African businesses are missing out on billions in revenue by relying solely on traditional payment methods. Crypto payments from the EU, UK, and US offer faster settlements, lower fees, and direct access to global customers without intermediaries.

We at Web3 Enabler have seen firsthand how stablecoins like USDC and USDT are transforming Africa crypto payments infrastructure. This guide walks you through everything you need to know to start accepting crypto payments today.

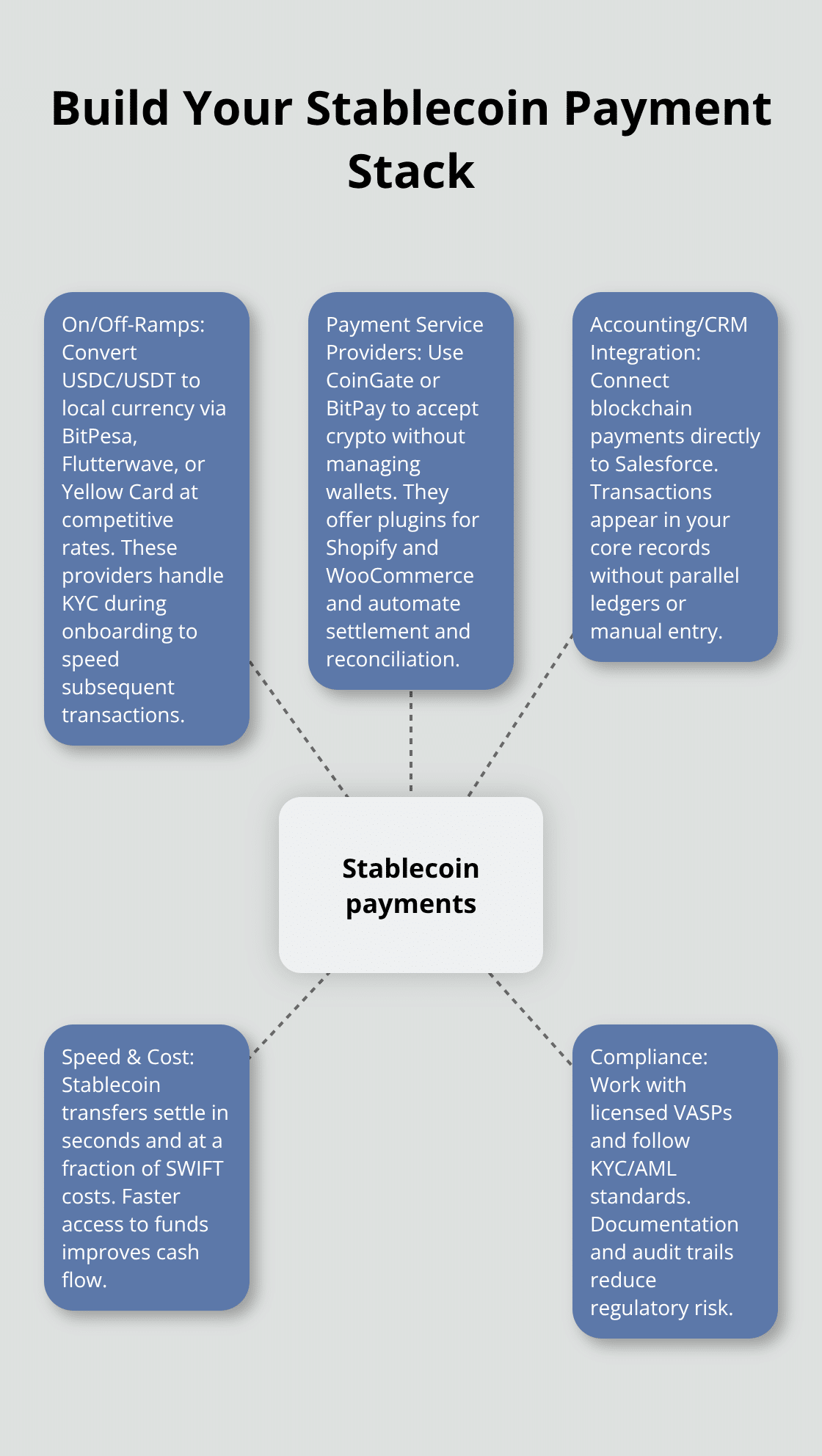

Building Your Stablecoin Payment Stack

USDC and USDT dominate cross-border crypto payments from the EU, UK, and US because they maintain a 1:1 peg to the US dollar, eliminating volatility concerns that plague other cryptocurrencies. USDC, issued by Circle, and USDT, issued by Tether, together account for the majority of stablecoin transaction volume globally. For African businesses, this matters because your EU, UK, and US customers send USDC or USDT instantly, and you receive funds in minutes rather than days. A transfer that costs $55 and takes four business days via traditional SWIFT settles in 12 seconds for under a quarter using stablecoins, according to examples cited by Crowe. The speed advantage translates directly to cash flow-you access funds immediately instead of waiting for correspondent banks to process transfers. Neither USDC nor USDT requires pre-funding accounts or maintaining nostro balances, so capital stays in your business until the moment you need it.

Converting Stablecoins to Local Currency

On-ramp and off-ramp services form the critical bridge between stablecoins and your local currency. BitPesa, Flutterwave, and Yellow Card operate across Kenya, Nigeria, Ghana, and other African markets, converting USDC or USDT directly to your local currency at competitive rates. Yellow Card lets you accept Bitcoin, Ethereum, and stablecoins with instant conversion to local currency, while BitPay supports multiple cryptocurrencies with settlement in your preferred fiat. The best platforms charge between 1% and 3% for conversion, significantly lower than the 5% to 8% you pay through traditional remittance corridors. Luno provides wallet integration for Bitcoin and Ethereum with instant fiat conversion and strong security features. These platforms also handle KYC verification upfront, meaning once you complete onboarding, subsequent transactions move faster. Ghana’s Virtual Asset Service Providers Bill, passed in 2025, creates a licensing framework for these services, which means working with licensed providers protects your business and ensures regulatory compliance as the framework rolls out during 2026.

Integrating Crypto Payments Into Your Operations

Payment service providers like CoinGate and BitPay simplify accepting crypto without managing wallets yourself. CoinGate supports over 50 cryptocurrencies, secure payments, and direct plugins for Shopify, WooCommerce, and other e-commerce platforms, plus invoicing features that integrate with your existing accounting. BitPay offers instant settlement to local currency and strong integrations with major shopping carts, reducing the technical burden of accepting crypto. These providers handle the conversion, settlement, and reconciliation automatically, feeding transactions directly into your accounting system. The real value lies in operational efficiency-you stop managing separate crypto wallets and ledgers and instead treat crypto payments like any other revenue stream within your existing infrastructure.

Connecting Blockchain to Your Business Systems

Your choice of payment infrastructure determines how smoothly crypto transactions flow into your existing business operations. If your business runs on Salesforce, native blockchain integration eliminates manual data entry and keeps all transaction records in one place. Web3 Enabler provides this seamless connection, enabling crypto transactions and settlements to appear directly in your CRM and financial records without separate ledgers or workarounds. This approach transforms crypto from a parallel payment channel into an integrated part of your revenue management. As you scale crypto payments from EU, UK, and US customers, the ability to track, reconcile, and report on these transactions within your core business system becomes essential for maintaining accurate financial records and forecasting cash flow.

Why Crypto Payments Beat SWIFT on Speed and Cost

Settlement Speed: Seconds Versus Days

Stablecoins settle in seconds while SWIFT transfers take days, and the cost difference is staggering. A $100,000 transfer via traditional banking corridors costs roughly $1,500 in fees spread across correspondent banks, currency conversion spreads, and intermediary markups. The same transfer using USDC or USDT settles in 12 seconds for under 25 cents, according to examples cited by Crowe. For monthly cross-border volumes of $500,000 to Asia, this difference compounds to savings of approximately $2,400 per month using blockchain rails instead of legacy systems.

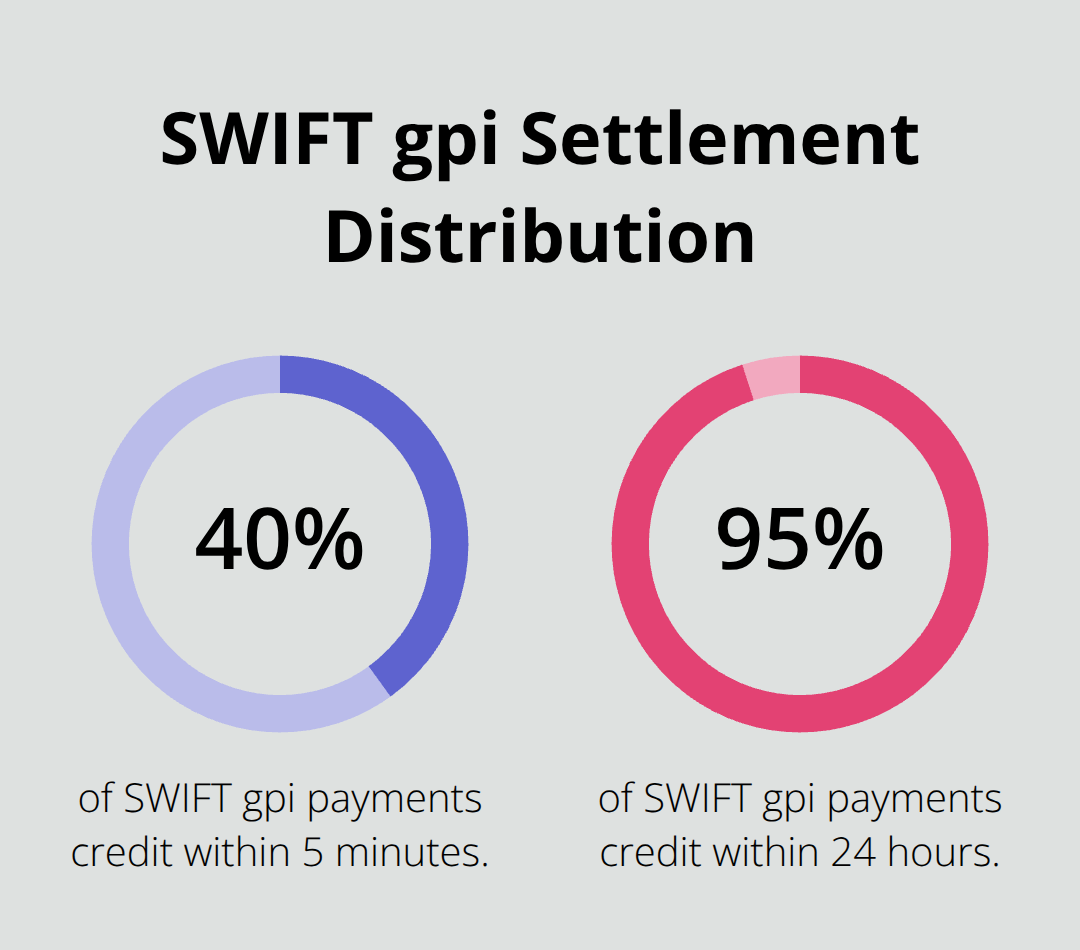

SWIFT’s Global Payments Initiative, launched to counter faster alternatives, has improved speed measurably-40% of payments now credit within 5 minutes and 95% within 24 hours. However, this still lags stablecoin settlement by orders of magnitude, and SWIFT gpi does not reduce the underlying fee structure that makes traditional corridors expensive.

Cash Flow Impact and Working Capital

The real impact shows up in cash flow. When you receive $100,000 in USDT from a UK customer, the funds arrive in your wallet within minutes. You convert to local currency immediately through platforms like BitPesa or Yellow Card at 1% to 3% conversion rates, dramatically cheaper than the 5% to 8% remittance corridors charge. Your cash sits in your account the same day, not locked in a nostro account for three to five business days.

This matters most for African SMEs operating on tight margins-immediate access to customer payments eliminates the need for expensive working capital credit lines that traditional banking forces you to maintain. You stop waiting for correspondent banks to process transfers and instead access funds when you need them.

Transparent Currency Conversion Without Hidden Spreads

Currency conversion through stablecoin rails removes the spread arbitrage that banks embed in cross-border transactions. When a US customer sends USDC, they send exactly 1 USDC per US dollar. You receive exactly 1 USDC, and conversion happens at transparent market rates on platforms like Yellow Card or Luno, not at the inflated mid-market rates banks quote.

Traditional SWIFT corridors quote you a rate that often sits 2% to 4% worse than the actual mid-market rate, a hidden fee most businesses never quantify. Over a year of regular international payments, these spreads cost thousands in value loss. Blockchain networks process international transfers in minutes instead of the days that SWIFT requires, freeing capital that would otherwise sit dormant across currencies.

Blockchain Corridors in Practice

SBI Remit processes thousands of transactions monthly to the Philippines and Vietnam via Ripple, illustrating how targeted blockchain corridors outperform SWIFT for specific high-volume routes. These platforms handle the conversion, settlement, and reconciliation automatically, feeding transactions directly into your accounting system. The real value lies in operational efficiency-you stop managing separate crypto wallets and ledgers and instead treat crypto payments like any other revenue stream within your existing infrastructure.

For African businesses, the practical strategy is clear: use stablecoin rails for EU, UK, and US payments where speed and cost matter most, while maintaining SWIFT connectivity for universal reach to markets where crypto payment infrastructure remains immature. This hybrid approach gives you the efficiency advantage without sacrificing access to global payment networks. As you scale crypto payments from international customers, the ability to track, reconcile, and report on these transactions within your core business system becomes essential for maintaining accurate financial records and forecasting cash flow.

Compliance and Risk Management Across Borders

Ghana’s Regulatory Framework Protects Your Business

Africa’s regulatory environment for crypto payments is hardening fast, and this shift works in your favor if you move now. Ghana’s Virtual Asset Service Providers Bill will establish a licensing and supervision framework. The Bank of Ghana will oversee digital asset service providers, requiring licenses and compliance with reporting standards while allowing individuals to trade cryptocurrency legally. This means the off-ramps and payment providers you work with must obtain licenses and meet consumer protection standards, which eliminates the operators that plagued African crypto markets two years ago.

About 3 million Ghanaians, roughly 17% of the adult population, have engaged in crypto transactions, with annual volumes reaching approximately $3 billion in the year ending June 2024. Ghana’s framework emphasizes consumer protection and financial stability, drawing lessons from the 2022 crypto downturn to prevent systemic risk. Noncompliant operators face sanctions or closure, so partnering with regulated platforms protects both your funds and your business reputation.

Working with Licensed VASPs

For your business, one actionable priority stands out: work exclusively with licensed VASPs that comply with Ghana’s new rules and comparable frameworks in other African jurisdictions. Platforms like BitPesa, Flutterwave, and Yellow Card operate across Kenya, Nigeria, Ghana, and other African markets with established compliance practices. These providers handle KYC verification during onboarding, and once completed, subsequent transactions move faster because the customer’s identity is already verified. Licensed VASPs carry regulatory oversight that protects your business from reputational and financial risk.

EU, UK, and US Compliance Standards Simplify Your Process

The EU, UK, and US impose stricter KYC and AML controls than Africa, but these requirements actually simplify your compliance burden rather than complicate it. The EU’s Markets in Crypto Assets Regulation, effective 2024, requires crypto service providers to implement robust customer verification, transaction monitoring, and suspicious activity reporting. The UK’s Financial Conduct Authority treats crypto service providers as money transmitters, requiring authorization and ongoing compliance with AML rules. The US Treasury’s FinCEN guidance treats stablecoin issuers and exchanges as money services businesses subject to Bank Secrecy Act reporting.

These regimes mean your EU, UK, and US customers send payments through providers already subject to stringent verification. Platforms operating in regulated markets have already completed the hard compliance work, so you inherit their compliance framework rather than building your own. When you receive stablecoins from verified EU, UK, or US customers, the transaction history is auditable and transparent, reducing your AML risk significantly.

Documentation and Transaction Records

Your responsibility is straightforward: maintain transaction records showing the source and destination of all crypto payments, reconcile these records monthly against your blockchain wallet addresses, and report suspicious activity if you observe it. Most African businesses never encounter suspicious activity because legitimate cross-border payments leave clear trails on public blockchains, unlike cash transfers that disappear into opacity. The key is documentation: keep records linking each incoming stablecoin transaction to the customer invoice, contract, or service delivery that triggered it (this audit trail proves the legitimacy of your crypto revenue and protects you if regulators ever question the source of funds).

Audit Trails and Blockchain Transparency

Public blockchains create permanent, auditable records that traditional banking cannot match. Every USDC or USDT transaction you receive includes a wallet address, timestamp, and amount that anyone can verify on the blockchain. This transparency actually reduces your compliance burden compared to traditional wire transfers, which require you to trust correspondent banks’ internal records. You can prove the legitimacy of your crypto revenue instantly by pointing to the blockchain transaction, whereas traditional banking forces you to request statements from multiple intermediaries and wait days for confirmation.

Final Thoughts

African businesses accepting crypto payments from the EU, UK, and US gain three immediate advantages: settlement in seconds instead of days, fees under 1% instead of 5% to 8%, and access to customer funds the moment they arrive. A business processing $50,000 monthly in cross-border payments saves roughly $2,000 annually in fees alone, plus gains the working capital benefit of immediate fund access. The regulatory environment now supports this shift, with Ghana’s Virtual Asset Service Providers Bill and comparable frameworks across Africa creating a legitimate ecosystem where licensed platforms protect your business and your customers.

Start with one high-volume customer or corridor, measure the speed and cost savings, then expand to additional customers as your team gains confidence. Select a licensed off-ramp provider like BitPesa, Flutterwave, or Yellow Card that operates in your country and offers competitive conversion rates. Web3 Enabler connects blockchain transactions directly to Salesforce, eliminating the operational friction that deters most African businesses from accepting Africa crypto payments.

The businesses winning in global payments today accept multiple settlement methods, and crypto payments from international customers represent the fastest, cheapest option available. Your competitors are already moving into this space. The question is whether you move now or wait until crypto payments become table stakes in your industry.

Africa Crypto Payments FAQ (EU, UK, US)

What are Africa crypto payments, and why do stablecoins matter?

Africa crypto payments usually refer to accepting blockchain-based payments from international customers, most often through stablecoins like USDC or USDT. Stablecoins are designed to track the value of the US dollar, which makes them more practical for business invoicing than volatile cryptocurrencies. For many African businesses, the benefit is faster settlement and simpler cross-border collection.

Should my business accept USDC or USDT?

Start with whichever stablecoin your customers already use and your payment partner can settle reliably. USDC is issued by Circle, and USDT is issued by Tether, both commonly used for cross-border payments. In practice, the “best” choice is the one your off-ramp supports for same-day or next-day conversion into your local currency at predictable fees.

How do EU, UK, and US customers pay an African business using stablecoins?

Most customers pay from a regulated exchange account or a wallet by sending USDC or USDT to the address you provide on an invoice or checkout page. For e-commerce, many payment providers generate a payment request that shows the exact amount, time window, and network to use. After the transaction confirms on-chain, you can treat it like a completed payment and fulfill the order.

Do I need to manage a crypto wallet myself?

Not necessarily. Many businesses use a crypto payment processor that generates wallet addresses, monitors confirmations, and provides a dashboard and receipts. This approach reduces operational risk, avoids manual wallet management, and makes reconciliation easier. If you do self-custody, you will need strong internal controls, secure key storage, and documented approval workflows.

How do I convert USDC or USDT into local currency in Africa?

You convert stablecoins through an off-ramp provider that supports your country and settlement currency. The best setup converts incoming stablecoins automatically and pays out to your bank or mobile money, so your team is not doing manual swaps and transfers. Before you integrate, confirm payout timelines, supported networks, and whether the provider is licensed or registered where required.

How do stablecoin payments compare to SWIFT transfers for settlement speed?

SWIFT transfers can be slow and fee-heavy because they often route through multiple intermediaries, even though tracking and speed have improved in recent years. Stablecoin payments can confirm in minutes or seconds depending on the network, and they settle 24/7. The main tradeoff is that you must rely on compliant on-ramp and off-ramp partners to convert and report properly.

What compliance steps matter most when accepting crypto payments in Ghana?

Work only with providers that can show licensing or registration status and can support KYC, AML monitoring, and audit-ready reporting. Ghana’s regulatory direction is toward formal registration and licensing of Virtual Asset Service Providers, which means your payment partners should be able to prove they are operating within the framework. Good documentation is essential: link each transaction to an invoice, customer, and service delivery record.

What rules affect payments coming from the EU, UK, and US?

In the EU, Markets in Crypto-Assets (MiCA) sets requirements for crypto-asset service providers and includes specific rules for stablecoins. In the UK, the FCA oversees AML registration requirements for certain cryptoasset businesses. In the US, FinCEN guidance treats many virtual-currency exchange and transmission activities as money services business activity, which drives KYC and reporting expectations for the platforms customers use.

What is the FATF “Travel Rule,” and does it affect my business?

The Travel Rule is an international standard that requires certain identifying information to travel with qualifying virtual asset transfers, typically handled by regulated exchanges and payment providers. If you use a compliant processor, much of this is automated. If you’re receiving larger B2B payments, choose partners that can support Travel Rule workflows so transactions do not get delayed or rejected.

How do I record stablecoin payments in accounting and reporting?

Track the invoice amount, the stablecoin received, the transaction hash, and the conversion rate at the time you recognize revenue. If you convert immediately to fiat, record the fiat proceeds and fees as part of the settlement. If you hold stablecoins, you still need clear policies for valuation timing, custody controls, and monthly reconciliation between your wallet balances and your ledger.

How can I integrate crypto payments with Shopify, WooCommerce, or Salesforce?

For Shopify or WooCommerce, many providers offer plugins that add stablecoin checkout and automatic confirmation. For custom sites, use APIs and webhooks for real-time payment status and automated invoicing. If your business runs on Salesforce, a native integration approach keeps payment data in the same system as customer and revenue records, reducing manual reconciliation and improving reporting accuracy.

What is the safest way to start accepting Africa crypto payments?

Start with a pilot focused on one corridor, one customer segment, or one product line. Use a licensed or reputable processor, enable automatic conversion to reduce exposure, and measure settlement time, total fees, and reconciliation effort. Once reporting and payouts are stable for 30 to 60 days, expand to more customers and additional corridors.