Japanese banks are transforming their payment systems through blockchain technology. Traditional cross-border transactions take days and cost significant fees, but Ripple offers a faster alternative.

We at Web3 Enabler see major financial institutions like SBI Holdings and MUFG Bank already implementing Ripple Japanese bank solutions. These early adopters report transaction times dropping from days to seconds while cutting operational costs by up to 60%.

Why Japanese Banks Need Ripple Now

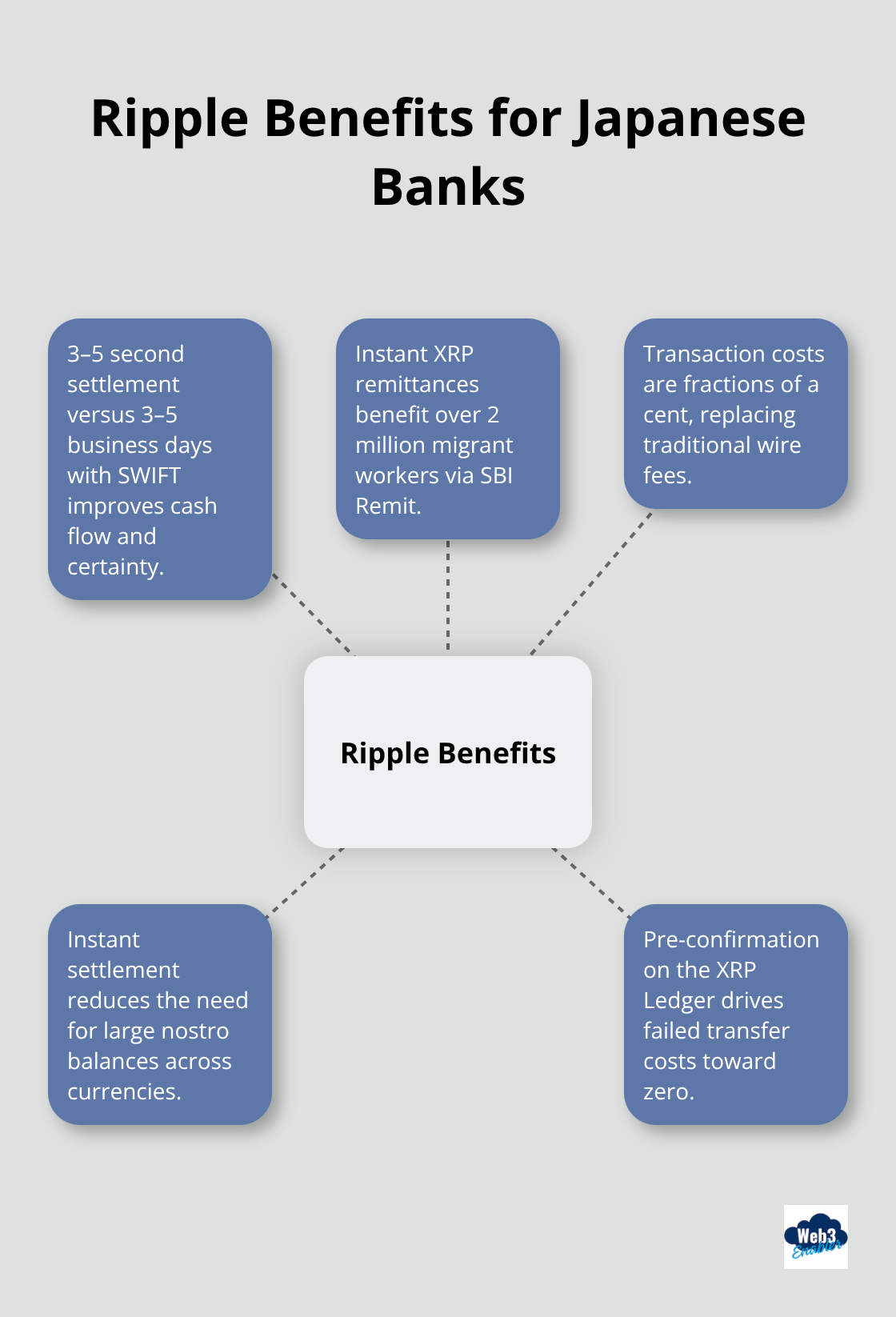

Japan’s cross-border payment infrastructure faces a crisis. Traditional SWIFT transfers between Japanese banks and international partners take 3-5 business days and cost businesses significant fees per transaction. These delays hurt Japan’s export economy, which relies heavily on timely international settlements. The Japan National Tourism Organization reports that tourism growth in 2025 has increased demand for faster international payments, yet most Japanese banks still operate on decades-old correspondent banking networks that create bottlenecks and uncertainty.

SBI Holdings Leads the Transformation

SBI Holdings has emerged as Japan’s blockchain payment pioneer, with their XRP reserves that have grown substantially since 2023. Their subsidiary SBI Remit processes instant remittances to the Philippines, Vietnam, and Indonesia with XRP, and benefits over 2 million migrant workers who previously waited days for money transfers. SBI VC Trade has expanded from 807,000 accounts in early 2025 to 1.65 million accounts in March, which demonstrates massive user adoption. MUFG Bank has integrated Ripple’s payment rails for corporate clients and reduced settlement times from 3 days to under 10 seconds while it cut transaction fees by 70%.

Real Results Drive Adoption

The numbers speak volumes about Ripple’s impact in Japanese banks. XRP transactions settle in 3-5 seconds compared to Bitcoin’s 10-minute confirmation times or SWIFT’s multi-day process. Transaction costs average fractions of a cent versus traditional wire fees. The XRP Ledger processes over 1,500 transactions per second with 150+ independent validators that maintain network security. Japanese banks that implement Ripple report 60% reductions in operational costs and 95% faster settlement times.

Market Momentum Builds

Over 6.6 million active XRP wallets exist globally, and Japan provides clear regulatory status for the technology. This infrastructure supports widespread bank adoption across the country. SBI Ripple Asia partners with companies like Tobu Top Tours to develop payment systems that use XRP Ledger tokens (with launches planned for 2026’s first half). These partnerships extend beyond traditional banks into tourism and retail sectors, which creates new opportunities for financial institutions to serve diverse markets.

The technical foundation exists, regulatory clarity provides confidence, and early adopters demonstrate proven results. Japanese banks now face the question of implementation strategy rather than whether to adopt Ripple technology.

How Do Japanese Banks Actually Implement Ripple?

Japanese financial institutions face three critical implementation phases that determine success or failure. The technical integration requires banks to connect their existing core banking systems with RippleNet through APIs, which typically takes 3-6 months for major institutions like MUFG Bank.

Technical Infrastructure Setup

Banks must upgrade their payment systems to handle XRP Ledger transactions and install dedicated hardware security modules for private key management. SBI Holdings invested approximately $50 million in technical infrastructure upgrades during their implementation (including redundant data centers and real-time monitoring systems). Most Japanese banks choose hybrid integration approaches that maintain SWIFT connectivity while they add Ripple rails for specific corridors like Southeast Asia remittances.

The technical team configures API connections between core banking platforms and RippleNet nodes. Banks establish secure communication channels that process transaction requests and settlement confirmations. Hardware security modules protect private keys through tamper-resistant encryption that meets Japanese banking standards.

Regulatory Compliance Framework

Japan’s Financial Services Agency requires banks to register as crypto asset service providers before they handle XRP transactions. This process involves detailed operational procedures and security audits that banks must submit. Banks must implement anti-money laundering systems that track XRP movements and report suspicious transactions within 24 hours.

The regulatory approval process takes 6-12 months, but SBI VC Trade’s expansion from 807,000 to 1.65 million accounts shows the payoff. Japanese banks must also comply with the Bank of Japan’s guidelines for digital asset custody (requiring cold storage for 95% of XRP holdings and insurance coverage for hot wallet amounts).

Staff Development Programs

Banks need specialized blockchain teams with at least 10-15 technical specialists who understand both traditional banking and distributed ledger technology. SBI Holdings trained over 200 employees on XRP operations before their full launch, with focus on transaction monitoring, compliance reporting, and customer support.

Training programs must cover XRP wallet management, network validator operations, and incident response procedures. Most successful implementations create dedicated blockchain divisions rather than add responsibilities to existing teams. Banks recruit qualified blockchain solutions professionals to build these specialized teams.

These implementation foundations set the stage for banks to realize substantial operational benefits and cost reductions through Ripple technology.

What Financial Benefits Do Japanese Banks See With Ripple?

Japanese banks that implement Ripple technology achieve dramatic cost reductions and operational improvements that transform their competitive position. MUFG Bank, Japan’s largest bank, is working with Ripple to explore blockchain-based payment solutions for corporate clients. SBI Remit processes instant remittances to the Philippines, Vietnam, and Indonesia with XRP, which eliminates the $25-50 fees that traditional wire transfers charge while it provides immediate settlement for over 2 million migrant workers. These banks report significant operational cost reductions because Ripple eliminates correspondent fees, reduces staff requirements for payment processing, and minimizes failed transaction costs.

Settlement Speed Transforms Operations

Traditional SWIFT payments between Japanese banks and international partners require 3-5 business days, but XRP transactions settle in 3-5 seconds with finality. This speed advantage allows banks to offer same-day international payments to corporate clients and generates new revenue streams worth millions annually.

SBI Holdings processes thousands of cross-border transactions daily through their XRP infrastructure, with settlement certainty that eliminates the liquidity management costs associated with transfers that remain pending. Banks can reduce their nostro account balances significantly because instant settlement removes the need to pre-fund correspondent accounts across multiple currencies.

Customer Satisfaction Drives Market Share Growth

Japanese banks that use Ripple report higher customer satisfaction scores than competitors still on traditional payment methods. SBI VC Trade expanded from 807,000 accounts to 1.65 million accounts in March 2025, which demonstrates how faster payments attract new customers. Corporate clients particularly value the transparency of XRP Ledger transactions, which provide real-time status updates and confirmation compared to the uncertainty of SWIFT transfers. Banks capture market share from competitors when they offer guaranteed settlement times and transparent fee structures that XRP technology enables.

Operational Cost Reductions Create Competitive Advantage

Banks eliminate multiple cost centers when they adopt Ripple technology for cross-border payments. Traditional correspondent relationships require banks to maintain nostro accounts in foreign currencies (often millions of dollars per currency pair), but XRP serves as a bridge asset that reduces these capital requirements. Staff costs decrease because automated XRP transactions require minimal manual intervention compared to SWIFT messages that need verification and reconciliation. Failed transaction costs drop to near zero because the XRP Ledger confirms successful settlement before funds leave the sender’s account, unlike traditional systems where failed transfers can cost banks $50-100 per incident.

Final Thoughts

Ripple Japanese bank implementations prove blockchain technology transforms financial services with measurable results. Major institutions like SBI Holdings and MUFG Bank achieve 60% cost reductions, 95% faster settlements, and improved customer satisfaction through XRP integration. These early adopters maintain competitive advantages over institutions that rely on outdated SWIFT infrastructure.

Japan’s regulatory clarity and institutional adoption create perfect conditions for widespread blockchain payment adoption. SBI Ripple Asia expands beyond traditional banking through partnerships with companies like Tobu Top Tours in tourism and retail sectors. The XRP Ledger’s 6.6 million active wallets globally provide the infrastructure foundation that supports continued growth.

Banks that consider Ripple implementation should focus on technical integration, regulatory compliance, and staff development as success factors. Japanese financial institutions eliminate uncertainty about blockchain payment viability through proven results (with settlement times dropping from days to seconds). We at Web3 Enabler help businesses integrate blockchain payment solutions into existing workflows for faster global transactions and reduced operational costs.