Receiving US ACH payments in Mexico is impossible, because only the US Banking System operates with ACH. A SWIFT transfer involves navigating multiple banking systems, currency conversion, and strict compliance requirements. Most companies struggle with the complexity of routing payments through correspondent banks, managing exchange rates, and reconciling transactions across borders. But what if you could get an ACH deposited directly in Mexico? Blockchain Payments with stablecoins makes that possible.

At Web3 Enabler, we’ve help businesses streamline this process by mapping ACH transfers into stablecoins, and then back into fiat via local Mexican rails like SPEI… while maintaining full regulatory compliance. This guide covers the practical routes, costs, timelines, and tools you need to move money efficiently from the US to your Mexican operations.

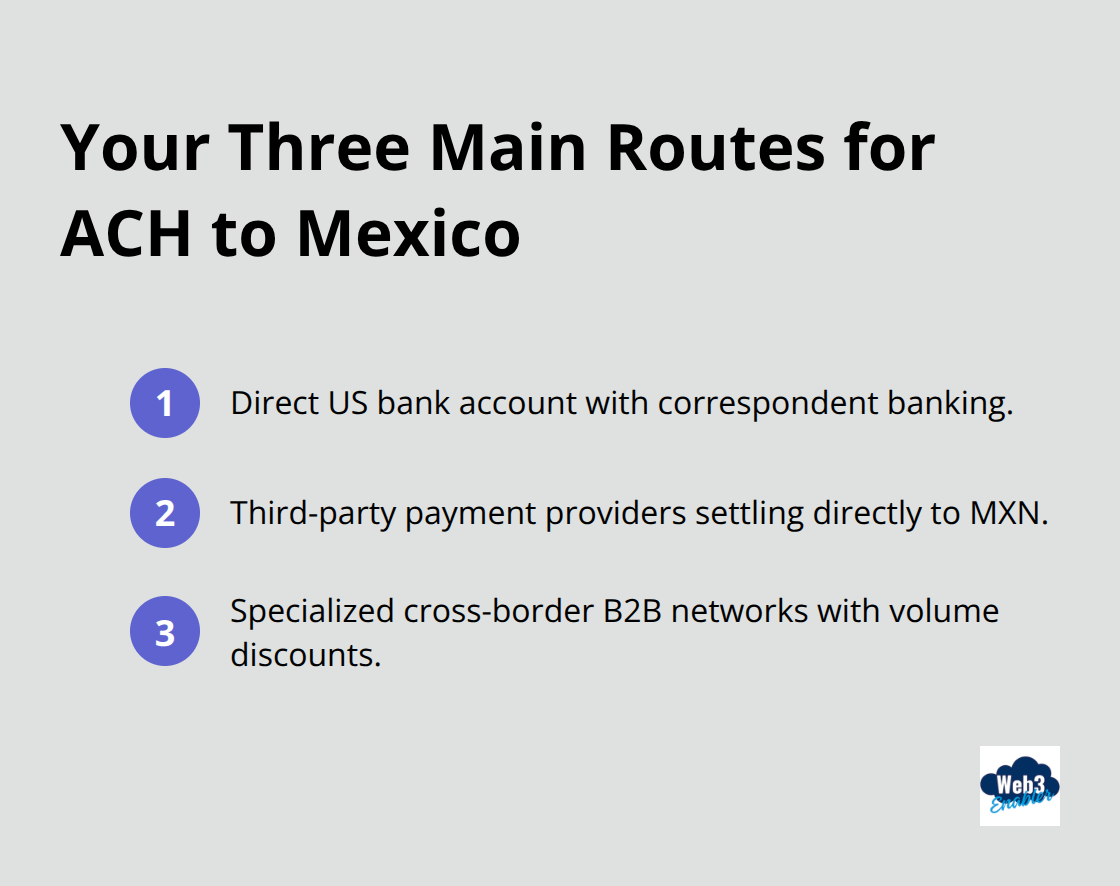

Getting Money Into Mexico: Your Three Main Routes

Direct US Bank Accounts and Correspondent Banking

Maintaining a US bank account tied to your Mexican entity or operations offers the most straightforward path for receiving US ACH payments, but it’s really complicated. When a US payer initiates an ACH transfer to your US account number and routing number, funds clear within one to two business days through the Federal Reserve’s ACH network. You then move the money to Mexico through your bank’s foreign exchange and international wire services. With Blockchain Payments’s Virtual On-Ramps, your client creates a virtual bank account that is tied to them in the United States, and you have a Liquidation Wallet connected to your bank account in Mexico. The ACH payment is used to buy stablecoins, which are sent to your liquidation wallet, and liquidated for Mexican Pesos, all without managing stablecoins.

This approach gives you full control and transparency, with everything staying within the US banking system and the Mexican banking system, with the routing between them via stablecoins. Correspondent banking fees typically run between 15 and 50 USD per transaction, depending on your bank relationship. Major US banks like JPMorgan Chase and Bank of America handle these transfers routinely, and the compliance trail remains clean because the transaction stays within national infrastructure.

The downside is clear: you pay for maintaining US infrastructure, and if your Mexican operations need immediate local currency, you absorb FX conversion costs at your US bank’s rates (typically 1.5 to 3 percent markup above interbank rates). This structure works well for companies that can tolerate a two- to three-day settlement cycle and don’t mind the markup on currency conversion.

Third-Party Payment Providers, Easy but Expensive

Payment providers like Stripe offer an alternative that can reduce friction and costs. Stripe supports payments across Mexico with options including SPEI bank transfers and local methods like OXXO vouchers, and it can receive US ACH on your behalf while settling directly into your Mexican bank account. The unified dashboard lets you view all payments by method in one place and toggle payment types on or off without coding.

These providers typically charge transaction fees ranging from 1.5 to 3 percent plus fixed per-transaction fees, which compounds for high-volume operations. The real advantage is speed: instead of waiting for a US-to-Mexico wire conversion cycle, you receive settlement into your local Mexican bank account within 24 hours in many cases. The compliance burden shifts partially to the provider, though you remain responsible for KYC documentation and AML monitoring on your end.

Specialized Cross-Border Networks

Specialized cross-border payment networks designed for B2B transfers often provide better rates for regular ACH inflows, sometimes as low as 0.5 percent plus a flat fee. These networks require integration work and higher minimum volumes, but they deliver faster settlement than traditional correspondent banking. The tradeoff is losing direct control over the banking relationship and accepting a middleman’s fee structure-a cost that matters less if you process dozens of transactions weekly but becomes painful if you move large lump sums occasionally.

Each route carries different compliance responsibilities and cost profiles. Your choice depends on transaction volume, settlement speed requirements, and how much control you want over the banking relationship. Understanding these three paths sets the stage for the next critical decision: how you’ll handle currency conversion and manage the timing and fees involved in moving dollars to pesos.

Converting Dollars to Pesos: Rates, Timing, and Real Costs

Exchange Rate Markups and Real Money Loss

Exchange rates and processing timelines determine where most companies lose money on cross-border ACH transfers to Mexico. The interbank USD to MXN rate fluctuates constantly-currently hovering around 17 to 18 pesos per dollar depending on market conditions-but your bank or payment provider won’t offer you that rate. US banks typically add a markup of 1.5 to 3 percent on top of the interbank rate, meaning you lose roughly 255 to 510 pesos on every 10,000 USD transferred. Payment providers like Stripe charge similar markups but sometimes offset this with faster settlement, moving funds into your Mexican account within 24 hours instead of waiting three to five days for a traditional wire conversion cycle.

If you process 20 ACH transfers monthly at 5,000 USD each, that 2 percent markup costs you 20,000 pesos monthly-240,000 pesos annually-money that vanishes simply because you don’t shop rates. The real problem is timing: ACH transfers from the US clear within one to two business days, but your bank may hold the conversion for another day or two, exposing you to FX movement. If the peso weakens by even 0.5 percent during that window, you lose another 250 pesos per 10,000 USD.

Processing Timelines Across Routes

Processing timelines vary dramatically depending on your route. A direct US bank account with correspondent banking takes three to five business days total: one to two days for ACH clearing, then another one to three days for the international wire and FX conversion. Third-party payment providers compress this to 24 to 48 hours by batching transfers and handling FX conversion in-house, though you sacrifice some control over the exact rate you receive. Specialized cross-border networks designed for B2B volume can settle even faster-sometimes same-day or next-day-but require higher transaction minimums and ongoing relationship management.

Fee Structures and Total Cost Comparison

Stablecoins make this much cheaper. With stablecoins, the on-ramping and off-ramping fees are 20-50 basis points, or 0.2% to 0.5%. The off-ramping fee in Mexico include the implicit exchange rate. Without the banking monopoly on your FX, the blockchain liquidity pools are much cheaper. Your transfer will usually cost under 1% and take less than a day for the on-ramp or off-ramp process. If your company does business in crypto, you can cut the fees in half by only off-ramping as needed. But even companies operating entirely in fiat benefit.

Contrast that with the traditional banking rails.

Fee structures are the final piece of the cost equation. Correspondent banking runs 15 to 50 USD per transaction plus the FX markup; payment providers charge 1.5 to 3 percent plus fixed fees ranging from 0.50 to 2 USD per transaction; cross-border networks often undercut both at 0.5 to 1.5 percent plus flat fees if you hit volume thresholds. For a 50,000 USD transfer, correspondent banking costs roughly 1,000 to 1,500 USD in fees and FX loss. The same transfer through a payment provider might cost 750 to 1,500 USD. Through a volume-discounted cross-border network, you could pay as little as 250 to 500 USD-but only if you process enough monthly volume to qualify.

Know Your Customer Rules and What Mexico Actually Requires

Mexican financial institutions require you to complete KYC verification before you receive regular cross-border ACH transfers, especially if those transfers exceed 10,000 USD monthly or represent ongoing business relationships. Banks in Mexico face penalties from CNBV, the Mexican banking regulator, if they accept transfers from unverified sources. When you open a Mexican bank account to receive US ACH payments, you must provide corporate documentation including your RFC tax ID, articles of incorporation, beneficial ownership declarations, and proof of business address. For individuals receiving payments, Mexican banks require government-issued ID, proof of address, and increasingly, source-of-funds documentation showing where the US ACH transfers originate.

The critical mistake companies make is treating KYC as a one-time event. Mexican regulations require you to refresh your documentation every two to three years or whenever your business structure changes. If your US ACH payer changes or you add new payment sources, inform your Mexican bank immediately. The FinCEN Southwest Border Geographic Targeting Order, effective March 7, 2026 through September 2, 2026, expands this requirement for Money Services Businesses in designated Arizona, California, New Mexico, and Texas counties. If you operate a payment service or remittance business in those areas, you must file Currency Transaction Reports for cash transactions between 1,000 and 10,000 USD within 30 days and verify customer identity consistent with federal regulations. New businesses in the expanded geographic scope have until April 6, 2026 to begin filing.

Mapping ACH to SPEI and Building Your Compliance Trail

The moment your US payment lands in your Mexican crypto wallet in USDC or USDC, your liquidation wallet sells your new stablecoins for Pesos. Those Pesos are transferred to your bank account via SPEI. SPEI, Mexico’s real-time electronic interbank transfer system, operates exclusively in MXN, so you must convert before you move money through SPEI rails. For compliance, Blockchain Payments tracks each movement. You track the client payment to their Virtual On-ramp, the transfer to your Wallet, and the transfer to your bank account. Your accounting department can choose how to account for the implicit transaction fees which are all clearly documented in the flow.

Documentation Standards That Prevent Problems Later

AML compliance requires you to document the entire chain from US payer to Mexican receipt. Blockchain Payments makes that easy. Your KYC information is in Salesforce, your CRM. The Virtual On-ramp, USD ACH, is titled to your client, with a reference stored in your Salesforce CRM. You only take possession when the money is in Mexico, elimianting the cross-border tracking. You have a clearly documented and KYC’d chain of custody.

Final Thoughts

Receiving USD to Mexico via the traditional banking system works smoothly only when your finance team tracks every dollar from US origination through Mexican settlement and into your local accounting records. Manual reconciliation across US bank statements, Mexican bank confirmations, and SPEI transaction logs creates delays and errors that compound monthly. Your team wastes hours matching transactions instead of analyzing cash flow or managing liquidity.

Stablecoins and Blockchain Payments eliminates the reconciliation bottleneck entirely. Instead of your team manually reviewing bank statements and creating spreadsheet matches, a system automatically reconciles ACH receipts, USDC stable coins, and Mexican settlement. You set the variance you accept to mark things as paid. Real-time visibility into cross-border transactions means your finance team sees cash position updates within seconds instead of days, knows exactly how much USD is pending conversion, and understands where funds sit in the SPEI system.

Web3 Enabler integrates blockchain-powered payments and settlement directly into Salesforce, giving you real-time visibility into on-chain transactions and automated reconciliation for faster settlement and reduced operational risk. For organizations managing cross-border ACH flows into Mexico, this approach lets your finance team focus on strategy instead of transaction matching.

FAQ: Receiving US ACH Payments in Mexico

Is it actually possible to receive a US ACH deposit in Mexico?

Technically, the ACH network only operates within the US banking system. However, by using Virtual On-Ramps, a Mexican business can provide a US-based account and routing number to their client. The funds are deposited as a domestic ACH, automatically converted into stablecoins (like USDC), and then settled into a Mexican bank account via SPEI in Pesos—all within 24 hours.

How much can I save using stablecoins compared to a SWIFT wire?

Traditional correspondent banking often charges $15–$50 per wire plus a 1.5% to 3% FX markup. Stablecoin “liquidation wallets” typically reduce these costs to 0.2%–0.5% (20-50 basis points). On a $50,000 transfer, this moves your total cost from roughly $1,250 down to as little as $250.

What are the 2026 compliance requirements for US-Mexico transfers?

As of March 7, 2026, FinCEN has expanded the Southwest Border Geographic Targeting Order. Businesses in designated border counties (across AZ, CA, NM, and TX) must file Currency Transaction Reports for amounts between $1,000 and $10,000. Additionally, Mexican regulators (CNBV) require updated corporate documentation, including your RFC tax ID and beneficial ownership declarations, every 2-3 years.

How long does the ACH-to-SPEI process take?

While a traditional international wire can take 3–5 business days to clear and convert, the blockchain-mapped route is significantly faster. The US ACH clears in 1–2 days, and the subsequent “on-ramp to off-ramp” process usually finishes in under 24 hours, allowing for same-day or next-day liquidity in Mexican Pesos.

Do I need to manage crypto wallets to receive these payments?

No. Modern B2B payment layers act as “invisible” infrastructure. Your client pays via a standard US bank transfer, and you receive Mexican Pesos via SPEI. The stablecoin conversion happens in the background, meaning your accounting team sees standard fiat currency while enjoying the speed and low cost of blockchain rails.