African enterprises face a critical gap: most lack formal frameworks for managing stablecoin treasuries effectively. Currency instability, limited custody options, and regulatory uncertainty make this challenge even steeper across the continent.

We at Web3 Enabler have built this guide to address exactly that. You’ll find practical policies, hedging tactics, and compliance steps to manage stablecoins as a core treasury asset.

Choosing the Right Stablecoins and Building Your Treasury Framework

African enterprises cannot treat stablecoin selection as a one-size-fits-all decision. USDT dominates with roughly 60% of the global stablecoin market, but USDC accounts for about 25% and offers full backing by cash, overnight repos, and U.S. Treasuries-a critical distinction for risk-conscious treasurers. Emerging alternatives like PayPal USD (PYUSD) have grown to over $2.5 billion and provide additional optionality. Different stablecoins carry different counterparty risks, redemption speeds, and regulatory trajectories.

For Nigerian enterprises managing FX shortages, holding USDT or USDC as working capital preserves value against naira depreciation. In Kenya, stablecoins hedge shilling volatility effectively when you maintain them as medium-term holdings rather than constant conversions. South Africa’s institutional players have moved beyond retail payments into formal treasury operations, signaling that stablecoin adoption scales with policy maturity.

Diversify Across Multiple Stablecoins

Your first step is not selecting one stablecoin but rather diversifying across at least two regulated issuers. This reduces single-issuer risk and protects you if one stablecoin faces redemption pressure or regulatory challenges. PwC recommends maintaining fiat liquidity buffers alongside stablecoin holdings, particularly during market stress. Set a clear policy: define which stablecoins your treasury will hold, establish maximum exposure per issuer, and document your rationale for auditors.

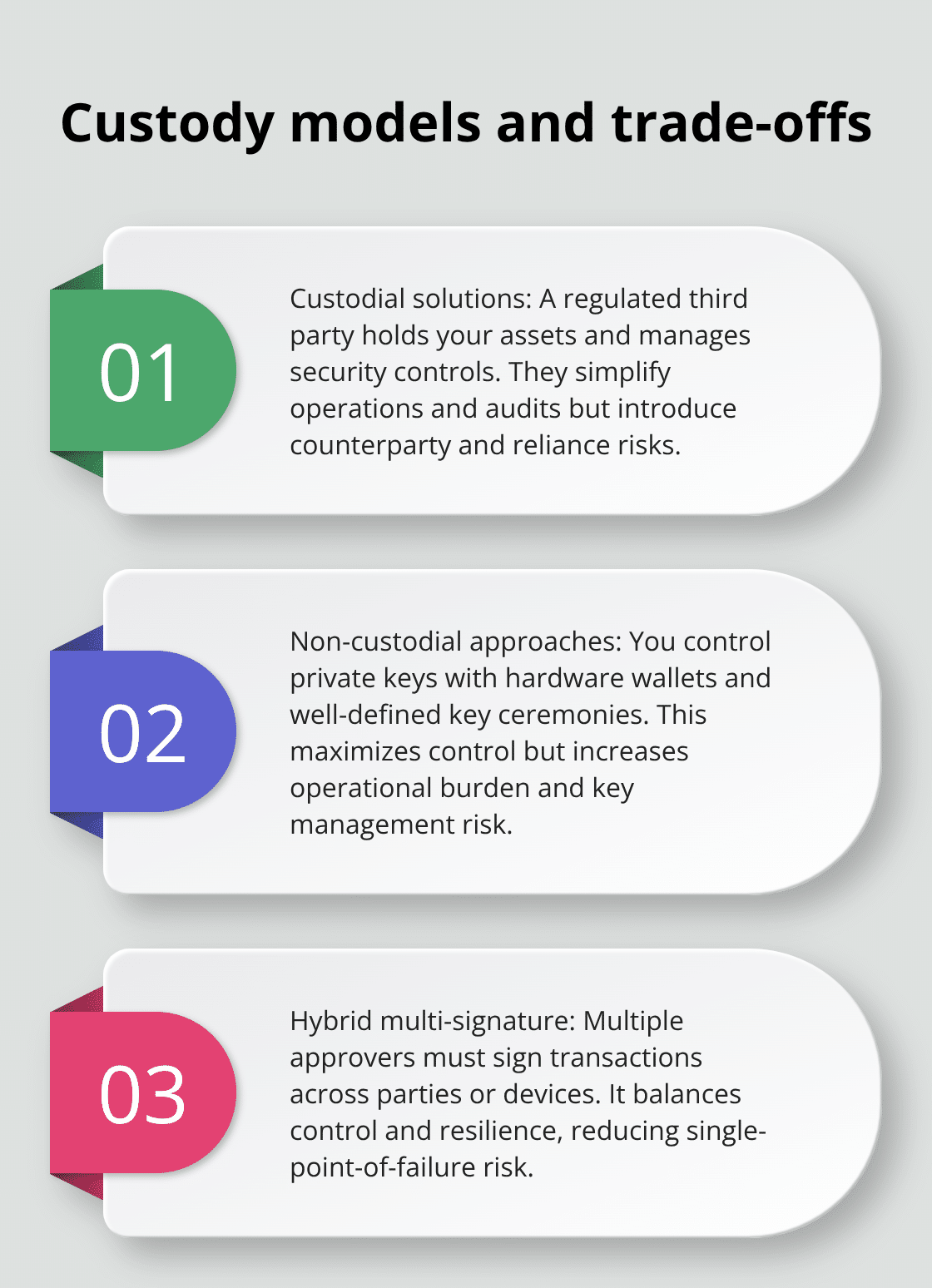

Custody Architecture Shapes Your Risk Profile

Custody decisions determine whether your stablecoin treasury operates securely or becomes a liability. Three models exist: custodial solutions where a third party holds your assets, non-custodial approaches where you control private keys, and hybrid multi-signature arrangements that distribute control. The licensing milestone in South Africa for stablecoin infrastructure providers signals regulatory credibility that matters for compliance teams.

If you choose custodial solutions, demand institutional-grade infrastructure with PCAOB-registered audits and verifiable reserve attestations-not quarterly promises but monthly proof. Non-custodial approaches give you control but require robust key management, hardware wallets, and backup procedures that most African enterprises lack the expertise to operate safely. Multi-signature custody, where multiple parties must approve transactions, offers a practical middle ground. The Dubai Insurance case demonstrates how institutional custodians provide the governance framework needed for regulated operations.

Your treasury policy must specify which custody model applies to which assets, who has signing authority, and what emergency procedures exist if a custodian becomes unavailable. Document these choices because auditors will ask, and regulators increasingly demand it under frameworks like the GENIUS Act, which requires audits of stablecoin issuers and enhanced disclosures by 2027.

Establish Liquidity Relationships Before You Need Them

Stablecoin liquidity is not infinite, and African enterprises often discover this too late. When you need to convert stablecoins back to local currency or move them between blockchains, execution costs and timing matter. Establish relationships with at least two liquidity providers before you need them. Providers serve specific corridors or blockchains, and understanding their capabilities prevents surprises during critical transactions.

Your treasury policy should specify minimum liquidity thresholds-the percentage of stablecoins you must maintain in highly liquid, fast-converting positions at any time. For Kenyan shillings or Nigerian naira, liquidity can tighten during currency crises, so conservative buffers protect you. Test your redemption process quarterly with small transactions to confirm that conversion times and fees match your assumptions.

The GENIUS Act’s monthly attestation requirements mean that regulated stablecoin issuers will publish reserve data more transparently starting in 2027, but you cannot wait until then to build confidence in your counterparties. Diversify across multiple blockchains where your stablecoins exist-Ethereum, Polygon, and others-because network congestion or security incidents can freeze access to a single chain. Your policy should explicitly address which chains you use for which purposes and how you monitor their operational status.

With your stablecoin selection and custody framework in place, the next challenge is protecting your holdings against currency volatility and optimizing how you move funds across borders.

Protecting Value While Moving Stablecoins Across Borders

Set Conversion Triggers Based on Operations, Not Markets

African enterprises holding stablecoins face a practical reality: currency volatility makes holding periods unpredictable, and conversion windows matter enormously. If you hold USDC or USDT in Kenya and the shilling weakens 3% in a week, that timing determines whether you convert immediately or wait. The answer is not to time markets but to establish clear conversion triggers tied to your business operations, not speculation.

Set thresholds based on your actual cash needs: when you must pay suppliers in local currency, when payroll deadlines arrive, when you need working capital for operations. Document these triggers in your treasury policy so conversions follow a mechanical process, removing emotion and preventing delayed decisions that cost money. Most African enterprises fail here because they lack discipline around when to convert, leading them to either hold too long and absorb losses or convert too early and miss favorable rates. Your policy should specify that conversions happen within defined windows tied to operational events, not market guesses. Test this quarterly by reviewing actual conversion decisions against your stated policy to identify drift and correct it before it becomes expensive.

Build Redundancy Across Multiple Liquidity Partners

Liquidity providers operating in African corridors know the pain points: Nigerian naira liquidity dries up during currency crises, Kenyan shilling conversions face settlement delays, and South African rand access varies by provider and time of day. You cannot rely on a single provider because their liquidity may vanish exactly when you need it most.

Establish relationships with at least two providers that cover your primary corridors, then run small test conversions monthly to confirm their execution times and fees match their promises. When evaluating liquidity partners, demand transparency on their reserve composition, redemption timelines measured in hours not days, and what happens if they face operational stress. Cross-border payments through stablecoins settle in minutes once you convert to local currency, dramatically faster than traditional banking corridors that require 3-5 business days and multiple intermediaries. This speed advantage only matters if your liquidity provider can execute immediately.

Maintain Stablecoin Positions Across Multiple Blockchains

Build redundancy by maintaining stablecoin positions across multiple blockchains where your providers operate, because a single blockchain congestion event should never freeze your treasury operations. Your policy must address which providers handle which corridors, minimum liquidity thresholds you maintain at each provider, and escalation procedures if a provider’s conversion time exceeds your tolerance.

Most African treasurers underestimate how often they will need emergency conversions during market stress, so conservative liquidity positioning costs you 0.1% in opportunity cost but prevents 5% losses from being forced into unfavorable conversions at the worst moment. When you establish these relationships and test them regularly, you move from reactive scrambling to predictable execution. This operational discipline transforms stablecoins from a speculative experiment into a reliable treasury tool that your finance team can depend on during volatile periods.

With your conversion discipline and liquidity partnerships in place, the next step involves protecting your stablecoin holdings against broader currency and counterparty risks through active hedging strategies.

Accounting, Compliance and Audit Considerations

Stablecoin transactions demand accounting treatment that your finance team has likely never encountered, and incorrect classification creates audit failures that regulators notice immediately. African enterprises holding USDC or USDT must classify these assets correctly in financial statements, track their fair value movements, and document the rationale for their treasury classification.

Classifying Stablecoins in Your Financial Statements

USDT and USDC do not qualify as cash equivalents under IFRS or US GAAP because they are not issued by regulated financial institutions and carry counterparty risk tied to the stablecoin issuer’s reserve composition. Instead, classify them as financial assets at fair value through profit or loss, which means quarterly revaluation and mark-to-market adjustments flow through your income statement. This treatment creates audit clarity because auditors understand fair-value accounting frameworks they have applied for decades to other financial instruments.

Your accounting team must establish a process to record stablecoin holdings at month-end and quarter-end using the blockchain address balance as the source of truth, then reconcile that balance to your treasury system to confirm no transactions were missed. Most African enterprises fail here because they maintain stablecoin positions off-chain without reconciling to on-chain reality, creating gaps that auditors flag as material control deficiencies.

Meeting Regulatory Requirements Across African Jurisdictions

The regulatory landscape across African jurisdictions remains fragmented, but enterprises holding stablecoins for treasury purposes should assume regulatory requirements will arrive within 18 months. Nigeria, Kenya, and South Africa have not yet formalized stablecoin frameworks, but your treasury policy must document the business rationale for holding stablecoins-whether for FX hedging, working capital preservation, or cross-border settlement-because regulators will ask whether these holdings constitute regulatory capital or reserve requirements under local banking rules.

Anticipate that African authorities may restrict the circulation of foreign-denominated stablecoins and work to build credible domestic currencies, so plan your strategy around potential policy shifts rather than assuming current conditions persist indefinitely.

Preparing for Internal and External Audits

Establish relationships with external auditors experienced in digital assets before your first audit cycle, because most Big Four firms lack African offices with stablecoin expertise and will require training on your specific implementation. Request that your auditor specify what evidence they require to attest to stablecoin holdings: blockchain transaction records, custodian statements, reserve attestations from issuers like Circle or Tether, and reconciliation procedures between on-chain and off-chain records.

Build your compliance infrastructure now to align with institutional-grade audit procedures that will become standard as regulators formalize requirements. Test your audit readiness quarterly through a mock audit where you gather all stablecoin documentation, trace transactions from your treasury system to the blockchain, and confirm that your auditor can verify your holdings independently. This discipline prevents surprises during actual audits and identifies gaps in your documentation before they become compliance failures.

Final Thoughts

African enterprises now have a clear path forward for stablecoin treasury operations. The framework you build-selecting regulated stablecoins, establishing custody architecture, managing liquidity across multiple providers, and preparing audit-ready documentation-transforms stablecoins from experimental tools into operational assets that your finance team can depend on. Stablecoins solve real problems for African treasurers: they preserve value against currency depreciation in Nigeria, hedge shilling volatility in Kenya, and enable institutional treasury operations in South Africa without the delays and costs of traditional banking corridors.

Your stablecoin treasury strategy must start with policy, not technology. Document your stablecoin selection criteria, custody model, liquidity thresholds, and conversion triggers before you move your first dollar, then test your procedures quarterly with small transactions to confirm that your assumptions about execution times and costs match reality. Regulatory frameworks are hardening across Africa and globally-the GENIUS Act in the United States requires audits and monthly attestations from stablecoin issuers starting in 2027, and African authorities will follow with their own requirements.

Start with a contained pilot using one stablecoin and one liquidity corridor, then measure your cost savings and settlement speed against your current banking process. We at Web3 Enabler understand that integrating stablecoins into your existing treasury infrastructure requires connecting digital assets to your operational systems, and our platform bridges that gap by providing native support for cryptocurrencies and digital assets within your existing corporate infrastructure. Once you confirm the operational benefits, expand to additional corridors and stablecoins with the same rigor you apply to your foreign exchange hedging and cash management.