfer history, and settlement status without lag, allowing advisors to provide accurate account information and treasury teams to execute settlement decisions with confidence that compliance records are synchronized.

Final Thoughts

Tokenization in financial services transforms how institutions settle assets, manage compliance, and operate beyond traditional market hours. Your institution gains three immediate advantages: settlement accelerates from days to minutes, audit trails become permanent and synchronized across systems, and your compliance team shifts from post-trade review to pre-trade enforcement through smart contracts. Regulatory clarity from the SEC, FDIC, OCC, and Federal Reserve removes adoption barriers, allowing your team to treat tokenized assets within existing securities frameworks rather than building parallel processes.

The operational bottleneck is not strategy or regulation anymore-it is execution. Your institution needs real-time synchronization between custody on-chain records and internal systems, automated reconciliation that eliminates manual spreadsheet matching, and compliance controls embedded into tokens themselves. Start with a single asset class and a pilot group of counterparties to de-risk early deployment, then map your chosen custody provider’s settlement workflow to your internal Salesforce objects and test token issuance, transfer, and redemption with real transactions.

Web3 Enabler empowers financial institutions to modernize treasury operations and digital asset management directly within Salesforce, bringing real-time on-chain visibility into client positions and settlement status without leaving your CRM. Your compliance, operations, and treasury teams collaborate seamlessly within a unified environment where blockchain transactions sync automatically to your internal records, and your tokenization financial services infrastructure scales as you add asset classes and counterparties.

FAQ: Tokenization in Financial Services

How does the 2026 regulatory landscape view tokenized securities?

According to the SEC Joint Statement (January 28, 2026), tokenized securities are treated as traditional securities under federal law, regardless of whether ownership is recorded on-chain or off-chain. Furthermore, March 2025 joint guidance from the FDIC, OCC, and Federal Reserve confirmed that these assets qualify as financial collateral for capital rule purposes, provided they confer identical legal rights to their non-tokenized counterparts.

Which institutional custodians support tokenized assets in 2026?

Major institutions have moved into production custody. Coinbase Custody and Anchorage Digital (which holds an OCC national bank charter) lead in the US, while Fidelity Digital Assets has expanded its ecosystem with its native FIDD stablecoin. Other key players include Fireblocks for MPC-based security and Zodia Custody, backed by Standard Chartered and Northern Trust.

What is the difference between “Issuer-Sponsored” and “Third-Party” tokenization?

The SEC distinguishes between two models: Issuer-Sponsored tokens, where the blockchain is integrated directly into the master securityholder file, and Third-Party tokens (often called “custodial receipts”), where a third party issues crypto assets representing an interest in an underlying security held in custody. Both require strict adherence to existing Securities Act and Exchange Act mandates.

How does “On-Chain” settlement affect capital markets?

Tokenization enables 24/7 settlement and reduces traditional T+1 or T+2 cycles to less than 20 minutes. This increases collateral mobility and allows treasury teams to manage liquidity outside traditional banking hours. Broadridge’s 2026 study found that over 54% of firms are now making significant investments in this infrastructure to capture these efficiency gains.

Can smart contracts automate compliance for token transfers?

Yes. Smart contracts allow for pre-trade enforcement. Instead of catching a violation after a trade settles, distribution controls are embedded into the token itself. These rules automatically prevent transfers to unauthorized wallets or non-KYC’d entities, shifting compliance from a manual post-trade review to an automated, programmable gatekeeper.