Cross-border payments eat up 6% of global GDP through fees and delays. Traditional banking takes 3-5 days and charges outrageous fees that make your accountant cry.

We at Web3 Enabler know finding the best crypto for cross border payments changes everything. The right choice cuts costs by 80% and settles in minutes, not days.

What Makes a Cross Border Payment Crypto Worth Your Time

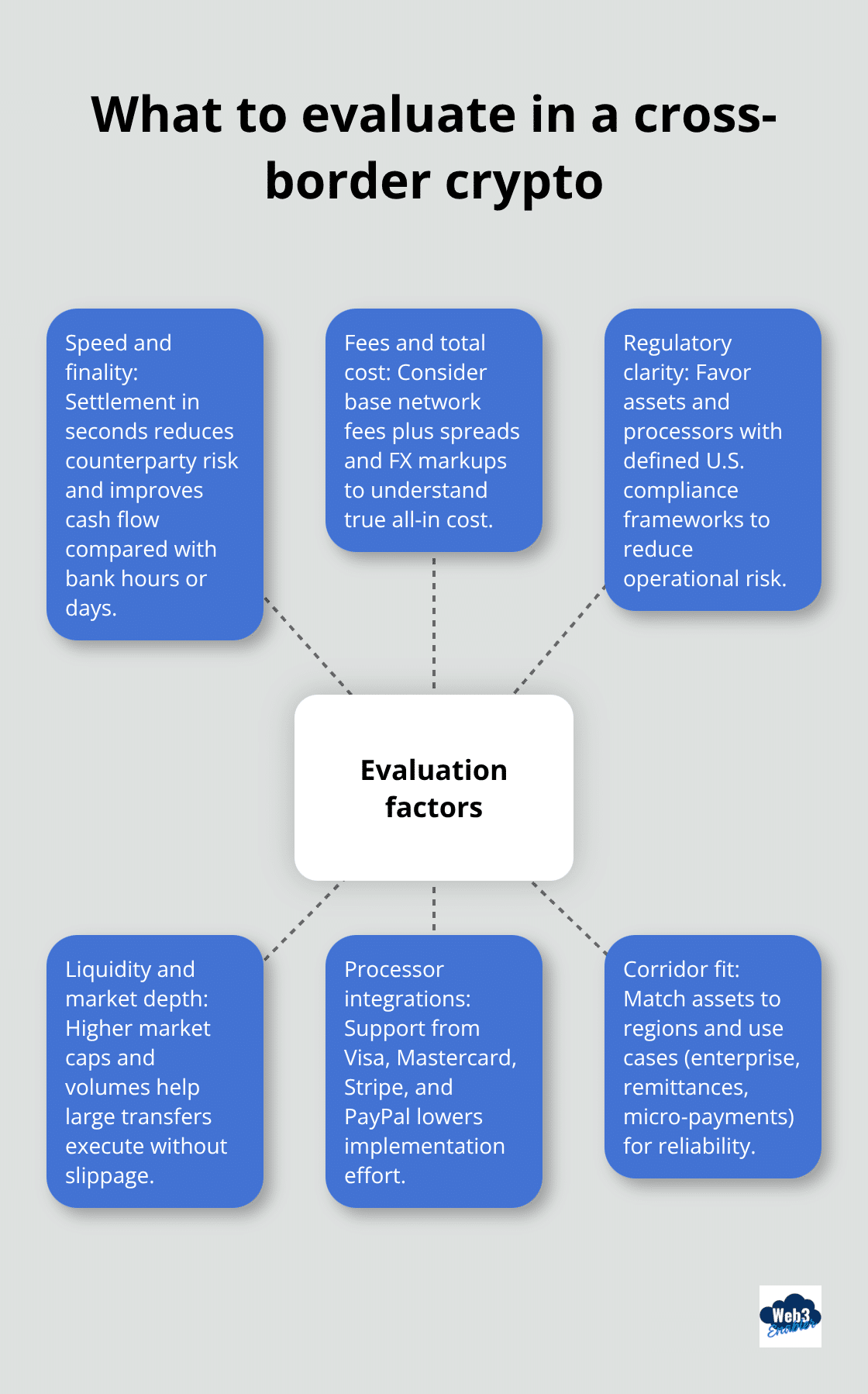

Speed separates winners from losers in cross border payments. XRP settles transactions in 3-5 seconds while Bitcoin takes 10-60 minutes. Stellar processes payments in 2-5 seconds with finality that makes traditional wire transfers look prehistoric.

The $250 trillion cross border payment market by 2027 demands instant settlement, not bank hours that stretch across time zones. Real-time payment networks now bypass traditional batch processes entirely and give businesses the cash flow control they actually need.

Network Fees That Won’t Kill Your Margins

Transaction costs make or break your payment strategy. XRP charges $0.0002 per transaction while Ethereum gas fees swing between $1-50 (network congestion drives these wild price swings).

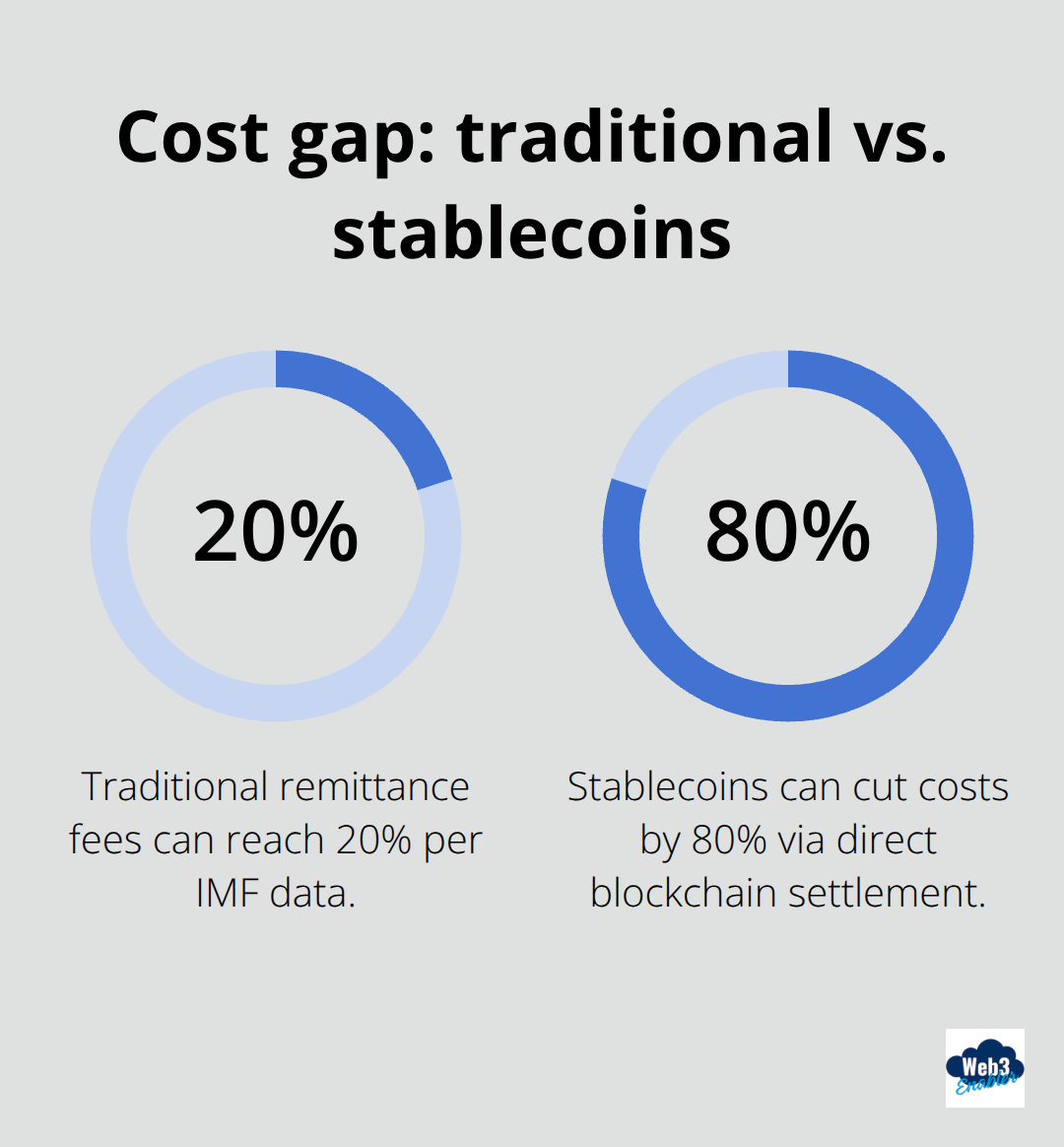

Stellar keeps fees under $0.00001, which makes micro-payments profitable for the first time. Traditional cross border payments charge up to 20% for remittances according to IMF data, while stablecoins cut costs by 80% through direct blockchain settlement. Smart businesses calculate total cost with exchange rate markups, not just base fees that hide the real expense.

Regulatory Reality Check

Compliance determines which cryptos actually work in business environments. The Genius Act provides regulatory framework for stablecoins, which makes USDC and USDT safer bets than experimental tokens. Major payment processors like Visa, Mastercard, and PayPal integrate stablecoin functionality because regulatory clarity reduces operational risk. XRP faces SEC scrutiny despite recent court victories, while established stablecoins backed by US Treasury bonds offer predictable compliance paths (audit requirements love this stability). Businesses need crypto that passes regulatory tests, not experimental tokens that threaten operations.

Liquidity and Market Depth

Market liquidity determines whether your payments actually execute at expected prices. XRP maintains a $125 billion market cap as the fourth-largest cryptocurrency, which provides deep liquidity for large transactions. Stellar’s $7.9 billion market cap offers sufficient depth for most business needs but may struggle with enterprise-scale transfers. Major stablecoins like USDC and USDT command massive daily volumes that support institutional-grade transactions without price slippage. Thin markets create execution risk that turns predictable costs into expensive surprises.

These technical foundations matter, but the real magic happens when you match crypto capabilities with your specific business requirements and payment corridors.

Which Crypto Actually Works for Business Payments

USDC dominates business cross-border payments with $75 billion market cap and Circle backing that includes BlackRock reserves. Visa partnered with Circle for stablecoin settlements across Latin America, while Mastercard enables USDC transactions across Eastern Europe and Africa. The regulatory framework under the Clarity for Payment Stablecoins Act gives USDC predictable compliance paths that enterprise finance teams demand. USDT processes $23 trillion in annual volume but faces regulatory uncertainty that makes USDC the safer enterprise choice. Fiserv launches FIUSD by year-end 2025 specifically for bank-to-bank settlements, while Klarna tests KlarnaUSD to cut international payment costs.

XRP Commands Banking Infrastructure

XRP commands institutional adoption through RippleNet partnerships with major banks for cross-border settlements. Ripple’s $1.2 billion Hidden Road acquisition positions the network to handle massive institutional transaction volumes. The company applied for a US national bank charter to deepen bank relationships and operational capabilities. XRP’s $125 billion market cap provides liquidity depth that supports enterprise-scale transfers without price slippage. Major financial institutions already leverage Ripple infrastructure to streamline international payment processes (making XRP the established choice for bank partnerships).

Stellar Targets Emerging Markets

Stellar Aid Assist enables NGOs to distribute humanitarian aid efficiently, notably during the Ukraine crisis. The network’s sub-penny transaction costs make micro-payments profitable in emerging markets where traditional banks charge prohibitive fees. Stellar’s $7.9 billion market cap targets remittances and low-cost transfers rather than high-margin institutional markets. The network processes 2-5 second settlements that compete directly with traditional money transfer services. African and Latin American markets show higher Stellar usage relative to GDP (reflecting its focus on underserved regions where cost matters more than sophisticated financial services).

Enterprise Payment Processors Join the Game

Major payment processors integrate stablecoin functionality to compete with traditional wire transfers. Stripe allows subscription payments with stablecoins that settle as fiat currency for merchants. PayPal, Visa, Mastercard, and Fiserv develop stablecoin solutions to enhance payment systems and reduce cross-border friction. These partnerships signal mainstream adoption that makes crypto payments less risky for conservative finance teams. The integration happens behind the scenes while businesses enjoy faster settlements and lower costs.

Smart businesses match these crypto options with their specific payment corridors and compliance requirements to build effective international payment strategies.

How Do You Actually Implement Crypto Payments

API integration determines implementation success, not blockchain complexity. Stripe enables stablecoin payments through existing merchant accounts with simple API calls that settle as fiat currency. PayPal Business accounts now support USDC transactions with standard integration processes that require zero blockchain expertise from your development team. Fiserv partners with banks to provide direct stablecoin settlement through existing APIs, while Visa Direct pilots pre-funded stablecoin accounts for financial institutions. Choose processors that handle blockchain complexity behind familiar payment interfaces your team already knows.

Start Small and Scale Smart

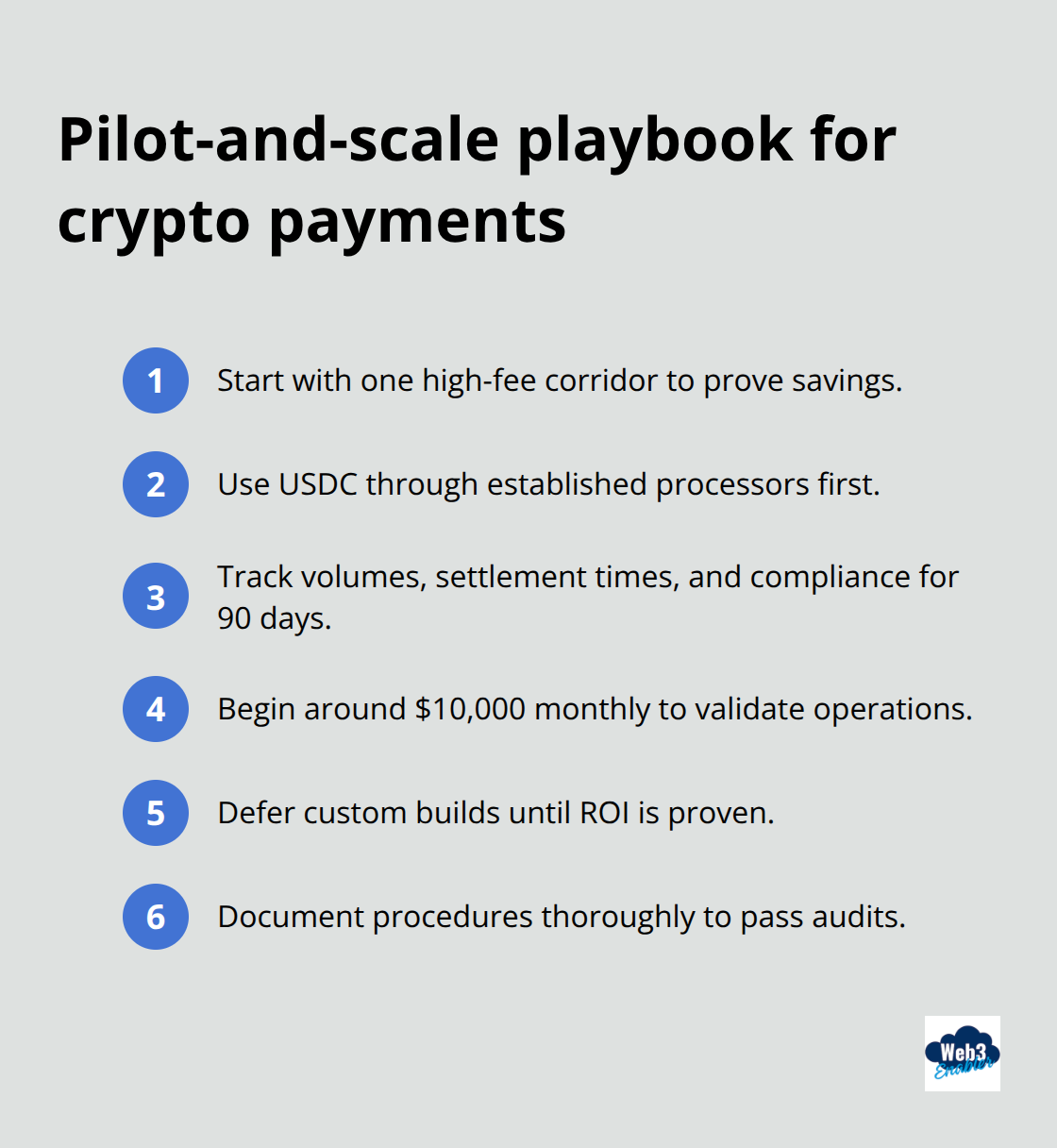

Pilot programs prevent costly mistakes that sink crypto payment initiatives. Begin with one payment corridor like US-to-Mexico remittances where traditional fees reach 8-12% and crypto saves substantial money immediately.

Test USDC payments through established processors before you build custom infrastructure that costs $500,000+ in development resources. Monitor transaction volumes, settlement times, and compliance reports for 90 days minimum before you expand to additional markets. Most businesses start with $10,000 monthly volumes to validate processes, then scale to enterprise levels once operational procedures prove reliable. Document every step because regulatory audits demand clear paper trails that traditional payments never required.

Compliance Automation Beats Manual Processes

AML and KYC compliance automation prevents regulatory disasters that shut down payment operations. Machine learning models analyze transaction patterns in real-time to flag suspicious activity before regulators notice problems. Chainalysis and Elliptic provide blockchain monitoring tools that banks trust for compliance reports, while TRM Labs offers real-time risk scores for crypto transactions. Set transaction limits at $50,000 per transfer initially because larger amounts trigger additional reports across most jurisdictions (automated systems handle technical monitoring while humans manage exception handling and regulatory communication).

Staff Training That Actually Works

Focus staff training on recognizing compliance alerts, not understanding blockchain technology. Your team needs to know how to read transaction status dashboards and escalate unusual patterns to compliance officers. Train finance staff to reconcile crypto payments with existing accounting systems through standard CSV exports that most processors provide. Operations teams learn to monitor settlement times and handle failed transactions through familiar support channels. Technical training stays minimal because modern processors abstract blockchain complexity into standard payment workflows (your existing payment expertise transfers directly to crypto implementations).

Final Thoughts

The best crypto for cross border payments depends on your specific business needs and payment corridors. USDC provides enterprise stability with regulatory clarity and major processor support, while XRP dominates institutional partnerships with deep liquidity. Stellar targets emerging markets with ultra-low fees that make micro-payments profitable. The $250 trillion cross border payment market evolves rapidly as stablecoins reach $273 billion circulation and major processors integrate crypto functionality.

Smart businesses start with pilot programs through established processors rather than custom blockchain development. Focus on high-fee corridors where crypto cuts costs by 80% immediately. Train your team on compliance alerts and transaction monitoring, not blockchain technology (modern processors handle the technical complexity behind familiar payment interfaces).

We at Web3 Enabler build Salesforce-native blockchain solutions that connect crypto payments with your existing corporate infrastructure. Our platform supports stablecoin acceptance and international transfers directly within Salesforce workflows. The future belongs to businesses that adopt crypto payments strategically, not speculatively.