Stablecoins regulation is reshaping how businesses handle digital payments. New rules from the US, EU, and Asia-Pacific are forcing companies to rethink their crypto strategies.

Stablecoins regulation is reshaping how businesses handle digital payments. New rules from the US, EU, and Asia-Pacific are forcing companies to rethink their crypto strategies.

We at Web3 Enabler see businesses scrambling to understand compliance requirements. The regulatory maze affects everything from treasury management to payment processing partnerships.

Where Do Regulators Stand on Stablecoins

The United States Embraces Bank-Issued Stablecoins

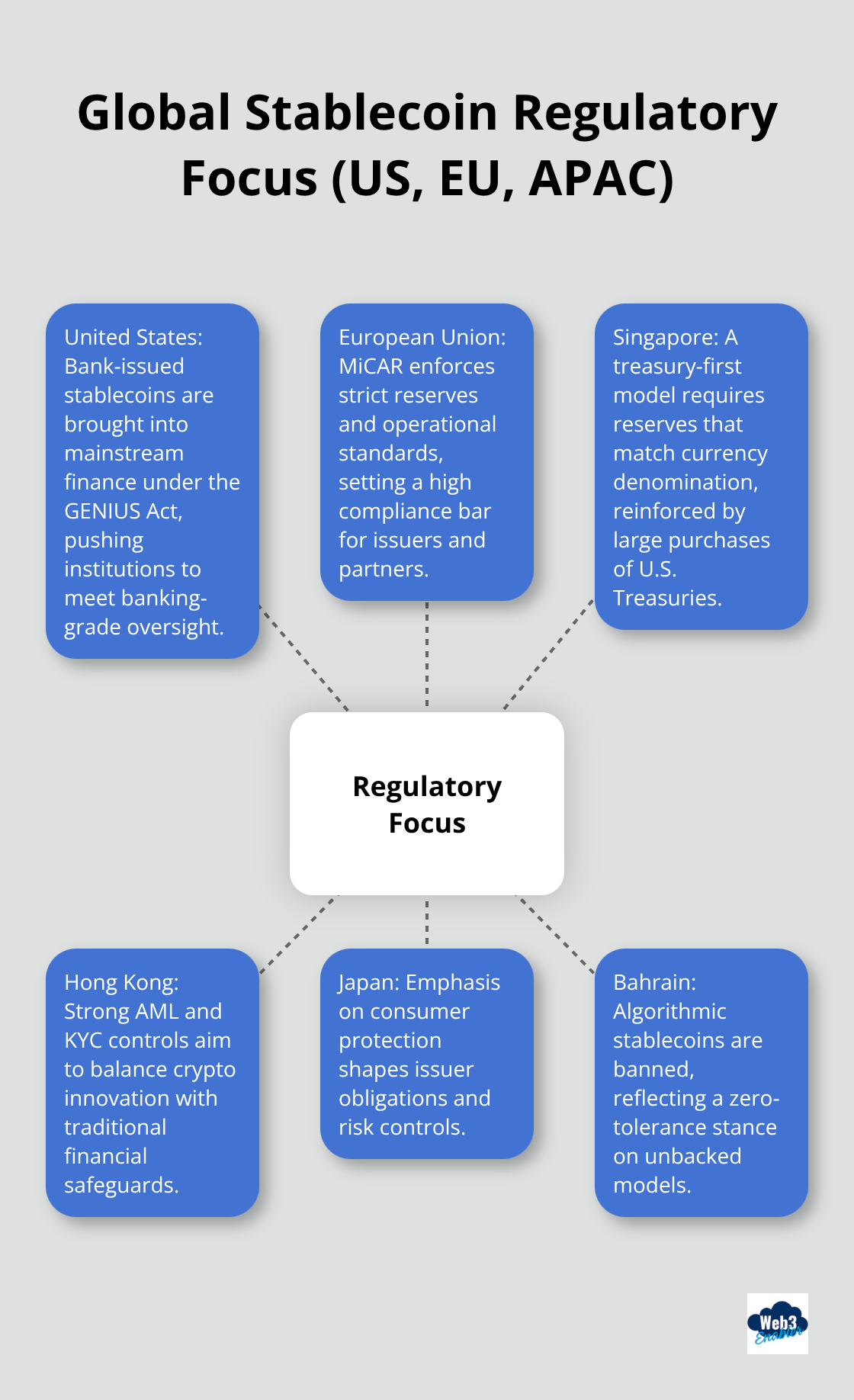

The United States leads with the GENIUS Act, which addresses vulnerabilities in the largely unregulated stablecoin market through bipartisan congressional action. This legislation shifts stablecoins from regulatory gray areas into mainstream finance, with institutions like Bank of America and Goldman Sachs now exploring G7 currency-pegged tokens.

The Federal Reserve warns that widespread adoption could drain $6.6 trillion from commercial bank deposits. This massive shift makes compliance frameworks absolutely essential for businesses that plan stablecoin integration into their operations.

Europe Sets the Compliance Bar High

The European Union implemented MiCAR regulations on June 30, 2024, which create strict reserve requirements and operational standards for stablecoin issuers. Nine major European banks formed a consortium to launch a euro-denominated stablecoin by 2026, with Citigroup joining to enhance blockchain capabilities.

MiCAR requires multi-country protocols that many view as overly complex. Businesses that operate in Europe must navigate these requirements regardless of complexity concerns (and trust us, the paperwork is real).

Singapore Takes a Treasury-First Approach

Singapore mandates stablecoin issuers maintain reserve portfolios that match their currency denomination. The Monetary Authority of Singapore purchased $40 billion in US Treasury bills last year, which demonstrates serious regulatory commitment to proper backing standards.

This approach creates clear guidelines for businesses but requires substantial capital reserves from issuers who want to operate in the region.

Hong Kong Focuses on Anti-Money Laundering

Hong Kong’s Stablecoins Bill enforces strict anti-money laundering practices and know-your-customer protocols. The territory positions itself as a crypto-friendly jurisdiction while maintaining traditional financial oversight standards.

Companies that expand into Hong Kong markets need robust compliance systems that can handle both crypto innovation and traditional banking requirements.

Japan and Regional Variations Create Complex Landscapes

Japan focuses on consumer protection measures, while Bahrain outright banned algorithmic stablecoins due to inherent risks (remember the TerraUSD collapse that wiped out $45 billion?). These jurisdiction-specific approaches mean companies need tailored compliance strategies rather than one-size-fits-all solutions.

The regulatory patchwork across Asia-Pacific creates both opportunities and challenges that directly impact how businesses structure their compliance requirements.

What Compliance Steps Must Your Business Take

Businesses that enter the stablecoin space face three non-negotiable compliance pillars that regulators enforce with strict oversight. Reserve transparency requirements now demand monthly attestations from certified auditors, with stablecoin issuers like Circle publishing detailed breakdowns of their USDC reserves across Treasury bills and cash equivalents.

Companies that partner with stablecoin providers must verify these audit trails and maintain documentation that proves compliance with local banking regulations. The Commodity Futures Trading Commission previously fined Tether for misleading statements about reserve backing, which shows regulators will penalize incomplete transparency.

Reserve Documentation Standards Get Stricter

Financial institutions must implement real-time monitoring systems that track reserve ratios and collateral quality for any stablecoin partnerships. Stablecoin issuers have significantly increased their holdings in US Treasury bills, but businesses need verification that their chosen providers maintain proper backing ratios.

Singapore requires reserve portfolios that match currency denominations exactly, while MiCAR mandates segregated accounts that protect customer funds during issuer insolvency. Companies should establish monthly review processes that validate partner compliance and create contingency plans for potential de-pegging events (like the temporary USDC crisis during March 2023’s banking turmoil).

Licensing Requirements Vary But Documentation Stays Constant

Registration obligations differ dramatically between jurisdictions, but all require extensive documentation of business operations, risk management procedures, and technical infrastructure. Hong Kong demands comprehensive anti-money laundering protocols that include transaction monitoring systems capable of flagging suspicious patterns in real-time.

The Financial Action Task Force guidelines require businesses to implement know-your-customer verification that goes beyond traditional banking standards, including source-of-funds documentation for large transactions. Companies must designate compliance officers who understand both traditional finance regulations and blockchain-specific requirements.

Staff Training Becomes Mission-Critical

Organizations need staff who can navigate reporting obligations that trigger regulatory scrutiny if mishandled. Training programs must cover both traditional finance regulations and blockchain-specific requirements, with particular focus on transaction monitoring and suspicious activity reporting (which differs significantly from standard banking protocols).

These compliance foundations directly impact how businesses structure their payment processing systems and choose their stablecoin integration partners.

How Do New Regulations Change Your Business Operations

Payment processors now demand enhanced due diligence that extends standard onboarding procedures by 3-5 business days. Companies that use stablecoins for treasury management must implement daily reconciliation processes that verify reserve backing and maintain audit trails for regulatory inspections. Visa and Stripe integrated stablecoin settlements that convert crypto payments instantly to fiat currencies, but businesses need compliance officers who understand both traditional banking regulations and blockchain-specific requirements.

Treasury Management Demands Real-Time Monitoring Systems

Treasury departments face new operational burdens that include monthly attestation reviews and segregated account management for stablecoin reserves. Standard Chartered warns that the rapid adoption of stablecoins could drain up to $1 trillion in deposits away from emerging market banks, which forces companies to restructure their international cash management strategies.

Organizations must designate compliance officers who can navigate reporting obligations and implement transaction monitoring systems that flag suspicious patterns in real-time. These systems go beyond traditional banking protocols and require specialized training for finance teams.

Partnership Availability Shrinks as Compliance Costs Rise

Stablecoin issuers increasingly limit partnerships to businesses that meet strict operational standards, with many providers requiring minimum transaction volumes of $100,000 monthly. Companies that operate across multiple jurisdictions need tailored compliance strategies rather than one-size-fits-all solutions (Bahrain banned algorithmic stablecoins while Singapore requires exact currency-matched reserve portfolios).

Risk Management Strategies Must Include Contingency Plans

Businesses must establish backup payment rails that can activate within 24 hours of compliance issues. Risk management strategies must include contingency plans for potential de-pegging events and partner insolvency scenarios, similar to the temporary USDC crisis during March 2023’s banking turmoil.

Companies should maintain relationships with multiple stablecoin providers to avoid single points of failure. This diversification approach helps businesses maintain operations when regulatory changes affect specific providers or jurisdictions.

Final Thoughts

Stablecoins regulation accelerates faster than most businesses expect. The GENIUS Act transforms US markets while MiCAR creates European compliance standards that demand immediate attention. Singapore’s treasury-focused approach and Hong Kong’s anti-money laundering requirements show regulators worldwide take oversight seriously.

Companies that delay compliance preparation face operational disruptions and partnership limitations. The regulatory patchwork across jurisdictions means businesses need specialized expertise to navigate requirements that change monthly. Treasury departments must implement real-time monitoring systems while finance teams require training on blockchain-specific protocols (and trust us, the learning curve is steep).

Smart businesses build compliance frameworks now rather than scramble later. The companies that succeed will treat regulatory compliance as a competitive advantage, not a burden. We at Web3 Enabler help businesses integrate stablecoin payments while maintaining full regulatory compliance through our Salesforce Native blockchain solutions. The stablecoin market will reach $2 trillion by 2028, but only compliant businesses will capture that growth opportunity.