Your crypto payment workflows need KYC compliance, whether you like it or not. Regulators are cracking down, and one missed verification could expose your business to serious legal trouble.

At Web3 Enabler, we’ve seen too many companies treat blockchain payments like a compliance-free zone. The good news? Building a KYC compliant Salesforce blockchain system isn’t complicated when you know where to start.

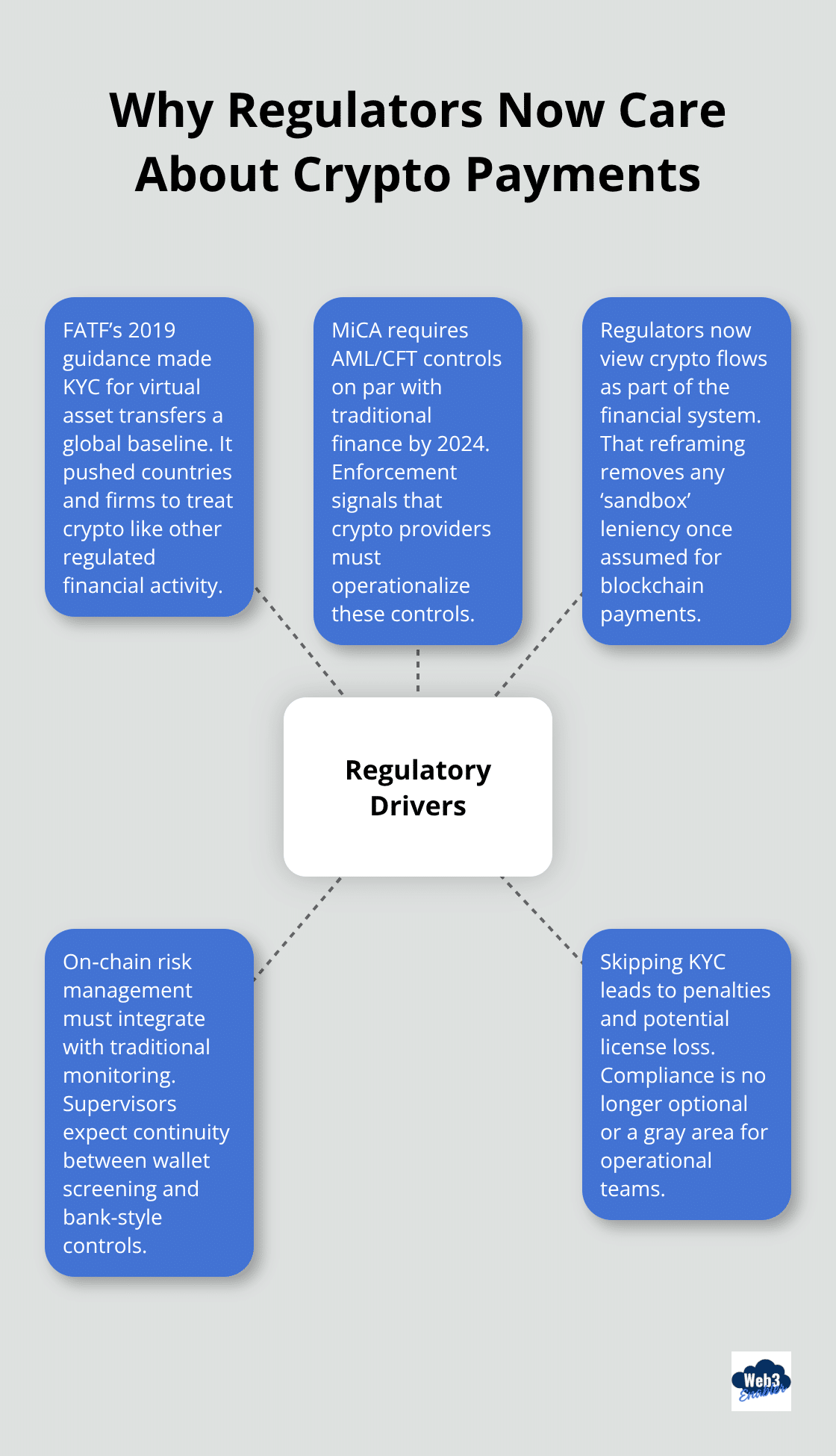

Why Regulators Now Care About Your Crypto Payments

Regulators worldwide have stopped treating crypto payments as a fringe experiment. The Financial Action Task Force, which coordinates anti-money laundering efforts across 200+ jurisdictions, issued binding guidance in 2019 requiring KYC checks for virtual asset transfers. The EU’s Markets in Crypto Assets Regulation mandated that crypto service providers implement AML/CFT controls matching traditional finance by 2024. Governments view crypto flows as part of the financial system, not outside it. MiCA enforcement actions confirm that regulators expect banks, payment service providers, and blockchain platforms to integrate on-chain risk management with traditional monitoring. Skipping KYC isn’t a gray area anymore-it’s a direct path to penalties, license revocation, or worse.

The Real Cost of Missing KYC Checks

Crypto payments without identity verification expose your business to three concrete risks. First, you become liable for moving illicit funds, and regulators don’t care if you “didn’t know.” The Coinbase enforcement action demonstrates that regulators hold institutions accountable for their own controls, regardless of platform promises. Second, your payment partners-banks, card networks, and stablecoin issuers-will cut you off if they detect non-compliant activity upstream. Circle and other stablecoin operators enforce strict KYC requirements and will freeze accounts or block transfers if your source-of-funds checks fail. Third, your customers and partners lose confidence. Institutions funding crypto-enabled card programs or treasury operations through your platform expect auditable compliance records. When you can’t produce them, you lose deals.

How Compliance Becomes Your Competitive Edge

Compliance isn’t just defensive; it’s a competitive advantage. Customers and institutional partners increasingly expect to see clear, auditable proof that their transactions meet regulatory standards. Decentralized KYC approaches using verifiable credentials stored in user wallets reduce breach risk and GDPR exposure compared to centralized PII storage. One-click verification and reusable credentials also dramatically improve onboarding conversion rates because users verify identity once and reuse that credential across platforms. Real-time blockchain intelligence integrated into your workflows lets you demonstrate measurable risk reduction to regulators and partners. When you can show that you screened wallets against sanctions lists, traced on-chain provenance, and documented every decision in an auditable trail, you shift from compliance burden to compliance advantage. Institutions managing crypto-funded programs or stablecoin settlements specifically look for partners who provide this level of transparency and speed.

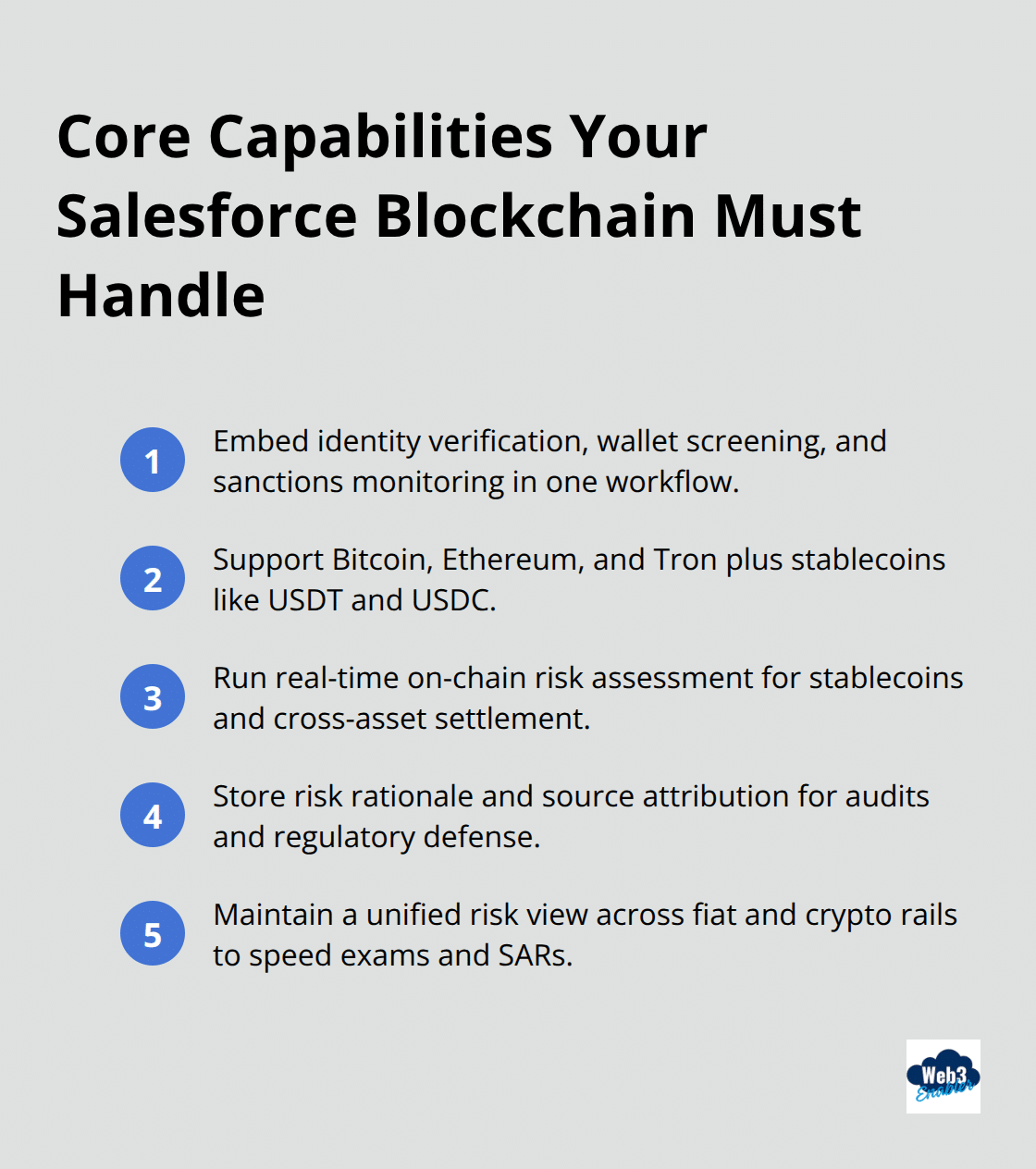

What Your Salesforce Blockchain Needs to Handle

Your payment infrastructure must embed KYC at every transaction point. Verification happens before a single transaction touches the blockchain-not after. This means your Salesforce system needs to connect identity checks, wallet screening, and sanctions monitoring into a single workflow. The integration covers major chains including Bitcoin, Ethereum, and Tron, plus stablecoins like USDT and USDC. Real-time on-chain risk assessment for stablecoins and cross-asset settlement is essential for KYC workflows in crypto-enabled payments and treasury operations. Risk rationale and source attribution must be stored to defend regulatory actions and audits. When you embed blockchain risk intelligence into compliance workflows, you maintain a unified risk view across both fiat and crypto rails. This unified approach supports easier regulatory examinations, audits, and SAR escalation across multi-asset ecosystems. The next section shows exactly how to build this into your Salesforce environment.

Building Your KYC Verification Stack in Salesforce

Connecting KYC tools directly into Salesforce means your compliance workflow lives where your transaction data lives. Wallet screening, sanctions monitoring, and identity verification integrate into the same CRM environment handling payments and customer records. This eliminates the manual handoff between systems and the compliance gaps that come with it.

Embed Screening Into Your Transaction Flow

When a customer initiates a stablecoin payment through your Salesforce interface, the system automatically pulls their wallet address, runs it against OFAC and other sanctions lists in real time, checks their transaction history on Bitcoin and Ethereum for illicit exposure, and surfaces risk signals before you process anything. The integration covers major chains including Bitcoin, Ethereum, and Tron, plus stablecoins USDT and USDC. You configure risk thresholds directly in Salesforce-decide whether to auto-approve low-risk transactions, flag medium-risk activity for manual review, or block high-risk transfers outright. This speed matters. Real-time screening reduces your time-to-detect from days to seconds.

Create Defensible Audit Trails

When regulators or stablecoin operators like Circle audit your controls, you export a complete audit trail showing exactly when verification occurred, what data triggered review, and who approved the transaction. That defensible record separates compliant operations from exposed ones. Configure Salesforce to automatically log every verification decision-timestamp, confidence level, source attribution, and reasoning-so when regulators ask why you approved or blocked a transaction, you have the answer ready. Store compliance records within Salesforce itself, not scattered across spreadsheets or external databases. This unified storage makes regulatory examinations faster and supports easier SAR escalation across multi-asset ecosystems.

Automate Identity Checks Without Bottlenecks

Automation in Salesforce means your KYC checks run instantly without slowing down legitimate transactions. Set up workflows that verify identity attributes using zero-knowledge proofs-you confirm a customer is over 18 or located in an approved jurisdiction without storing their actual passport data. Decentralized KYC approaches using verifiable credentials stored in user wallets reduce both your breach risk and GDPR exposure compared to centralized PII storage. One-click verification and reusable credentials also dramatically improve onboarding conversion rates because users verify identity once and reuse that credential across platforms.

Connect Compliance to Transaction Data

Institutions funding crypto-enabled card programs or treasury operations through your platform expect auditable compliance records tied to transaction data. Salesforce gives you exactly that integration point. When you embed blockchain risk intelligence into compliance workflows, you maintain a unified risk view across both fiat and crypto rails. This unified approach supports easier regulatory examinations, audits, and SAR escalation across multi-asset ecosystems.

The next challenge isn’t building the stack-it’s avoiding the mistakes that trip up most businesses when they first activate these controls.

Where Your KYC Controls Actually Fail

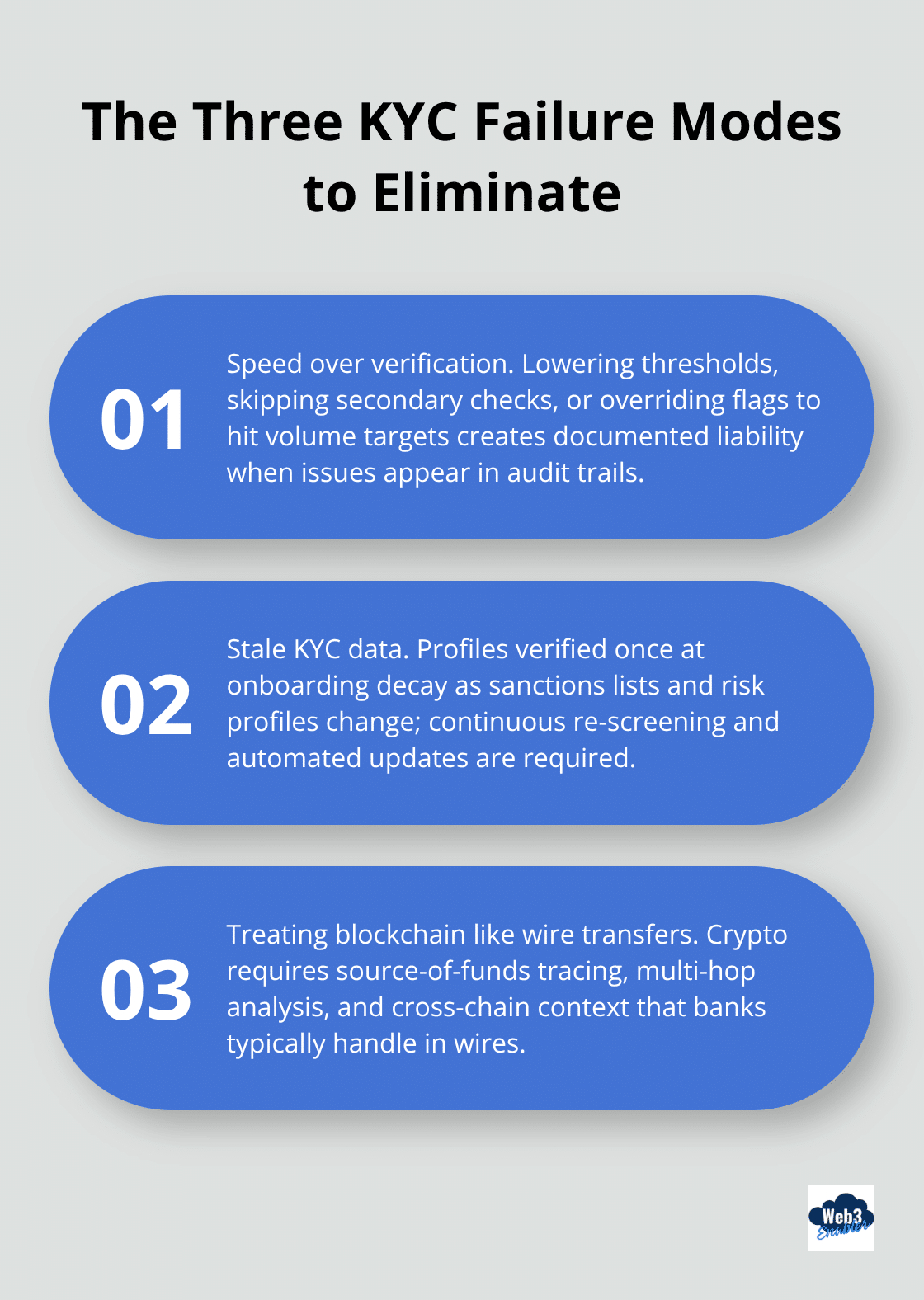

Most businesses install KYC tools and assume they’re protected. Then reality hits. The problem isn’t the technology-it’s how teams use it. We’ve watched compliance teams make the same critical mistakes repeatedly, and they all stem from treating blockchain payments like something they already understand.

Speed Kills Your Compliance Record

The first mistake is treating speed as more important than verification. Teams pressure compliance to approve transactions faster, so they lower risk thresholds, skip secondary checks, or manually override system flags to clear backlogs. MiCA enforcement actions show that regulators don’t care about your transaction volume targets. They care about what you actually verified. When your Salesforce system flags a wallet with sanctions exposure, approving it anyway because it’s a “good customer” creates documented liability. Regulators will find that approval in your audit trail and treat it as willful negligence.

Your KYC Data Rots Without Active Management

The second mistake is assuming your KYC data stays current without active management. Customer profiles get verified once during onboarding, then nobody touches them again. But regulations evolve, sanctions lists update daily, and customer risk profiles change. If a customer’s wallet suddenly shows exposure to illicit marketplaces or gets linked to a sanctioned entity, your six-month-old verification means nothing. You need Salesforce workflows that automatically re-screen wallets quarterly or whenever transaction patterns shift. Real-time monitoring also catches regulatory changes instantly. When OFAC updates its list, your system refreshes automatically. When stablecoin operators adjust their compliance requirements, you adjust your thresholds without manual intervention. Teams that still rely on weekly manual list updates are already behind.

Blockchain Compliance Isn’t Wire Transfer Compliance

The third mistake is the most expensive: treating blockchain payments like traditional wire transfers. Wire transfers move through banks that handle compliance for you. Blockchain doesn’t. When a customer sends stablecoins from their wallet to yours, you own the full compliance burden. That includes tracing the source of those stablecoins-where did they originate on-chain, what wallets touched them, is there illicit exposure buried three hops back in the transaction chain? Traditional wire compliance stops at the immediate counterparty. Blockchain compliance requires cross-chain tracing and multi-hop analysis because value flows through multiple addresses before reaching you. Your Salesforce system needs to surface that upstream exposure automatically, not expect your team to manually investigate wallet histories.

Configuration Matters More Than Features

Teams deploy blockchain intelligence tools but configure them with static blocklists and generic risk scores instead of dynamic, evidence-based screening. Static lists lag reality by weeks. A wallet sanctioned last Tuesday might not hit your system until next Monday. Dynamic risk scoring surfaces exposure in real time and shows your team exactly why a wallet triggered a flag-sanctions match, illicit marketplace connection, or transaction pattern anomaly. When you can see the evidence and confidence level, your team makes faster, more defensible decisions. Configuration matters more than the tool itself. You decide whether to auto-approve low-risk transactions, flag medium-risk activity for manual review, or block high-risk transfers outright. This speed matters because real-time screening reduces your time-to-detect from days to seconds.

FAQ: Salesforce Blockchain KYC & Compliance

Why is KYC mandatory for stablecoin payments in 2026?

The regulatory landscape has shifted from wait and see to active enforcement. In the US, the GENIUS Act (enacted July 2025) and the CLARITY Act have established clear federal oversight. In the EU, MiCA (Markets in Crypto-Assets) is now fully applicable as of 2026. These laws treat stablecoin issuers and businesses processing them as financial institutions, requiring strict Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols.

How does Salesforce help with the Travel Rule?

The FATF Travel Rule requires that information about the sender and receiver of a crypto transaction travels with that transaction. By integrating blockchain intelligence directly into Salesforce, your CRM can automatically attach the required KYC data to the blockchain transaction hash. This creates a unified record that satisfies both the FATF Recommendation 15 and the specific reporting requirements mandated by the US Treasury’s 2026 implementing rules.

Can I run KYC checks without storing sensitive passport data in Salesforce?

Yes. Using Decentralized Identifiers (DIDs) and Zero-Knowledge Proofs (ZKPs), you can verify a customer’s identity attributes (like age or country of residence) without actually ingesting or storing their raw PII (Personally Identifiable Information). Salesforce-native compliance tools can receive a pass or fail signal from a ZKP-enabled identity provider, reducing your GDPR and data breach liability while still meeting MiCA compliance standards.

What happens if a wallet I interact with gets sanctioned?

In 2026, sanctions lists (like the OFAC SDN list) are updated in real-time. A Salesforce-native compliance stack uses API hooks to automatically screen every inbound and outbound wallet address against these lists before the transaction is broadcast to the network. If a match is found, Salesforce can instantly freeze the transaction and alert your compliance officer, preventing a willful negligence charge from regulators.

Is blockchain compliance different from traditional wire compliance?

Significantly. Traditional wire compliance usually stops at the immediate bank. Blockchain compliance requires multi-hop analysis. Salesforce-native tools allow you to see if a customer’s USDC originated from a high-risk source (like a sanctioned mixer or illicit marketplace) several transactions ago. This depth of on-chain provenance is a specific expectation of the EBA (European Banking Authority) and the SEC’s Crypto Task Force in 2026.

Final Thoughts

KYC compliance in your Salesforce blockchain workflows isn’t optional anymore, and frankly, it shouldn’t feel like a burden. Regulators have made their position crystal clear: crypto payments move through the same compliance framework as traditional finance. When you embed KYC controls directly into Salesforce, you build speed and defensibility simultaneously instead of adding friction.

Your business wins when compliance becomes invisible. Customers complete onboarding in seconds using reusable verifiable credentials instead of uploading documents repeatedly. Transactions process instantly because your system screens wallets and sanctions exposure before anything touches the blockchain. Regulators see auditable trails showing exactly what you verified, when you verified it, and why you made each decision.

The infrastructure for KYC compliant Salesforce blockchain already exists. Real-time screening covers Bitcoin, Ethereum, Tron, and major stablecoins like USDT and USDC. Dynamic risk scoring surfaces evidence-based flags instead of static blocklist noise. Unified case management brings wallet screening, sanctions monitoring, and transaction data into one environment. If you’re ready to move beyond treating blockchain payments as a compliance afterthought, explore what Web3 Enabler can do for your organization.