Your business moves at the speed of digital commerce, but your cross-border payments still operate like they’re stuck in the 1990s. International stablecoin payments are changing that reality, offering financial leaders a way to settle transactions in minutes instead of days.

At Web3 Enabler, we’ve seen firsthand how organizations are leveraging stablecoins to cut costs and accelerate cash flow across borders. This guide walks you through the opportunity and how to implement it in your organization.

Why Stablecoins Beat Traditional Cross-Border Payments

Traditional wire transfers cost between $25 and $50 per transaction, plus foreign exchange markups that consume another 1–2% of the amount transferred. A $100,000 payment across borders loses roughly $3,000 to fees and conversion spreads before it arrives. That payment then sits in the correspondent banking system for 3–5 business days. The Bank for International Settlements confirms that cross-border B2B payments still rely on legacy SWIFT infrastructure designed for a different era. Stablecoins eliminate this friction. A stablecoin payment settles in minutes on blockchain networks like Ethereum or BASE, moving directly without intermediary banks. The cost difference is striking: on-chain fees on BASE run around 0.5% plus pennies-level transaction costs, reducing your effective fees to less than one-tenth of traditional rails. The global cross-border payment market is valued at USD 303.24 billion in 2025 and is expected to reach USD 552.72 billion by 2033, with blockchain payments representing a growing share of this expansion. That growth accelerates because enterprises see the math immediately-faster settlement means better cash flow, lower operational overhead, and predictable costs.

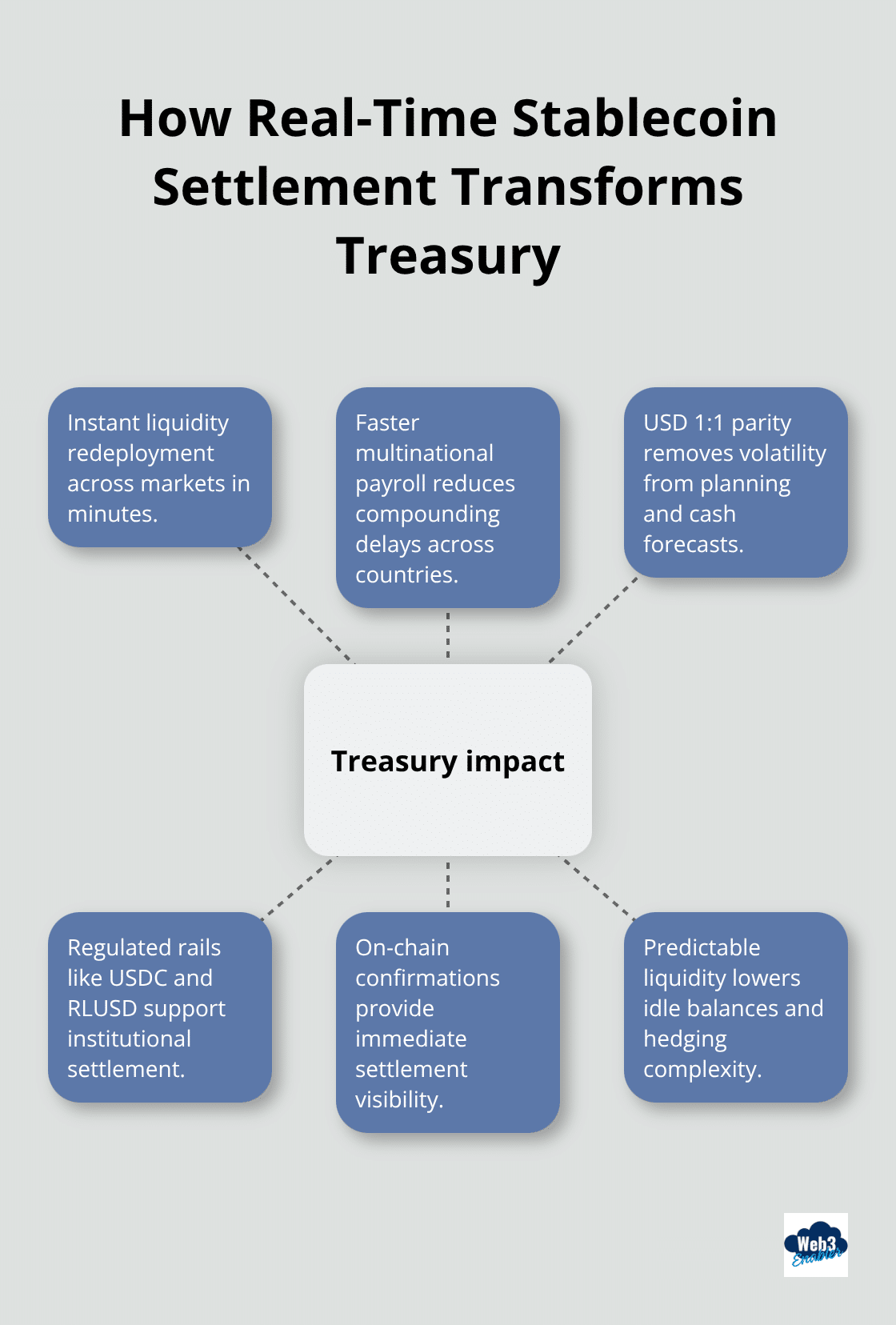

Speed transforms treasury operations

Real-time settlement changes how you manage global liquidity. Instead of waiting days for funds to arrive, your treasury team receives payments in minutes and redeploys capital across markets instantly. This matters especially for multinational payroll operations, where every day of delay compounds across dozens of countries.

Stablecoins maintain 1:1 parity with USD, so you avoid the volatility that derails cross-border planning. Financial institutions from Circle to Ripple build stablecoin rails specifically for this use case, offering regulated settlement options like USDC and RLUSD.

Integration with your existing workflows

Web3 Enabler integrates stablecoin rails directly into Salesforce, allowing your finance team to execute cross-border payments without leaving Revenue Cloud or Financial Services Cloud. The compliance layer sits within your existing workflows, with automated KYC and audit trails that regulators expect. Organizations that move first capture the advantage: lower costs compound over thousands of transactions annually, and faster settlement unlocks working capital that would otherwise sit idle.

The competitive window narrows

More enterprises test stablecoin corridors and realize the operational gains. Your peers are already evaluating how stablecoins fit into their treasury strategy. The question now is whether your organization implements this capability first or follows the market trend. The next section shows you how to build this into your organization without disrupting existing systems.

How Stablecoins Actually Settle Across Borders

The mechanics of blockchain settlement

Stablecoin settlement operates on a completely different infrastructure than traditional banking. When you initiate a stablecoin payment, the transaction broadcasts to a blockchain network-Ethereum, BASE, or XRP Ledger-where validators confirm it within seconds to minutes. The payment arrives in the recipient’s wallet immediately, with no correspondent banks involved. This matters because traditional SWIFT transfers move through 4–6 intermediary banks, each adding processing delays and fees. A $500,000 international payment that settles in minutes with stablecoins versus 3–5 business days with wire transfer, and your treasury team sees the confirmation on-chain in real time.

Why institutions trust stablecoin corridors

Regulators and financial institutions recognize this advantage. Circle’s USDC and Ripple’s RLUSD now operate in institutional corridors specifically because they eliminate settlement friction. The cost structure reveals why enterprises move quickly. Traditional wire transfers charge $25–$50 per transaction plus 1–2% foreign exchange markups. Stablecoin payments on blockchain cost roughly 0.5% plus pennies in on-chain fees, cutting your effective cost to less than one-tenth of wire transfer pricing. For a company executing 500 cross-border payments monthly, this difference compounds to $150,000–$200,000 in annual savings.

How blockchain architecture removes intermediaries

Stablecoins work because blockchain networks don’t need intermediaries to verify account ownership or manage liquidity reserves across borders. Your payment moves peer-to-peer, with the blockchain itself providing the settlement guarantee. This architectural advantage transforms treasury operations. Instead of waiting days for international payments to clear, your finance team redeploys capital instantly across markets, improving cash flow and reducing idle balances.

Real-time visibility and liquidity management

Real-time visibility into on-chain transactions means your treasury can track payment status to the second, eliminating the uncertainty of traditional banking where funds disappear into the correspondent system for days. For multinational organizations managing payroll across 20+ countries, this speed advantage is material-employees receive funds faster, and your finance team reduces operational overhead managing multiple currency corridors and banking relationships. Liquidity management becomes predictable because stablecoins maintain 1:1 parity with USD, eliminating the volatility that creates hedging complexity in cross-border operations.

Gaining structural advantage through early implementation

Organizations that implement stablecoin corridors first gain a structural advantage: lower costs per transaction, faster working capital deployment, and simplified compliance because blockchain transactions create permanent, auditable records that regulators expect. Web3 Enabler integrates these stablecoin rails directly into Salesforce Revenue Cloud, so your accounting team records transactions and reconciles payments without switching systems. The next section shows you how to navigate the compliance and regulatory requirements that protect your organization while you capture these operational gains.

Building Your Stablecoin Implementation Strategy

Start with Salesforce as your control center

Stablecoin payments integrate directly into your existing Salesforce environment without requiring system replacements. Your finance team records transactions in Revenue Cloud, Financial Services Cloud, or Commerce Cloud the same way they always have. Compliance teams maintain audit trails automatically, and treasury teams gain real-time visibility into settlement without switching platforms. Increasingly, financial institutions are expected to demonstrate that blockchain transactions receive the same rigor as traditional payments, which means your Salesforce audit trail becomes your regulatory defense.

Web3 Enabler operates as a native application on the Salesforce AppExchange, eliminating friction that third-party crypto gateways introduce. This approach saves your IT team months of custom integration work and prevents stablecoin payments from becoming a separate shadow system that compliance cannot monitor effectively.

Execute a narrow pilot before scaling

Your implementation roadmap should start specific rather than attempting a company-wide stablecoin overhaul immediately. Select a single corridor: perhaps a recurring supplier payment in a high-cost geography or a cross-border payroll run to one country. Execute that payment in stablecoins, measure the actual cost savings against your baseline wire transfer expenses, and document the time to settlement. Cross-border payments often deliver meaningful savings once you factor in FX markups and intermediary fees.

Run that pilot for three to six months, then expand to a second corridor while you build internal confidence and train your teams on the mechanics. This measured approach prevents chaos that comes from implementing a new payment rail across 50 countries simultaneously.

Embed compliance into your workflow from day one

Regulatory compliance sits at the core of your implementation, not as an afterthought. Standards require that you conduct KYC on counterparties, maintain transaction records for seven years, and verify that your stablecoin provider maintains adequate reserves. Circle and Ripple, major institutional stablecoin issuers, both publish regular attestations of their reserves and maintain compliance frameworks that satisfy institutional requirements.

Your Salesforce implementation should automate KYC verification when payments initiate, creating an audit trail that regulators expect. This integration ensures your compliance team sees every transaction recorded within Salesforce with full auditability.

Expand systematically across corridors

Once your teams execute three to five successful corridors and your finance team confirms the cost savings, expand to your entire supplier base in those geographies. This systematic expansion builds organizational confidence and demonstrates measurable ROI before you commit resources to additional regions. Each successful corridor creates internal advocates who champion stablecoin adoption to other departments.

Final Thoughts

Organizations that move first on international stablecoin payments capture a structural advantage that compounds over time. A company executing 500 cross-border payments monthly saves $150,000 to $200,000 annually by switching from wire transfers to stablecoin corridors, and faster settlement means your treasury team redeploys capital instantly instead of waiting days for funds to arrive. Your competitors are evaluating this capability right now, so the question is whether you implement it before they do or spend the next two years catching up while they extract millions in cost savings.

Your implementation path remains straightforward: start with Salesforce as your control center, execute a narrow pilot on a single high-cost corridor, measure the actual savings, and expand systematically as your teams build confidence. Regulatory clarity around stablecoins continues to improve, reducing implementation risk for enterprises that move now, and Circle and Ripple operate institutional corridors with transparent reserve attestations that satisfy regulatory requirements. Your finance team gains real-time visibility into settlement, your accounting team records transactions without switching systems, and your compliance team maintains the audit trails that regulators expect.

Web3 Enabler integrates stablecoin rails directly into Salesforce as a native application on the AppExchange, eliminating the integration friction that third-party gateways introduce. Your teams execute international stablecoin payments within Revenue Cloud, Financial Services Cloud, or Commerce Cloud without leaving your existing environment. The competitive window narrows as more enterprises recognize the operational gains, so your next step is selecting that first corridor and executing your pilot.