Cross-border payments remain one of the biggest pain points for businesses worldwide. Traditional systems take days to settle while newer blockchain solutions promise near-instant transfers.

Cross-border payments remain one of the biggest pain points for businesses worldwide. Traditional systems take days to settle while newer blockchain solutions promise near-instant transfers.

The Ripple vs SWIFT debate has dominated treasury discussions for years. We at Web3 Enabler see companies struggling with slow international payments that drain resources and delay operations.

This comparison examines which system actually delivers better results for modern businesses.

How Do Ripple and SWIFT Actually Work?

SWIFT Messages Banks But Moves No Money

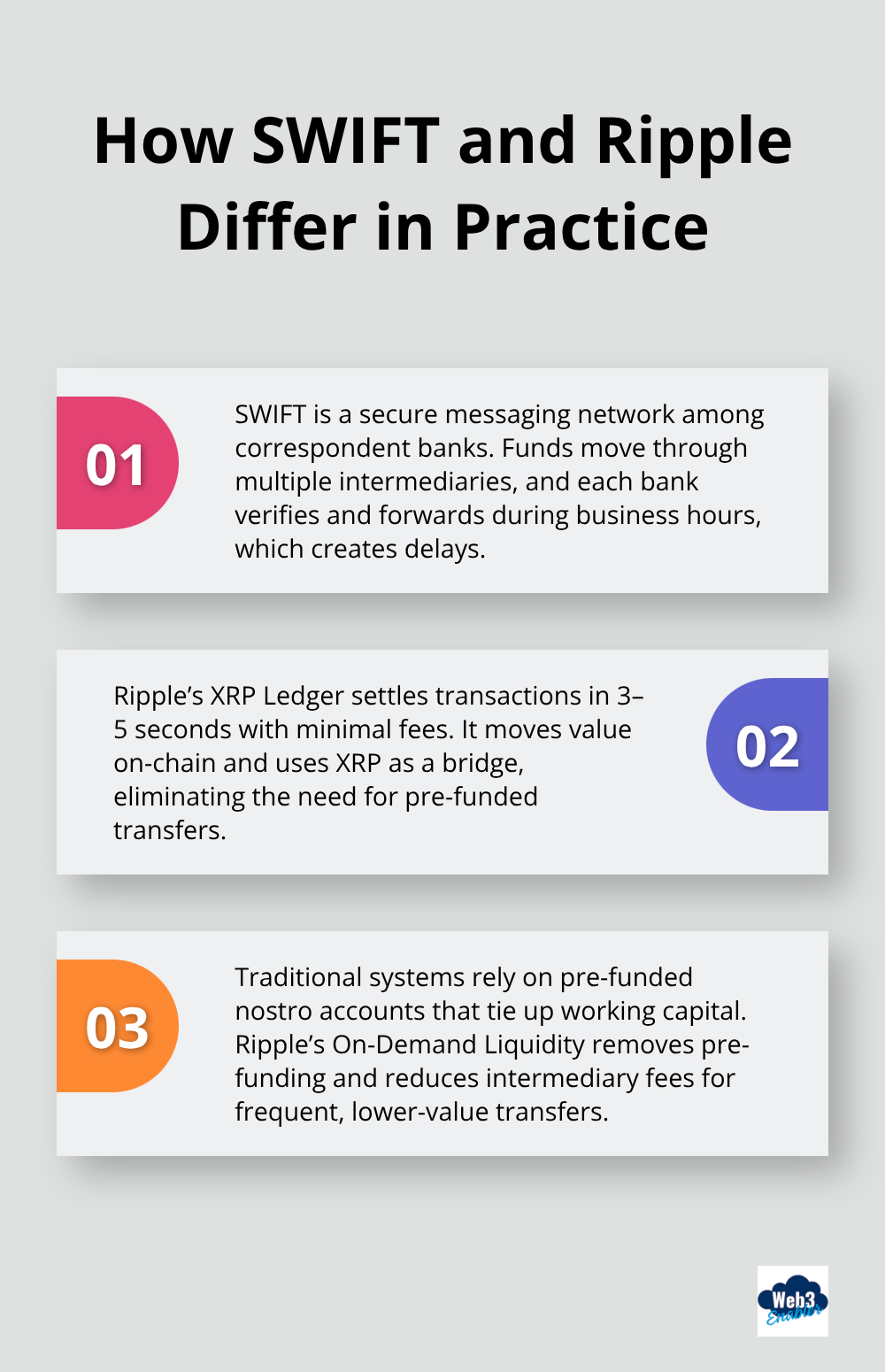

SWIFT operates as a messaging network that has connected banks since 1973, but it doesn’t move money directly. When you send a wire transfer, SWIFT sends secure messages between correspondent banks while the actual funds travel through multiple intermediary institutions. This process creates delays because each bank must verify, process, and forward the transaction during business hours only.

The system relies on pre-funded nostro accounts that banks maintain with partners worldwide, which ties up billions in working capital. Traditional payment systems show varying settlement speeds, but this doesn’t guarantee the recipient gets credited immediately due to local clearing systems and compliance checks.

Ripple Settles in Seconds Not Days

Ripple’s XRP Ledger processes transactions in 3-5 seconds with fees of just 0.00001 XRP per transaction. Unlike SWIFT’s messaging approach, Ripple actually moves value instantly through its blockchain network. Companies that use Ripple’s On-Demand Liquidity service eliminate pre-funding requirements entirely because XRP acts as a bridge currency that converts instantly between any two currencies.

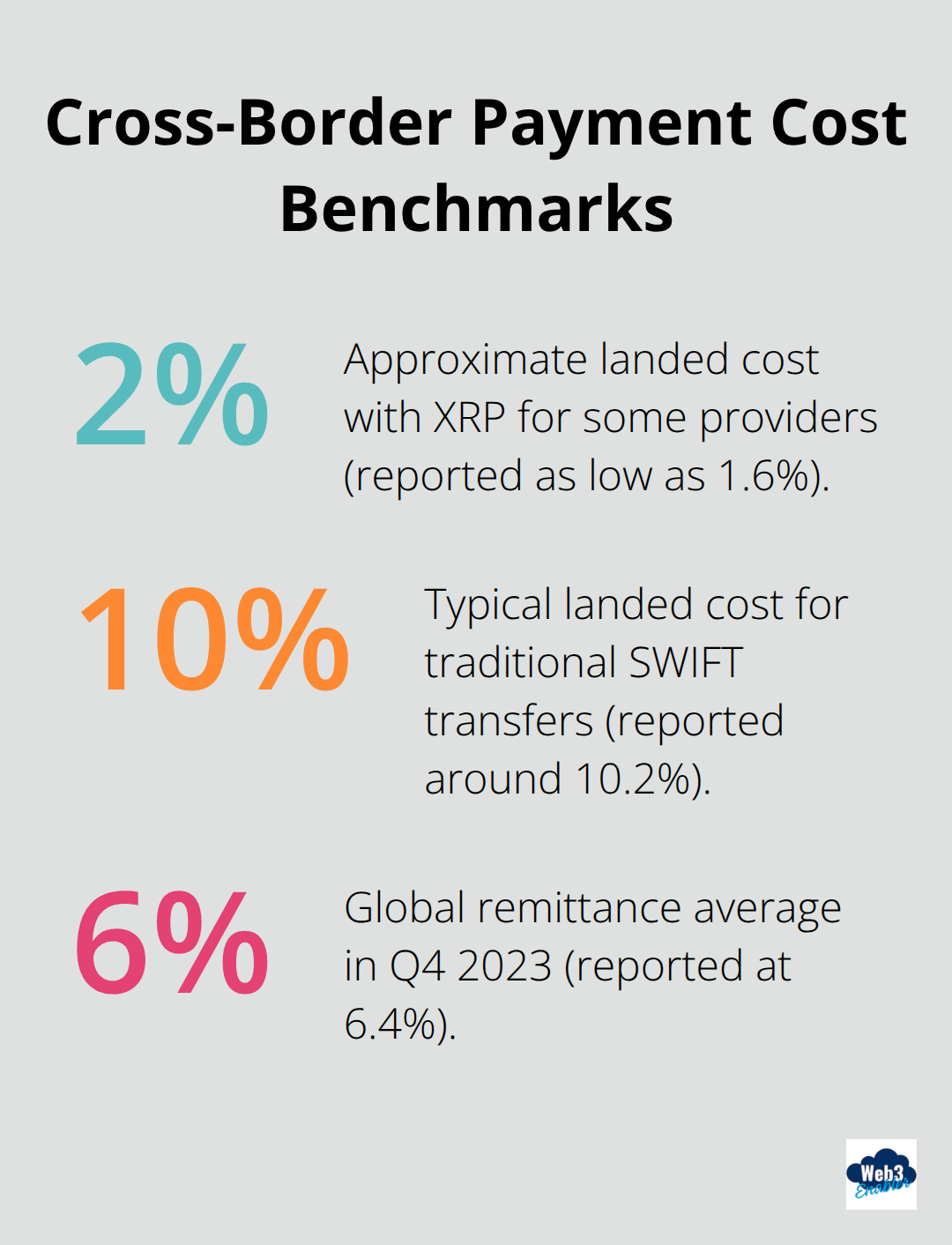

SBI Remit and other payment providers report landed costs as low as 1.6% with XRP compared to 10.2% for traditional SWIFT transfers. The 24/7 operation means payments process outside banking hours, weekends, and holidays (something SWIFT cannot match).

Traditional Banks Face Higher Operational Costs

Traditional SWIFT transfers cost $25-50 per transaction with 3-5 day settlement periods. The global remittance average reached 6.4% in Q4 2023 according to World Bank data, double the UN Sustainable Development Goal target of 3%.

Multiple compliance checks at each correspondent bank add processing time and operational overhead. Ripple eliminates most intermediary fees and provides transparent exchange rates (particularly effective for high-volume, low-to-mid value payments where fixed SWIFT fees become prohibitively expensive).

These fundamental differences in architecture create vastly different experiences for businesses that need to move money across borders regularly.

Which System Do Banks Actually Use?

SWIFT Dominates Traditional Banking Networks

SWIFT connects over 11,000 financial institutions across 200 countries and territories, processing messages for trillions in daily transactions. The network handles 1 million average daily volume of transactions, making it the backbone of international banking.

Major banks like JPMorgan Chase, Bank of America, and Deutsche Bank rely exclusively on SWIFT for correspondent banking relationships. The system’s 50-year track record provides regulatory certainty that compliance officers trust, especially for large-value transactions exceeding $1 million where bank-to-bank guarantees matter most.

Ripple Gains Ground in Payment Corridors

Ripple operates in over 40 countries with partnerships that include Santander, American Express, and Standard Chartered. The network processes roughly 1.5 billion XRP transactions annually, though this represents a fraction of SWIFT’s volume.

SBI Holdings uses Ripple’s technology for remittances across Asia, while MoneyGram integrated On-Demand Liquidity for select corridors in 2021. Banks that choose Ripple typically focus on specific high-frequency, low-value payment corridors where speed and cost reduction justify the regulatory complexity.

Regulatory Challenges Shape Adoption Patterns

Regulatory clarity remains Ripple’s biggest challenge, with ongoing SEC litigation in the United States creating uncertainty for potential US bank partners. However, markets like Japan, Singapore, and the UK provide clearer frameworks that enable institutional adoption.

SWIFT benefits from established regulatory relationships built over decades, particularly in heavily regulated markets like the European Union and United States. Financial institutions often prefer the regulatory certainty that comes with traditional correspondent banking relationships, even when newer technologies offer operational advantages for cross-border payments.

These adoption patterns reveal how regulatory environment and transaction types influence which payment system businesses choose for their treasury operations.

What Business Value Do These Systems Actually Deliver?

Treasury Teams Save Hours With Faster Settlement

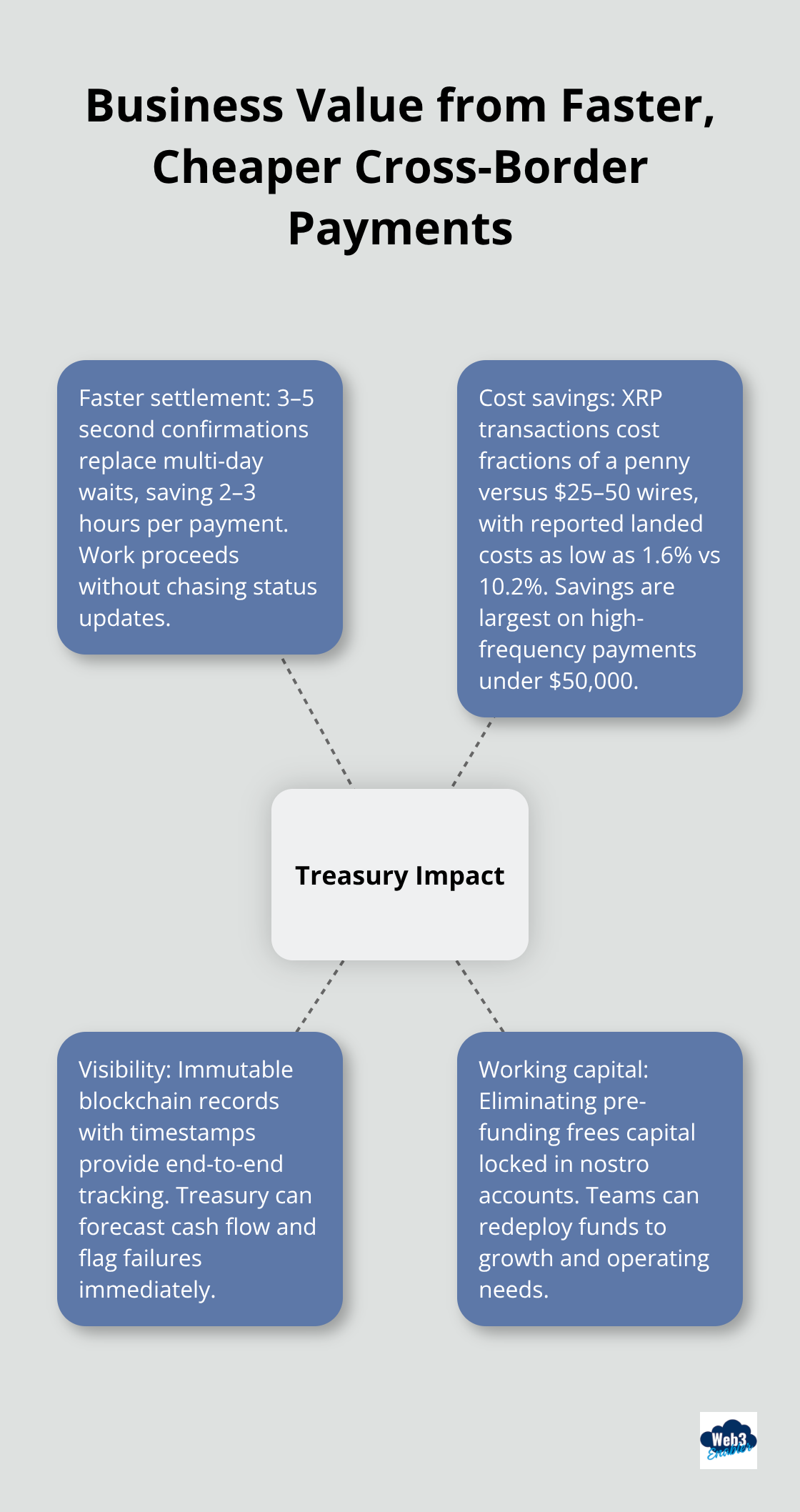

Finance teams waste 2-3 hours per international payment when they track SWIFT transfers through correspondent banks. Ripple’s 3-5 second settlement eliminates this administrative burden entirely and frees treasury staff for strategic work instead of payment reconciliation. Companies that process 100+ monthly international payments save 200-300 hours annually when they switch from SWIFT’s multi-day settlement to instant blockchain confirmation.

The 24/7 operation means payments complete outside standard hours and removes the Friday afternoon cutoff that delays urgent vendor payments until Monday.

Cost Savings Reach 85% for High-Volume Corridors

Businesses that send frequent payments under $50,000 see dramatic cost reductions with Ripple versus SWIFT. Traditional wire transfers cost $25-50 per transaction plus correspondent bank fees, while XRP transactions cost fractions of a penny. Companies like SBI Remit report significant cost reductions when they use On-Demand Liquidity instead of correspondent banks, with industry targets to reduce transaction costs to less than 3% by 2030. The elimination of nostro account pre-funding frees working capital that banks previously locked in foreign accounts (which improves cash flow management for multinational operations).

Real-Time Visibility Beats Opaque SWIFT Messages

SWIFT’s message-based system provides limited visibility once payments enter correspondent bank networks and creates uncertainty for finance teams that manage cash flow. Ripple’s blockchain provides immutable transaction records with precise timestamps and confirmation status, which eliminates the guesswork that plagues traditional international transfers. Treasury managers gain complete payment transparency from initiation to final settlement and can forecast cash flow accurately while they identify failed transactions immediately before these issues impact operations.

Working Capital Optimization Changes Treasury Strategy

Traditional SWIFT payments require banks to maintain nostro accounts across multiple currencies, which ties up billions in idle capital. Ripple’s just-in-time conversion eliminates pre-funding requirements entirely because XRP acts as an instant bridge between any two currencies. Finance teams can redeploy this freed capital for business growth instead of maintaining dormant foreign currency reserves (particularly valuable for companies with seasonal payment patterns or expanding into new markets).

Final Thoughts

The Ripple vs SWIFT debate shows two systems that serve different business needs. SWIFT excels for large-value transactions that require bank guarantees and regulatory certainty, while Ripple dominates high-frequency, low-value payments where speed and cost matter most. SWIFT’s 50-year track record and 11,000 institution network provide unmatched stability for traditional finance operations.

Ripple’s 3-5 second settlement and 85% cost savings transform treasury operations for companies that process frequent international payments under $50,000. The future belongs to hybrid strategies where large enterprises use SWIFT for million-dollar transactions and Ripple for operational payments like vendor disbursements and remittances. This dual approach maximizes both security and efficiency (particularly for multinational corporations with diverse payment needs).

Smart treasury teams evaluate payment volumes, transaction sizes, and regulatory requirements when they choose systems. Companies ready to modernize their payment infrastructure can explore blockchain payment solutions that connect traditional finance with digital payment networks. The cross-border payments market will continue to evolve as both systems adapt to business demands and regulatory landscapes.