Sending money across borders just got a major upgrade. While banks still take days and charge hefty fees, crypto cross border payments happen in minutes for a fraction of the cost.

We at Web3 Enabler see businesses and individuals making the switch daily. The process is simpler than you think, and the savings are real.

What Makes Crypto Cross Border Payments Different

Crypto cross border payments operate through blockchain networks instead of traditional banks. When you send USDC from New York to London, the transaction travels directly through the Ethereum or Solana network without SWIFT or correspondent banks. The recipient receives their funds in minutes, not the 3-5 business days banks typically demand.

Speed Beats Everything

Traditional wire transfers crawl through multiple intermediaries. Your payment stops at your bank, a correspondent bank, possibly another intermediary, and finally reaches the destination bank. Each stop adds time and fees. Stablecoin payments skip this maze entirely.

Stripe data shows businesses that handle over $1 million monthly in cross-border payments adopt stablecoins 92% more often than smaller competitors. The reason hits you immediately: speed equals cash flow. Minutes matter when you need to pay suppliers or employees across continents.

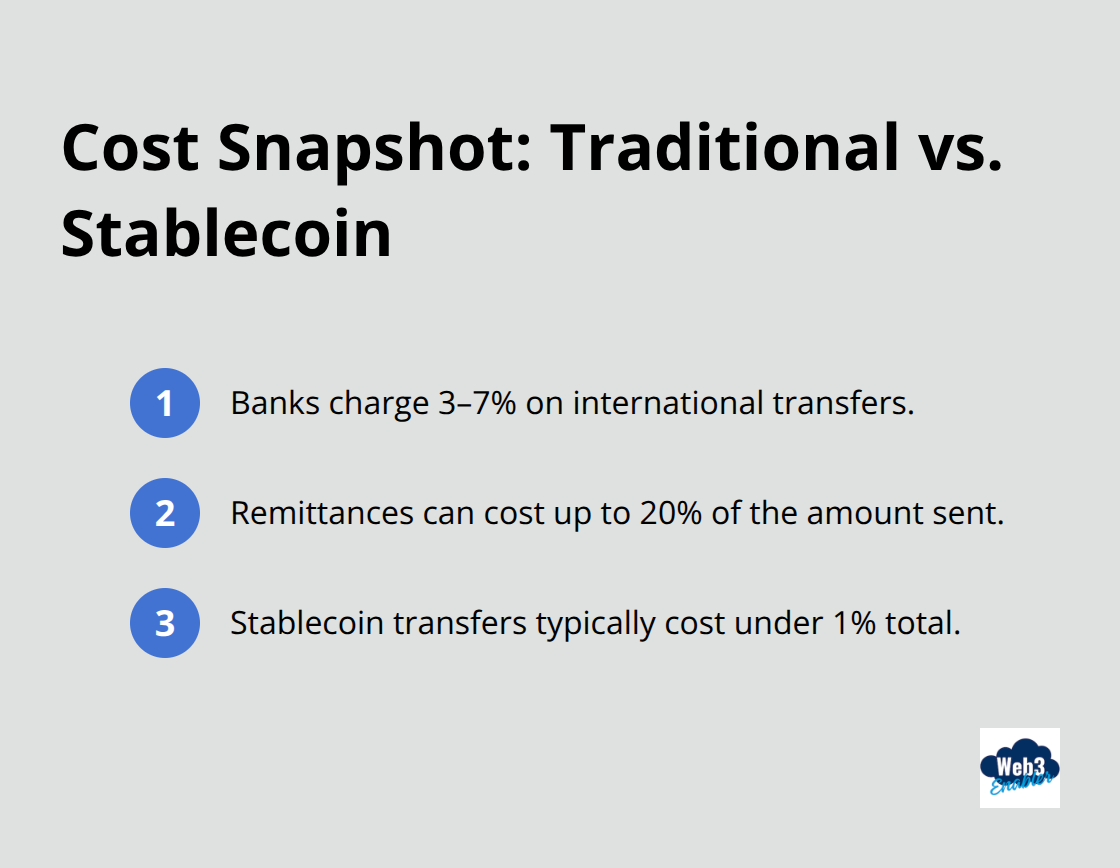

Cost Structure That Actually Works

Banks charge 3-7% for international transfers through currency conversion fees and intermediary charges. Remittances can cost up to 20% of the amount sent (ouch). Stablecoin transfers typically cost under 1% total, sometimes just network fees of a few dollars regardless of transfer size.

The math becomes obvious when you move significant amounts regularly. A $100,000 transfer saves you thousands compared to traditional methods. Companies using stablecoins gain new customers twice as often as those stuck with legacy payment systems.

Global Adoption Tells the Story

Asia currently leads global stablecoin activity and surpasses North America in transaction volume. Trading volume jumped 90% in 2024 to reach $23 trillion. These numbers prove businesses have moved beyond experimentation into full adoption mode.

The two largest stablecoins tripled their combined market cap since 2023, reaching $260 billion total. This growth reflects real business demand, not speculation hype.

Now that you understand why crypto payments outperform traditional methods, let’s walk through exactly how to set up your first transaction.

How Do You Actually Send Crypto Cross Border Payments

Set Up Your Digital Wallet First

Your crypto payment journey starts with wallet selection. MetaMask dominates with over 30 million users globally, while Coinbase Wallet offers better business account integration. Enterprise transactions need multi-signature wallets like Gnosis Safe that require multiple approvals for enhanced security.

Browser extensions work fine for small amounts, but hardware wallets like Ledger or Trezor protect large transfers from online threats. Your wallet choice determines blockchain access, so pick one that supports Ethereum, Solana, and Polygon for maximum flexibility.

Pick USDC for Business Transactions

USDC wins the stablecoin race for cross border payments. Circle backs each token with actual US dollars and publishes monthly attestations from Grant Thornton. USDT processes higher volumes but faces transparency concerns that make compliance teams nervous.

For amounts above $50,000, USDC offers institutional collaboration and strict compliance standards that satisfy auditors. Ethereum provides the most liquidity but charges $10-50 in gas fees. Solana and Polygon reduce fees to under $1 while they maintain speed. Tron offers the lowest fees at pennies per transaction but has limited bank integrations.

Execute Your First Transfer

Start with a test transaction of $100 before you move larger amounts. Copy the recipient’s wallet address twice and verify each character matches – one wrong digit sends funds to a stranger forever (no takebacks in crypto land).

Set gas fees at medium priority for transactions under $10,000 to balance speed and cost. Higher amounts warrant priority fees for faster confirmation. Most payments confirm within 2-15 minutes depending on network congestion.

Screenshot your transaction hash immediately – this proves payment completion for accounting purposes. The recipient converts stablecoins to local currency through exchanges like Kraken or directly through payment processors that handle conversion automatically.

Now that you know the mechanics, let’s talk about the security measures that separate smart operators from cautionary tales.

How Do You Stay Safe with Crypto Payments

Choose Platforms That Actually Matter

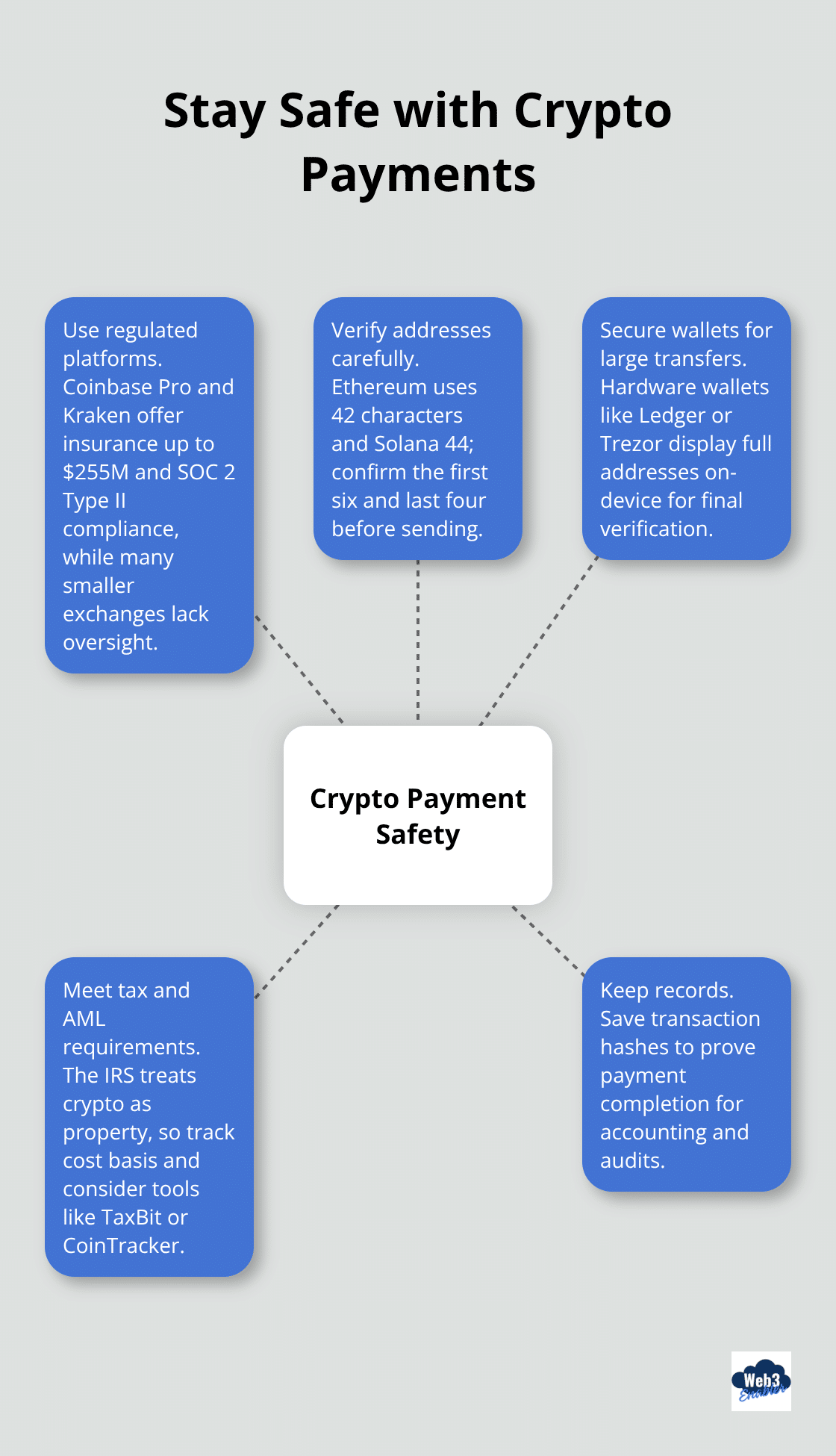

Coinbase Pro and Kraken lead exchange security with insurance coverage up to $255 million and SOC 2 Type II compliance certifications. Binance processes higher volumes but faces regulatory scrutiny in multiple jurisdictions that creates compliance headaches for businesses. Smaller exchanges lack insurance protection and regulatory oversight that enterprises require for audit trails.

Stripe accepts stablecoins with full KYC integration while BitPay offers lower fees but limited currency support. Circle provides direct USDC redemption with same-day ACH settlement for amounts above $100,000. Your compliance team will appreciate trusted platforms over flashy startups that promise unrealistic fee structures.

Triple Check Every Address

Wallet addresses contain 42 characters for Ethereum and 44 for Solana with no error correction built in. One wrong character sends funds into the void permanently. Copy addresses directly from recipient communications, never type them manually. Most wallets display the first six and last four characters prominently – verify these match before you confirm transactions.

Address scams flood transaction histories with similar addresses to trick users into copying wrong destinations. Always use fresh addresses from trusted sources and ignore addresses from your transaction history unless you personally verified them previously. Hardware wallets like Ledger display full addresses on-device for final verification before you sign transactions.

Know Your Tax Obligations Before You Start

The IRS treats cryptocurrency transactions as property sales that require capital gains reports for each transfer. Businesses must track cost basis for every stablecoin purchase and conversion, which creates accounting complexity that traditional wire transfers avoid. TaxBit and CoinTracker automate crypto tax reports but charge $200-500 annually for business accounts.

Most countries require AML compliance for transactions above $10,000 equivalent, which triggers reports similar to cash transactions. The EU’s MiCA regulations and similar frameworks in Singapore demand transaction monitoring and suspicious activity reports. Your finance team needs dedicated crypto accounting software and clear policies before they process the first payment to avoid compliance surprises during audits.

Final Thoughts

Crypto cross border payments transform how businesses move money globally. The process requires three simple steps: set up a secure digital wallet, choose USDC for stability and compliance, then execute transfers with proper address verification. Your payments arrive in minutes instead of days while you save thousands in fees compared to traditional banks.

The numbers speak volumes about this shift. Stablecoin volume hit $23 trillion in 2024, with businesses that handle over $1 million monthly adopting these solutions 92% more often than smaller competitors. Asia leads adoption while regulatory frameworks like MiCA create clearer compliance paths for enterprises (making crypto payments more accessible than ever).

Security remains paramount for successful transactions. Use reputable exchanges with insurance coverage, verify wallet addresses character by character, and maintain proper tax documentation for every transaction. The technology eliminates intermediaries but requires careful attention to detail. Web3 Enabler helps businesses integrate blockchain solutions into their existing processes for faster global payments.