Your ecommerce business is bleeding money on currency conversions and international payment delays. Stablecoins for ecommerce fix this-they’re fast, cheap, and they work across borders without the banking middleman taking a cut.

We at Web3 Enabler have watched sellers discover that accepting stablecoins isn’t some futuristic experiment anymore. It’s a competitive advantage happening right now.

Why Stablecoins Actually Matter for Your Bottom Line

The Math That Makes Traditional Payments Look Outdated

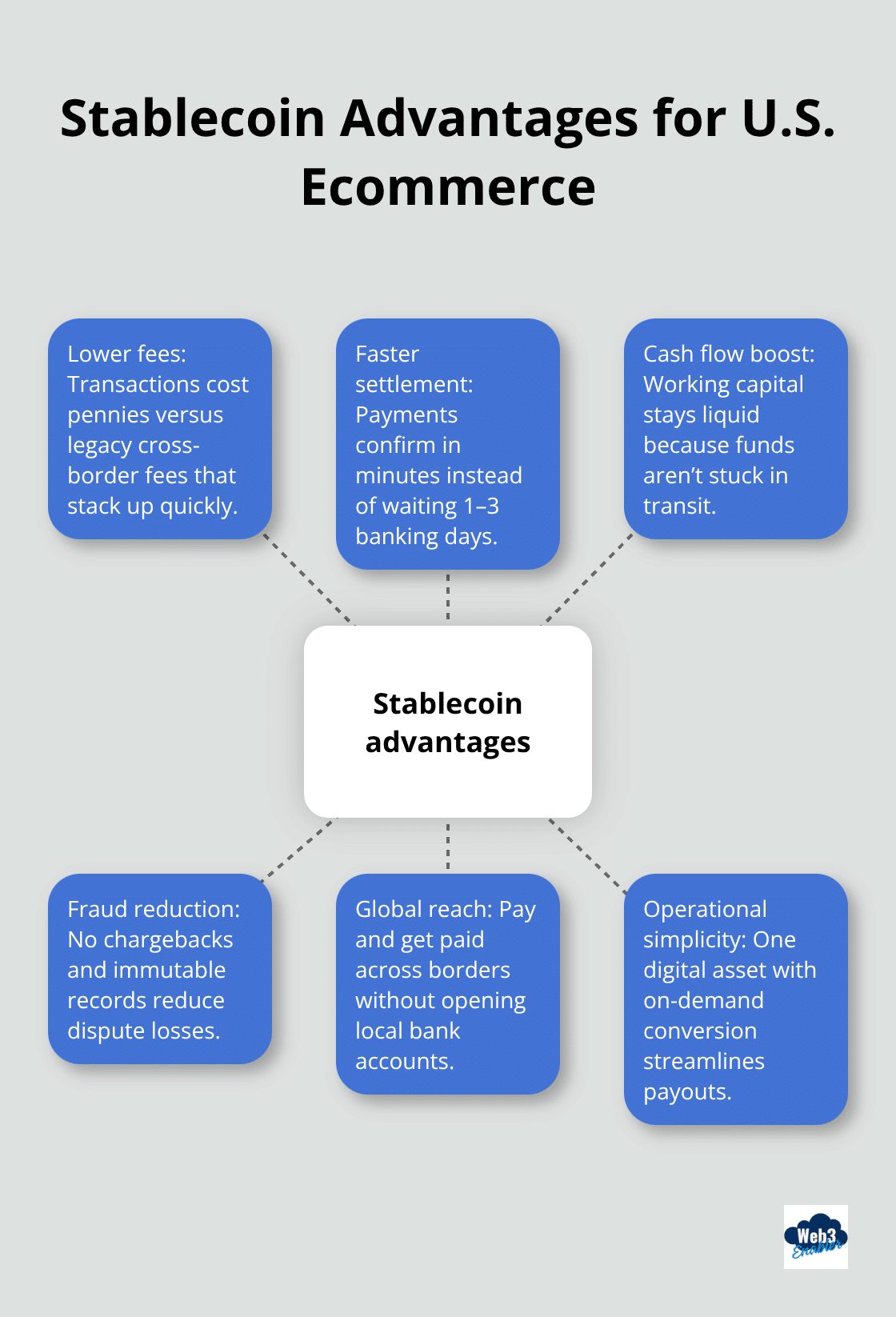

Traditional international payments drain 6.49% in fees alone, according to World Bank data, before currency conversion spreads that banks don’t advertise even enter the picture. When you sell globally, that’s money vanishing before it hits your account. Stablecoins eliminate this entirely. A vendor in Mexico receives payment in minutes for pennies in network fees-no wire transfer delays, no hidden FX markups. In 2024, stablecoins processed over 27 trillion dollars in transactions, surpassing Visa and Mastercard combined. That’s not hype; that’s real volume moving through the system.

Speed That Actually Matters to Your Cash Flow

Sellers move fast toward stablecoins because blockchains don’t sleep. Networks like Ethereum, Solana, and Polygon settle transactions instantly while traditional banks still operate on a 1-3 day cycle. You’re not waiting for intermediaries to shuffle money around-settlement happens in minutes, which means your working capital stays liquid instead of sitting in transit. For sellers managing marketplace payouts or paying contractors across continents, that operational upgrade transforms how you manage cash flow.

The Real Cost Comparison Nobody Talks About

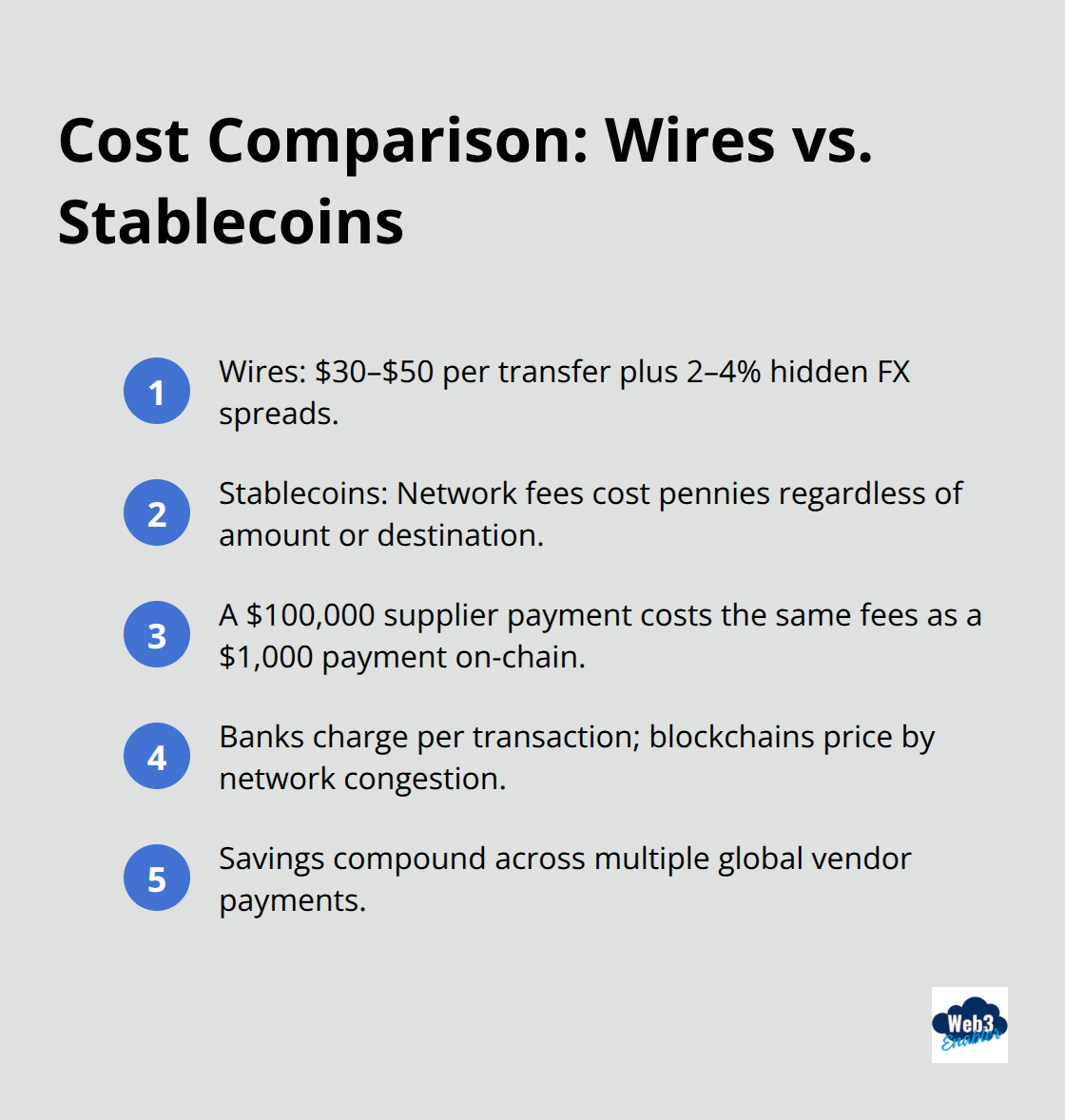

Wire transfers average 30-50 dollars per transaction plus 2-4% in hidden FX spreads. Stablecoin transfers cost pennies-literally cents-regardless of amount or destination. A 100,000 dollar payment to a supplier in Singapore costs the same in fees as a 1,000 dollar payment. Blockchains charge by network congestion; banks charge per transaction. For businesses paying multiple vendors globally, the cumulative savings compound fast.

You also avoid maintaining local bank accounts in every currency zone. Instead, you hold stablecoins and convert only when you actually need local currency for payroll or taxes. That flexibility means fewer dormant accounts, less compliance overhead, and faster cash flow management.

Why USDC and USDT Lead the Pack

USDC and USDT drive adoption because regulated entities issue them with transparent reserves and widespread exchange support. Circle, the issuer behind USDC, operates under regulatory oversight in multiple jurisdictions, which matters when you move real business money. The irreversibility of on-chain payments sounds risky, but it’s actually a feature for sellers. No chargebacks, no disputes after the fact. That certainty lets you price more aggressively for international buyers and reduces the fraud losses that plague traditional ecommerce.

Fraud risk drops dramatically too. Stablecoin transactions are immutable and recorded on-chain with cryptographic verification, making them harder to dispute falsely or reverse fraudulently compared to credit card chargebacks. You get transparency and finality that traditional payments simply can’t match-and that’s exactly what makes accepting stablecoins the logical next step for any seller serious about global expansion.

What Do Stablecoin Payments Actually Save You

The savings from stablecoin payments hit your bottom line immediately, not someday in the future. A seller paying ten vendors across five countries via wire transfer spends roughly 300 to 500 dollars monthly in fees alone, plus another 2 to 4 percent in hidden FX spreads that banks bury in the exchange rate. Switch those same payments to stablecoins and you’re looking at maybe 10 dollars total in network fees, regardless of amount or destination. For a business processing 500,000 dollars in monthly vendor payments, that translates to between 10,000 and 20,000 dollars annually recovered from fees that currently vanish. The math gets more aggressive when you factor in working capital.

Traditional cross-border payments lock your money in transit for 1 to 3 days while banks shuffle it through correspondent networks. Stablecoins settle in minutes, which means your cash converts to local currency only when you actually need it for payroll or taxes. That operational shift alone can free up 50,000 to 100,000 dollars in working capital for a mid-sized ecommerce business-cash you can reinvest in inventory or marketing instead of letting it sit dormant in bank accounts across different countries.

Settlement Speed Transforms Your Operations

Instant settlement changes how you manage marketplace payouts and contractor payments. Traditional methods force you to predict payment volumes days in advance and pre-fund local accounts in multiple currencies-a nightmare for seasonal sellers or those with volatile payout schedules. Stablecoins flip this model entirely. You hold stablecoins centrally and push payments out on demand, settling in minutes rather than days. A marketplace paying 500 sellers daily in 15 different countries no longer needs 15 separate bank accounts or complex treasury management systems. You send stablecoins to seller wallets and they convert to local currency when ready, or immediately through integrated onramps that handle the conversion. This flexibility means smaller sellers can accept payments globally without maintaining expensive banking relationships in each region.

Why Irreversibility Works in Your Favor

The irreversibility of blockchain transactions actually works in your favor here-no chargebacks, no disputes after settlement, no fraud reversals eating into your margins weeks later. That certainty lets you price more competitively for international transactions and reduces the 2.4 percent average chargeback rate that crushes ecommerce margins. You eliminate the fraud losses that plague traditional ecommerce because stablecoin transactions are immutable and recorded on-chain with cryptographic verification, making them harder to dispute falsely or reverse fraudulently compared to credit card chargebacks.

Breaking Into Markets Without Traditional Banking

Stablecoins remove the biggest barrier to global expansion: the requirement to establish banking relationships in every market you want to serve. A seller in Nigeria can receive USDC instantly without needing a US dollar bank account or navigating the approval process that traditional banks demand. In 2024, stablecoins processed over 27 trillion dollars in transactions, with roughly two-thirds of that volume moving through stablecoins in digital wallets. That volume concentration shows where adoption is strongest-in emerging markets and cross-border commerce where traditional banking is expensive or inaccessible. For your business, this means marketplace sellers in underbanked regions become viable partners instead of logistical nightmares. You’re not maintaining local accounts or dealing with compliance complexity that traditional banks layer onto international payments. Instead, you offer sellers a direct stablecoin payout option and let them handle conversion to local currency on their timeline. The operational simplicity alone reduces your accounts payable workload while simultaneously improving payment speed for your partners.

What Comes Next for Your Payment Stack

These savings compound when you integrate stablecoin payments into your existing infrastructure. The next chapter explores how to actually implement this-choosing the right provider, connecting it to your store, and setting up the compliance framework that makes stablecoin payments work alongside your current operations.

Getting Started With Stablecoin Payments

Starting with stablecoins doesn’t require ripping out your existing payment infrastructure or hiring a blockchain team. The reality is simpler: you need a payment provider that handles the conversion between stablecoins and fiat, integrates cleanly with your ecommerce platform, and manages compliance so you don’t have to become a regulatory expert overnight. Stripe Payments accepts stablecoins globally across 195 countries while settling directly into your Stripe balance in fiat currency. That means your accounting team sees dollars, not USDC, and your existing workflows stay intact. The integration takes hours, not weeks. You connect Stripe’s API to your store, enable stablecoin as a payment method alongside credit cards, and customers pay in USDC or USDT while you receive settlement in your preferred currency. No wallet confusion for your customers, no treasury management headaches for you.

Choose Your Payment Provider Wisely

Other providers like Circle’s Payments Network exist for enterprise-scale operations, but unless you process millions monthly or need direct on-chain settlement, Stripe handles 95 percent of ecommerce use cases without unnecessary complexity. The provider you select should offer three things: automatic fiat conversion so your team never touches blockchain mechanics, compliance automation that screens transactions against sanctions lists, and accounting integration that feeds transaction records into your existing software. Stripe covers all three. Your payment provider becomes the bridge between your customers’ wallets and your bank account, handling the technical and regulatory complexity that would otherwise consume weeks of your time.

Run a Controlled Pilot First

Start small with a single payment flow instead of trying to accept stablecoins everywhere simultaneously. If you run a marketplace, enable stablecoin payouts to sellers in one region first-perhaps your highest-volume vendors in countries where traditional wire transfers are slowest or most expensive. This controlled pilot reveals real operational friction before you roll out globally. You’ll discover whether your accounting software can handle the conversion records, whether your sellers actually want stablecoin settlement, and what compliance questions your legal team raises. After two weeks of live transactions, you’ll know exactly what to fix before expanding.

For ecommerce stores, test stablecoin checkout on your highest-value customer segment-international buyers who currently abandon carts due to payment friction or currency conversion costs. Measure conversion rate improvement, average order value, and repeat purchase behavior. Real data beats theoretical projections every time. The compliance piece matters more than most sellers realize. KYC and AML screening still apply to stablecoin transactions, meaning you verify customer identity and screen against sanctions lists. Stripe handles this automatically through its fraud detection tools, but if you build custom integration, you’ll need to implement these checks yourself or partner with a compliance provider.

Handle Compliance and Accounting Correctly

For payouts to vendors, Travel Rule compliance requires you to report transaction details to financial authorities in certain jurisdictions-another layer Stripe manages for you. Your accounting team needs to understand that stablecoin conversions create taxable events. A payment received in USDC and converted to USD triggers a transaction record that your accountant must log for tax purposes. Most accounting software now supports stablecoin transactions, but verify this before going live. QuickBooks Online, Xero, and similar platforms have added blockchain transaction support, though you may need to manually categorize conversions initially until automation improves.

The compliance and accounting setup takes longer than the technical integration, so start these conversations with your finance and legal teams immediately rather than treating them as afterthoughts. Your legal team should review the stablecoin issuer’s regulatory status. This verification matters when you move real business money across borders.

Execute Your Launch Timeline

The competitive advantage belongs to sellers who ship stablecoin acceptance this quarter, not next year. Your competitors are still haggling with banks about wire transfer fees while you’ve already automated vendor payouts to 50 countries in minutes. The actual implementation moves quickly once you commit. Stripe integration typically takes 48 to 72 hours of engineering time. Compliance review takes one to two weeks depending on your jurisdiction and transaction volume. Accounting setup takes another week. Total timeline from decision to live: one month. That’s not a long runway. Set a launch date, assign owners to technical integration and compliance review, and treat this like any other product launch-because it is.

The sellers moving fastest are the ones who stop waiting for perfect blockchain understanding and start accepting stablecoins with their existing payment processor. You don’t need to become a stablecoin expert. You need to know that USDC carries full cash backing, that transfers cost pennies, and that settlement happens instantly. Everything else-wallet management, blockchain mechanics, custody-your payment provider handles behind the scenes.

Final Thoughts

Stablecoins for ecommerce aren’t coming-they’re already here, reshaping how global transactions work. In 2024, stablecoins processed over 27 trillion dollars in transactions, outpacing Visa and Mastercard combined. That volume represents real businesses moving real money across borders in minutes instead of days, paying pennies instead of percentages in fees.

The sellers winning right now stopped waiting for perfect blockchain literacy and started accepting stablecoins through providers like Stripe. They’re not blockchain experts-just business owners who realized that instant settlement, transparent fees, and access to underbanked markets translate directly into competitive advantage. Your competitors still negotiate with banks about wire transfer timelines while you automate vendor payouts to 50 countries before lunch, and that operational gap compounds fast.

We at Web3 Enabler help businesses connect blockchain technology with existing infrastructure like Salesforce, making stablecoin payments work seamlessly alongside your current operations. Web3 Enabler can guide your implementation with tools built specifically for business payments, compliance, and automation. The competitive advantage belongs to early adopters, and that window closes fast.