Your business receives payments in stablecoins, but converting them back to traditional currency shouldn’t be complicated. Stablecoin off-ramp payments bridge that gap, letting you move digital assets into your bank account quickly and affordably.

At Web3 Enabler, we’ve seen finance teams waste time and money on clunky conversion processes. This guide shows you how to implement seamless off-ramps directly within your Salesforce environment.

Why Off-Ramps Matter Now

The Scale of Stablecoin Adoption Versus Conversion Friction

Stablecoins handled record transaction volumes in 2025, yet most businesses still struggle to convert those holdings back to fiat currency efficiently. The problem isn’t adoption-it’s friction. Your finance team receives payments in USDC or USDT, but converting them requires jumping between wallets, exchanges, and banking systems. Each step adds time, cost, and reconciliation headaches.

A transfer that costs about 55 dollars and takes four days through traditional wires settles in roughly 12 seconds for under 25 cents with stablecoins, according to research from Crowe. That speed difference matters when you manage global operations across multiple currencies and time zones.

Why Traditional Systems Fall Short

Traditional cross-border payments still dominate because businesses haven’t built the infrastructure to make off-ramps seamless. Banks process payments through aging systems that weren’t designed for digital assets. Finance teams manually track on-chain transactions separately from their accounting records. Compliance and audit trails become fragmented across multiple platforms.

Web3 Enabler recognized this gap early-we built a native blockchain platform on the Salesforce AppExchange that lets your off-ramp work directly within your CRM. Your finance team no longer needs to leave Salesforce to convert stablecoins to fiat.

The Economics of Off-Ramp Conversion

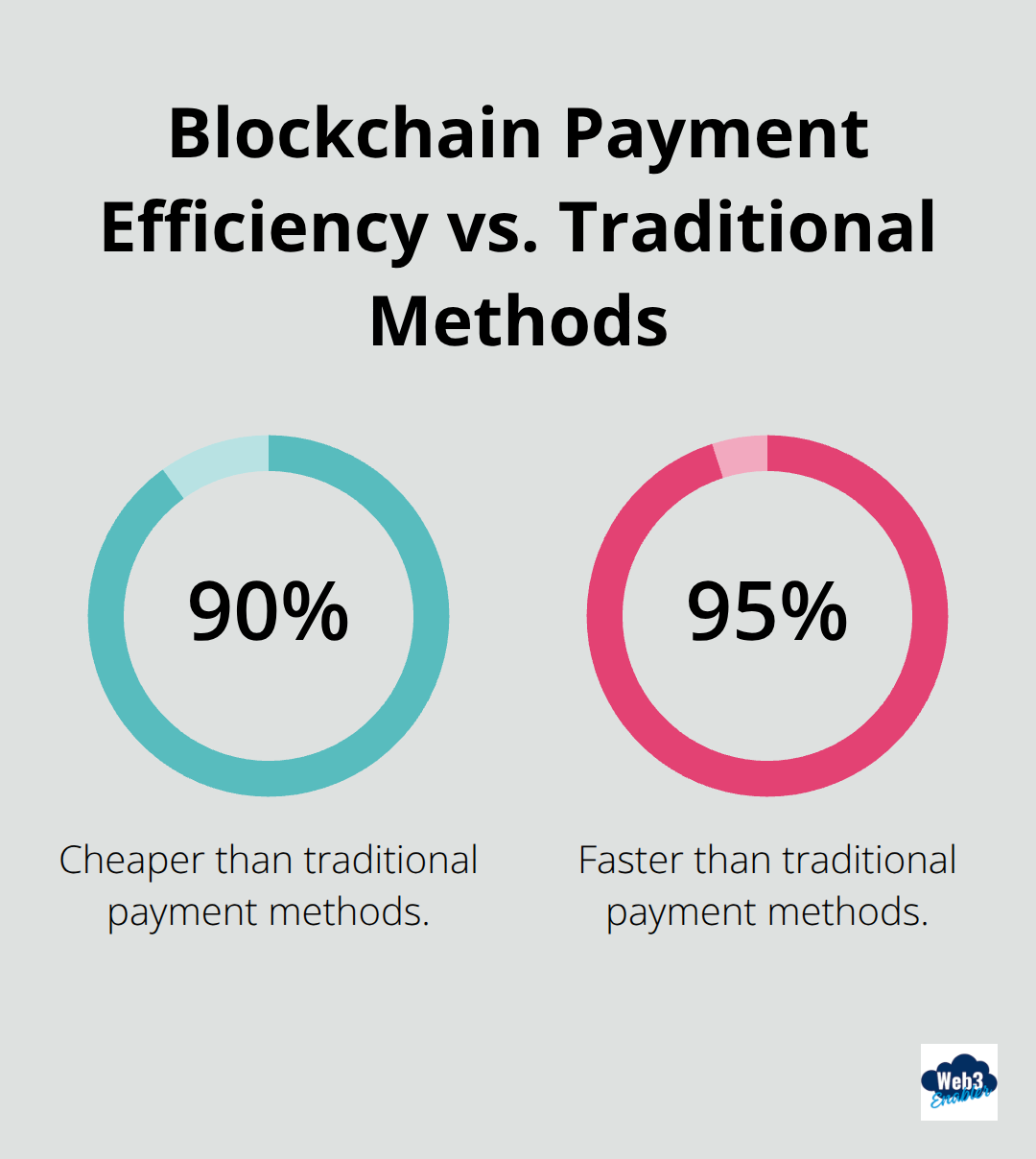

Blockchain payments are 90 percent cheaper and 95 percent faster than traditional methods, with BASE on-ramp and off-ramp costs around 0.5 percent and transaction fees measured in pennies. Compare that to wire fees of 25 to 50 dollars, ACH delays of 1 to 3 days, and international correspondent banking fees that can exceed 100 dollars per transaction.

For a company processing 10 million dollars monthly in cross-border payments, traditional rails cost roughly 100,000 dollars annually in fees alone. Stablecoin off-ramps cut that to under 5,000 dollars. The math is straightforward-off-ramps eliminate the middlemen and the delays that inflate costs.

Liquidity Management and Operational Flexibility

Off-ramps solve a real operational problem: they let your treasury team manage liquidity without converting to fiat unnecessarily. You hold stablecoins longer, capture yield on idle balances, and convert only when you need to pay suppliers or meet payroll. Modern Treasury has processed over 400 billion dollars in payments, and their partnership with Paxos shows that enterprises increasingly view stablecoins as a faster, programmable form of money movement.

Your finance team shouldn’t choose between speed and safety-off-ramps deliver both. The next section shows how these conversions actually work and what happens when you integrate them into your Salesforce environment.

How Off-Ramps Actually Work

The Conversion Process: From Blockchain to Bank Account

When your business receives stablecoins, the conversion back to fiat currency happens through a series of on-chain and off-chain steps that take seconds rather than days. Your stablecoins sit in a wallet address controlled by your organization, and when you initiate an off-ramp, a conversion service exchanges those tokens for fiat currency at the current market rate, then deposits the funds directly into your designated bank account. Settlement typically completes within 12 seconds for under 25 cents according to research from Crowe, compared to traditional wire transfers that offer settlement time advantage. The speed advantage compounds when you manage multiple currencies across time zones-your treasury team executes conversions during business hours in one region while funds appear in bank accounts across different markets almost instantaneously.

Banking Infrastructure and Regulatory Handoffs

The integration between blockchain rails and banking systems relies on partnerships between stablecoin issuers and regulated financial institutions. Circle’s USDC Access, Stripe’s Bridge, and platforms like Abyiss connect stablecoin networks to traditional banking infrastructure, handling the regulatory handoff that allows your off-ramp to settle as legitimate fiat deposits. Compliance happens at the on-ramp and off-ramp boundaries through KYC and AML checks performed by these providers, not throughout the blockchain transaction itself. Your finance team gains a significant advantage here: instead of managing separate audit trails for on-chain activity and banking records, you can embed off-ramp conversions directly into your Salesforce environment. This eliminates the manual reconciliation work that traditionally plagues stablecoin operations.

Real-World Cost Impact and Scale

Real-world implementations show that enterprises processing substantial cross-border volumes reduce conversion costs dramatically. A company moving 10 million dollars monthly internationally spends roughly 100,000 dollars annually on traditional rails but under 5,000 dollars when using stablecoin off-ramps with BASE network costs around 0.5 percent plus transaction fees measured in pennies. Modern Treasury’s processing of over 400 billion dollars in payments demonstrates that enterprises increasingly trust stablecoin infrastructure for mission-critical financial workflows. Their partnership with Paxos shows how regulated stablecoin rails integrate seamlessly with existing accounting systems and payment stacks without requiring wholesale rewrites of your core financial infrastructure.

Regulatory Clarity and Operational Predictability

Regulatory frameworks like the GENIUS Act (signed in July 2025) establish clear guardrails for stablecoin issuance and reserve requirements, making the compliance environment more predictable for your treasury operations. These frameworks create confidence that your off-ramp conversions operate within established legal boundaries. Financial institutions now have the regulatory certainty they need to build stablecoin infrastructure into their standard payment offerings, which means your organization can rely on stable, compliant conversion pathways rather than experimental or uncertain channels.

The mechanics of off-ramp conversion are now clear-but the real transformation happens when you integrate these conversions into your existing financial systems. The next section shows how to embed off-ramp functionality directly within Salesforce, turning conversion from a separate process into a seamless part of your treasury workflow.

Building Off-Ramps Into Your Salesforce Workflow

Your finance team currently manages off-ramps outside Salesforce, which means stablecoin conversions live in a separate system from your revenue recognition, customer accounts, and treasury records. This fragmentation creates reconciliation delays and audit risk. Web3 Enabler built a native blockchain platform on the Salesforce AppExchange that eliminates that separation entirely. When your organization receives stablecoin payments through Financial Services Cloud or Commerce Cloud, the off-ramp conversion happens natively within Salesforce itself. Your conversion request triggers an automated workflow that connects to regulated off-ramp providers like Circle’s USDC Access or Stripe’s Bridge, executes the exchange at current market rates, and deposits funds directly into your bank account. The entire transaction creates a single audit trail within Salesforce. Your finance team sees the customer payment, the conversion execution, and the bank deposit in one place, eliminating the manual record-keeping that traditionally plagues stablecoin operations.

Native Integration Across Your Salesforce Clouds

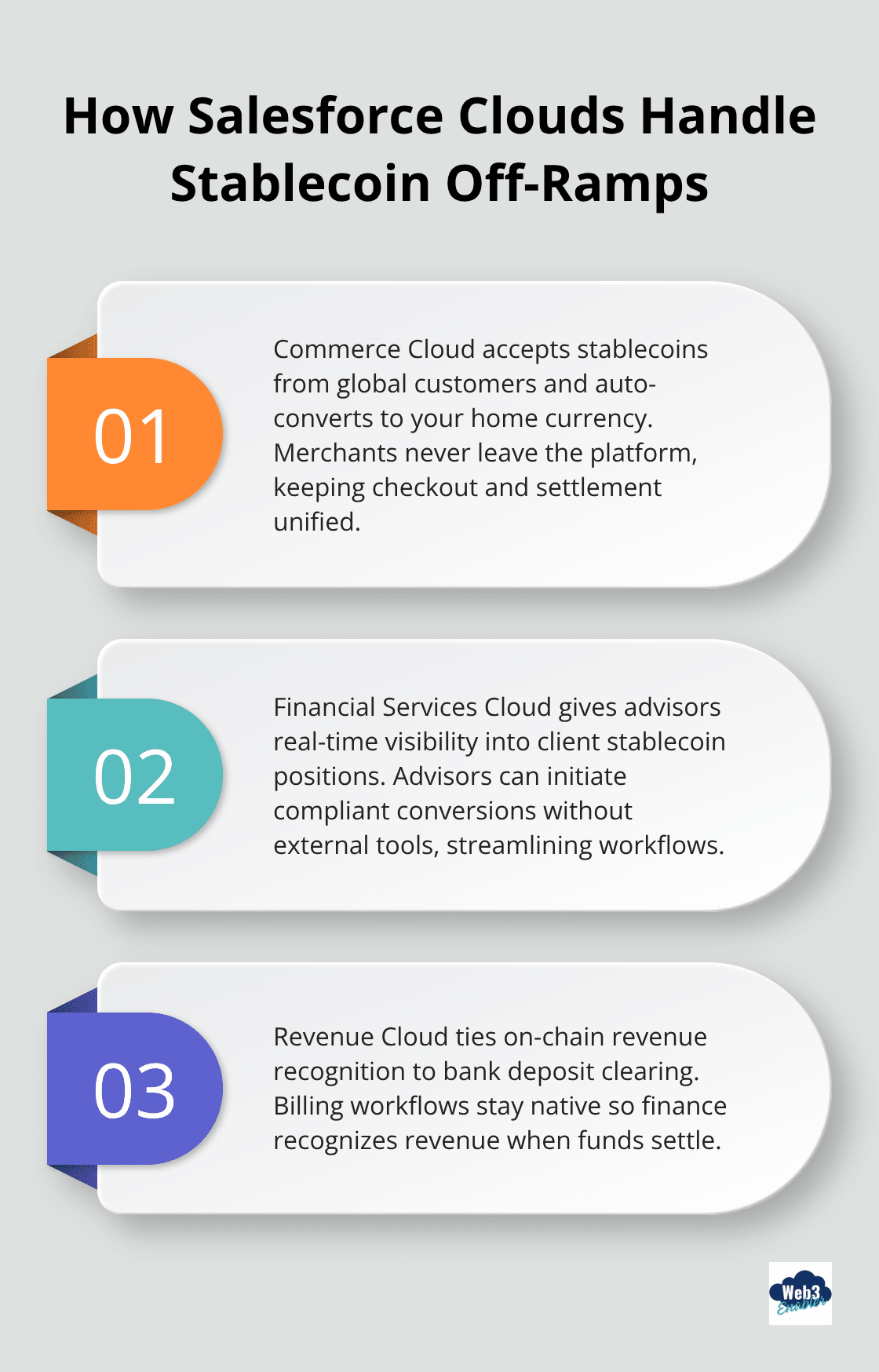

Commerce Cloud merchants accept stablecoins from global customers and automatically convert them to their home currency without ever leaving the platform. Financial Services Cloud advisors gain real-time visibility into client stablecoin positions and can initiate conversions on their behalf, streamlining wealth management workflows that previously required external tools and manual intervention.

Revenue Cloud users automate on-chain revenue recognition and settlement directly within their billing workflows, meaning your finance team recognizes revenue when the bank deposit clears, not when they manually match blockchain data to accounting records.

Real-Time Reconciliation and Liquidity Visibility

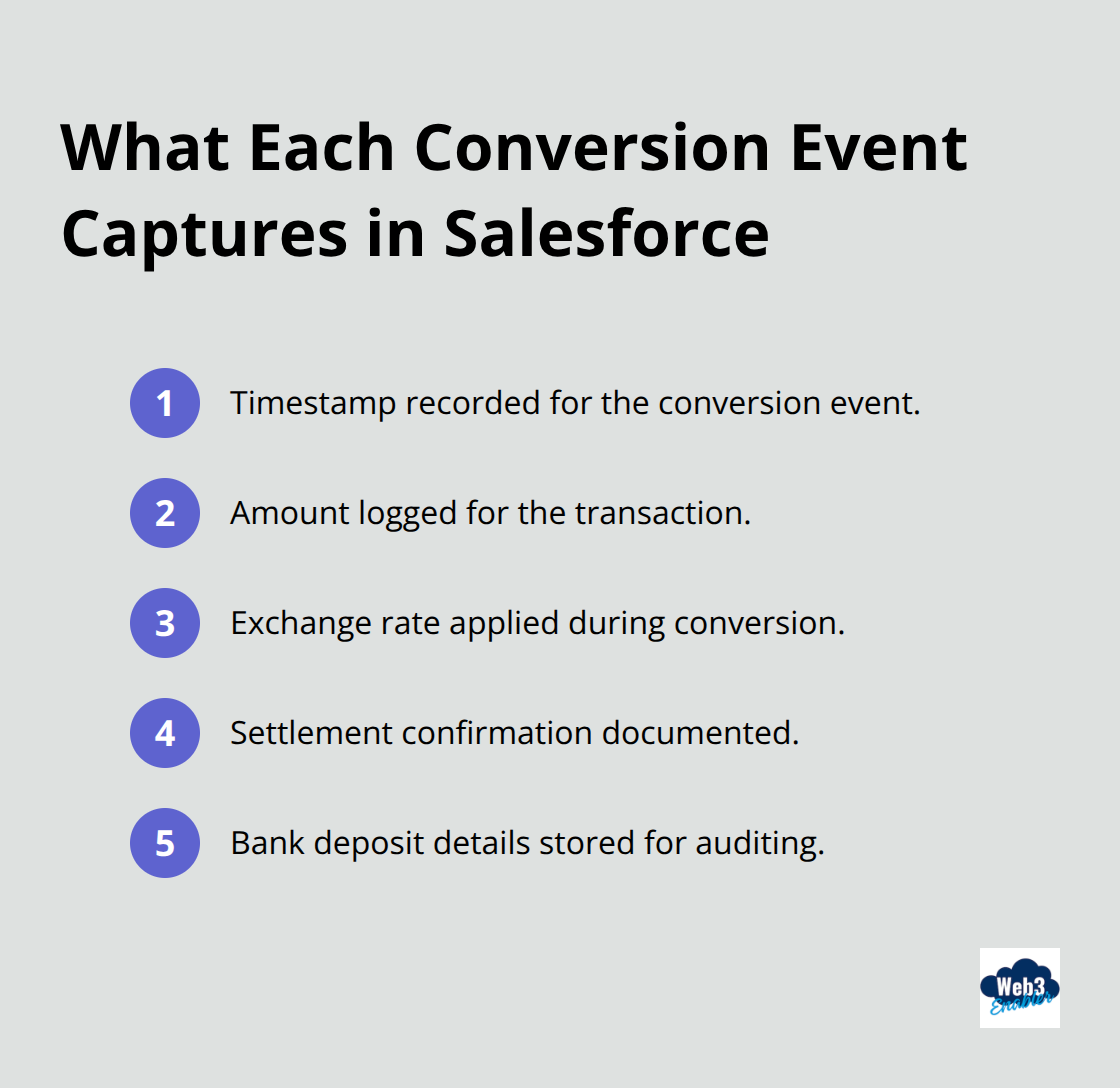

Traditional off-ramp workflows force your treasury team to reconcile blockchain transactions against bank statements manually, creating delays and error risk. Web3 Enabler eliminates this friction through native Salesforce objects that capture every conversion event-timestamp, amount, exchange rate, settlement confirmation, and bank deposit details.

Your liquidity management improves because you hold stablecoins longer, capture yield on idle balances, and convert only when operational needs require it.

Compliance and Audit Trail Management

Web3 Enabler integrates with Salesforce’s native compliance and reporting tools, so your team maintains full auditability without building custom solutions. You track which users initiated conversions, when they executed, at what rates, and how they settled-all within Salesforce’s audit trail system that satisfies regulatory requirements and internal governance standards. Your conversion data lives in the same system as your customer records and financial transactions, eliminating the fragmented documentation that creates compliance risk.

Final Thoughts

Stablecoin off-ramp payments transform how your finance team manages global liquidity by consolidating treasury operations into a single Salesforce environment where conversions happen in seconds at a fraction of traditional costs. A transaction that costs fifty-five dollars and takes four days through wire transfer settles for under twenty-five cents in twelve seconds with stablecoins, and your organization captures that speed advantage immediately. Your operational costs drop dramatically when you eliminate wire fees, correspondent banking charges, and the labor required to reconcile blockchain transactions against bank statements manually.

The regulatory environment now supports this transition with frameworks like the GENIUS Act establishing clear guardrails for stablecoin operations, giving your organization confidence that off-ramp conversions operate within established legal boundaries. Financial institutions increasingly embed stablecoin infrastructure into standard payment offerings, meaning your conversion pathways remain stable and compliant rather than experimental. Web3 Enabler brings this capability directly into your Salesforce environment as the only native blockchain platform on the Salesforce AppExchange, integrating seamlessly across Financial Services Cloud, Commerce Cloud, and Revenue Cloud without requiring system rewrites or external tools.

Start by evaluating one use case-perhaps cross-border supplier payments or customer refunds-and measure the cost and time savings against your current process. Your compliance team maintains full auditability through native Salesforce objects, and your operations team executes conversions without leaving the CRM. Explore how Web3 Enabler modernizes your payment infrastructure and captures the efficiency gains your treasury team deserves.

Stablecoin Off-Ramp Payments FAQs

What are stablecoin off-ramp payments?

Stablecoin off-ramp payments are the process of converting stablecoins like USDC or USDT into traditional currency (fiat) and depositing those funds into your business bank account. Off-ramps bridge blockchain rails and the banking system, so you can accept stablecoin payments globally while still running payroll, paying vendors, and closing your books in fiat. :contentReference[oaicite:1]{index=1}

How is an off-ramp different from an on-ramp?

An on-ramp converts fiat into crypto or stablecoins so customers can pay on-chain. An off-ramp converts stablecoins back into fiat so your business can use funds in traditional banking workflows. Most companies need both: on-ramps to receive stablecoin payments, and off-ramps to settle into bank accounts for accounting, taxes, and operating expenses. :contentReference[oaicite:2]{index=2}

How long does it take to convert USDC or USDT to fiat?

The blockchain portion of a stablecoin transfer can confirm quickly, but the total off-ramp time depends on your provider’s compliance checks, liquidity, and bank payout rails. In practice, well-integrated off-ramps aim to move from stablecoins to a bank deposit far faster than traditional cross-border wires, especially when compliance and payout steps are automated. :contentReference[oaicite:3]{index=3}

What fees should businesses expect with stablecoin off-ramps?

Off-ramp costs typically include (1) blockchain network fees and (2) a conversion or settlement fee charged by your provider. Fees vary by network, corridor, and payout method, but off-ramps are often used to reduce the stacked intermediary fees common in traditional cross-border payments. The biggest cost driver is usually the provider’s conversion/spread and payout fee, not the blockchain transaction itself. :contentReference[oaicite:4]{index=4}

Why do finance teams struggle with off-ramps today?

Most off-ramp headaches come from fragmentation: payments arrive in a wallet, conversions happen in a separate platform, and bank deposits show up elsewhere, leaving teams to manually reconcile across systems. That creates delays, reporting risk, and extra labor. The cleanest workflows keep payment, conversion, and settlement records tied together so reconciliation and audit trails are consistent end-to-end. :contentReference[oaicite:5]{index=5}

What compliance checks happen during off-ramp conversion?

Off-ramps typically involve identity and risk controls at the points where stablecoins touch regulated financial infrastructure. Providers commonly perform KYC/AML and transaction monitoring so the fiat payout to a bank account is compliant. In the U.S., stablecoin regulation has moved toward clearer federal guardrails, which is one reason more mainstream payment and treasury providers are building stablecoin settlement pathways. :contentReference[oaicite:6]{index=6}

Is stablecoin adoption really big enough to justify building off-ramps?

Yes, stablecoin usage has reached “infrastructure” scale. Industry reporting shows stablecoins hit record transaction volume in 2025, and major payments players are actively expanding stablecoin settlement and account capabilities. If your business is paid internationally, manages multi-currency flows, or wants faster settlement, off-ramps are increasingly a practical requirement, not an experiment. :contentReference[oaicite:7]{index=7}

How do Stripe, Visa, and Modern Treasury relate to stablecoin settlement?

Large platforms have publicly signaled stablecoin momentum. Stripe has announced stablecoin account and payments support including USDC. Visa has announced USDC settlement capabilities with U.S. partners as part of its stablecoin settlement efforts. Modern Treasury has announced a partnership to integrate stablecoin and settlement technology into its platform for business money movement and reconciliation. :contentReference[oaicite:8]{index=8}

What should businesses look for in an off-ramp provider?

Prioritize (1) regulatory posture and strong compliance controls, (2) reliable liquidity and predictable settlement timelines, (3) transparent fees and clear FX/conversion handling, (4) security and auditability, and (5) integrations that reduce manual reconciliation. If the provider can’t connect cleanly to your finance stack and produce consistent reporting, you’ll save minutes on settlement but lose hours in operations.

How do off-ramps fit into a Salesforce-based finance workflow?

For Salesforce-centered teams, the goal is to keep customer payment, conversion details, and settlement outcomes connected to the same customer and revenue records. That way, finance teams can reconcile faster, prove an audit trail, and report reliably without exporting data across multiple tools. The best implementations treat off-ramping as a standard treasury step inside the system of record, not a separate “crypto workflow.”