Digital payments are growing faster than ever, and the money-making opportunities are real. The global digital payments market hit $9.04 trillion in 2023, with projections to reach $14.89 trillion by 2030.

Digital payments are growing faster than ever, and the money-making opportunities are real. The global digital payments market hit $9.04 trillion in 2023, with projections to reach $14.89 trillion by 2030.

At Web3 Enabler, we’ve watched businesses unlock serious revenue by tapping into this shift. Whether through transaction fees, subscription models, or blockchain-based solutions, there are multiple ways to profit from how people pay today.

The Numbers Behind Digital Payment Growth

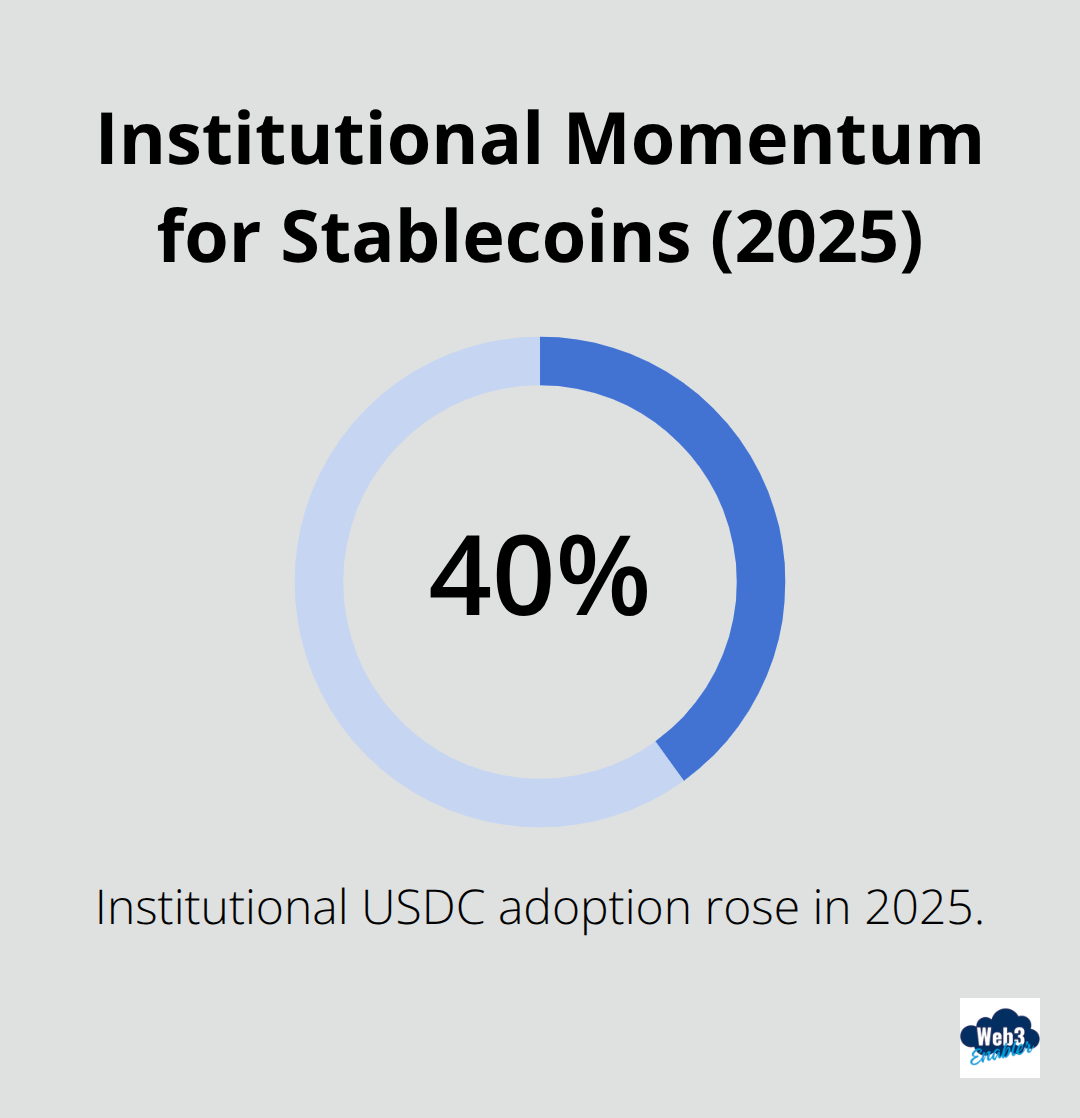

The digital payments market isn’t just growing-it’s reshaping how money moves. The sector is expected to reach USD 3.12 trillion in 2025 and grow at a CAGR of 11.29% to reach USD 5.34 trillion by 2030. This growth creates real opportunities for businesses willing to capture them. Cross-border payments accelerate faster than domestic ones, with blockchain-based solutions processing transactions at speeds traditional banking cannot match. Visa’s pilot with Solana handled 24,000 transactions per second, proving that the infrastructure exists today to handle massive payment volumes. Meanwhile, stablecoin adoption climbs steadily-Circle reported that institutional USDC adoption rose about 40 percent in 2025, signaling serious money flowing into blockchain rails. The real opportunity lies not in competing with legacy systems, but in capturing the segments they’ve neglected or failed to serve efficiently.

Consumer behavior is shifting fast

More than 85 percent of US consumers shopped online in 2025, and they increasingly accept alternative payment methods. Stripe now accepts USDC, Shopify enables USDC checkout, and GrabPay integrated blockchain settlement into its platform. These aren’t experimental features-they’re production systems handling real transactions. Merchants see tangible benefits: lower fees, faster settlement, and reduced chargebacks. The momentum reflects genuine business value, not hype.

Emerging markets show the biggest wins

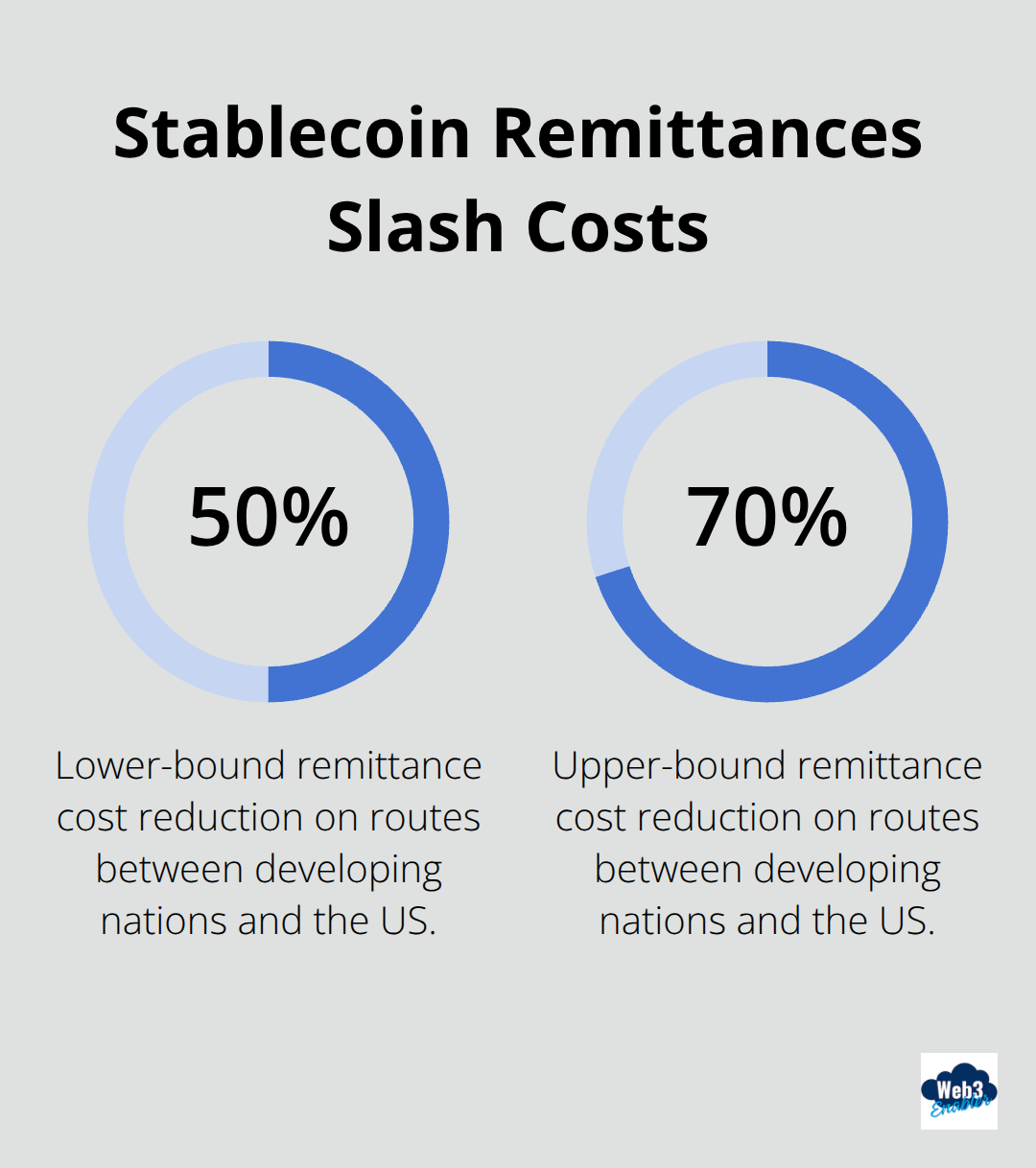

In developing nations, blockchain payments solve problems that traditional systems created. Remittance corridors that previously took days now settle in minutes using stablecoins, cutting costs by 50 to 70 percent on routes between developing nations and the US. Workers send money home faster. Families receive funds without waiting. Costs drop dramatically. This isn’t theoretical-it’s happening right now across Africa, Southeast Asia, and Latin America.

Why adoption accelerates when friction drops

The shift away from traditional methods isn’t driven by ideology; it’s driven by friction reduction. When a payment method costs less and arrives faster, adoption follows naturally. Institutional players like Visa and Revolut wouldn’t integrate blockchain if the revenue opportunity didn’t exist. They test, measure, and scale what works. Their integration signals that blockchain payments have moved from experimental to essential.

The infrastructure is ready for scale

Ethereum and its 2.0 upgrade deliver up to 100,000 transactions per second with a 99.5 percent drop in energy use, supporting large-scale payment deployments. Solana’s Proof of History adds cryptographic timestamps to transactions, increasing throughput and reducing latency for high-volume payments. These aren’t theoretical improvements-they’re live networks processing billions in value daily. The technical foundation exists. The merchant adoption exists. The consumer comfort exists. What remains is capturing the revenue streams these systems create.

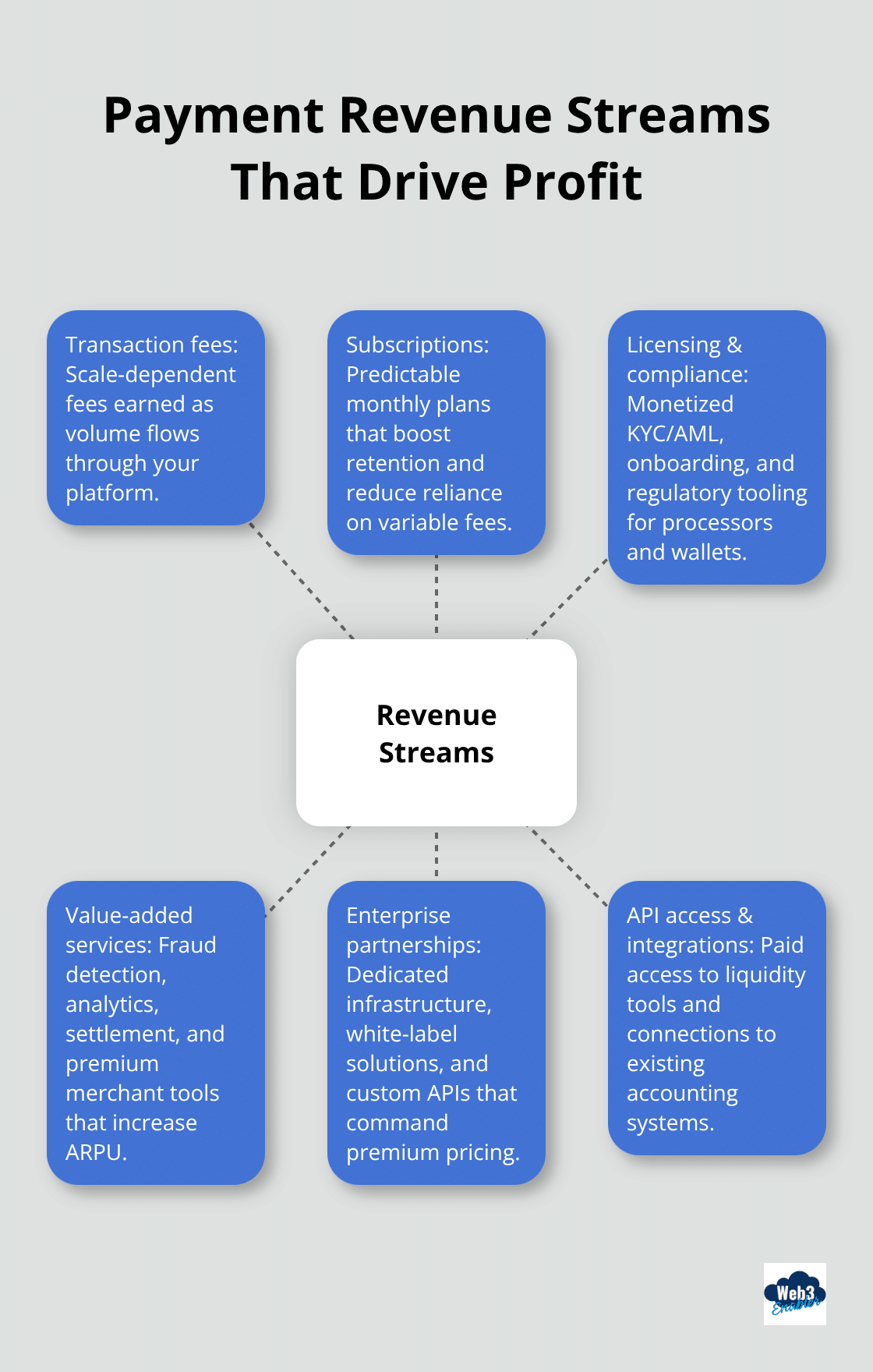

How Payment Businesses Actually Make Money

The infrastructure for digital payments exists, but the real question is how to extract revenue from it. Transaction fees remain the most straightforward model, but they’re not the only path. Transaction-based monetization works at scale when volume flows through your platform, as demonstrated by the highest-volume DEXs in the market generating massive fee revenue. However, relying solely on transaction fees creates vulnerability. Aave and Compound together generated over 500 million dollars in protocol fees in 2025, but they achieved this by layering multiple revenue streams.

The most successful payment businesses combine transaction fees with subscription models, licensing arrangements, and value-added services that merchants and enterprises actually pay for. Stripe’s acceptance of USDC and Shopify’s USDC checkout aren’t free features-they’re monetized through payment processing cuts, subscription tiers, and premium merchant tools. The key insight is that payment volume alone doesn’t guarantee profit. You need customers willing to pay for convenience, compliance, security, or speed beyond the basic transaction itself.

Subscription models beat per-transaction dependency

Merchants hate surprise fees. Subscription pricing creates predictability, which enterprises demand. A business paying 99 dollars monthly for payment processing tools with unlimited transactions at a fixed 1.5 percent fee knows exactly what it costs. This beats variable models where costs fluctuate with volume. OpenSea and Blur combined processed over 10 billion dollars in sales during the first half of 2025, but their real revenue came from subscription memberships, premium features, and listing tiers-not just transaction volume. You can layer subscription tiers: basic plans for startups at 29 dollars monthly, professional plans for mid-market at 199 dollars monthly, and enterprise deals with custom pricing and dedicated support. The subscription approach also improves customer retention because switching costs rise once merchants integrate your tools into their operations and staff training happens. Compliance and security features justify premium tiers better than speed alone, since regulatory requirements vary by jurisdiction and merchant size.

Cross-selling and bundled services drive real margins

Payment processing alone operates on thin margins. Bundling compliance tools, fraud detection, analytics dashboards, and settlement services into your platform multiplies revenue per customer. Notabene’s compliance platform cut onboarding times by roughly 50 percent in 2025, and they monetized this through licensing fees to payment processors and wallet providers. You’re not selling transactions-you’re selling operational efficiency. A merchant using your payment infrastructure needs wallet integration, customer KYC verification, transaction reporting for accounting systems, and tax compliance tools. Each adds 10 to 50 dollars monthly to the base subscription. Enterprise customers with multi-currency operations or cross-border B2B requirements pay significantly more for features like real-time liquidity pools, settlement optimization, and API access to integrate with their existing accounting software. The businesses winning this market aren’t competing on processing fees-they’re competing on total cost of ownership and ease of integration.

Enterprise partnerships unlock premium pricing

Large financial institutions and payment networks don’t negotiate on transaction fees alone. They negotiate on integration speed, regulatory compliance, and operational reliability. RippleNet demonstrates this model: an initial investment of 1 million dollars, partnerships with 300-plus financial institutions, and ROI around 18 months generated revenue exceeding 100 million dollars by 2025. Enterprise customers pay for dedicated infrastructure, white-label solutions, and custom API implementations that fit their existing systems. When you position your payment solution as a compliance and operational tool rather than just a transaction processor, you unlock pricing power that transaction fees alone cannot deliver.

Where Stablecoins and Blockchain Actually Win

Stablecoin payments demolish traditional cross-border transfer economics. A remittance from the US to the Philippines using SWIFT costs 15 to 30 dollars and takes 3 to 5 business days. The same transfer using USDC settles in minutes for under 2 dollars. This isn’t marginal improvement-it’s the difference between a worker keeping 85 percent of their paycheck or 70 percent. Circle reported institutional USDC adoption rose 40 percent in 2025, and that momentum reflects hard numbers, not speculation. Remittance corridors between developing nations and the US saw cost reductions of 50 to 70 percent when stablecoins replaced traditional rails.

For businesses, the math proves equally brutal. Suppliers in Southeast Asia demanding payment within 30 days now receive settlement in 2 hours using stablecoins on Layer 2 networks. Working capital improves immediately. Cash conversion cycles compress. Companies like Stripe and Shopify monetize this efficiency by charging merchants a processing fee of 1.5 to 2 percent for USDC checkout-lower than card processing at 2.9 percent plus interchange-while capturing volume from merchants willing to accept faster settlement over traditional methods.

Speed Transforms Operations Faster Than Cost Alone

Settlement speed matters more than most payment processors acknowledge. A marketplace processing vendor payouts across 15 countries using traditional banking handles settlement delays, currency conversions, and stuck funds in limbo accounts. Blockchain-based settlement using stablecoins eliminates this friction entirely. GrabPay integrated blockchain settlement into its platform, and the operational simplification alone reduced payment processing infrastructure costs. For payroll operations handling global teams, near-instant wallet deposits beat delayed direct deposits across time zones.

Institutional adoption accelerates when speed translates directly to operational efficiency rather than just cost savings. The EU’s MiCA regulation went live in 2025, providing harmonized rules for token issuance and trading that facilitate institutional participation in digital payments. This regulatory clarity opened enterprise treasury departments to stablecoin settlement for intra-group transfers and supplier payments. Companies now justify blockchain payment adoption to compliance teams and CFOs because the regulatory framework exists. Visa’s Solana pilot processed 24,000 transactions per second-the real story isn’t throughput, but that tier-one payment networks validated the infrastructure as production-ready.

Underbanked Markets Represent Genuine Revenue Opportunities

Sub-Saharan Africa has 600 million people with mobile phones but no bank accounts. Southeast Asia has 1.2 billion people where traditional banking remains inaccessible to half the population. These aren’t niche markets-they’re massive addressable customer bases with real purchasing power. Mobile money operators in Africa and Southeast Asia already process trillions in transactions annually, and blockchain provides a path to international settlement without correspondent banking fees.

A worker in Nigeria sending money to London via traditional channels loses 10 to 15 percent to intermediaries. Stablecoin transfers cost under 1 percent. The difference compounds across millions of transactions. Businesses targeting these segments don’t compete on transaction fees with established payment networks-they compete on accessibility. A payment solution that works on feature phones with offline transaction capability captures markets that card networks never reached.

Transak serves as a bridge between traditional money and blockchain settlement, handling compliance and local rails for seamless checkout. The monetization model here differs from developed markets: you charge merchants a percentage of transaction volume, but that volume comes from merchants previously excluded from digital payment infrastructure entirely. Platform marketplaces serving developing economies-from freelance platforms to e-commerce sites-generate revenue by offering blockchain payment rails that traditional processors refused to support.

Real Revenue Flows From Capturing Neglected Segments

The real revenue opportunity lies in capturing the merchants and enterprises that traditional payment networks failed to serve efficiently. Businesses with high-volume cross-border operations, gig economy platforms needing global payouts, and suppliers dependent on tight cash flow margins see blockchain payments not as experimental but as mandatory for competitive survival. These segments represent genuine monetization paths because they face real friction that traditional systems cannot solve cost-effectively.

Final Thoughts

The path to making money from digital payments isn’t theoretical anymore. The infrastructure exists, merchants are adopting it, and revenue models prove themselves in production systems. Transaction fees work at scale, subscription pricing creates the predictability that enterprises demand, and bundled services multiply margins per customer. Stablecoins have already reduced remittance costs by 50 to 70 percent in developing markets, and institutional adoption of USDC climbed 40 percent in 2025.

The businesses winning this space compete on total operational efficiency rather than transaction speed alone. They solve compliance headaches, reduce settlement complexity, and capture merchants that traditional payment networks abandoned. Enterprise partnerships unlock premium pricing that transaction fees cannot deliver, while underbanked markets represent genuine revenue opportunities because they’ve never had access to efficient payment infrastructure. Your strategic position depends on choosing the right segment-cross-border B2B payments, gig economy platforms, marketplace vendor payouts, and emerging market e-commerce all represent different revenue opportunities with different monetization models.

The next step involves identifying which segment aligns with your existing customer base and operational strengths. Build for the merchants and enterprises that traditional systems failed to serve efficiently, layer multiple revenue streams rather than relying on transaction fees alone, and prioritize compliance and security features that justify premium pricing. Web3 Enabler helps businesses connect blockchain technology with existing corporate infrastructure through Salesforce Native solutions that support payments, compliance, and automation.