Cross-border payments with crypto are reshaping how companies move money globally. Traditional banking channels remain slow and expensive, while blockchain-based solutions settle transactions in minutes at a fraction of the cost.

Cross-border payments with crypto are reshaping how companies move money globally. Traditional banking channels remain slow and expensive, while blockchain-based solutions settle transactions in minutes at a fraction of the cost.

At Web3 Enabler, we’ve seen firsthand how stablecoins eliminate intermediaries and reduce friction in international payments. This guide walks you through the practical steps to implement crypto payments for payroll, supplier settlements, and treasury operations across borders.

Why Traditional Banking Slows Down Global Payments

The Hidden Cost of Correspondent Banking

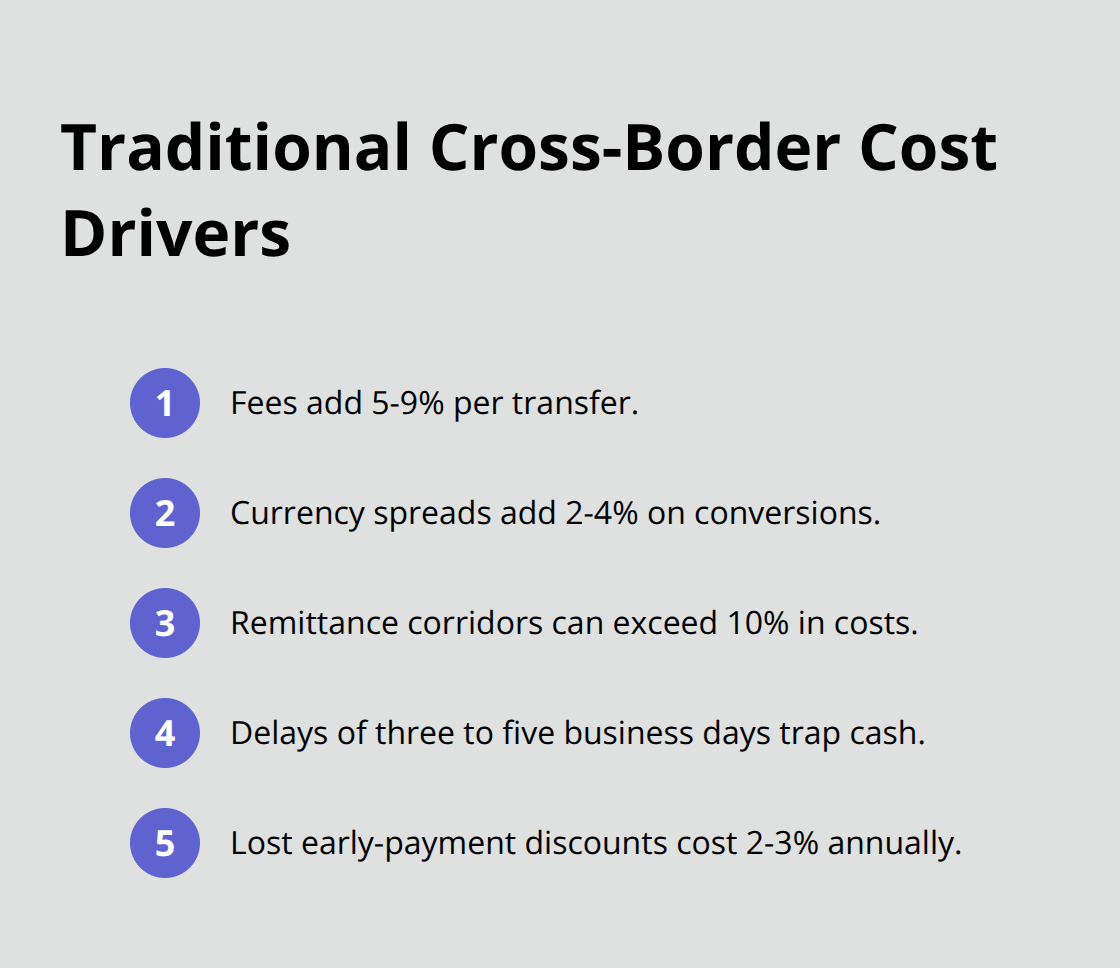

Wire transfers and SWIFT payments dominate international business, yet they remain fundamentally broken for modern commerce. A standard wire transfer takes three to five business days to settle, even between major financial centers. SWIFT messages travel instantly, but the actual money sits in correspondent banking delays, waiting for nostro account reconciliation across multiple intermediaries. During this delay, your cash sits trapped, exchange rates shift, and supplier relationships suffer.

For a company sending $10 million monthly across borders, those delays compound into working capital problems and lost early-payment discounts worth 2-3% annually. The cost structure reveals why speed matters. Traditional cross-border payments charge 5-9% in fees plus 2-4% currency spreads, according to analysis from Allium Labs and Visa data.

What Traditional Payments Actually Cost

A $100,000 supplier payment to Africa incurs $7,000-13,000 in combined fees and conversion costs. In sub-Saharan Africa, remittance corridors exceed 10% costs, making traditional banking economically punitive for smaller flows. These expenses accumulate across dozens of monthly transactions, creating substantial drains on working capital.

Blockchain-based stablecoins settle the same payment in 90 seconds for under $100. That $12,000 difference compounds across your payment volume. USDC transactions settle on blockchain networks within seconds, eliminating correspondent banking delays entirely. You pay transaction fees measured in cents, not percentages.

How Stablecoins Invert the Economics

Currency conversion happens through smart contracts at market rates, removing the manual markup that traditional FX desks apply. For treasury teams managing multi-currency payroll, supplier payments, and cash positioning across regions, this speed and cost efficiency directly improves cash flow and operational flexibility.

Companies implementing blockchain-based cross-border payments report settlement times dropping from days to minutes while cutting total transaction costs below 1%, according to McKinsey research on real-time payment adoption. A mid-market company processing $50 million in annual cross-border payments moves from $4.5 million in combined fees to under $500,000 in blockchain-based costs. This isn’t theoretical savings-these numbers reflect actual operational improvements across organizations that have made the shift.

The financial case for stablecoin infrastructure is clear. Now the question becomes how to select the right stablecoin and integrate it into your existing systems without disrupting current workflows.

Building Your Stablecoin Payment Infrastructure

Selecting the Right Stablecoin for Enterprise Payments

USDC has emerged as the dominant stablecoin for business payments, backed by regulated Circle affiliates with publicly listed authorizations across multiple jurisdictions. This matters operationally because regulated issuers provide the transparency and compliance infrastructure that enterprise treasury teams require. When you send USDC across borders, you move a token issued by entities subject to banking oversight, not speculative assets. Lipaworld’s cross-border payment platform demonstrates this in practice, using USDC to deliver near-instant settlements for remittances and supplier payments across Africa, eliminating the multi-day delays inherent in traditional banking.

Your choice of stablecoin directly impacts your compliance posture and settlement speed. USDC settles in seconds across multiple blockchains through Circle’s Cross-Chain Transfer Protocol, meaning you can move funds between Ethereum, Solana, and other networks without converting back to fiat. This flexibility matters when your suppliers operate across different blockchain ecosystems or when you need to optimize gas fees and settlement times. Alternative stablecoins exist, but most lack the regulatory clarity or institutional backing that USDC provides. Tether’s USDT commands larger trading volumes, yet Circle’s regulated structure offers stronger compliance frameworks for corporate treasuries managing material payment flows.

Integrating Blockchain into Your Existing Workflows

Integration into your existing systems requires a different approach than bolting on a separate crypto payment layer. Web3 Enabler provides a seamless interface between Salesforce and blockchain infrastructure, allowing you to manage crypto payments directly within your existing corporate environment rather than toggling between multiple platforms. This native integration matters because your finance and procurement teams already work within Salesforce for vendor management, invoice processing, and payment authorization. Adding crypto payments through Web3 Enabler means your accounts payable workflows remain unchanged while settlement happens on-chain.

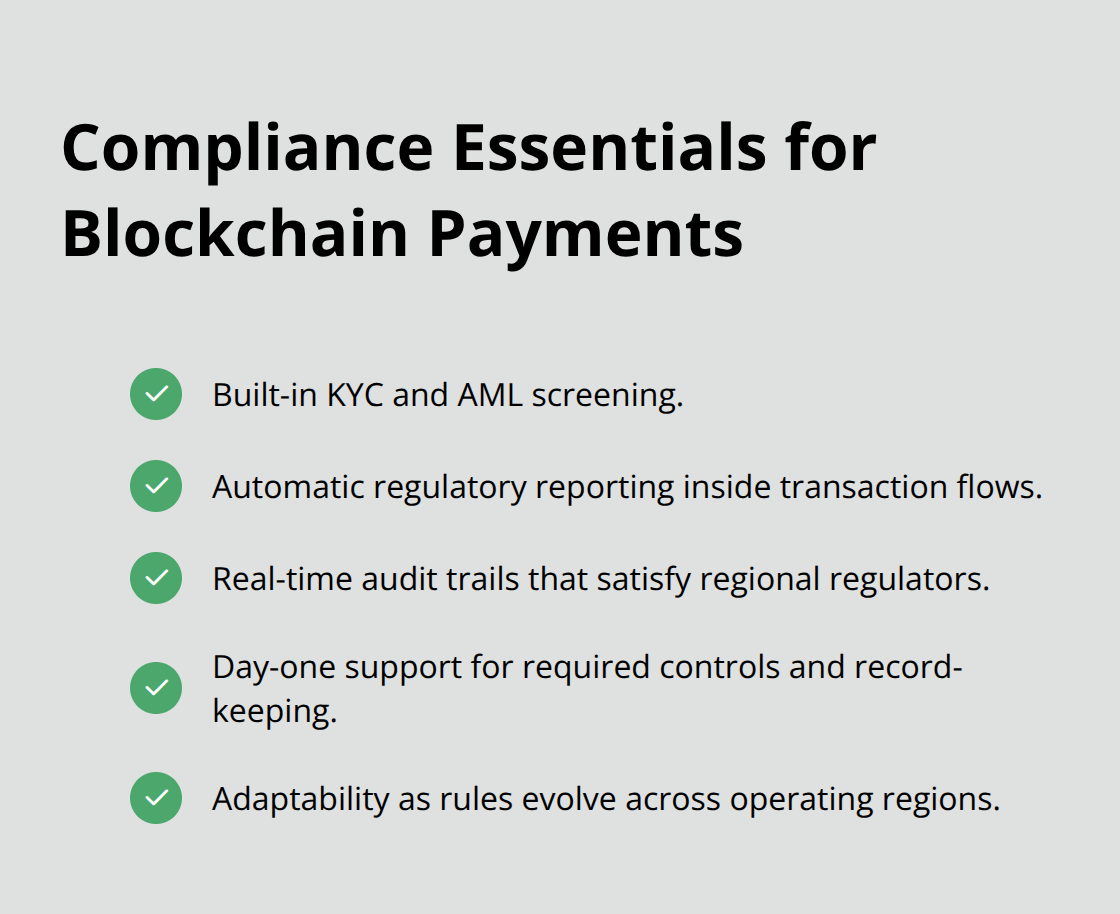

When implementing, prioritize platforms that embed KYC, AML screening, and automatic regulatory reporting into transaction flows, according to compliance standards outlined by FATF guidance. This reduces manual verification overhead and creates real-time audit trails that satisfy regional regulators. Your payment infrastructure must support these requirements from day one, especially as regulatory frameworks evolve across your operating regions.

Meeting Regional Compliance Standards

In Africa, where regulatory frameworks are rapidly evolving, South Africa’s Travel Rule implementation in 2025 established a standard that other regional authorities are adopting. The EU’s MiCA regulation, which took full effect in 2024, requires stablecoin issuers to maintain transparent reserves and undergo regular audits. This regulatory moat protects you from depegging risks that plagued earlier stablecoin ecosystems.

When selecting vendors, demand proof of MiCA compliance and GENIUS Act alignment if serving US-based operations. The GENIUS Act, established in the United States, sets reserve and audit expectations that most serious stablecoin providers now meet. Regional compliance varies substantially. Sub-Saharan Africa’s remittance corridors are seeing regulatory momentum toward stablecoin rails through platforms like the SADC Real-Time Gross Settlement system. This infrastructure shift means your compliance requirements will shift from purely banking-centric to include blockchain-native verification.

Automating Currency Conversion and FX Operations

Treasury operations across multiple currencies require FX infrastructure that moves beyond traditional banking spreads. Circle’s StableFX offering provides 24/7 stablecoin currency conversion, eliminating the 2-4% spreads that traditional FX desks charge and the delays associated with banking hours. Smart contracts automatically convert supplier payments from your base currency to their preferred denomination at market rates, removing the manual FX desk markup entirely.

This automation directly improves cash positioning for multi-currency payroll and vendor payments across regions. Your finance team no longer waits for banking hours or negotiates FX rates with intermediaries. Instead, transactions settle at transparent market prices within seconds, giving you precise control over payment timing and currency exposure. As your organization scales cross-border operations, this operational efficiency compounds into substantial working capital advantages.

How Stablecoins Transform Payroll, Supplier Payments, and Treasury Operations

International Contractor Payments Across Borders

International contractor payments expose the weaknesses of traditional banking immediately. A software developer in Lagos working for a US-based startup waits five to seven business days for salary deposits while banks charge 8-12% in combined fees and spreads. USDC payments settle in 90 seconds with transaction costs under one dollar. Crypto-native teams already operate this way, compensating distributed staff across 20+ countries through stablecoin payroll that eliminates the need for local bank accounts in each jurisdiction.

This operational shift matters because your finance team no longer manages 15 different banking relationships across regions. One stablecoin address receives payroll distributions, and employees withdraw to local fiat rails instantly. Professional athletes receiving cross-border payments for sponsorships and appearance fees increasingly demand USDC settlement because traditional wire transfers impose delays and costs that make smaller payments economically unviable. Lipaworld demonstrates this at scale, using USDC to handle recurring payments for employees, contractors, and suppliers across Africa where traditional banking infrastructure remains fragmented and expensive.

Supplier Payments in Emerging Markets

Supplier payments in Africa and emerging markets represent where stablecoin infrastructure delivers the strongest financial case. A mid-market exporter in South Africa supplying goods to European retailers currently receives payment 30-45 days after shipment due to correspondent banking delays and currency conversion bottlenecks. USDC settlement compresses this to same-day confirmation, improving cash flow by weeks and enabling suppliers to negotiate early payment discounts of 2-3% that traditional banking structures prevent.

Remittance corridors in sub-Saharan Africa exceed 10% costs according to FSB KPI data, making traditional channels economically destructive for smaller cross-border transactions. Treasury teams managing multi-currency operations across Nigeria, Kenya, and South Africa now route supplier payments through stablecoin infrastructure that costs under 1% total while settling within minutes. The SADC Real-Time Gross Settlement system expanding across Southern Africa signals regulatory acceptance of blockchain-based payment rails, meaning compliance frameworks harden around these structures.

Treasury Operations and Cash Flow Management

Treasury operations benefit most directly because cash flow visibility improves dramatically. When your supplier in Lagos receives USDC payment confirmation within seconds rather than waiting days for correspondent bank confirmation, your working capital position stabilizes immediately. Multi-currency payroll becomes straightforward because smart contracts convert USDC to local currency at transparent market rates without the 2-4% spreads traditional FX desks charge.

Your finance team manages supplier payments and payroll authorization within existing workflows while settlement happens on-chain automatically. This integration eliminates the manual reconciliation overhead that plagues traditional cross-border operations.

Real-time payment networks have shown about 400% growth in some regions, according to McKinsey research, reflecting how organizations are shifting away from correspondent banking toward blockchain-native settlement. Your treasury operations gain the speed and cost efficiency that modern commerce demands.

Final Thoughts

Cross-border payments with crypto eliminate the friction that has defined international business for decades. Settlement happens in seconds instead of days, costs fall below 1% instead of 5-9%, and your finance team manages transactions within Salesforce rather than toggling between separate systems. USDC provides the regulatory backing and institutional acceptance that enterprise treasuries require across jurisdictions.

Start with your highest-friction payment corridors-international contractor payments and supplier settlements in Africa deliver the strongest financial case because traditional banking costs exceed 10% in these regions. Route these payments through stablecoin infrastructure, measure the working capital improvements, and expand to payroll and treasury operations as your team gains operational confidence. Web3 Enabler connects blockchain transactions directly to your corporate infrastructure without disrupting existing workflows.

MiCA compliance, the GENIUS Act framework, and emerging Travel Rule implementations across Africa create structural advantages for organizations that move now rather than waiting. These standards protect you from depegging risks and provide the compliance infrastructure that enterprise treasuries require. Organizations that implement cross-border payments crypto infrastructure today gain working capital advantages and operational efficiency that compound across years.