Stablecoins have quietly become the backbone of digital finance, processing over $7 trillion in transactions during 2024 alone. These digital dollars are reshaping everything from international payments to corporate treasuries.

We at Web3 Enabler are investigating the impact of global stablecoins on traditional financial markets. The results might surprise you – and change how you think about money itself.

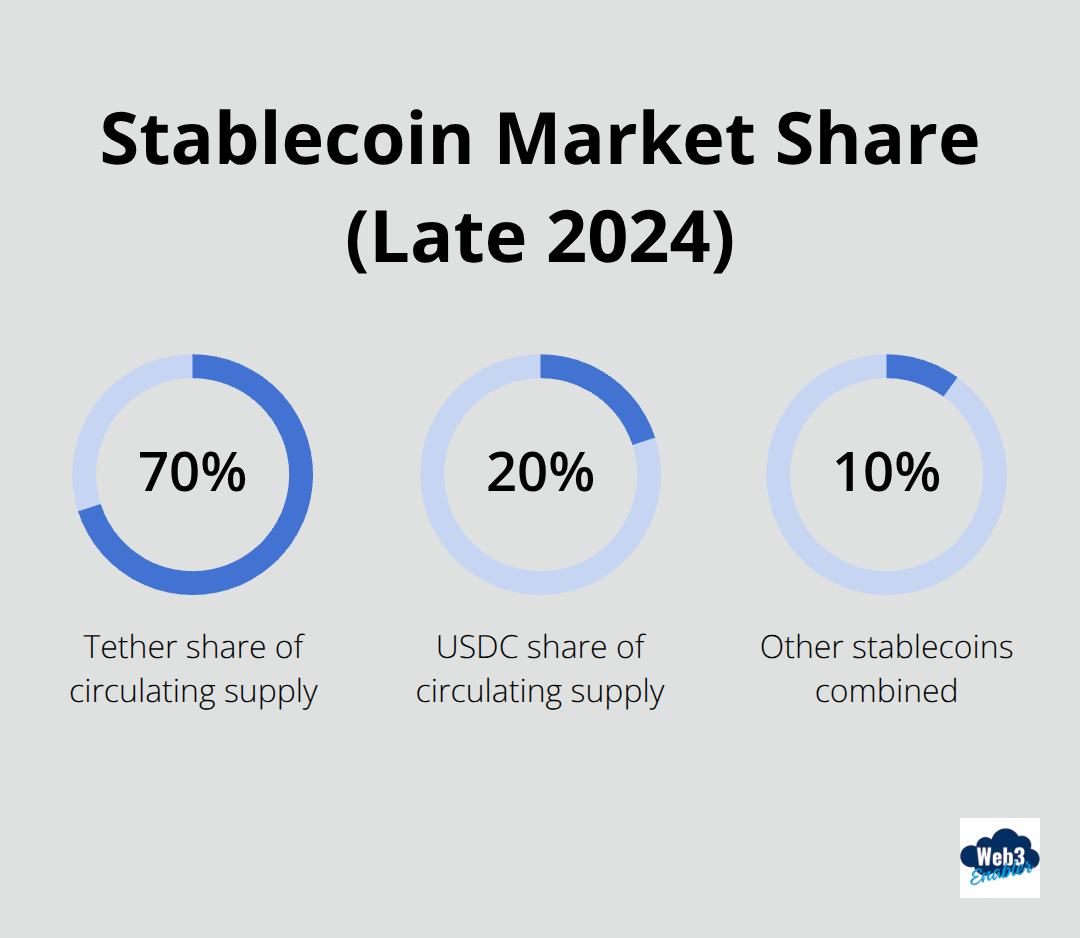

Who Controls the $190 Billion Stablecoin Market

The stablecoin market exploded from $5 billion to $190 billion in just four years, with monthly transaction volumes that hit $1.8 trillion by late 2024. Tether dominates with 70% market share and $120 billion in circulation, while USDC holds 20% at $38 billion according to CoinGecko data. The other 10% splits between newer players like PayPal USD and Binance USD, though regulatory pressure forced several competitors to shut down operations.

Corporate Treasuries Go Digital

Over 75% of Fortune 100 companies in 2025 are using blockchain for payment processing or tracking, with Tesla, MicroStrategy, and Block that led adoption rates. Corporate treasury managers choose stablecoins for international payments because wire transfers cost $25-50 per transaction while stablecoin transfers cost under $1. Shopify processes $2.1 billion annually through stablecoin payments and saves roughly 3% in fees compared to traditional payment rails. PayPal reported 58% growth in stablecoin transaction volume among business accounts (a clear signal of mainstream corporate acceptance).

Institutional Infrastructure Matures Fast

Goldman Sachs, JPMorgan, and Fidelity launched stablecoin custody services in 2024 and now manage over $15 billion in institutional assets. BlackRock partnered with Coinbase to offer stablecoin exposure through ETFs, which attracted $8.2 billion in inflows within six months. Traditional banks face pressure as businesses bypass correspondent networks entirely – Wells Fargo reported a 12% decline in international wire transfer revenue as clients switched to stablecoin rails.

Payment Rails Transform Global Commerce

Stablecoins process cross-border payments in minutes rather than days, which forces traditional correspondent banks to compete on speed and cost. Major payment processors like Stripe and Square integrated stablecoin options after merchants demanded faster settlement times (particularly for international e-commerce). This shift creates ripple effects across foreign exchange markets, where daily stablecoin trading volumes now exceed $180 billion and compete directly with traditional forex pairs.

How Stablecoins Shake Up Currency Trading

Stablecoins disrupted forex markets when they created parallel trading systems that operate 24/7 without traditional banking hours. While stablecoin trading volumes have grown significantly, they directly compete with EUR/USD pairs that process $1.1 trillion daily according to the Bank for International Settlements. Currency traders now watch USDT/USDC spreads as closely as traditional forex pairs because stablecoin arbitrage opportunities signal broader market movements. Major exchanges like Binance report that stablecoin pairs account for 65% of all crypto trading volume and create new liquidity pools that bypass traditional market makers entirely.

Cross-Border Payments Face Real Competition

Traditional wire transfers take 3-5 business days and cost $25-50 per transaction, while stablecoin transfers settle in minutes for under $1. Remittance giants like Western Union lost 18% market share in key corridors as migrants discovered they could send money home instantly with stablecoins. Businesses that process international payments save 2-4% in foreign exchange spreads when they use stablecoin rails instead of correspondent networks. Circle reported that 40% of USDC transactions in Q4 2024 were cross-border payments, with average transaction sizes of $12,000 compared to $500 for traditional remittances.

Banks Fight Back or Fall Behind

JPMorgan launched JPM Coin and processed $300 billion in transactions through 2024, while smaller regional banks struggle to compete with stablecoin speed and transparency. Bank of America reported 15% fewer international wire transfers in 2024 as corporate clients switched to blockchain rails for treasury operations. Traditional correspondent relationships face pressure as businesses question why they pay premium fees for slower settlement times. Smart treasury managers now split international payments between stablecoins for speed and traditional methods for regulatory compliance (a strategy that forces banks to innovate or lose revenue streams permanently).

Market Makers Adapt to New Reality

Traditional forex market makers watch stablecoin flows because large USDT movements often predict currency volatility before it hits spot markets. Citadel Securities and Jump Trading now provide liquidity across both traditional forex and stablecoin pairs to capture arbitrage opportunities. The 24/7 nature of stablecoin markets means price discovery happens continuously, which creates information advantages for traders who monitor both ecosystems. This constant price action puts pressure on central banks to respond faster to market conditions, especially when stablecoin demand signals capital flight from emerging market currencies.

Why Central Banks Panic Over Stablecoins

Central banks accelerated CBDC development after stablecoin circulation reached over $308 billion because they realized private digital currencies threatened monetary policy control. The Federal Reserve fast-tracked digital dollar research in 2024 when USDC transactions exceeded $1.8 trillion monthly, while the European Central Bank launched digital euro pilots after Tether gained 15% market share in eurozone payments.

China Shows How Governments Fight Back

China banned stablecoins entirely and pushed CBDC adoption to 260 million users by 2024, which proves that governments view private stablecoins as existential threats to currency sovereignty. The People’s Bank of China forces all digital payments through state-controlled channels and blocks access to foreign stablecoin networks. This aggressive approach demonstrates how authoritarian regimes can eliminate stablecoin competition when they control internet infrastructure and payment rails.

Banks Build Defense Systems Against Disruption

Banks now treat stablecoin exposure like any other credit risk and require 100% reserves for custody services after Circle’s USDC showed 14% of assets exceeded FDIC insurance limits. JPMorgan developed proprietary risk models that stress-test stablecoin collateral daily and limit exposure to $50 million per issuer to prevent concentration risk. Goldman Sachs requires stablecoin issuers to provide monthly attestations and maintain 120% collateral ratios before they offer custody services to institutional clients.

Regulatory Frameworks Force Market Consolidation

The GENIUS Act forces nonbank stablecoin issuers to comply with capital requirements within 18 months, which means only well-capitalized firms will survive regulatory scrutiny. Smaller stablecoin projects face extinction as compliance costs exceed their revenue potential (particularly those without banking partnerships or institutional backing). This regulatory pressure creates barriers to entry that protect established players like Tether and Circle while eliminating experimental competitors.

Corporate Treasuries Split Their Bets

Treasury departments at Fortune 500 companies now split stablecoin holdings across multiple issuers and maintain traditional banking relationships as backup liquidity sources. This strategy creates a two-tier financial system that operates in parallel rather than replacement of existing infrastructure. Smart CFOs hedge their digital currency exposure while they test stablecoin efficiency for specific use cases like international payments and vendor settlements.

Final Thoughts

The numbers tell a clear story: stablecoins processed $7 trillion in 2024 and fundamentally changed how money moves globally. Traditional banks lost wire transfer revenue while businesses discovered they could send international payments in minutes for under $1. Central banks panicked and accelerated CBDC development when private stablecoins reached $308 billion in circulation.

We’re investigating the impact of global stablecoins on financial markets, and the transformation runs deeper than most executives realize. Corporate treasuries now split between traditional banking and stablecoin rails, which creates parallel financial systems that operate simultaneously. This isn’t replacement – it’s evolution that smart businesses can’t ignore.

Companies that integrate stablecoin payments gain competitive advantages through faster settlement times and lower transaction costs. The infrastructure exists today, and regulatory frameworks solidify around established players (making adoption safer for enterprise clients). At Web3 Enabler, we help businesses connect blockchain technology with existing systems through practical solutions that work today.