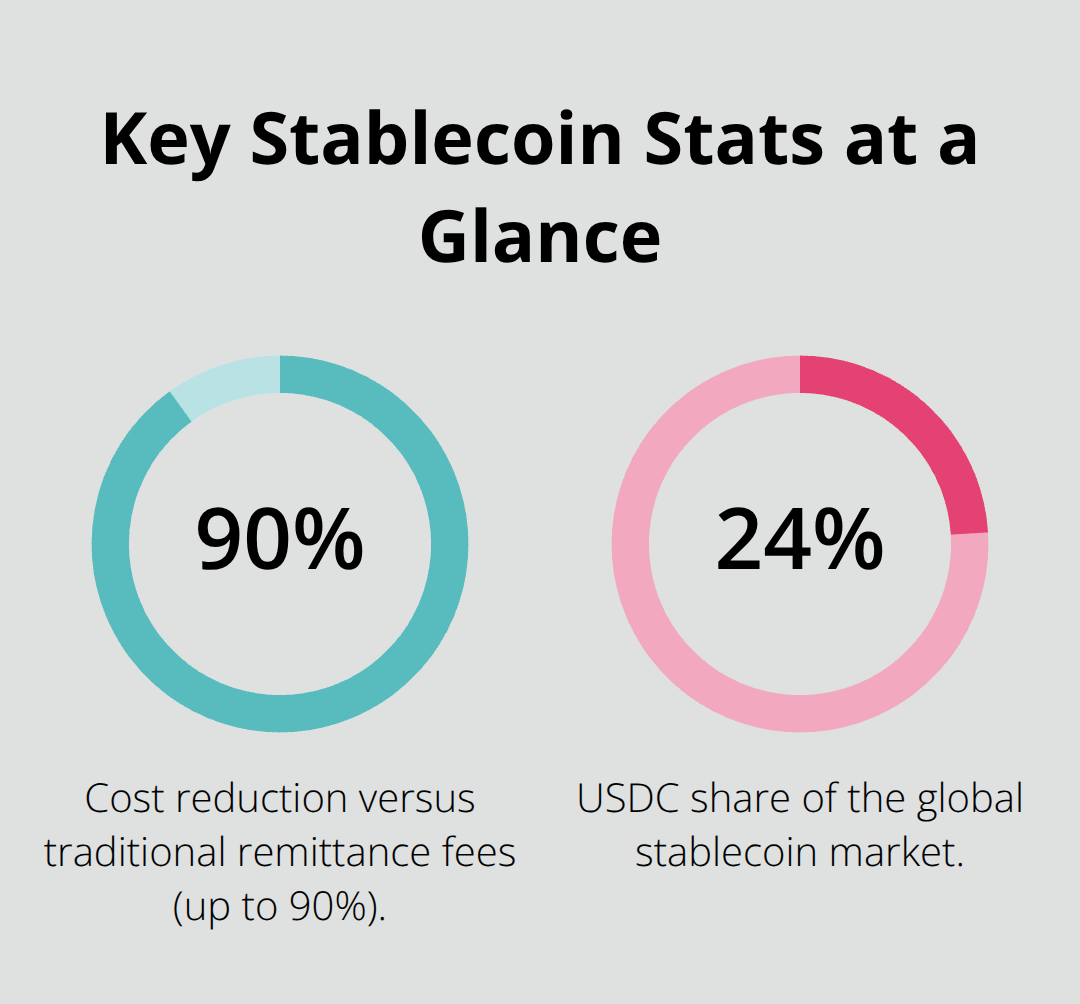

African and MENA businesses lose millions annually to traditional remittance fees and slow settlement times. Stablecoin remittances offer a direct alternative that cuts costs by up to 90% and settles in minutes instead of days.

We at Web3 Enabler have seen firsthand how blockchain infrastructure is reshaping cross-border payments in these regions. This guide walks you through the mechanics, compliance requirements, real ROI numbers, and practical steps to implement stablecoin remittances.

How Stablecoin Remittances Actually Work

A traditional remittance from Lagos to Nairobi takes three to five business days and costs the sender 6 to 8 percent of the transfer amount, according to the World Bank. A stablecoin remittance on the same corridor completes in roughly 60 seconds and costs 1.5 to 2.5 percent all-in, including liquidity and compliance fees. The difference comes down to infrastructure. Traditional rails move money through multiple intermediaries-correspondent banks, clearinghouses, and money transfer operators-each taking a cut and adding delays. Stablecoins move value directly on a blockchain, peer-to-peer, with no middlemen. A sender in Lagos converts Nigerian naira to USDC, the stablecoin settles on-chain in seconds, and a recipient in Nairobi receives it as Kenyan shillings through a local mobile money operator or exchange. The entire flow remains transparent, immutable, and final. No reversals, no chargebacks, no mystery delays buried in banking queues.

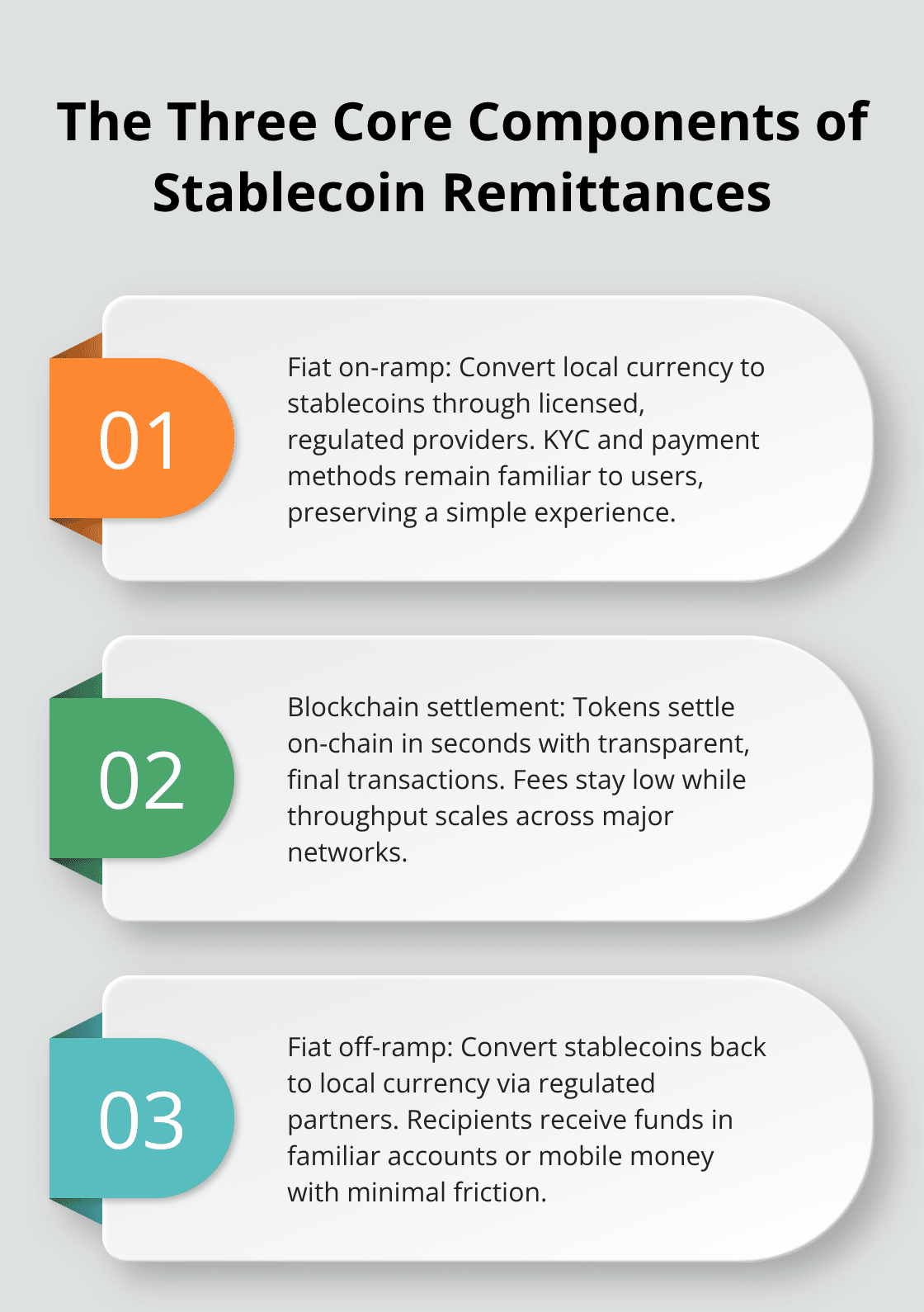

Three core components power stablecoin remittances

Stablecoin remittances require a fiat on-ramp where senders convert local currency to stablecoins, a blockchain network where the token settles, and a fiat off-ramp where recipients convert back to local currency. USDC accounts for roughly 24 percent of the global stablecoin market and serves as the most practical choice for remittances because networks like Ethereum, Tron, and Polygon all support it. Transaction fees on Tron or Polygon cost fractions of a cent, whereas Ethereum gas fees run a few dollars but remain trivial compared to traditional remittance costs. The real complexity sits in liquidity management and compliance automation. Mobile Money Operators across Africa and MENA have already integrated licensed stablecoin rails into their existing platforms, eliminating the need for customers to hold crypto wallets. A user simply sends money through their familiar app, and the operator handles the on-chain conversion behind the scenes.

Early adopters captured massive volume growth

Early movers in 2025 saw 200 to 300 percent year-over-year growth in cross-border transaction volume after launching stablecoin corridors, proving that speed and cost alone drive adoption when the user experience remains familiar. For a business sending $100,000 monthly to Africa or MENA, this shift from traditional wires to stablecoin rails adds $3 to $5 million in annual gross profit without acquiring a single new customer. This ROI emerges directly from fee compression and settlement speed.

Minutes of settlement unlock working capital advantages

Settlement finality in minutes instead of days transforms cash flow management. A small enterprise in Cairo paying suppliers in Istanbul no longer waits five days for funds to arrive. Money lands in the supplier’s account in less than two minutes, improving inventory turnover and reducing the need for bridge financing. The December 2025 remittance data from Dhaka Tribune showed $3.277 billion in transfers, a 22.3 percent year-over-year increase, signaling sustained demand for faster cross-border payments. Stablecoin infrastructure captures this demand by eliminating the settlement lag entirely. For businesses processing $50,000 monthly in supplier payments, the difference between five-day and two-minute settlement frees up cash that would otherwise sit idle in nostro accounts.

Speed-to-market creates lasting competitive advantage

Traditional cross-border corridors take 24 to 36 months to establish; stablecoin infrastructure enables new corridors in 6 to 12 weeks. This speed-to-market advantage is not theoretical-it is a competitive moat. Operators who deploy stablecoin rails first capture disproportionate market share while competitors are still waiting for regulatory clarity. The infrastructure exists today. The question for businesses and payment operators is whether they move now or watch market share consolidate among early movers. Understanding the compliance requirements that underpin these corridors determines whether implementation succeeds or stalls.

Real-World ROI and Business Impact

A business in Lagos sends $100,000 monthly to suppliers across Africa and MENA via traditional wire transfers and pays $6,000 to $8,000 in fees annually. The same volume through stablecoin rails costs $1,500 to $2,500 all-in, delivering $4,500 to $6,500 in annual savings without changing supplier relationships or payment frequency. For mid-market enterprises processing $500,000 monthly, this gap widens to $45,000 to $65,000 saved per year. Mobile Money Operators who launched stablecoin corridors in early 2025 reported 200 to 300 percent year-over-year growth in cross-border volumes, proving that businesses actively seek faster, cheaper alternatives the moment they become available.

Cost advantages compound across currency conversion

The cost advantage compounds when you factor in currency conversion spreads. Traditional corridors charge 3 to 5 percent on top of base fees for unfavorable exchange rates; stablecoin platforms reduce this to 0.5 to 1 percent through liquid on-chain markets. A $50,000 supplier payment from Cairo to Istanbul saves roughly $1,000 to $2,000 on FX alone, not counting reduced wire fees. These are not theoretical savings. African and MENA operators now report ARPU from cross-border activity rising 40 to 60 percent in 2025 while transaction costs dropped about 70 percent after integrating stablecoin rails, directly translating to higher margins per transaction.

Settlement speed transforms working capital cycles

Traditional bank transfers lock funds in transit for three to five business days; stablecoin settlements finalize in 60 seconds. A small business in Amman pays monthly invoices to 15 suppliers across the region and no longer waits for payments to clear before processing the next cycle. This eliminates the need for bridge financing or excess cash reserves tied up in nostro accounts. For a company with $50,000 in monthly outflows, the difference between five-day and two-minute settlement frees approximately $8,000 to $10,000 in working capital that can be reinvested immediately.

Remittances in December 2025 amounted to $3.277 billion, a 22.3 percent year-over-year increase, indicating sustained growth in cross-border payment demand. Businesses capturing this demand through stablecoin infrastructure gain a structural advantage over competitors still reliant on traditional rails.

Speed benefits extend to payroll and batch operations

The speed benefit extends to payroll operations. A company with 50 contractors across Nigeria, Kenya, and Ghana pays all of them in a single batch that settles in minutes rather than submitting 50 separate wire requests that clear over five business days. This reduces administrative overhead and contractor frustration while improving cash flow predictability. B2B cross-border payments globally total approximately $31 trillion annually, with emerging markets capturing a growing share. Even capturing 0.1 percent of B2B flow in emerging markets through faster settlement cycles yields millions in incremental revenue for payment operators and millions in cost savings for businesses making those payments.

The financial case for stablecoin remittances is clear, but implementation requires navigating a complex compliance landscape that varies significantly across Africa and MENA jurisdictions.

Building Trust Through Compliance

Stablecoin remittances succeed only when regulatory confidence is earned, not assumed. The GENIUS Act establishes hard requirements for reserve backing, ongoing audits, and AML controls that ripple across international remittance corridors. Any platform serving US users-even from offshore locations-must comply with these standards. This means one-to-one reserves backed by cash or short-term US Treasuries, segregated from operating funds, with third-party audits validating reserve sufficiency before each major settlement batch. For remittance operators in Africa and MENA, this is non-negotiable. A business in Lagos routing payments through a compliant platform gains banking relationships that would otherwise take years to establish. Non-compliant platforms face derisking by correspondent banks, liquidity freezes, and regulatory enforcement that destroys operations overnight.

Compliance Automation Reduces Friction and Risk

The upfront cost of compliance automation-KYC verification, real-time AML screening, sanctions watchlist checks, and audit-ready transaction logs-appears steep until you factor in the alternative: losing access to dollar liquidity entirely. Platform providers now offer integrated compliance workflows that handle government ID verification, corporate beneficial owner checks, and continuous transaction monitoring across 80+ jurisdictions. This automation reduces onboarding time from weeks to hours while maintaining regulatory alignment, a critical advantage when speed-to-market determines competitive position.

Individual and Business Onboarding Flows

Individual senders and businesses navigate a straightforward but mandatory onboarding sequence. A person in Accra sending $500 to family in Cairo starts with government ID verification, phone number confirmation, and a source-of-funds declaration. A business making $50,000 monthly supplier payments completes corporate verification, beneficial owner identification, and transaction-monitoring enrollment. Neither process requires crypto expertise or a blockchain wallet. Mobile Money Operators handle on-chain conversions behind the scenes; senders and recipients interact only with familiar interfaces.

Liquidity and Off-Ramp Challenges

The real friction point emerges at the off-ramp: converting stablecoins back to local currency. Liquidity depth varies sharply across corridors. Nigeria-Kenya corridors now support deep liquidity pools from multiple exchanges, enabling $100,000+ conversions with minimal slippage. Smaller corridors like Somalia-UAE may require manual liquidity routing through licensed custodians, adding 2-4 hours to settlement. Platform operators who pre-position stablecoin reserves in high-volume off-ramp locations reduce this friction significantly. For a business sending regular payments, whitelisting recipient wallet addresses before the first transfer eliminates address-verification delays on subsequent transactions.

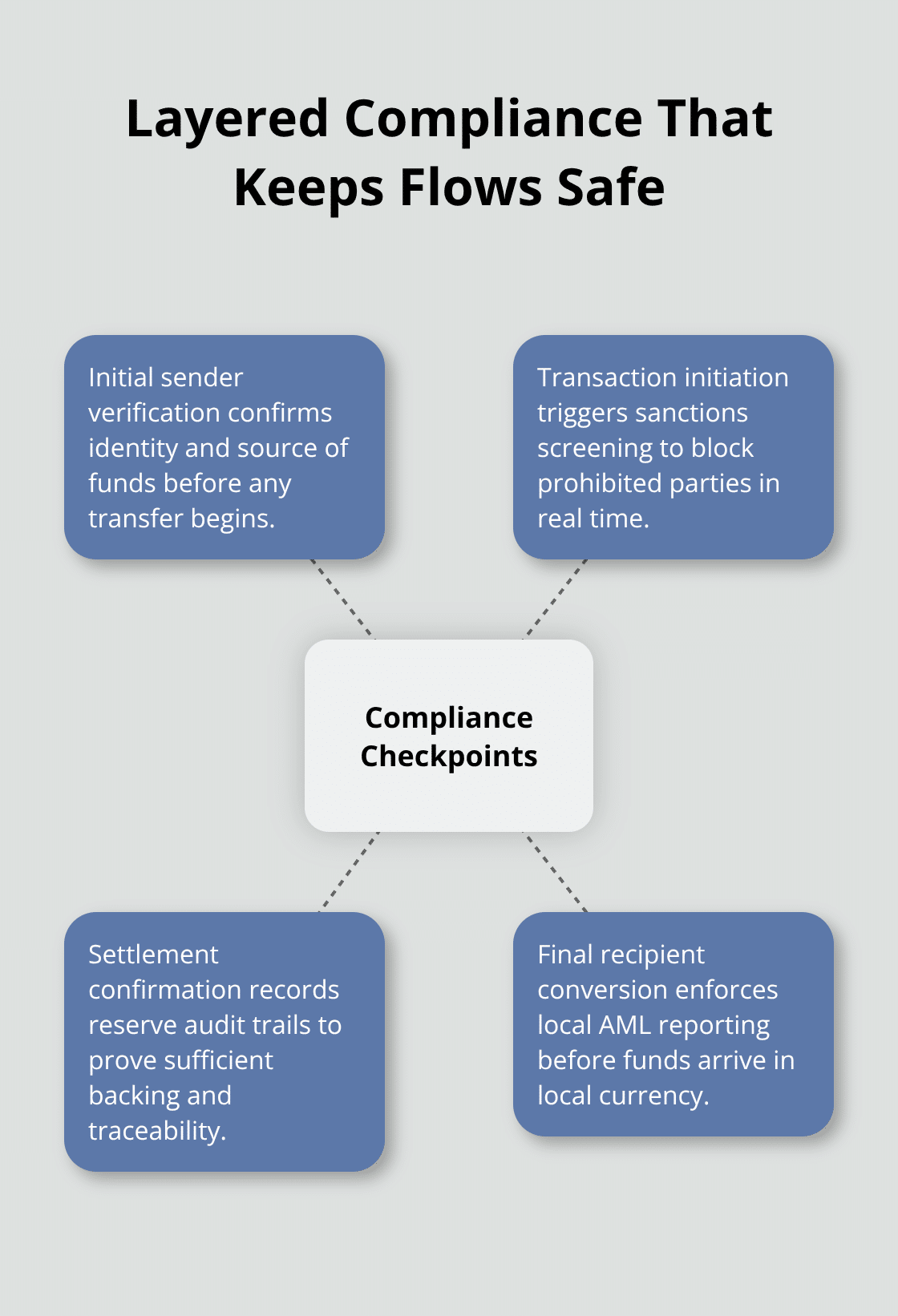

Layered Compliance Checkpoints Prevent Abuse

Compliance checkpoints occur at four critical moments: initial sender verification, transaction initiation with sanctions screening, settlement confirmation with reserve audit trails, and final recipient conversion with local AML reporting. Each checkpoint triggers automated monitoring; suspicious patterns flag for manual review within minutes.

This layered approach prevents illicit actors from exploiting remittance corridors while keeping legitimate flows moving at near-instant speeds. Operators who automate these checkpoints rather than handling them manually scale efficiently; those who delay compliance face the opposite problem-growing volumes trigger compliance debt that eventually collapses operations.

Final Thoughts

Stablecoin remittances have moved from experimental to operational across Africa and MENA, with early adopters in 2025 capturing 200 to 300 percent year-over-year growth in cross-border volumes. A business sending $100,000 monthly now saves $3,000 to $6,500 annually through stablecoin rails instead of wire transfers, while settlement happens in 60 seconds rather than five days. The December 2025 remittance surge to $3.277 billion, up 22.3 percent year-over-year, confirms sustained demand for faster cross-border payments that stablecoin platforms satisfy through direct peer-to-peer transfers.

Mobile Money Operators across Africa and MENA have shifted from viewing stablecoins as a threat to treating them as a revenue engine, integrating licensed stablecoin rails to serve customers who demand speed and transparency. The global stablecoin market reached $251.7 billion in mid-2025, with monthly transaction volumes projected to reach $6 trillion by 2028, and B2B cross-border payments alone total $31 trillion annually. Even capturing 0.1 percent of emerging market flow through stablecoin infrastructure yields millions in incremental revenue for operators and millions in cost savings for businesses making those payments.

The question is no longer whether stablecoin remittances work-they do. The question is whether your business moves now or waits while competitors solidify their lead. Contact Web3 Enabler to explore how stablecoin remittances fit your cross-border payment strategy and integrate blockchain infrastructure directly into your existing systems.

Stablecoin Remittances FAQs

What are stablecoin remittances?

Stablecoin remittances are cross-border transfers that use price-stable digital currencies like USDC or USDT (typically pegged 1:1 to the U.S. dollar) to move value faster and often cheaper than traditional remittance rails. They are commonly used to send money to Africa and MENA where banking delays and FX spreads can be significant.

How do stablecoin remittances work from sender to recipient?

Most flows have three steps: the sender converts local currency to a stablecoin through an on-ramp, the stablecoin is transferred on a blockchain network, and the recipient converts it back to local currency through an off-ramp. Many operators hide the blockchain step inside a familiar app experience, so customers may never need to manage crypto directly.

How fast are stablecoin remittances compared to traditional remittances?

On-chain settlement can occur in seconds to minutes, and stablecoins can move 24/7. The total “door-to-door” time depends on the off-ramp, local liquidity, banking hours, and compliance checks, but it is often much faster than multi-day bank wires or slower remittance corridors.

How much do stablecoin remittances cost?

Network fees can be very low on certain chains, but total cost also includes on-ramp/off-ramp fees, FX conversion, liquidity spread, and compliance. For a fair comparison, evaluate “all-in” cost per transfer, not just blockchain fees, especially for Africa and MENA corridors where cash-out pricing and liquidity vary by country.

Why are remittance costs to Africa and MENA often higher on traditional rails?

Traditional remittances can include layered fees from intermediaries plus FX spreads. Costs are often higher for certain Africa corridors due to liquidity constraints, correspondent banking complexity, and fragmented payout networks. Stablecoins can reduce reliance on multiple intermediaries when the on-ramp and off-ramp are strong.

Which stablecoin is better for remittances, USDC or USDT?

USDC and USDT are the most widely used for cross-border payments because of their liquidity and broad exchange support. The better option is usually the one your on-ramp/off-ramp supports best in your target corridor, with the deepest local liquidity, the cleanest compliance workflow, and predictable settlement to bank or mobile money.

Do customers need a crypto wallet to send or receive stablecoin remittances?

Not always. Many remittance and mobile money providers abstract away wallets so customers interact with a normal app and receive local currency. Wallets may be used behind the scenes by the provider or by businesses that want direct on-chain settlement and transparent transaction records.

How do recipients cash out stablecoins to mobile money or bank accounts?

Recipients typically cash out through an off-ramp provider or payout partner that converts stablecoins into local currency and delivers funds to mobile money, a bank account, or cash pickup. The practical success of stablecoin remittances depends heavily on off-ramp liquidity and payout coverage in the recipient’s country.

Are stablecoin remittances compliant with regulations and AML requirements?

They can be, but compliance is not optional. Remittance operators and crypto service providers typically apply KYC, sanctions screening, and transaction monitoring, and some corridors must meet “Travel Rule” information-sharing requirements. Businesses should work with regulated partners and keep invoice-level documentation tied to each transfer.

What are the biggest risks with stablecoin remittances?

The main risks include off-ramp liquidity constraints, partner compliance gaps, fraud attempts, sanctions exposure, and operational reconciliation issues if transactions are not properly recorded. A strong implementation focuses on regulated partners, clear audit trails, automated reconciliation, and defined exception handling for delayed or flagged transfers.

How can a business start using stablecoin remittances to Africa and MENA?

Start with one corridor and one use case, such as supplier payments or contractor payroll. Choose regulated on-ramp/off-ramp partners with proven payout coverage, run a pilot with real transactions, measure all-in cost and settlement time, and then scale to additional corridors once the compliance and reconciliation workflow is stable.