Stablecoin payments are moving into the mainstream, but regulators are watching closely. The rules keep shifting, and getting them wrong can tank your business faster than you’d expect.

At Web3 Enabler, we’ve seen companies stumble because they treated compliance as an afterthought. The good news? Stablecoin payments compliance isn’t complicated when you know what you’re doing.

Why Compliance Actually Matters Right Now

The regulatory environment around stablecoins isn’t just evolving-it’s crystallizing into concrete rules that will make or break your ability to operate. In the US, the GENIUS Act pushes federal clarity on Know Your Customer and Anti-Money Laundering requirements for stablecoin platforms, while the EU’s MiCA framework has already locked in mandatory licensing and transaction monitoring for issuers. Hong Kong, Japan, and the UAE have all established operational standards that demand AML/CFT compliance and sanctions screening. If you’re thinking compliance is optional, you’re already behind.

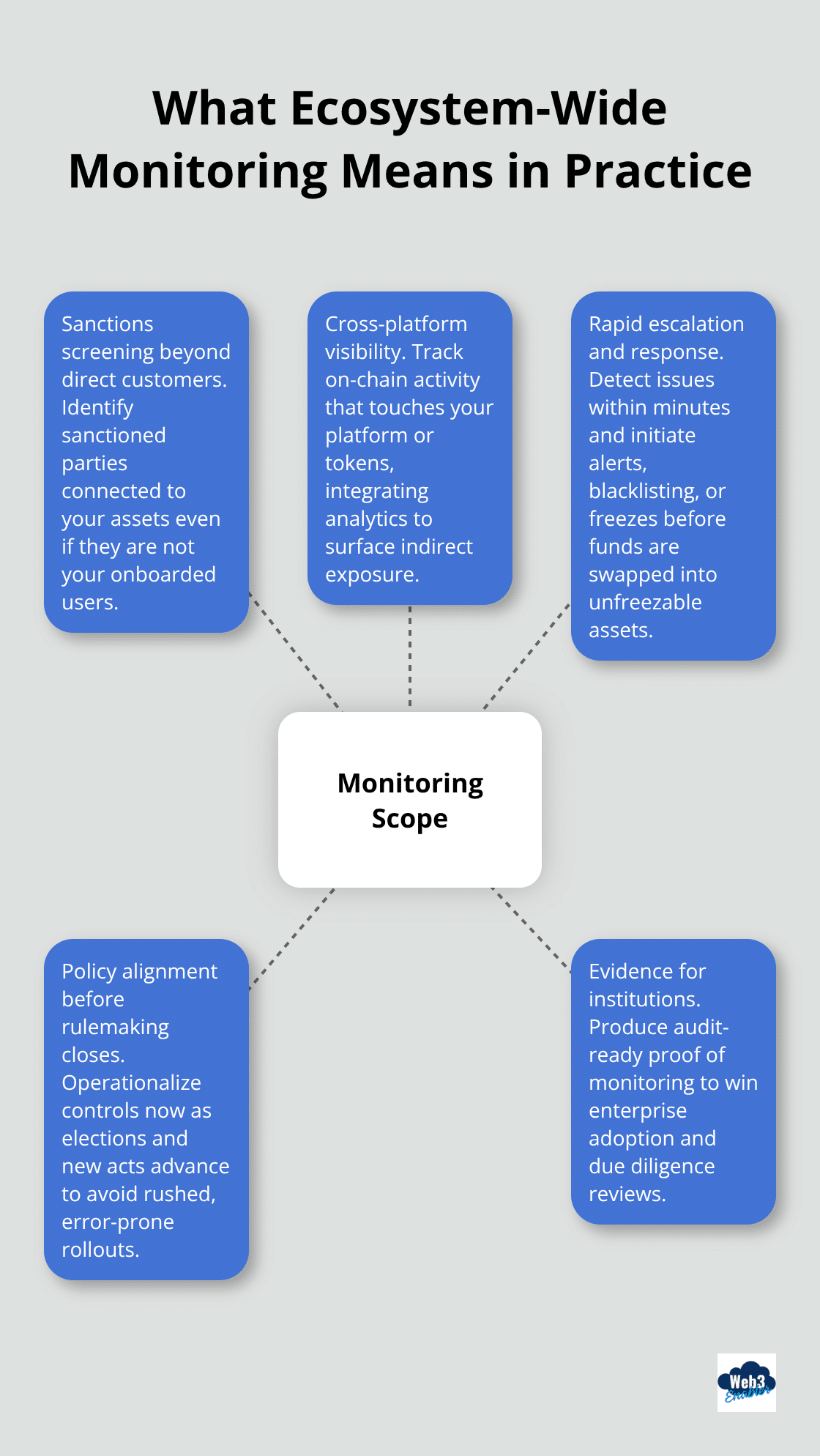

Regulators Now Expect Ecosystem-Wide Monitoring

According to Elliptic’s January 2026 stablecoin report, regulators now expect issuers to identify sanctioned parties even when they aren’t direct customers-meaning ecosystem-wide monitoring isn’t a nice-to-have, it’s table stakes. The window to get ahead of these requirements is closing fast, especially as midterm elections approach and legislative momentum around the Clarity Act intensifies. Your compliance posture determines whether you participate in the next wave of institutional adoption or get left behind.

Non-Compliance Carries Real Penalties

Non-compliance isn’t a slap on the wrist. Financial crime enforcement in crypto has ramped up significantly, with regulators imposing hefty penalties for lax controls. The Wolfsberg Group’s September 2025 principles for financial institutions working with stablecoin issuers set the bar high: banks must verify issuer licensing, assess compliance controls, and screen counterparties for high-risk activity. If your payment infrastructure can’t demonstrate robust transaction monitoring, Travel Rule compliance, and sanctions screening, you expose yourself to regulatory action, customer loss, and reputational damage.

Regulators are cracking down on institutions that enabled illicit flows, and your customers-especially institutional ones-won’t touch a payments partner without proof of serious compliance infrastructure.

Institutions Demand Visible Controls

Institutions considering stablecoin payments want assurance, not promises. They need to see that your platform monitors on-chain activity in real time, flags suspicious patterns, and can freeze or blacklist compromised assets within minutes. Hackers steal stablecoins and rapidly swap them to unfreezable tokens, so speed matters; issuers who can’t demonstrate rapid intervention capabilities will lose institutional confidence.

Banks integrating stablecoins-whether by issuing their own token, partnering with a regulated issuer, or enabling public stablecoins like USDC-all require the same foundation: documented controls that show you’re serious about preventing illicit use. The compliance infrastructure isn’t a cost center; it’s the credential that opens doors to enterprise adoption. Companies that treat compliance as a checkbox rather than a competitive advantage are choosing to stay small.

This foundation of trust and control sets the stage for what comes next: understanding the specific compliance requirements that your stablecoin payment strategy must address.

What Compliance Actually Demands From Your Stablecoin Operation

KYC and AML Form Your First Line of Defense

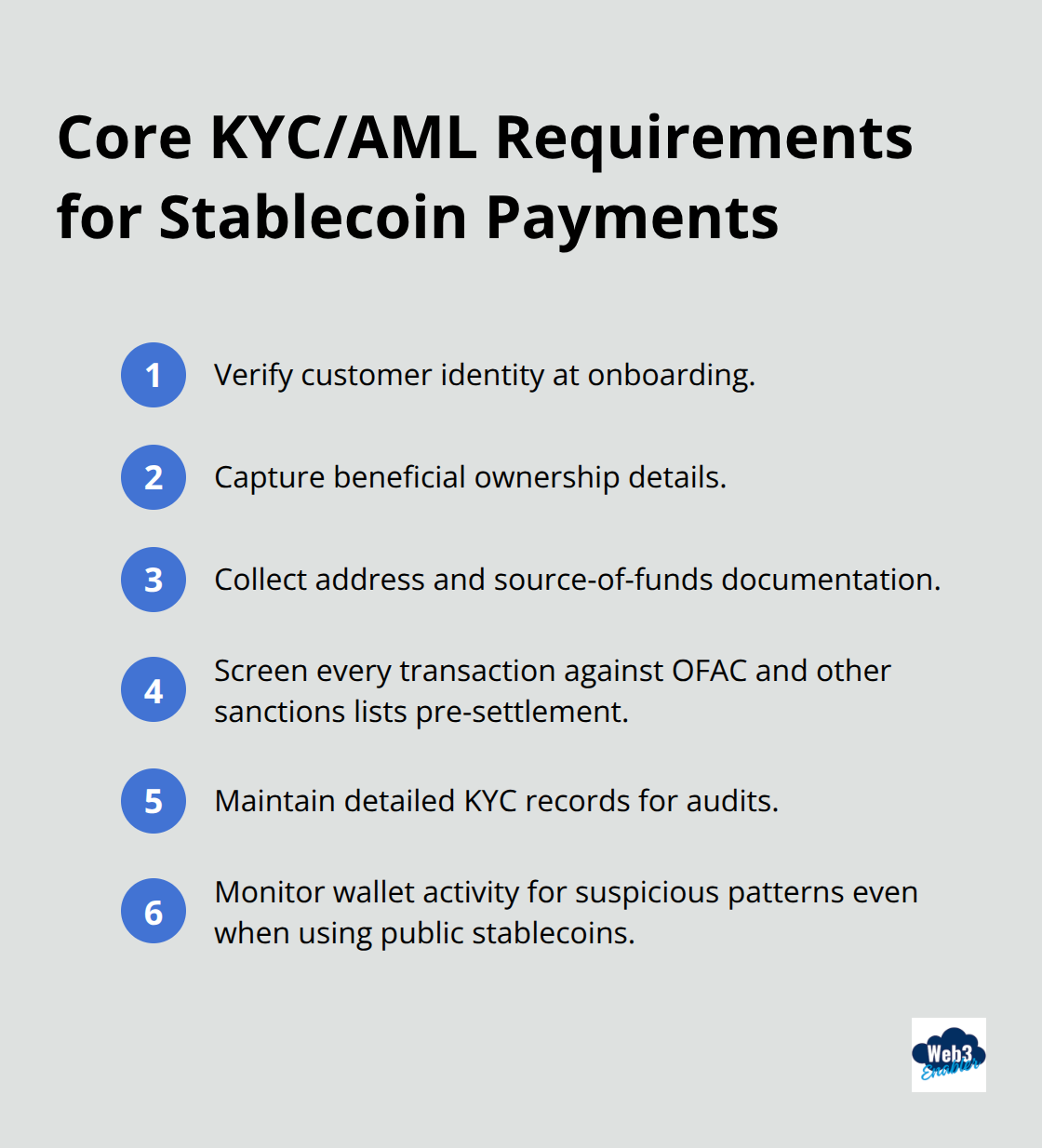

KYC and AML aren’t bureaucratic boxes to tick-they’re your first line of defense against becoming a money laundering pipeline. When you accept stablecoin payments, you must know who sends and receives funds, and regulators expect you to screen every transaction against sanctions lists before it settles.

The GENIUS Act mandates that platforms verify customer identity upfront and maintain detailed records of beneficial ownership, which means you can’t accept a wallet address and call it done. You need to collect names, addresses, and source-of-funds documentation from customers before they move money through your system.

KYC and AML requirements form the backbone of baseline controls for stablecoin issuers and payment platforms. If you integrate public stablecoins like USDC or USDT, you still screen wallet activity against OFAC lists and other sanctions databases. The cost of skipping this step hits hard: regulators have imposed seven-figure penalties on platforms that failed to catch illicit flows, and institutional partners will drop you instantly if you can’t prove your KYC process works.

Real-Time Transaction Monitoring Separates Leaders From Laggards

Transaction monitoring transforms compliance from theory into operational reality. You need systems that flag anomalies-sudden spikes in transaction volume, transfers to high-risk jurisdictions, rapid movement of funds through multiple wallets-and alert your compliance team within minutes, not days. Regulators now expect ongoing transaction monitoring across your entire ecosystem, not just direct customer activity. This means you’re responsible for detecting suspicious patterns even when the originating customer isn’t your direct client.

Travel Rule compliance adds another layer: when customers send stablecoins across platforms, you must transmit sender and recipient information to receiving platforms to maintain traceability and prevent bad actors from hiding in transaction chains. If hackers steal stablecoins from your system, you need the ability to freeze or blacklist those tokens within minutes-delays of hours or days give criminals time to swap stolen tokens into unfreezable assets. Automated monitoring tools integrated into your payment infrastructure beat manual spreadsheet reviews every time. Platforms using blockchain analytics solutions can screen transactions pre-settlement, catching risks before funds move, whereas platforms relying on post-transaction reviews play catch-up.

Cross-Border Payments Demand Layered Controls

When stablecoins cross borders, complexity multiplies. The Wolfsberg Group’s September 2025 principles for financial institutions require banks to assess the regulatory regime of each jurisdiction where stablecoins flow and verify that receiving jurisdictions maintain equivalent AML/CFT standards. You can’t simply enable payments to every country-some jurisdictions lack adequate financial crime controls, and sending stablecoins there exposes you to regulatory action.

Your payment system must block transfers to sanctioned jurisdictions, high-risk countries, and known illicit actors before settlement occurs. Beneficial ownership disclosures become mandatory for cross-border transfers above certain thresholds, so you need documentation that proves the ultimate beneficiary of funds isn’t a shell company or sanctions-listed entity.

If you partner with a regulated stablecoin issuer or integrate public stablecoins, you still carry responsibility for knowing your counterparties and screening their reserve management practices. Banks now verify issuer compliance controls and assess whether issuers maintain adequate reserves before agreeing to process their transactions, which means your due diligence on partners becomes part of your compliance posture. Robust cross-border stablecoin payments require a compliance infrastructure that most traditional payment systems lack-and that infrastructure gap is precisely why institutional adoption has accelerated only recently, as regulatory frameworks solidified across major markets.

How to Build Stablecoin Payments That Actually Work

Your compliance strategy lives or dies based on the partners and tools you choose. We at Web3 Enabler see too many companies pick stablecoin infrastructure based on speed-to-market alone, then scramble when regulators ask uncomfortable questions about their transaction monitoring or reserve verification. The truth is simpler: strong compliance infrastructure costs less than regulatory penalties, and institutions won’t touch your payments offering without it.

Vet Your Partners With Ruthless Discipline

Start by vetting partners ruthlessly. If you issue your own stablecoin, your banking partner must verify your licensing, assess your compliance controls, and screen your reserve management practices before they hold your funds. The Wolfsberg Group’s September 2025 principles spell this out clearly: banks now require issuers to document their governance, risk management frameworks, and blockchain monitoring capabilities.

If you partner with a regulated issuer like Circle or integrate public stablecoins, conduct the same due diligence in reverse. Demand that your issuer partner demonstrate real-time transaction monitoring, Travel Rule compliance across platforms, and the ability to freeze or blacklist tokens within minutes. Ask for their compliance policies in writing, request third-party audit reports on their controls, and verify they hold licenses in major jurisdictions (the US, EU, and Hong Kong). Partners that dodge these questions aren’t worth the regulatory risk. Your customers will ask the same questions, so get comfortable answering them now.

Automate Compliance to Scale Without Risk

Automation separates compliant operations from ones that crash under regulatory scrutiny. Manual compliance-spreadsheets tracking transactions, humans reviewing OFAC lists, email-based incident reporting-fails at scale and leaves audit trails that regulators hate. Implement systems that screen transactions against sanctions databases before settlement occurs, flag anomalies in real time, and generate audit-ready reports automatically.

Blockchain analytics solutions integrate into your payment infrastructure and catch suspicious patterns within seconds: sudden volume spikes, rapid movement through multiple wallets, transfers to high-risk jurisdictions. You need documentation systems that capture KYC data, beneficial ownership information, and source-of-funds verification at onboarding, then maintain audit trails as transactions flow through your system. If you operate within Salesforce, connect blockchain compliance directly into your existing corporate infrastructure to eliminate manual handoffs between systems.

Establish Governance That Regulators Respect

Regular audits and internal controls complete the picture. Conduct independent audits of your transaction monitoring systems at least annually, testing whether your controls actually catch the suspicious activity they’re supposed to catch. Have your compliance team run monthly reviews of flagged transactions to verify your monitoring rules aren’t missing threats or generating false positives that waste resources.

Document everything: your KYC procedures, your transaction monitoring rules, your incident response protocols. When regulators knock on the door-and they will-auditable documentation proves you built controls with intent, not after the fact. Assign a dedicated compliance officer who reports directly to leadership, not buried in operations. That person owns the compliance strategy, manages vendor relationships, and ensures your team stays current on regulatory changes across jurisdictions where you operate. Regulators expect compliance governance to have teeth, which means your compliance officer needs authority to block transactions, reject customers, and override business pressure when controls demand it.

Final Thoughts

Stablecoin payments compliance isn’t a barrier to entry anymore-it’s your competitive advantage. Companies that build compliance into their payment strategy from day one move faster, not slower, and they attract institutional partners who demand proof of controls. Banks issuing their own tokens, platforms partnering with regulated issuers, and businesses integrating public stablecoins all need the same foundation: documented controls that prove you take illicit use seriously.

The regulatory frameworks now exist across the US, EU, Hong Kong, and beyond, and institutional capital waits for clarity to flow into stablecoin payments. The companies that move now will own the next generation of payment infrastructure, while the ones that delay will scramble to retrofit compliance into systems that weren’t built for it. Vetting your partners, automating your monitoring, and establishing governance that regulators respect separate winners from the rest.

Web3 Enabler connects your blockchain infrastructure directly into your existing Salesforce systems, eliminating manual handoffs and building stablecoin payments compliance into your payment flow from the start. Visit Web3 Enabler to explore how Salesforce-native blockchain solutions accelerate your stablecoin payment strategy without sacrificing control. The path forward is clear, the tools exist, and the regulatory framework is solid.