Your international payments are stuck in the 1990s. Banks are still shuffling money through multiple intermediaries, taking days to settle what should take minutes, and charging fees that would make a loan shark blush.

Stablecoin cross-border payments change that equation entirely. We at Web3 Enabler have watched businesses waste millions on slow transfers when a faster alternative already exists.

Why Banks Love Slow Payments

The 1970s Architecture That Still Runs Your Money

Traditional cross-border payments move at a glacial pace because the system was literally designed in the 1970s. A typical wire takes three to five business days to settle, during which your money sits in limbo across multiple correspondent banks, each one taking a cut and adding delays. When you add everything together, even supposedly low-cost transfers regularly exceed 5% in total cost, and some corridors hit double digits.

Why Your Payment Takes a Tour of the World

Your payment doesn’t go directly to the recipient-it bounces through an average of four to six intermediary banks, each one verifying, processing, and forwarding the funds. Compliance checks happen at nearly every stop, regulatory requirements differ by jurisdiction, and if anything looks slightly unusual, the entire transfer gets flagged and delayed. Banks also have no financial incentive to speed this up; the longer money sits in the system, the more they earn from float.

Stablecoins Blow Up This Model

Stablecoins sidestep this entire architecture. Settlement happens in minutes on networks like TRON or Solana, not days. You pay network fees typically under 1% rather than the hidden FX margins that dominate traditional costs. There are no correspondent banks taking cuts, no compliance delays at intermediaries, and no opaque tracking where you can’t see where your money actually is. The blockchain provides a permanent, verifiable ledger that any auditor can check instantly.

The Real Money Impact

For a multinational company running global payroll, this difference translates to real cash flow improvement-funds reach contractors and employees faster, reducing the working capital gap between when you send payment and when recipients can actually use it. For SMEs competing internationally, lower transfer costs mean better margins on cross-border sales. The math is straightforward: stablecoin transfers on efficient networks cost a fraction of traditional banking, and the money arrives the same day instead of waiting a week for settlement.

This speed and cost advantage isn’t theoretical-it’s what makes stablecoins the practical choice for businesses that actually need their payments to move.

How Stablecoins Actually Move Money Across Borders

Stablecoins operate on a fundamentally different infrastructure than traditional banking, and the difference shows up immediately in your bank account. When you send USDC or USDT across borders, the transaction settles on blockchain networks like Ethereum, Tron, Solana, or Layer 2 solutions such as Polygon and Arbitrum. These networks run 24/7/365, so your payment doesn’t wait for Monday morning or a bank holiday. A contractor in Berlin receives funds in minutes, not the three to five business days that traditional wires demand. The World Bank reported that the average cost of sending a $200 remittance globally was 6.62% in Q1 2025, far above the G20 target of 3% or less.

Stablecoin transfers typically cost 0.5% to 2% total, with most expenses coming from network fees that amount to pennies rather than the FX markups and correspondent bank charges that dominate traditional costs.

For businesses running regular cross-border payroll or supplier payments, this difference compounds quickly. A company paying 50 contractors monthly saves thousands of dollars annually by switching from 5%+ wire fees to sub-2% stablecoin transfers. The transparency matters just as much as the speed. Traditional wires hide their true cost in FX spreads that banks never clearly disclose. Stablecoin fees appear directly on the blockchain, auditable and unchanging. Your accounting team tracks exactly what they paid and when settlement occurred, eliminating the guesswork that comes with opaque banking corridors.

Removing the Intermediary Tax

Traditional cross-border payments pass through four to six correspondent banks, each one extracting value through processing fees, float, and FX markups. Stablecoins eliminate this middleman chain entirely. A payment travels directly from sender to recipient’s wallet in a single transaction, with only network validators processing the transfer rather than institutions designed to profit from delay. This architectural simplicity translates to tangible benefits.

An SME exporting goods to Asia no longer watches their margins shrink from hidden banking costs. A freelancer in Eastern Europe receives their full payment amount without correspondent banks in London, New York, and Singapore each taking a cut. The blockchain provides complete settlement finality within minutes, whereas traditional wires leave money in limbo for days while compliance checks and settlement procedures grind through the system.

Real Speed for Real Business Operations

Minutes versus days sounds like marketing speak until you actually run a payroll cycle. A multinational company paying 200 employees across 15 countries executes the entire operation in a single blockchain transaction rather than orchestrating dozens of separate wires with different cutoff times and settlement windows. Recipients holding stablecoins in regulated custodial wallets can convert to local currency immediately if they prefer, or hold dollars as a hedge against local currency volatility.

For businesses managing inter-company liquidity across time zones, stablecoin transfers eliminate the Friday cutoff problem where weekend transfers become impossible. Treasury teams gain intraday and weekend windows for moving capital, which genuinely matters when managing global cash positions. The immutable ledger creates an audit trail that satisfies corporate governance and regulatory requirements without the manual reconciliation that traditional banking demands.

What Happens Next With Your Payments

The speed and cost advantages only work if you actually implement them. Real-world applications show where stablecoins create the most immediate impact for different business types-and which payment scenarios benefit most from this shift away from traditional banking rails.

Where Stablecoins Actually Create Business Value

Global Payroll: One Transaction, Multiple Countries

Multinational payroll departments waste enormous time coordinating payment runs across dozens of countries and currencies. A company with 300 employees spread across North America, Europe, and Asia traditionally manages this chaos through multiple bank accounts, wire transfers on different cutoff schedules, and settlement windows that span a week or more. Stablecoins collapse this complexity into a single operation. One blockchain transaction sends USDC to contractor wallets across all time zones simultaneously, with settlement confirmed in minutes rather than waiting for each country’s banking system to process the funds.

Traditional remittance costs averaged 6.62% globally, while stablecoin transfers typically cost between 0.5% and 2%. For a company distributing $5 million monthly to global contractors, switching from 5% traditional wire fees to 1% stablecoin costs saves roughly $200,000 annually. Recipients in regulated custodial wallets can hold the stablecoins as dollar-denominated assets or convert to local currency immediately, eliminating the foreign exchange exposure that makes traditional cross-border payroll budgeting unpredictable.

Financial Services and Client Payments

Financial services firms face their own constraints when processing client payments across borders. Correspondent banking chains create delays that frustrate clients and create reconciliation nightmares for compliance teams. Stablecoins enable direct settlement with transparent fees that appear on an immutable ledger, satisfying audit requirements without manual record-matching. The blockchain provides a permanent transaction history that auditors increasingly recognize as more reliable than traditional bank reconciliations.

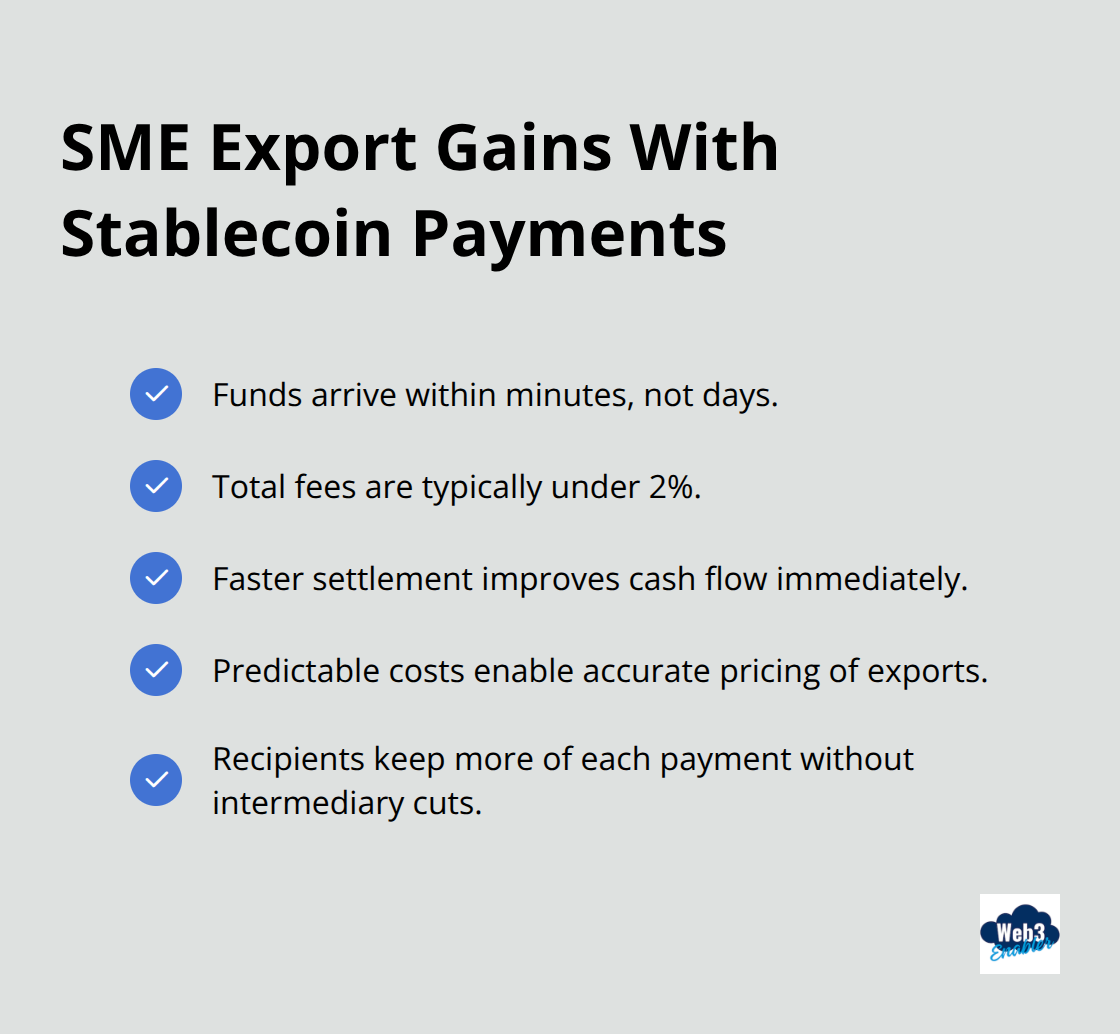

SME Export Economics

SMEs exporting goods internationally face particularly brutal economics with traditional banking. A $100,000 shipment payment arrives after three to five days while sitting in correspondent banks, and the recipient loses 5% or more to hidden FX spreads and processing fees. With stablecoins, that same payment arrives within minutes and costs less than 2% total. The faster receipt of funds improves cash flow immediately, and the predictable costs let small businesses actually price their exports accurately instead of absorbing banking surprises.

Starting Small and Scaling Up

Companies starting with stablecoins should pilot the approach with two to three trusted contractors first, documenting current costs and settlement timelines against traditional methods. This parallel comparison reveals the actual savings without disrupting core payment operations. Integration with accounting systems happens through standard transaction exports and blockchain’s immutable ledger, which auditors increasingly recognize as more reliable than traditional bank reconciliations.

Network Selection for Different Corridors

The choice between networks matters for specific corridors. USDC and USDT operate on Ethereum, Tron, Solana, and Layer 2 solutions like Polygon and Arbitrum, with Tron and Solana typically offering the fastest settlement and lowest fees for high-volume transfers. Try starting with the network that serves your primary payment corridor, then expand to additional networks as your operation scales.

Final Thoughts

Stablecoin cross-border payments work right now for companies that need faster, cheaper international transfers. The shift from correspondent banking to blockchain settlement represents a genuine break from the 1970s infrastructure that still dominates traditional finance. Your money no longer bounces through six intermediaries, sits in limbo for days, or disappears into opaque FX spreads-settlement happens in minutes, costs drop from 5%+ to under 2%, and your accounting team gets an auditable ledger instead of guesswork.

The practical impact compounds across every payment scenario. Multinational payroll departments execute global distributions in a single transaction. SMEs competing internationally keep more margin on cross-border sales. Financial services firms satisfy compliance requirements with transparent, immutable transaction records. Freelancers and contractors receive their full payment amount without correspondent banks extracting value at every step.

Run a pilot with two or three trusted contractors, document your current costs and settlement timelines, and compare results against traditional methods. Most companies discover the savings immediately and expand from there. Web3 Enabler helps businesses connect blockchain technology with existing corporate systems, handling stablecoin cross-border payments, compliance, and automation without requiring you to become a crypto expert.