International payments remain broken for most businesses. Companies sending money across borders still face fees that eat into margins, settlement delays that disrupt cash flow, and barriers that exclude emerging markets entirely.

Crypto-based international transfers change this equation. At Web3 Enabler, we’ve seen firsthand how blockchain-powered payments eliminate intermediaries, cut costs dramatically, and settle in minutes instead of days.

The Real Cost of Moving Money Across Borders

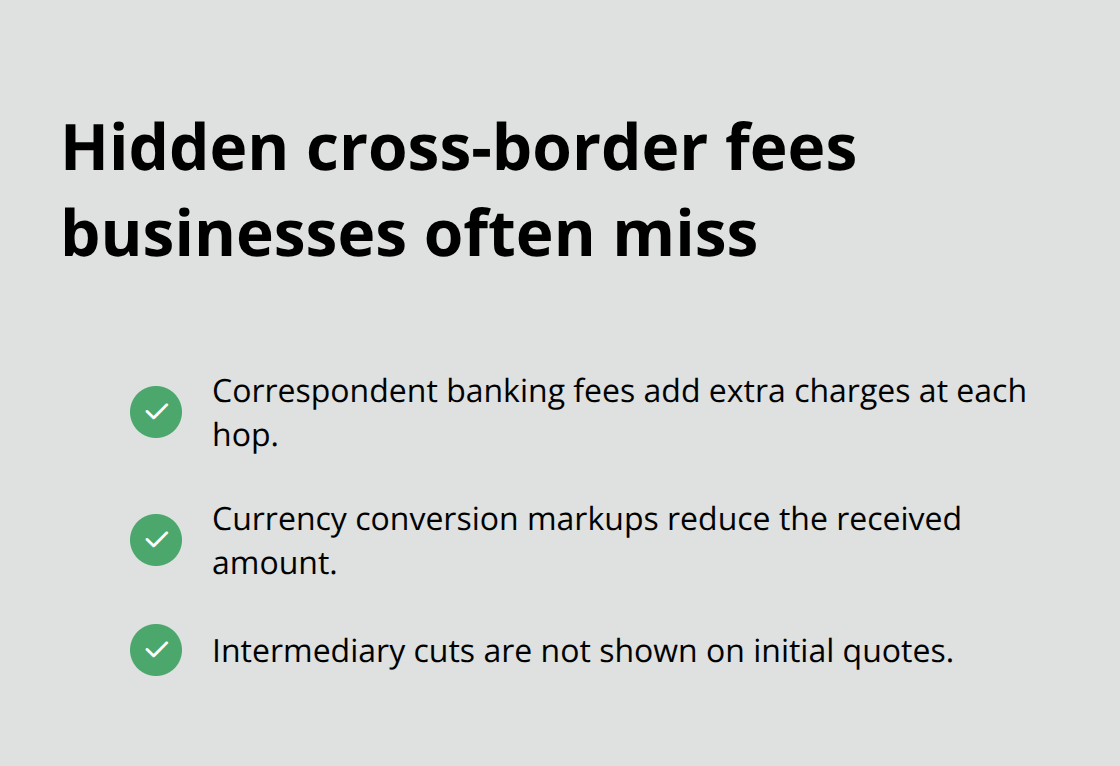

Traditional international transfers impose a financial toll that most businesses accept as inevitable. The World Bank reports that cross-border payment costs have risen significantly, with average transaction costs for €5,000 transfers increasing from 0.67 percent in 2024 to 0.78 percent in 2025. A company that pays ten contractors across five countries loses thousands monthly to transfer fees alone. These costs compound for businesses that manage payroll in multiple regions or settle supplier invoices internationally. Beyond the headline fee, hidden charges emerge at each step: correspondent banking fees, currency conversion markups, and intermediary cuts that never appear on the initial quote. A $10,000 wire to Nigeria might arrive as $9,200 after banks, currency exchanges, and local processing fees strip away nearly 8% of the value.

Most finance teams budget for this leakage as normal operating expense rather than recognizing it as a problem worth solving.

Settlement Delays Disrupt Cash Flow

Speed matters more than most finance leaders admit. Traditional correspondent banking networks require transfers to pass through multiple intermediaries, each adding processing time. A payment initiated Monday morning might not clear until Wednesday or Thursday, leaving suppliers waiting and contractors frustrated. During volatile market periods, these delays create real risk. A contractor in Kenya needs the funds to cover payroll Friday, but a wire transfer from the US won’t arrive until the following Monday. Emerging market businesses face even worse timelines-transfers to Sub-Saharan Africa typically require 3–5 business days minimum, sometimes stretching longer when weekend gaps and regional banking hours align poorly. This isn’t merely inconvenient; it forces companies to maintain larger cash reserves than necessary and complicates forecasting. Finance teams must predict demand several days in advance, holding capital idle to cover gaps. For fast-growing startups that manage dozens of international payments weekly, these delays become a genuine operational constraint that slows scaling.

Barriers Keep Emerging Markets Underserved

Access to international payment infrastructure remains unequal. Banks in developed markets offer straightforward cross-border services, while institutions in Africa and parts of the Middle East face correspondent banking relationships that are expensive, slow, or simply unavailable. Some African banks have been de-risked entirely by Western financial institutions, making it nearly impossible for legitimate businesses to move money internationally at reasonable rates. This exclusion forces regional companies to use informal channels, accept punitive exchange rates, or hold multiple currency accounts across different geographies. A Nigerian exporter that receives USD from international clients might face days of settlement uncertainty and fees just to convert and receive funds locally. Small and medium businesses in these regions compete globally but pay locally inflated costs for the privilege. This structural disadvantage persists even as digital banking expands, because the underlying infrastructure still depends on correspondent bank relationships that haven’t modernized in decades.

Why Crypto-Based Solutions Address These Gaps

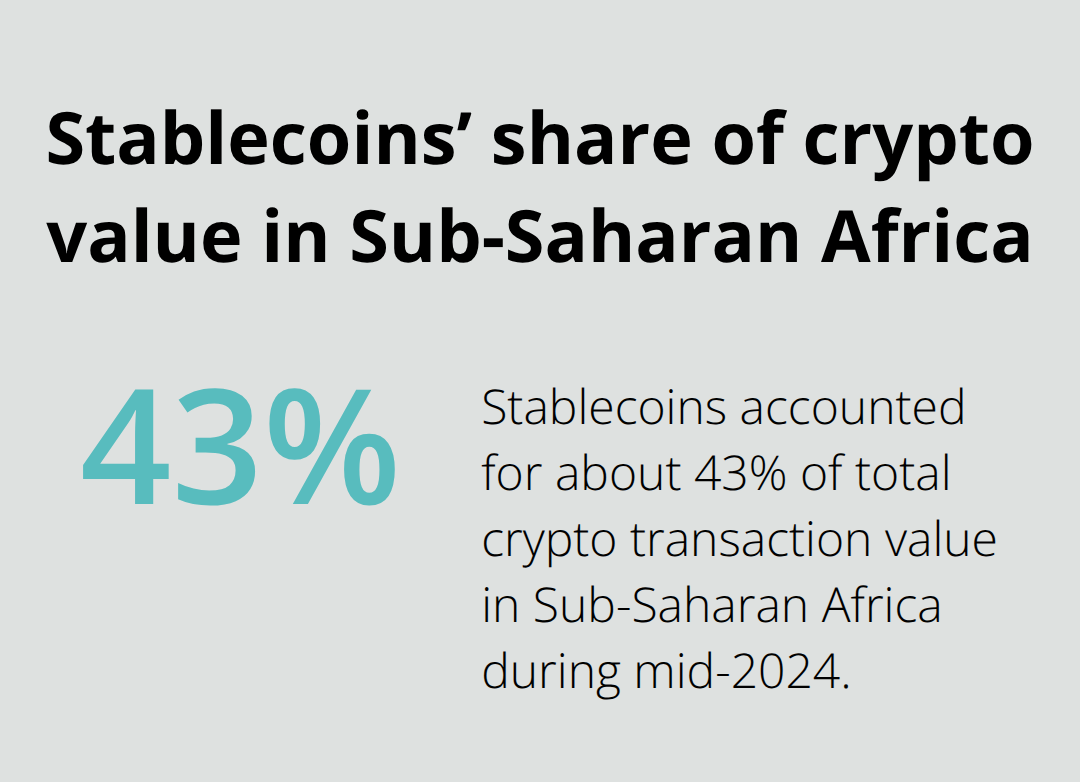

Blockchain technology eliminates the intermediaries that create delays and extract fees. Stablecoins (cryptocurrency tokens pegged to fiat currencies like the US dollar) settle transactions in minutes rather than days, and they operate across borders without the correspondent banking friction that plagues traditional systems. A payment to Nigeria or Kenya clears in the same timeframe as a domestic transfer, removing the geographic penalty that currently exists. For businesses operating across Africa and the Middle East, where stablecoin adoption has accelerated significantly, this shift transforms treasury operations. Nigeria recorded nearly $22 billion in stablecoin transactions from July 2023 to June 2024, illustrating how heavily regional businesses rely on these rails for cross-border and domestic value transfer. Sub-Saharan Africa stablecoin flows may exceed $54 billion between mid-2024 and mid-2025, with stablecoins representing about 43% of total crypto transaction value in the region. These numbers reflect real operational adoption, not speculation.

Companies that move payroll, supplier payments, and contractor settlements across these corridors now have a faster, cheaper alternative to traditional banking. The next section explores how crypto-based transfers actually work and why they deliver the speed and cost advantages that traditional systems cannot match.

How Blockchain Removes the Middlemen

Blockchain networks operate without the correspondent banks, currency exchanges, and processing centers that currently slow international payments. When you send a stablecoin across a blockchain network, the transaction moves directly from your wallet to the recipient’s wallet without intermediaries extracting fees at each step. This architectural difference is why a payment to Lagos settles at the same speed as a payment to London. Traditional systems require a payment to hop through multiple banks, each running their own settlement processes and applying their own margins. A transfer from a US company to a Nigerian supplier passes through at least three to four institutions before the recipient receives funds. Each institution adds processing time measured in hours or days, plus fees that compound. Stablecoins eliminate these hops entirely. The blockchain records the transaction once, and settlement becomes final within minutes.

Direct Settlement Transforms Cash Flow

For a company managing payroll across ten countries, the operational shift is dramatic. Payments that initiate Monday morning and clear Wednesday now settle the same day. Cash flow forecasting improves because you no longer predict demand several days in advance or hold capital idle to cover gaps. Reconciliation becomes immediate and precise. A traditional wire to Sub-Saharan Africa might clear on an uncertain timeline, forcing accounting teams to track payments across fragmented systems and time zones. Stablecoin transactions settle with blockchain finality, making reconciliation automatic. The capital freed up from reduced float requirements can be deployed elsewhere in the business. If you typically need $200,000 in float to cover the gap between payment initiation and settlement across five countries, stablecoin transfers eliminate most of that requirement.

Stablecoins Lock in Exchange Rates

Price volatility makes cryptocurrency unsuitable for most business payments, but stablecoins solve this problem by tying token value to fiat currencies. USDC maintains a one-to-one peg with the US dollar through collateralization and regular audits. A company paying a contractor in Kenya in USDC knows exactly what the payment costs in USD terms, with no exchange rate surprise between transaction initiation and settlement. This certainty matters enormously for budgeting and financial planning. Traditional wire transfers to emerging markets expose companies to hidden fees and currency conversion spreads that can shift significantly depending on market conditions and the bank’s rates. Stablecoins remove this friction entirely.

Sub-Saharan Africa stablecoin flows reached approximately 43% of total crypto transaction value in the region during mid-2024, with projections exceeding $54 billion between mid-2024 and mid-2025. These flows represent real businesses that use stablecoins specifically because they eliminate currency volatility and settlement delays. The stability also strengthens supplier relationships. A contractor receives USDC and knows the payment amount won’t fluctuate before they convert to local currency, removing negotiation friction around exchange rates.

Speed Enables New Operational Models

Minutes matter when a business operates across time zones and currencies. A contractor in Nairobi working for a US company receives payment in USDC and converts to Kenyan shillings instantly, rather than waiting 3–5 business days for a wire transfer to clear through correspondent banks. This speed transforms contractor management and payroll operations. Companies can run payroll on Friday and have funds in contractor wallets by end of business, rather than initiating transfers early in the week and hoping they arrive by month-end. For supplier payments, the speed advantage compounds. A business importing goods from Egypt settles invoices in USDC within the same business day, improving supplier cash flow and strengthening commercial relationships. Platforms like Grey demonstrate this in practice, enabling bulk payouts that settle in minutes rather than days, with support for USDC and USD corporate accounts across 170+ countries.

The speed and cost advantages of stablecoin transfers create a competitive edge for businesses that operate globally. Yet the real transformation happens when companies integrate these capabilities directly into their existing systems. The next section explores how businesses embed crypto payments into their core infrastructure, making international transfers as routine as domestic ones.

How Stablecoins Cut Costs and Accelerate Global Operations

The Financial Case for Stablecoin Payments

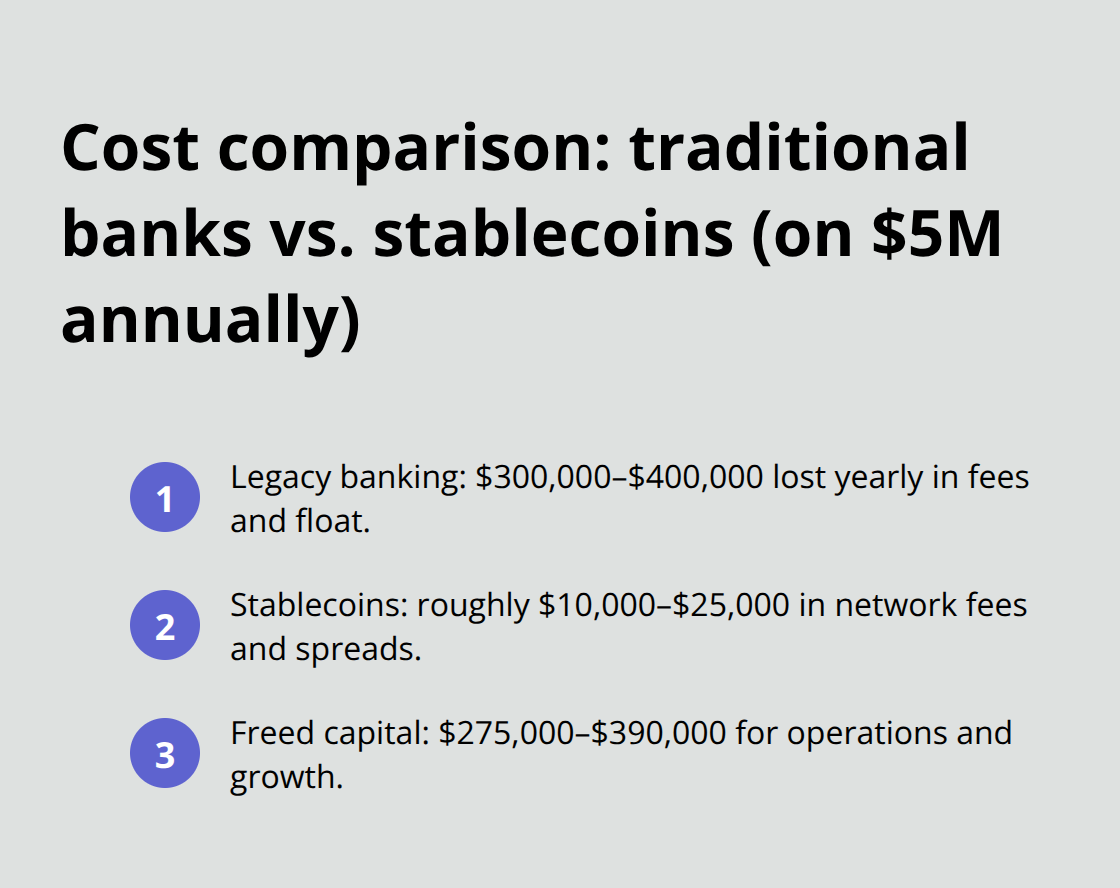

Multinationals that operate across Africa and the Middle East face a choice: continue absorbing cross-border transfer costs or shift to stablecoin-based payments that settle in minutes for a fraction of the price. The financial impact compounds quickly. A company with $5 million in annual cross-border payroll and supplier payments loses $300,000 to $400,000 yearly in fees and float costs under traditional banking. That same $5 million moved via stablecoins costs roughly $10,000–$25,000 in network fees and exchange spreads, freeing $275,000 to $390,000 for operations, growth, or margin improvement. The difference isn’t marginal; it’s transformative for mid-market businesses and material even for large enterprises managing dozens of corridors.

A multinational that pays 500 contractors across Nigeria, Kenya, Egypt, and the UAE sees immediate relief when payroll shifts to USDC. Contractors receive payment in minutes instead of waiting for wire transfers to clear across correspondent banking networks. The operational simplification alone justifies the shift; the cost savings make it obvious.

How Speed Transforms Cash Flow and Forecasting

Faster settlement transforms how finance teams operate. Cash flow forecasting becomes precise because you no longer hold excess float to cover settlement gaps. Accounting teams stop chasing payments across fragmented systems and time zones. Reconciliation happens automatically when blockchain transactions settle with finality. If you typically need $200,000 in float to cover the gap between payment initiation and settlement across five countries, stablecoin transfers eliminate most of that requirement.

The capital freed from reduced float requirements can be deployed elsewhere in the business. A company that previously initiated payments early in the week hoping they’d clear by Friday now settles on the same business day, reducing inventory holding periods and improving days payable outstanding management.

Supplier Relationships and Working Capital Efficiency

Faster settlement transforms supplier relationships and unlocks working capital efficiency that traditional systems cannot match. When a business in South Africa imports raw materials from Egypt and settles invoices in USDC within hours, supplier cash flow improves dramatically, strengthening commercial terms and negotiating power. For businesses managing contractor networks across Sub-Saharan Africa, this shift from days to minutes changes how operations function.

A US software company that pays developers in Lagos no longer schedules payroll three days early to account for settlement delays. A retailer importing goods from Nairobi settles invoices without currency conversion friction or hidden intermediary fees. These operational gains accumulate across every payment function: payroll runs faster, supplier terms improve, cash forecasting becomes accurate, and finance teams redirect energy from payment logistics to strategic work.

Integration with Existing Business Systems

The speed advantage compounds when integrated into existing systems like Salesforce, enabling teams to manage cryptocurrency payments alongside traditional transactions without context switching or parallel processes. Web3 Enabler provides a seamless interface between Salesforce and the blockchain, offering native Salesforce support for cryptocurrencies and digital assets. This integration connects blockchain transactions directly to your existing corporate infrastructure, making crypto accessible for your business without requiring separate tools or workflows. Finance teams can manage digital assets, track investment returns, and handle international contractor payments all within their Salesforce environment, streamlining operations and reducing the complexity that typically accompanies crypto adoption.

FAQ: Crypto-Based International Transfers

Why are international transfer fees rising in 2026?

According to World Bank data, the average cost of international transfers increased in 2025 due to rising compliance costs and a reduction in correspondent banking relationships. Traditional wires for corridors like Sub-Saharan Africa now average nearly 8% in total costs when including FX markups and intermediary fees. Crypto-based transfers bypass these banks entirely, allowing businesses to avoid the “middleman tax” that traditional institutions impose.

How does stablecoin settlement speed improve my cash flow?

Traditional international wires often take 3 to 5 business days to clear, forcing businesses to maintain larger cash reserves (float) to cover the gap. Stablecoins settle with “blockchain finality” in minutes. By integrating this into Salesforce, your finance team can reduce float requirements by up to 90%, freeing up hundreds of thousands of dollars that would otherwise be sitting idle in the banking system.

Is it legal to pay international contractors in USDC?

Yes. Following the passage of the GENIUS Act in July 2025, the U.S. established a clear federal framework for “Permitted Payment Stablecoin Issuers.” This law confirms that regulated stablecoins like USDC are not securities or commodities, but legitimate payment tools. This gives U.S. businesses the legal green light to use stablecoins for global payroll and supplier settlements with full regulatory clarity.

How do I handle exchange rate volatility with crypto transfers?

By using stablecoins like USDC, you eliminate the volatility typically associated with assets like Bitcoin. USDC maintains a 1:1 peg to the US Dollar and is backed by audited reserves. When you send a payment from Salesforce, the recipient receives exactly the value sent, without the “exchange rate surprise” or hidden spreads that banks often slip into traditional wire transfers.

Can I manage these transfers directly within my Salesforce instance?

Absolutely. Web3 Enabler provides native Salesforce support, allowing you to trigger international payments directly from your CRM. You don’t need to switch between banking portals or manage separate crypto wallets. The integration connects blockchain transactions to your existing vendor and contractor records, making international crypto transfers as routine as domestic ones.

Final Thoughts

Crypto-based international transfers solve the payment problems that have plagued global business for decades. Traditional systems impose hidden costs, force companies to hold excess capital idle, and exclude entire regions from efficient financial infrastructure. Stablecoins eliminate these constraints by settling transactions in minutes, cutting costs by 90% or more, and operating across borders without correspondent banking friction.

The competitive advantage is immediate and measurable. A company managing payroll across Nigeria, Kenya, and Egypt frees up hundreds of thousands of dollars annually while improving contractor satisfaction through faster settlement. Supplier relationships strengthen when invoices settle in hours instead of days, and finance teams redirect energy from payment logistics to strategic work when reconciliation becomes automatic.

Web3 Enabler provides native Salesforce support for cryptocurrencies and digital assets, connecting blockchain transactions directly to your corporate infrastructure without requiring parallel tools or workflows. Businesses across Africa and the Middle East have already moved billions through stablecoin rails, proving the model works in practice.