Your payment options are stuck in 2010 while your customers expect 2026 experiences. That’s the gap a solid digital payments strategy closes.

We at Web3 Enabler see businesses leaving money on the table every day-higher transaction costs, slower settlements, and customers abandoning carts because their preferred payment method isn’t available. The good news? Building a modern digital payments strategy isn’t complicated, and the payoff is real.

Why Your Business Needs a Digital Payments Strategy

The US proximity mobile payments market hit $670.5 billion in 2024 and is projected to exceed $1 trillion by 2027. That’s not hype-that’s where your customers are already spending money. Fifty-three percent of Americans now use digital wallets more often than traditional payment methods, which means your checkout experience directly impacts whether customers complete purchases or abandon them mid-transaction. A slow or unsafe checkout wipes out weeks of marketing investment and tanks conversion rates. Your competitors aren’t debating whether to modernize payments anymore; they’re already doing it. If you’re still relying on legacy payment infrastructure, you’re actively losing revenue to businesses that moved faster.

The Real Cost of Staying Behind

Traditional payment systems bleed money in ways that aren’t always obvious. Check processing, manual reconciliation, failed transactions, and fraud losses add up quickly. Real-time cash flow visibility becomes a game-changer when you manage multiple payment channels, because you see exactly where money moves and spot problems before they become expensive disasters. Faster receivables improve working capital management, which directly affects your ability to invest in growth. Digital wallets also reduce payment friction-customers check out in seconds rather than filling out endless form fields-which translates to higher conversion rates and lower cart abandonment. For B2B operations, accepting digital wallets shortens the procurement-to-payment cycle and simplifies supplier onboarding, cutting administrative overhead that drains resources.

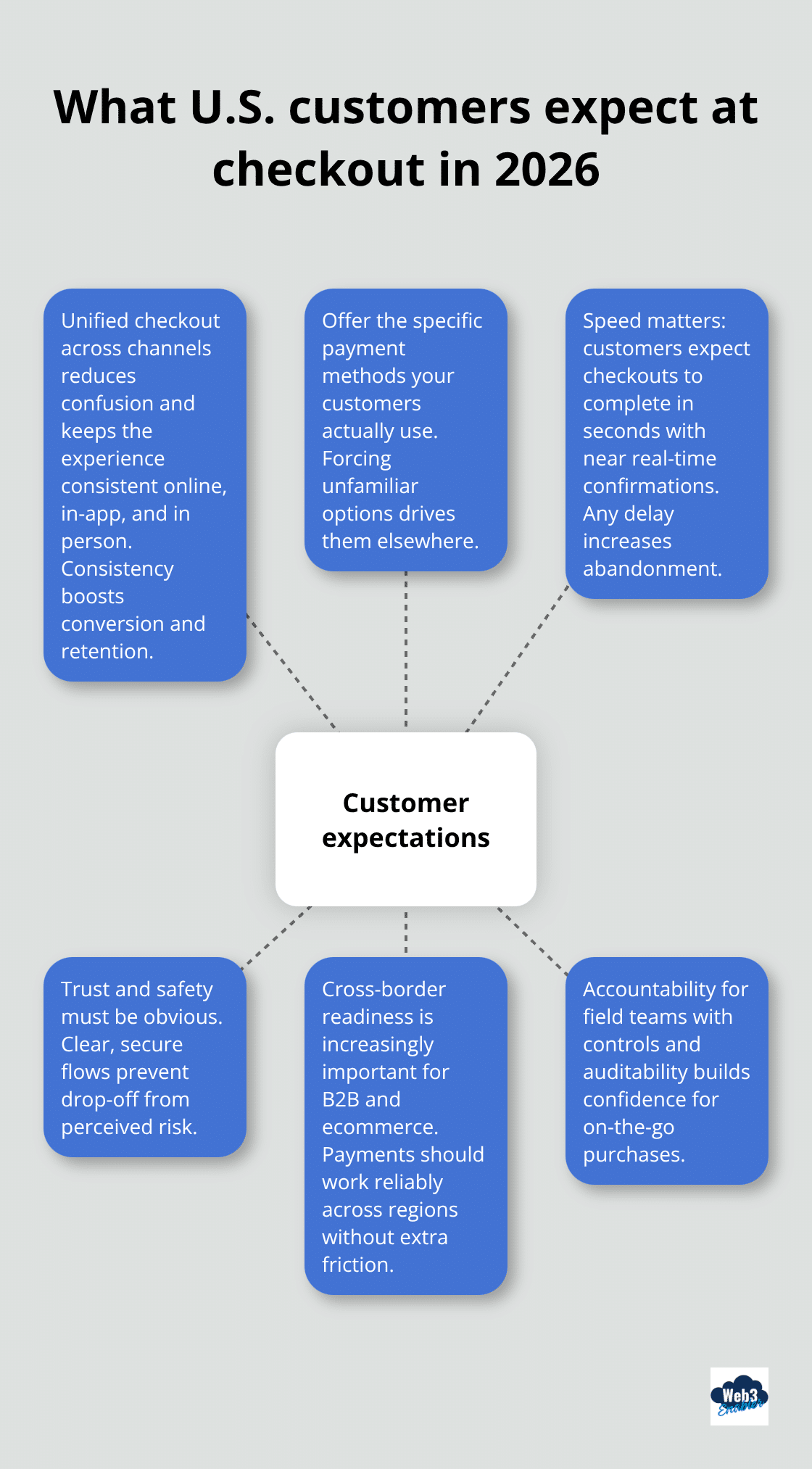

What Customers Actually Expect Now

Your customers don’t want options-they want their preferred payment method. If you force them to use a payment method they don’t trust or don’t have, they’ll go somewhere else. The shift is real and it’s accelerating. Businesses that unify checkout across channels and offer payment methods that match their customer base see measurable improvements in conversion and retention. This isn’t about offering every payment method under the sun; it’s about understanding who your customers are and what they actually use. A construction company’s field teams need to buy materials on the go with full accountability and compliance.

An ecommerce business needs checkout to complete in seconds with near real-time confirmations. A B2B service provider needs transparent, effortless payments that work across borders. Each scenario demands a different approach, which is why a strategy matters more than just bolting on another payment processor.

Now that you understand why digital payments matter, the next step is building a strategy that actually works for your business.

Building Your Digital Payments Strategy

Map Your Current Payment Infrastructure

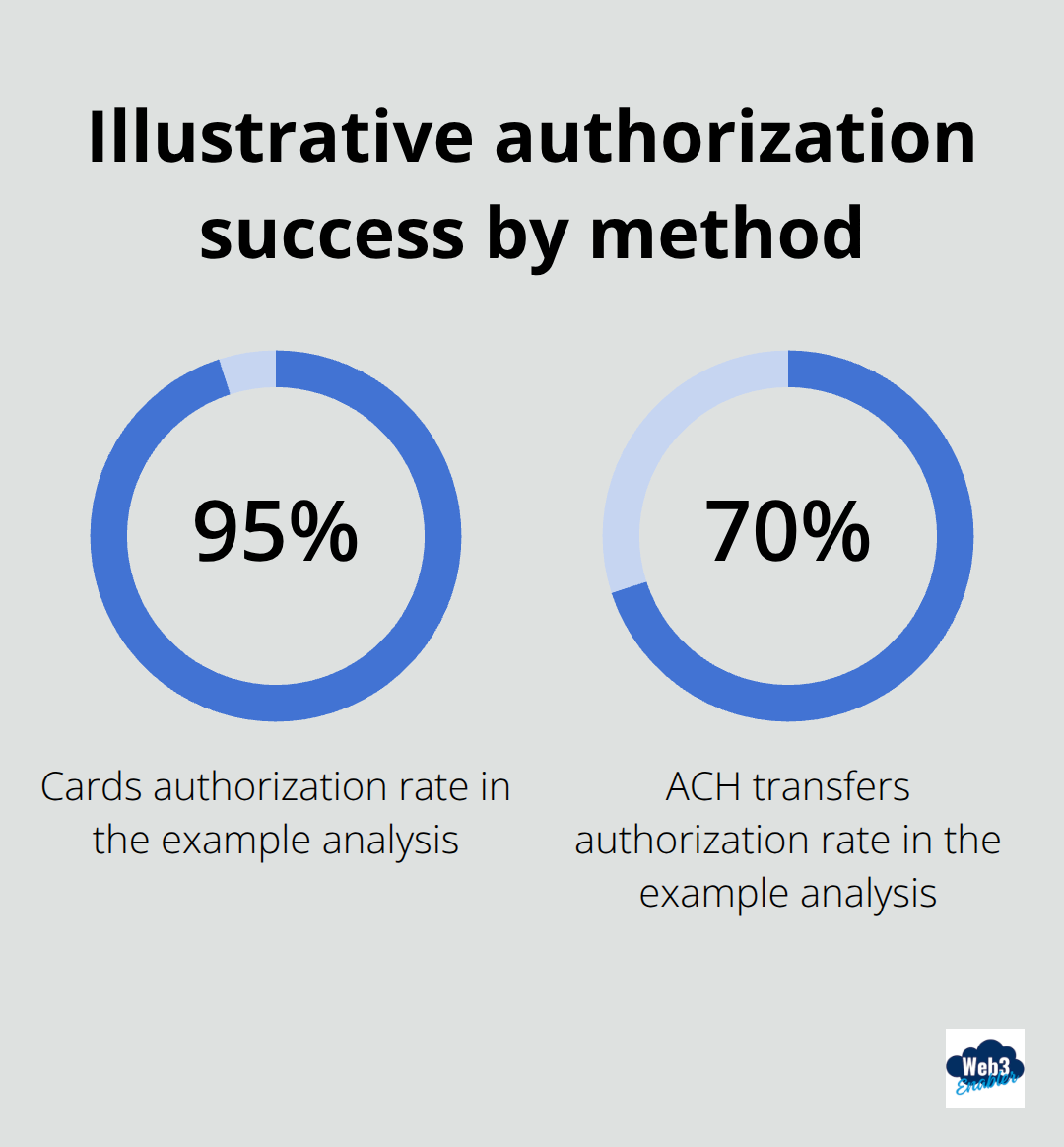

Start by mapping what you actually have right now, not what you think you have. Pull together your payment processors, merchant accounts, banking relationships, and transaction data from the last twelve months. Look at your authorization rates versus decline rates by payment method and geography-this reveals where customers hit friction. If you’re seeing 95% authorization on cards but only 70% on ACH transfers, that tells you something about your customer base and where you need to focus. Check your settlement times across each method; if some payments take three days to clear while others settle in minutes, that gap costs you working capital.

Audit your current fraud and chargeback rates too. The baseline matters because it’s your benchmark for improvement.

Once you see the full picture, you’ll spot the obvious wins: maybe you’re losing 5% of transactions to payment failures that a secondary payment method could recover, or your manual reconciliation eats 40 hours per month that automation could eliminate. This isn’t about replacing everything at once; it’s about identifying which improvements deliver the fastest payoff.

Match Payment Methods to Your Customer Segments

Stop guessing about what payment methods your customers want and start looking at actual behavior. If you’re in B2B, your customers might demand faster settlement and real-time visibility into transactions-digital wallets and virtual cards deliver both. If you’re in ecommerce, your data should show which payment methods convert highest and which have the lowest chargeback rates. Construction and professional services teams that work in the field need to buy essentials on the go with full accountability, which means virtual cards with spending limits and merchant restrictions become non-negotiable. The key is matching payment methods to your specific customer segments, not adopting every option available.

Build Compliance Into Your Roadmap From Day One

Security and compliance can’t be an afterthought. If you’re accepting card payments, PCI DSS compliance is mandatory and shapes how you architect your entire system. If you’re moving toward digital wallets or blockchain-based payments, you need to understand Travel Rule compliance for certain jurisdictions and data residency requirements. Retrofitting compliance later costs far more than planning ahead. Your payment infrastructure should handle 10x your current transaction volume without melting down. That means choosing systems and partners that grow with you, offer real-time reporting for instant visibility into what’s happening, and provide smart routing across multiple gateways so a failure at one processor doesn’t crash your entire operation.

With your current infrastructure mapped, your customer segments identified, and your compliance framework in place, you’re ready to explore how blockchain and stablecoins fit into your strategy-and whether they’re the right move for your business.

When Should You Add Blockchain Payments to Your Mix

Stablecoins Solve Specific Problems Your Current Setup Can’t Handle

Stablecoins aren’t a replacement for your existing payment infrastructure-they’re an addition that solves specific problems your current setup can’t handle efficiently. The real value emerges when you manage cross-border payments, need settlement to happen faster than traditional rails allow, or want to reduce the cost and friction of international transactions. Visa piloted USDC settlement on Solana, Stripe enabled USDC payments and settlement, and Shopify added USDC checkout because these companies identified customer segments where blockchain payments deliver measurable advantages. The mechanics are straightforward: a stablecoin payment settles on-chain without requiring multiple intermediaries or correspondent banks, which means you avoid the delays and liquidity constraints that plague traditional cross-border transfers.

Where Blockchain Payments Win Against Traditional Systems

For a B2B company sending payments to vendors across five countries, blockchain settlement can compress a three-to-five-day process into minutes while cutting wire fees and currency conversion markups. For an ecommerce business accepting USDC at checkout, you gain immediate settlement certainty and eliminate chargeback risk because blockchain payments are push-based-the customer authorizes the transaction directly rather than giving a merchant permission to pull funds. This matters more than it sounds: chargebacks cost you time, fees, and customer relationships. Stablecoins also enable programmable payments, meaning you can automate recurring payouts, enforce spending limits on corporate virtual cards, and trigger actions based on transaction conditions-capabilities that traditional payment processors charge premium fees for or don’t offer at all.

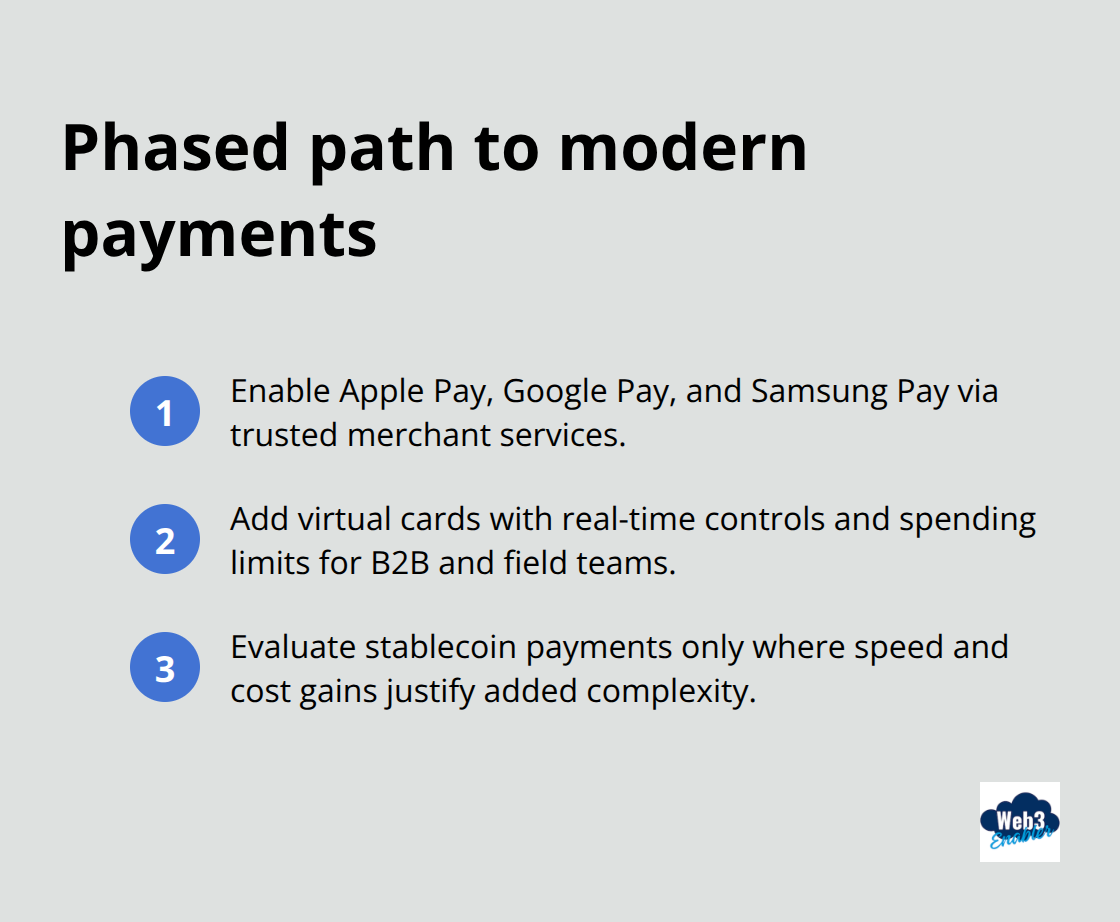

The Phased Approach: Start Small, Scale Smart

The practical path forward is phased, not revolutionary. Start by accepting wallet payments through trusted brands like Apple Pay, Google Pay, and Samsung Pay using merchant services that handle the technical complexity for you. This step costs almost nothing and immediately improves checkout speed and customer experience. Next, explore whether your B2B customers or field teams would benefit from virtual cards with real-time usage controls and spending limits-these integrate with your existing cash management tools and enforce compliance automatically.

Only after you’ve optimized those layers should you evaluate stablecoin payments for specific corridors where the speed and cost advantages justify the additional complexity.

Learn From Companies That Got It Right

GrabPay added USDC and USDT with XSGD conversion because their Southeast Asian customer base needed faster, cheaper cross-border settlement. Revolut moved toward blockchain payment capabilities because their user base demanded it. The difference between these companies and most others is that they didn’t start with blockchain; they started with customer pain points and worked backward to identify which payment rails solved them best. Your customers probably aren’t demanding stablecoins yet, but they’re definitely demanding faster checkouts, lower fees, and payment methods that actually work in their region. Build toward blockchain payments strategically, not ideologically, and you’ll find the right moment to integrate them into your stack.

Final Thoughts

Start your audit today by examining what you have right now-your current processors, settlement times, authorization rates, and fraud losses form your baseline for improvement. Match your payment methods to your actual customer segments, not to assumptions about what they want, and build compliance into your roadmap from the beginning because retrofitting security costs far more than planning ahead. The blockchain and stablecoin layer comes later, once you’ve optimized your core payment infrastructure through wallet acceptance, virtual cards, and real-time visibility.

The competitive advantage doesn’t come from offering every payment option available; it comes from having the right ones for your customers, integrated seamlessly, and working reliably. We at Web3 Enabler help businesses connect blockchain technology with their existing infrastructure, making it simple to accept stablecoin payments and send global payments faster without the speculation noise. If you’re ready to explore how blockchain fits into your digital payments strategy, we can show you the practical path forward.

That advantage compounds over time as you capture more revenue, reduce friction, and build customer loyalty through faster checkouts and transparent transactions. The question isn’t whether to move forward-it’s how fast you can get started.

Frequently Asked Questions About Building a Digital Payments Strategy

What is a digital payments strategy?

A digital payments strategy is your plan for which payment methods you accept, how payments flow across channels, and how you manage settlement, fraud, reporting, and compliance. It aligns payment options with your customer segments so checkout is fast, trusted, and reliable.

Why does my business need a digital payments strategy in 2026?

Customer behavior has shifted heavily toward mobile and wallet-based payments. US proximity mobile payment transaction value was estimated around $670.5B in 2024 and is forecast to pass $1T by 2027, which means modern checkout expectations are now mainstream, not optional.

How do digital wallets impact conversion and cart abandonment?

Digital wallets reduce checkout friction by removing manual card entry and speeding up authorization. Surveys also show 53% of Americans used digital wallets more often than traditional payment methods in 2023, so missing wallet options can directly increase abandonment and lost revenue.

Which payment methods should I prioritize first?

Start with the methods your customers already use most: cards plus major digital wallets like Apple Pay and Google Pay for consumer checkout, and ACH or bank transfer options where appropriate. Then add secondary methods strategically, such as virtual cards for B2B controls or stablecoins for specific cross-border corridors.

How do I map my current payment infrastructure the right way?

Inventory every processor, merchant account, banking relationship, and payment method, then pull 12 months of transaction data. Track authorization rate vs decline rate by method and geography, settlement timelines, average fees, chargebacks, and the hours spent on reconciliation so you can measure improvements against a baseline.

What are authorization rates, and why do they matter in a payments strategy?

Authorization rate is the percentage of attempted transactions that are approved. Low authorization rates usually indicate avoidable friction, such as poor routing, limited local payment methods, issuer declines, or overly aggressive fraud rules, and improving it can raise revenue without increasing traffic.

What are virtual cards, and when should a business use them?

Virtual cards are digital card numbers you can issue with controls like spending limits, time windows, and merchant restrictions. They are especially useful for B2B purchasing, field teams, and vendor payments where you need accountability and policy enforcement without slowing down procurement.

How do I build compliance and security into my payments roadmap?

Plan security and compliance from day one. If you accept card payments, PCI DSS applies to entities that store, process, or transmit cardholder data, so your architecture, vendors, and processes need to support those requirements. If you add blockchain or stablecoin payouts, you also need to design for Travel Rule obligations in relevant jurisdictions.

How can I reduce chargebacks and fraud without hurting good customers?

Use layered controls: strong identity verification where needed, risk-based authentication, device and behavioral signals, and clear dispute management. Also segment rules by channel and customer type, and monitor false declines, because overly strict fraud filters can reduce authorization rates and hurt revenue.

When should I add blockchain or stablecoin payments to my digital payments strategy?

Add stablecoins when they solve a measurable problem your current rails cannot, usually cross-border speed, settlement timing, or cost. Most businesses win by optimizing wallets and routing first, then adding stablecoins selectively for the payment corridors and customer segments where the ROI is clear.

What is the best way to roll out a modern payments strategy?

Take a phased approach: add wallet acceptance first for quick conversion wins, introduce virtual cards or better bank payment options for operational control, then pilot stablecoins for specific cross-border use cases. Run pilots with real transactions and track settlement time, fees, fraud, and reconciliation hours before scaling.