Your finance team is probably losing sleep over stablecoin payments. The regulatory landscape keeps shifting, your systems aren’t built for blockchain, and nobody’s quite sure who approves what.

We at Web3 Enabler know this pain point well. That’s why we’ve built this guide to stablecoin payments governance-practical frameworks that actually work inside your existing FinOps structure, not theoretical blockchain fantasies.

What Stablecoins Actually Mean for Your Payment Stack

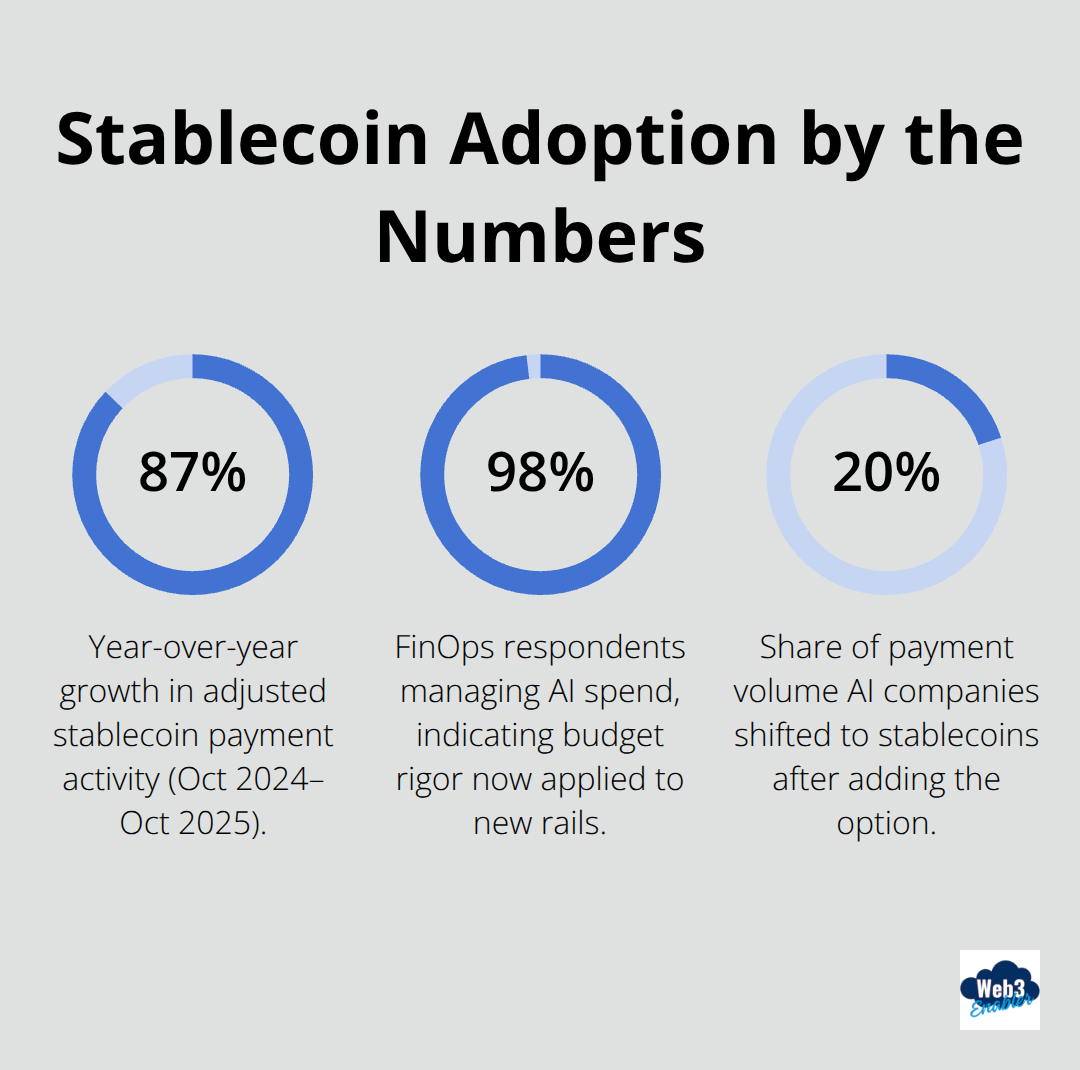

Stablecoins aren’t just another payment method your team can ignore. According to Stripe data, stablecoins processed $9 trillion in adjusted payment activity between October 2024 and October 2025, up 87% year over year. That’s not niche behavior anymore.

Speed and Cost Reshape Your Economics

What separates stablecoins from your credit card rails and wire transfers is speed and cost. Traditional cross-border payments take 3–5 business days and cost 6% or more in remittance fees. Stablecoins settle in minutes on networks like Ethereum, Solana, or Polygon, with flat fees often measured in pennies. They’re also programmable, meaning you can build conditional payouts, escrow logic, and automated splits directly into the transaction itself. That’s functionality your ACH transfers will never touch.

The catch is that stablecoins operate on blockchain infrastructure, which means your finance and ops teams need to understand reserve backing, issuer risk, and custody arrangements. Fiat-backed stablecoins like USDC are backed 1:1 by cash or cash equivalents with audited reserves, making them predictable for pricing and accounting. Crypto-collateralized alternatives rely on overcollateralized digital assets and automated liquidations, which introduces volatility and liquidation risk that your treasury shouldn’t tolerate.

Regulatory Fragmentation Demands Clear Boundaries

The regulatory environment is fractured by region. The US GENIUS Act, expected to reshape reserve requirements and issuer oversight by 2027, signals that stablecoin issuers will face bank-like scrutiny. Meanwhile, emerging markets in Africa, Asia, and Latin America already embed stablecoins into payroll, corporate cash management, and cross-border settlement, according to economist Eduardo Levy Yeyati writing in Project Syndicate. Your governance framework needs to account for this patchwork.

FinOps teams must treat stablecoin adoption as a financial control problem, not a technology experiment. The FinOps Foundation reports that 98% of FinOps survey respondents manage AI spend, up from 31% two years ago, and many of those AI companies shift payment volume to stablecoins. After adding stablecoins as a payment option, AI companies moved roughly 20% of their payment volume to them, according to Stripe. That’s measurable demand. Your governance should measure per-transaction costs, settlement speed, liquidity costs, and fraud mitigation ROI the same way you’d track cloud spend or SaaS licensing. Mature FinOps practices emphasize unit economics and cost quantification, and stablecoin governance demands the same discipline. The alternative is chaos: unsanctioned stablecoin experiments, misrouted funds across fragmented networks, and compliance gaps that create liability.

Regulatory Gray Zones Create Real Risk

Stablecoins operate in regulatory gray zones that your legal and compliance teams can’t ignore. Many jurisdictions have overlapping KYC, AML, and licensing requirements that vary by region and by the specific use case. In the US, stablecoins aren’t yet subject to unified federal oversight, though the GENIUS Act signals change is coming. The EU’s Markets in Crypto Assets Regulation takes effect in December 2024 and applies strict reserve and governance rules. Singapore’s Monetary Authority treats stablecoins as payment instruments and demands issuer licensing. Your governance framework should explicitly address which networks and issuers your organization will support based on regulatory maturity and reserve transparency.

Fiat-backed stablecoins with audited, real-time reserve reporting reduce peg risk and regulatory exposure. Algorithmic stablecoins, which peg via software-controlled supply changes, carry historical fragility exemplified by TerraUSD’s collapse in 2022. Your policy should restrict those outright. Cross-border settlement adds complexity because stablecoin transactions lack traditional protections like chargebacks. If a payment goes to the wrong wallet address, it’s irreversible. Your governance needs robust error-handling procedures, dispute mitigation processes, and clear liability rules before you process a single transaction.

Integration Challenges Require Deliberate Design

Your ERP and accounting systems weren’t built for blockchain, and that’s your real constraint. Stablecoin transactions generate on-chain records that don’t automatically feed into QuickBooks, NetSuite, or SAP. Integration challenges are real. You need governance that specifies how stablecoin transactions get recorded, reconciled, and reported.

Try a narrow pilot: a specific payout stream or cross-border workflow where stablecoins solve a concrete problem-faster settlement, lower cost, or reduced currency friction. A pilot lets your team learn network choices, write internal controls, and train staff without disrupting core systems. Accepting stablecoins means choosing infrastructure that fits your existing business, not rebuilding everything from scratch. As you scale, governance should cover network routing decisions, token choices, custody arrangements, and compliance tooling. Blockchain analytics integrated into your payment flow for sanctions screening and transaction monitoring is non-negotiable.

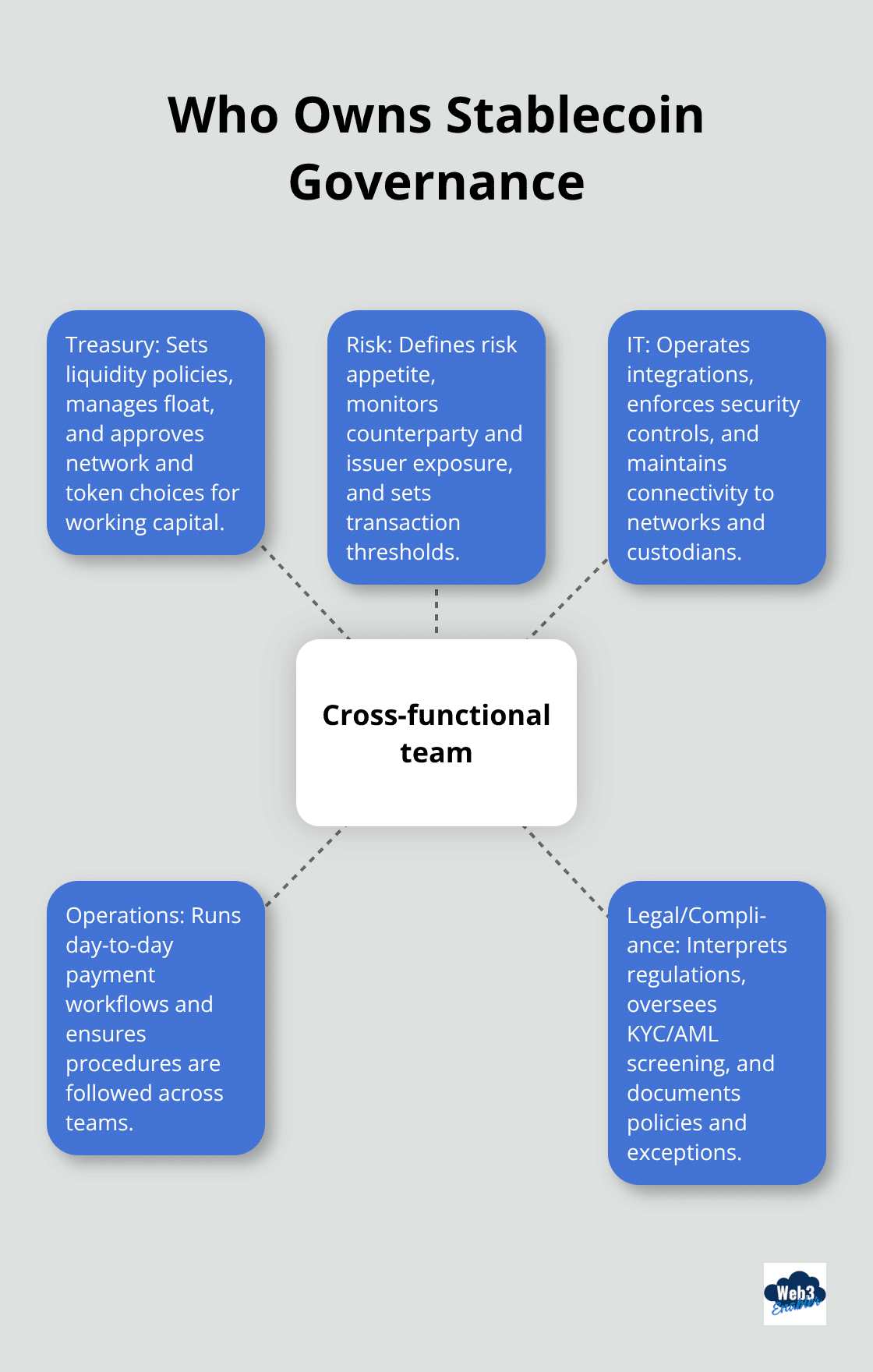

FinOps teams should build a cross-functional governance model spanning treasury, risk, IT, operations, and legal. About 78% of FinOps teams report to CTO or CIO, which means tech leadership sponsorship is essential. Executives significantly influence technology choices, so stablecoin rails and custodians deserve the same board-level scrutiny as cloud providers. With these structural foundations in place, your organization is ready to establish the specific compliance checkpoints and controls that prevent payment chaos.

Building Compliance Into Your Payment Workflows

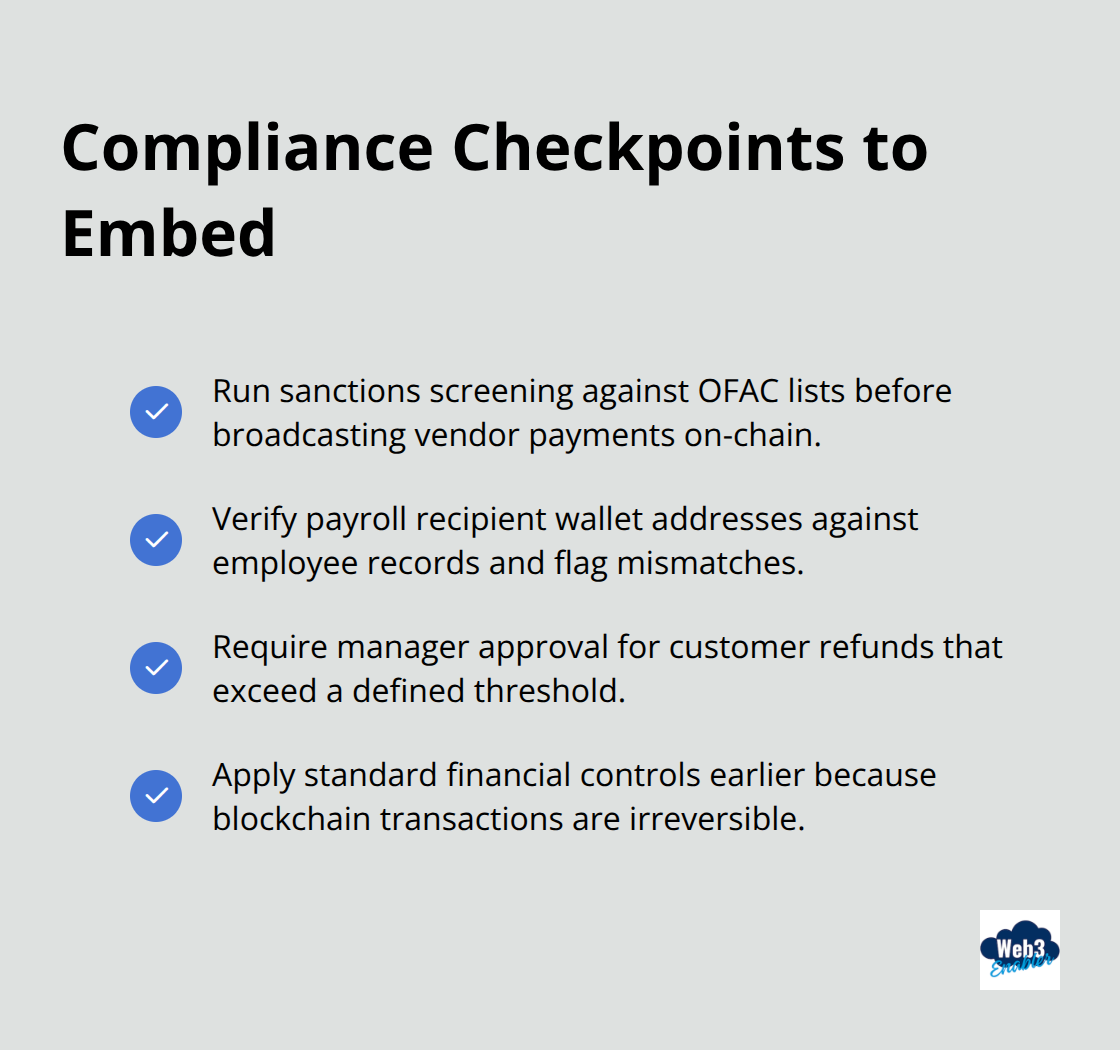

Your stablecoin payments won’t work without compliance checkpoints woven into the actual transaction flow. Compliance must happen before a single dollar moves on-chain, not as a separate box you check afterward. Start by mapping your existing stablecoin payment workflows to identify which transaction types would benefit from faster settlement or lower fees. Then, at each step in that workflow, build a checkpoint.

Embed Compliance at Every Transaction Stage

A stablecoin payment for vendor invoices should trigger sanctions screening against OFAC lists before the transaction broadcasts to the blockchain. A payroll payment should verify the recipient wallet address against employee records and flag any mismatches. A customer refund should require manager approval if it exceeds a threshold. These aren’t blockchain-specific controls; they’re standard financial controls applied earlier in the process because blockchain transactions are irreversible.

Your treasury, compliance, and IT teams need to agree on which networks and stablecoin issuers you’ll support. Not all stablecoins are equal. Fiat-backed options like USDC come with audited reserves and issuer transparency, which reduces peg risk. Crypto-collateralized alternatives introduce liquidation risk that your finance team shouldn’t accept for operational payments. Restrict your organization to fiat-backed stablecoins with real-time reserve reporting.

Select Vendors Based on Governance and Transparency

Your vendor selection process should verify issuer governance and assess issuer quality and track transaction volumes and settlement timelines. This data informs your FinOps budgeting because you can model per-transaction costs, liquidity costs, and settlement speed before you commit volume. Document your choices in a policy that specifies approved networks, approved issuers, transaction limits by user role, and escalation procedures for exceptions.

Bridge Blockchain Records to Your General Ledger

Your accounting and treasury systems won’t automatically recognize blockchain transactions, so you need to build the bridge. Stablecoin transactions generate on-chain records that must reconcile with your general ledger. If you use Salesforce for financial operations, solutions exist that capture stablecoin transactions and map them directly into your finance module without manual workarounds. If you use NetSuite or another ERP, you’ll need custom integration logic or middleware that translates blockchain records into GL entries. The integration should capture the transaction hash, wallet addresses, timestamp, amount, and fee data.

Monitor Transactions in Real Time

Real-time monitoring is non-negotiable. Set up alerts for transactions that exceed thresholds, fail compliance checks, or route to unexpected addresses. Blockchain analytics tools integrated into your payment flow should screen every outbound transaction for sanctions risk and every inbound transaction for source verification. If a payment routes to an address flagged by financial intelligence, the transaction should block automatically. Your team should review blocked transactions within 24 hours and decide whether to escalate, adjust parameters, or reject the transaction outright.

For inbound stablecoin payments, implement transaction monitoring that flags patterns consistent with money laundering or terrorist financing. This is the same monitoring standard you apply to wire transfers and ACH payments, now applied to blockchain. Document every transaction decision in an auditable trail. Apply that discipline to stablecoins by tracking settlement speed, per-transaction fees, liquidity costs, and compliance event frequency. Measure how often your compliance checkpoints block or escalate transactions and whether those rates improve as your team gains experience.

Build a dashboard that compares stablecoin costs and speed against your traditional payment rails. If stablecoins aren’t delivering measurable cost or speed benefits within 90 days of your pilot, don’t scale them. Once you’ve locked in your compliance framework and proven the economics work, your organization faces a different challenge: managing the operational and security risks that come with holding and moving digital assets on-chain.

How to Pick Vendors and Set Payment Limits That Actually Work

Picking the right stablecoin vendor shapes your cost per transaction, settlement speed, compliance risk, and operational headaches for years. Most organizations rush this decision or default to whatever their payment processor offers. That’s a mistake.

Define Issuer Quality Before You Evaluate Vendors

Start by defining what stablecoin issuer quality actually means for your business. Fiat-backed stablecoins with audited reserves reduce peg risk, but issuer governance matters more than most finance teams realize. S&P Global Market Intelligence tracks stablecoin transaction volumes, liquidity, and settlement timelines across issuers, which you should integrate into your vendor scorecard.

Pull that data and compare settlement speed and per-transaction costs across USDC, USDT, and other fiat-backed options your team is considering. A 2-second difference in settlement time might seem trivial until you manage payroll for 500 contractors across five countries. Liquidity matters too. If your chosen stablecoin issuer has thin liquidity in your region, your last-mile conversion to local currency will cost more and take longer.

Document your vendor selection criteria in writing: reserve transparency, issuer financial health, custody arrangement, compliance tooling, and regional liquidity. Have your treasury and legal teams sign off on that criteria before you evaluate a single vendor. This forces alignment and prevents product teams from bypassing governance later.

Set Transaction Limits by Role and Risk

Transaction limits and approval hierarchies prevent chaos when stablecoin payments scale. Set hard limits by transaction type and user role. A junior accountant should not approve a $500,000 cross-border payment; a CFO or controller should. A vendor payment under $10,000 should not require five approvals if your fraud controls are solid.

Your limits should reflect your risk appetite and your ability to reverse mistakes. Since stablecoin transactions are irreversible on-chain, your approval thresholds should be tighter than your ACH or wire transfer limits. If your organization typically approves wire transfers up to $100,000 without escalation, consider capping stablecoin approvals at $25,000 until your team gains operational maturity.

Build an Auditable Approval Trail

Document every approval decision in an auditable trail tied to the transaction hash on-chain. Your finance system should log who approved what, when, and why. If a transaction later becomes subject to regulatory inquiry or internal audit, that trail proves your controls worked.

Reconcile Blockchain Records to Your General Ledger

Reporting standards should specify how you capture stablecoin transaction data, reconcile it to your general ledger, and surface it in financial statements. Blockchain transactions generate hash values, wallet addresses, and on-chain timestamps that don’t map naturally to your accounting system.

Build a reconciliation process that matches on-chain records to your invoice ledger, payment request records, and vendor master files. If your ERP system doesn’t natively support blockchain data, implement middleware or custom logic that translates blockchain records into GL entries within 24 hours of settlement. This delay matters because your month-end close depends on complete transaction data.

Monthly reconciliation should compare your internal stablecoin transaction log against blockchain explorers like Etherscan to verify no transactions were missed or duplicated. Run this reconciliation before your controller signs off on the close.

Wrapping Up

Stablecoin payments governance isn’t a future problem you can defer. Your finance team is already losing sleep over it, and the longer you wait, the more chaotic your adoption becomes. The frameworks we’ve covered-compliance checkpoints, vendor selection, transaction limits, and auditable reporting-aren’t theoretical. They’re the same controls your organization already applies to wire transfers and ACH payments, now adapted for blockchain speed and irreversibility.

The math is straightforward: stablecoins processed $9 trillion in adjusted payment activity between October 2024 and October 2025, up 87% year over year. Your competitors are moving volume to stablecoin rails, and your AI-enabled teams are already shifting roughly 20% of payment volume to them after adding the option.

If your organization hasn’t established clear stablecoin payments governance, you’re either missing cost savings or exposing yourself to compliance risk (probably both).

Start narrow with one payment workflow where stablecoins solve a concrete problem-faster cross-border settlement, lower remittance costs, or reduced currency friction. Run a pilot with clear success metrics: per-transaction cost, settlement speed, and compliance event frequency. We at Web3 Enabler have built tools specifically for this challenge, and our Salesforce-native solutions connect blockchain technology directly to your existing corporate infrastructure, so explore how Web3 Enabler can support your organization and move beyond theory into implementation that actually works.

Frequently Asked Questions

Why should FinOps teams prioritize stablecoin governance now?

Stablecoin volume reached $9 trillion between 2024 and 2025, with AI companies shifting nearly 20% of their payments to these rails. Without a governance framework, organizations face “shadow” crypto experiments, reconciliation gaps in their ERP, and significant compliance liability.

What are the primary cost and speed benefits of stablecoins?

Traditional cross-border payments typically take 3–5 business days with fees up to 6%. Stablecoins settle in minutes on networks like Solana or Polygon with flat fees often measured in pennies. This allows for real-time liquidity management and automated, programmable payouts.

How do you integrate blockchain records with an ERP like NetSuite or SAP?

Since ERPs aren’t built for blockchain, governance must define a “bridge” process. This involves using middleware or Salesforce-native integrations to capture transaction hashes, wallet addresses, and timestamps, translating them into General Ledger (GL) entries within 24 hours to ensure a clean month-end close.

What is the difference between fiat-backed and algorithmic stablecoins?

Fiat-backed stablecoins (like USDC) are backed 1:1 by cash or treasuries and undergo regular audits, making them safe for corporate treasury. Algorithmic stablecoins rely on software and are prone to volatility and “de-pegging,” which introduces unacceptable risk to a professional FinOps structure.

How should a company set stablecoin payment limits?

Because blockchain transactions are irreversible, approval thresholds should initially be tighter than ACH or wire transfers. For example, if a manager can approve $100,000 via wire, a company might cap their stablecoin approval at $25,000 until the team reaches operational maturity.