Global businesses moving money across borders face a choice: stick with slow, expensive traditional systems or build a modern framework for international engagement on digital assets.

We at Web3 Enabler see firsthand how outdated treasury operations hold companies back. The right digital assets strategy cuts costs, speeds up payments, and keeps compliance simple.

Why Your Business Needs Digital Assets Now

Cross-Border Payments Still Move at 20th-Century Speed

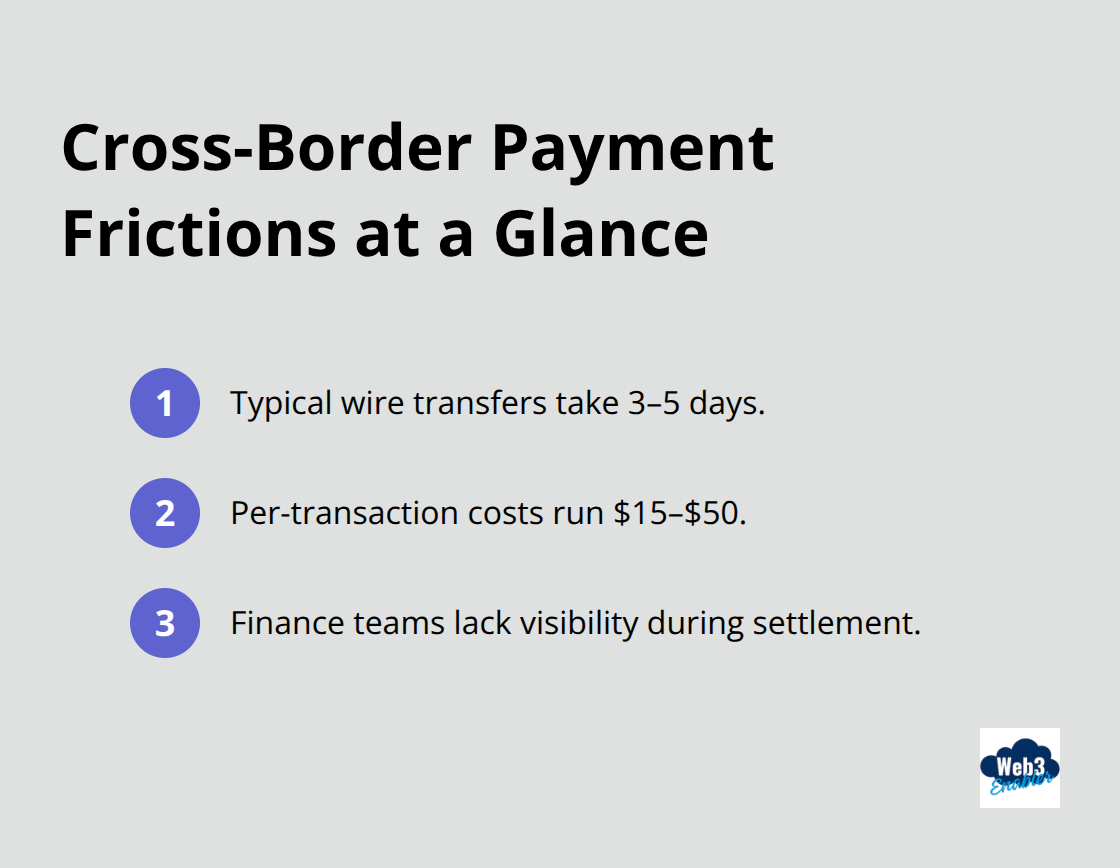

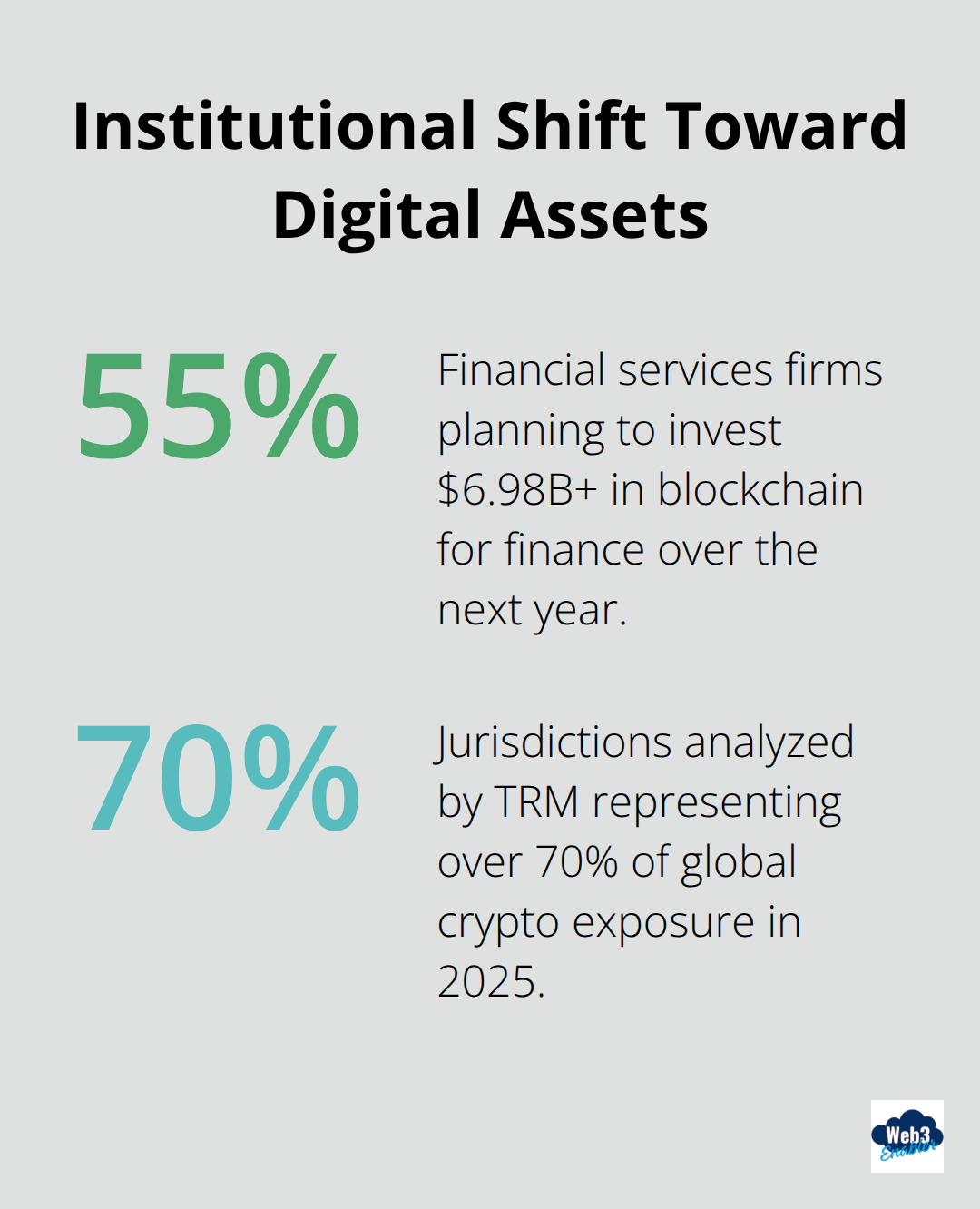

Cross-border payments remain trapped in outdated systems. A typical wire transfer takes 3–5 days, costs $15–$50 per transaction, and leaves your finance team blind to where money sits during settlement. For companies with multiple subsidiaries, vendors, and partners across regions, this friction adds up fast. According to The Business Research Company, 55% of financial services firms plan to invest $6.98 billion or more in blockchain for finance over the next year-not because it’s trendy, but because traditional rails are hemorrhaging time and money.

Regulatory Fragmentation Creates Operational Complexity

Regulatory frameworks now exist across major markets, but they differ significantly. In 2025, TRM analyzed crypto policy across 30 jurisdictions representing over 70% of global crypto exposure and found that regulatory clarity drives institutional participation. The EU’s MiCA framework, the US GENIUS Act, and frameworks in Hong Kong, Singapore, and Australia have all matured.

What complies in one region may trigger red flags in another, forcing your compliance team to build separate playbooks for each market. This complexity slows expansion and creates operational risk.

Legacy Systems Create Bottlenecks in Treasury Operations

Your treasury operations feel the squeeze hardest. Legacy systems fail to communicate with each other. Your accounts payable team uses one platform, your cash management system sits elsewhere, and your compliance records live in a third tool. When you move money internationally or settle with a vendor in a different region, everything stalls while teams manually verify, approve, and reconcile. Real-time settlement via digital assets eliminates this friction. Stablecoins and tokenized settlement rails allow you to move value across borders in minutes, not days, and settle transactions 24/7 instead of during banking hours.

Stablecoins Become Core Financial Infrastructure in 2026

The 2026 outlook is clear: stablecoins graduate from experimental tools to core institutional plumbing. Global banks deepen their roles as stablecoin issuers and custodians, and corporates increasingly move funds instantly across markets. Companies that wait find themselves at a competitive disadvantage, paying more for slower service while competitors settle faster and manage working capital more efficiently. Institutions that adopt digital assets now position themselves to capitalize on faster settlement, reduced costs, and real-time visibility into cash flow.

Your finance team faces a decision: build a modern framework for digital assets engagement or fall behind competitors who already have. The infrastructure exists. The regulatory clarity exists. What remains is implementation-and that starts with assessing your current payment infrastructure and identifying where digital assets create the most immediate value.

Building Your Digital Assets Framework

Audit Your Current Payment Infrastructure

Start by examining your current payment infrastructure without vendor sales pitches. Pull your last six months of transaction data: How many cross-border payments did you execute? What were the average costs per transaction, and how long did settlement take? Map where money gets stuck-between your accounts payable system and your bank, between regional subsidiaries, or during vendor settlements. Most finance teams discover that 30-40% of their transaction time involves manual reconciliation, not actual movement. That’s your baseline.

Identify Your Highest-Friction Payment Corridors

Next, identify which payment corridors cause the most friction. If you’re paying vendors in Southeast Asia, Europe, and Latin America, those lanes matter most. Regulatory clarity in Hong Kong, Singapore, the EU under MiCA, and Australia means you can now route payments through compliant digital asset channels in those regions without building separate playbooks for each market. The FATF’s analysis found that compliance infrastructure for virtual asset AML/CFT licensing frameworks now exists across materially important jurisdictions, so you just need to map it to your specific corridors. Don’t overthink this phase. Your goal is to understand which payment routes waste the most time and money, then prioritize those for digital asset integration.

Select a Technology Partner That Integrates Seamlessly

Selecting the right technology partner matters more than the technology itself. Your partner must integrate directly into your existing systems-your ERP, your accounting software, your Salesforce instance if you use Financial Services Cloud. Web3 Enabler stands out as the only native blockchain platform available on the Salesforce AppExchange, which means if your finance and operations teams already live in Salesforce, you avoid the nightmare of juggling separate platforms for payments, compliance, and reconciliation. Your partner should handle stablecoin settlement, real-time transaction visibility, and automated reconciliation without forcing your team to learn blockchain terminology or manage wallets manually.

Build Compliance and Operational Workflows Into Your Integration

Compliance workflows matter just as much as technical integration. Your partner must support AML/CFT checks, audit trails that satisfy regulators in all your operating regions, and reporting that aligns with frameworks like DAC8 tax reporting rolling out across the EU. Map out how digital asset settlement integrates with your existing workflows. When you send a stablecoin payment, your accounting system should record it automatically. When settlement completes, your cash position should update in real time. Your compliance team should see audit trails without extra work. This integration is what separates tools that create friction from solutions that eliminate it.

Prepare Your Team for Real-Time Settlement Operations

Your finance team now faces a new operational reality: payments that settle in minutes instead of days. This shift requires your accounts payable team to adjust approval workflows, your treasury team to monitor real-time cash positions differently, and your compliance team to track on-chain transactions alongside traditional banking records. The good news is that modern platforms handle most of this automatically. Your team doesn’t need to become blockchain experts-they need systems that translate on-chain activity into the language your finance department already speaks. Once your integration is live and your team understands the new workflows, you’re ready to move from planning to execution. The next phase focuses on how to roll out digital assets across your organization without disrupting existing operations.

Making Digital Assets Operational Without Disrupting Your Team

Your integration launches next week, and your finance team feels the pressure. Real-time settlement sounds efficient on paper, but operationally, it transforms how your accounts payable process works. Your treasury team now monitors cash positions that update by the minute instead of by the day. Your compliance team tracks transactions on-chain alongside traditional banking records. The difference between a smooth rollout and organizational chaos comes down to three things: how you integrate into systems your team already uses, how you prepare them for the operational shift, and how quickly you spot and fix problems once payments start moving.

Start Small With Your Highest-Friction Corridor

Route your first digital asset payments through your highest-friction corridor, not your entire global operation. If paying Southeast Asian vendors takes longest and costs most, that’s your pilot. Move 10-15% of those payments through digital assets while keeping the rest on traditional rails. This approach lets your accounts payable team adjust workflows at human speed and lets your finance team validate that real-time settlement actually improves cash visibility without creating new compliance headaches. When you integrate into your existing ERP or accounting platform, the technical work matters less than the operational translation. Your payment moves on-chain, but your accounts payable system records it exactly as it would a traditional wire transfer. Your cash position updates in real time without requiring manual journal entries. If your finance operations already live in Salesforce, Web3 Enabler operates natively within Financial Services Cloud or Commerce Cloud, which means your integration avoids the fragmentation that kills most digital asset projects. Your team doesn’t learn blockchain terminology or manage wallets separately. They execute payments through the same interface they use today, and the platform handles the on-chain complexity behind the scenes.

Train Your Team on Outcomes, Not Technology

Your team doesn’t need blockchain education. They need to understand that their approval workflows now work faster and their cash visibility improves. When you train your accounts payable team, focus on what changes operationally. A stablecoin payment to a Southeast Asian vendor settles in 15 minutes instead of 3-5 days, which means your vendor receives funds faster and your balance sheet updates in real time instead of waiting for international clearing. Your treasury team can now monitor exact cash positions across all corridors simultaneously rather than waiting for nostro account statements. Your compliance team sees a complete, immutable audit trail of every transaction on-chain, which simplifies regulatory reporting under frameworks like DAC8 tax reporting rolling out across the EU. Frame training around outcomes your team actually cares about: faster vendor payments mean stronger supplier relationships and better negotiating terms. Real-time cash visibility means better working capital decisions. Complete audit trails mean compliance work takes hours instead of days. Schedule training 2-3 weeks before your pilot launches and keep sessions short. Your accounts payable team needs 30 minutes to learn the new payment flow. Your treasury team needs 45 minutes to understand the new cash monitoring dashboard. Your compliance team needs one session covering audit trail access and reporting exports. Oversell the time you’re giving them back, not the technology.

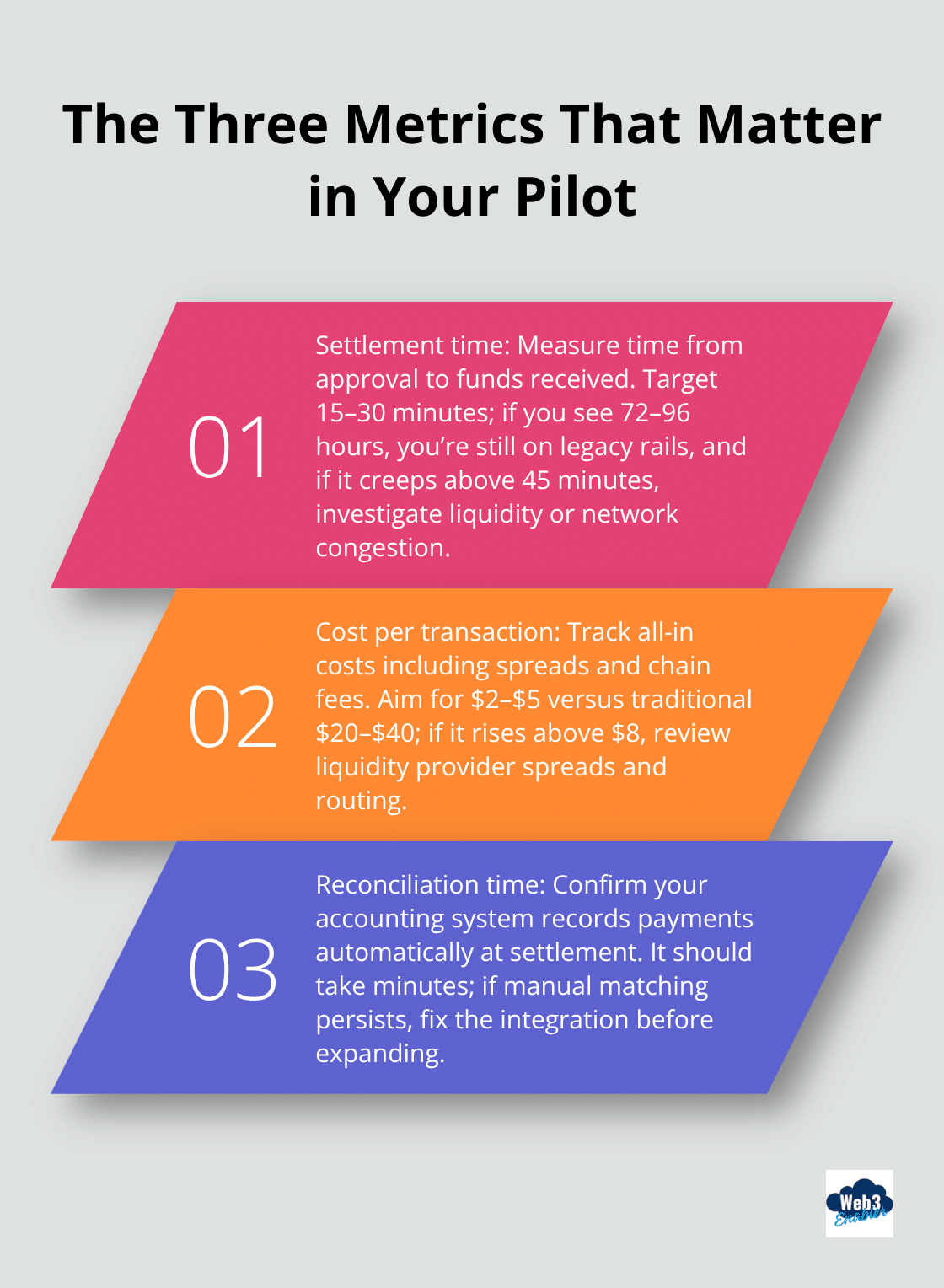

Measure Three Metrics That Actually Matter

Once your pilot runs, measure three specific metrics: average settlement time from approval to funds received, cost per transaction including all fees and spreads, and reconciliation time from settlement to accounting record. For Southeast Asian corridors, traditional wire transfers average 72-96 hours and cost $20-40 per transaction. Digital asset settlements should hit 15-30 minutes and cost $2-5 per transaction including all blockchain and stablecoin fees. If your first week shows settlement times above 45 minutes or costs above $8, something’s wrong and you need to fix it before expanding. Reconciliation time tells you whether your integration actually works.

If your accounting system automatically records the payment when it settles on-chain, reconciliation takes minutes. If your compliance team still manually matches blockchain records to accounting entries, your integration failed and you’ve created extra work instead of eliminating it. Check these metrics weekly during your pilot. If settlement times slow down, your stablecoin liquidity or bridge infrastructure might face congestion. If costs spike, your liquidity provider spreads might have widened. If reconciliation takes longer than expected, your accounting integration needs adjustment. Most organizations that fail at digital asset implementation don’t fail because the technology doesn’t work. They fail because they expanded before validating that their operational processes actually improved.

Final Thoughts

Digital assets represent operational infrastructure that your competitors are already deploying, not a future consideration for global businesses. Regulatory frameworks now exist across major markets, the technology works reliably, and the cost savings are measurable-companies that implemented digital asset payment infrastructure report settlement times dropping from 72–96 hours to 15–30 minutes and transaction costs falling from $20–40 to $2–5 per payment. What separates leaders from laggards is execution speed and the willingness to build a framework for international engagement on digital assets before market pressure forces your hand.

Start small with your highest-friction payment corridor and validate that your integration actually improves operational outcomes before expanding globally. Measure settlement time, transaction cost, and reconciliation time during your pilot, then expand to your next corridor only if those metrics improve. Regulatory clarity exists in Hong Kong, Singapore, the EU under MiCA, Australia, and the US under the GENIUS Act, and compliance infrastructure for virtual asset AML/CFT frameworks now spans materially important jurisdictions.

Your finance team can execute payments through interfaces they already use while Web3 Enabler handles blockchain complexity behind the scenes by integrating directly into Salesforce. The decision isn’t whether to adopt digital assets-it’s whether you’ll build your framework now while you control the pace, or wait until competitive pressure forces a rushed implementation.