Think digital money is all the same? Think again.

The difference between digital currency and cryptocurrency might seem subtle, but it’s actually huge. We at Web3 Enabler see businesses getting confused about this daily.

One’s controlled by governments, the other runs wild and free. Let’s break down what actually matters for your business.

What Exactly Is Digital Currency?

Digital currency is electronic money that a central authority controls, typically a government or central bank. Unlike physical cash, it exists only in digital form but maintains the same regulatory oversight and stability mechanisms. The Reserve Bank of India has issued over 5 million Digital Rupee transactions since its pilot launch in 2022, while China’s digital yuan processed 100 billion yuan worth of transactions by 2023.

These currencies operate through centralized systems where the authority monitors and approves every transaction. Think of it as cash’s digital twin with a government babysitter.

Government Control Makes the Difference

Central banks issue digital currencies to maintain monetary policy control while they modernize payment systems. Japan revised its Payment Services Act in 2022 to provide legal clarity for digital currency operations (this accelerated adoption among financial institutions). The European Central Bank plans to launch a digital euro by 2026, with 500 million potential users across the eurozone as their target.

Government-backed digital currencies offer legal tender status. This means businesses must accept them for debt payments, unlike private digital tokens that operate in regulatory gray areas.

Real-World Implementation Examples

JPMorgan’s JPM Coin completed 170 billion transactions in 2024, which demonstrates enterprise adoption of tokenized deposits. Major banks like Citibank and DBS actively use tokenized deposits for trade finance and cross-border payments (they reduce settlement times from days to minutes). The Bahamas launched the Sand Dollar in 2020 as the world’s first nationwide central bank digital currency, and it reached 80% of the population within two years.

These implementations show digital currencies work best for institutional payments, regulatory compliance, and financial inclusion rather than speculative trades.

But what happens when you remove the government from the equation entirely?

How Does Cryptocurrency Actually Work

Cryptocurrency operates on decentralized networks where no single authority controls the money supply or transaction processing. Bitcoin’s network relies on approximately 15,000 nodes worldwide that validate transactions through computational proof, while Ethereum processes roughly 1.2 million transactions daily across its decentralized infrastructure. These networks use blockchain technology to record every transaction permanently and create an immutable ledger that anyone can verify but no one can alter once confirmed.

Mining Powers the Network

Bitcoin miners consume more electricity than Finland to secure the network through proof-of-work validation. Each block requires the solution of complex mathematical puzzles, with successful miners who earn 6.25 Bitcoin per block as of 2024. Ethereum switched to proof-of-stake in September 2022, which reduced its energy consumption by 99.9% while it maintains security through 35.7 million staked ETH from over one million validators.

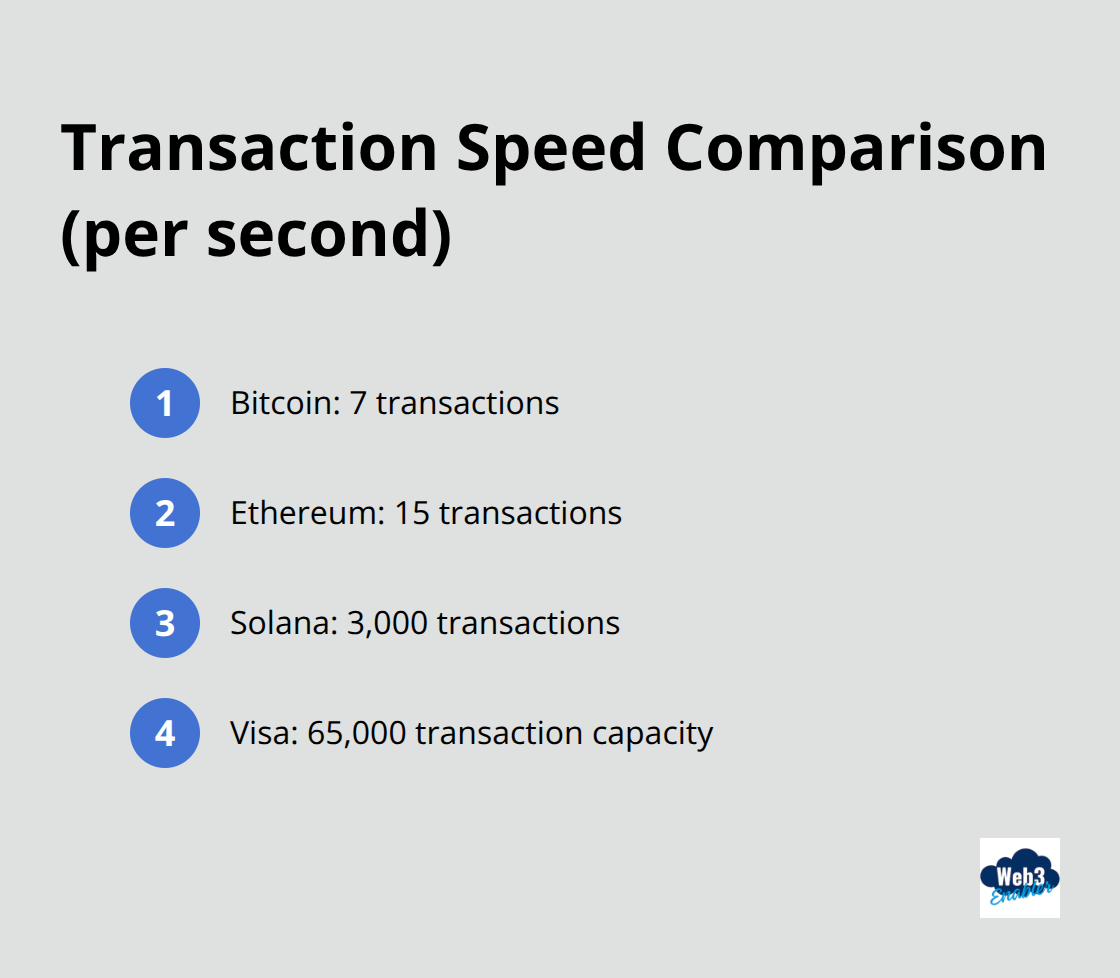

Transaction Speed Varies Wildly

Bitcoin processes 7 transactions per second compared to Visa’s 65,000 capacity, which makes it unsuitable for daily retail payments. Ethereum handles 15 transactions per second but costs $5-50 per transaction when network congestion occurs. Solana achieves 3,000 transactions per second with sub-second finality (this positions it for business applications that need speed over maximum decentralization).

Popular Cryptocurrencies Serve Different Purposes

Bitcoin remains the digital gold standard with a market cap that exceeds $600 billion, and businesses primarily use it for store of value rather than payments. Ethereum enables smart contracts and decentralized applications, and it hosts over 4,000 active projects that include stablecoins like USDC which maintain dollar parity. Ripple’s XRP targets cross-border payments for banks and settles transactions in 3-5 seconds at costs under $0.01 per transaction.

So cryptocurrencies run free without government oversight, but what happens when these two worlds collide? The differences between controlled digital money and wild crypto create some fascinating contrasts that every business needs to understand.

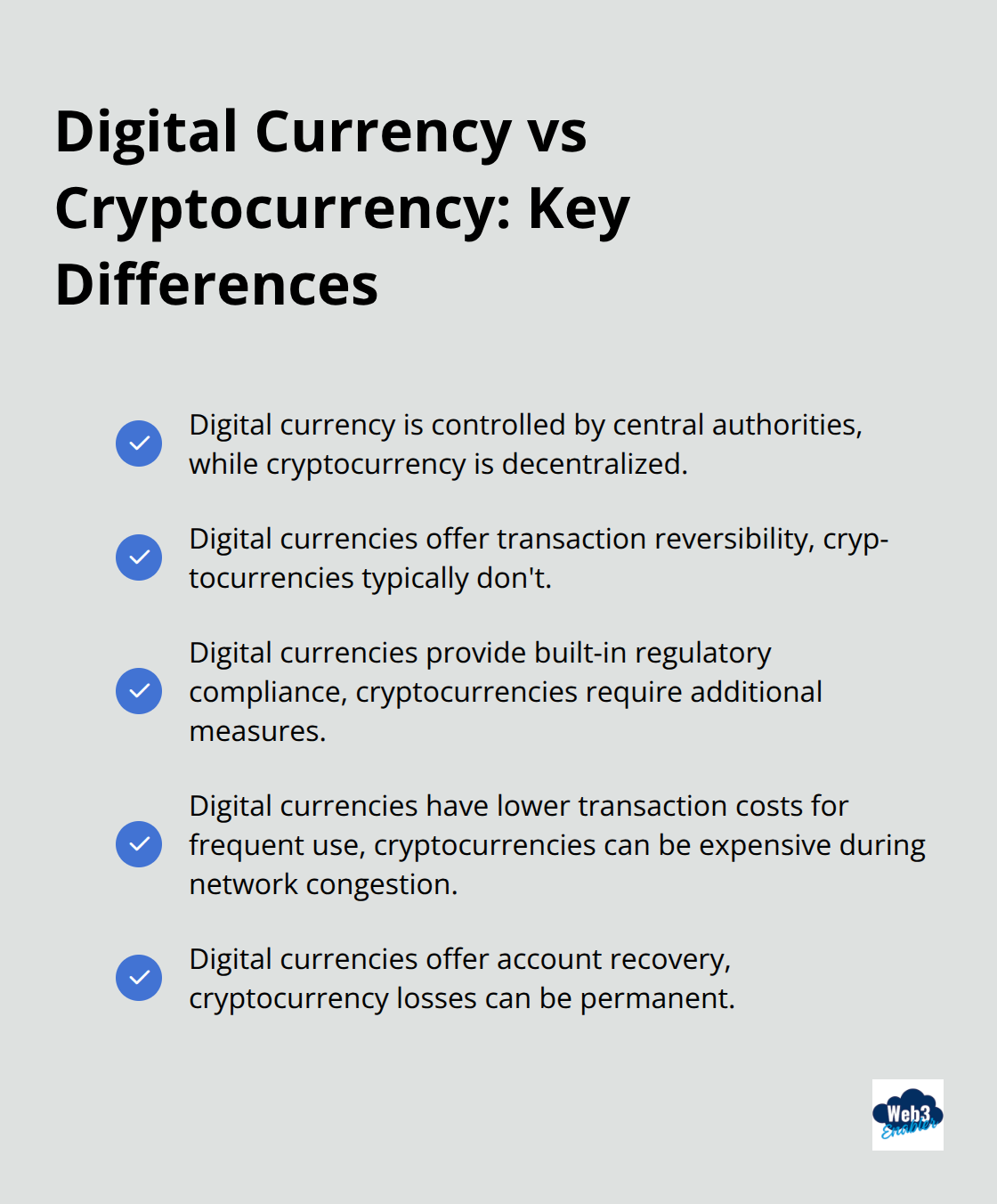

What Makes Digital Currency and Crypto So Different

The control gap between digital currencies and cryptocurrencies creates massive operational differences for businesses. Digital currencies operate under central bank supervision with instant reversibility features, while cryptocurrencies run on immutable networks where transaction mistakes become permanent. The Federal Reserve can freeze Digital Dollar accounts within minutes, but Bitcoin transactions remain irreversible once the blockchain confirms them. China’s digital yuan allows the People’s Bank to track every transaction in real-time and implement restrictions, whereas Bitcoin provides pseudonymous transactions that governments struggle to monitor without additional compliance layers.

Speed Wars and Transaction Costs

Transaction processing reveals stark performance differences that impact business operations. Digital currencies like JPMorgan’s JPM Coin enable near-instant, 24/7 payments through blockchain infrastructure, while Bitcoin requires 10-60 minutes for confirmation and costs $15-45 per transaction during network congestion. The Digital Rupee processes payments in under 3 seconds with zero fees for consumers, but Ethereum charges $5-50 per transaction based on network demand. Stablecoins on Ethereum cost businesses $20-100 for simple transfers (this makes them unsuitable for micro-payments or frequent transactions that traditional digital currencies handle efficiently).

Privacy and Security Trade-offs

Security models create opposite approaches to user protection and regulatory compliance. Digital currencies offer account recovery through central authorities and fraud protection similar to traditional banks, while cryptocurrency losses from forgotten passwords or hacks become permanent with no recourse options. The Bahamas Sand Dollar provides full transaction reversal capabilities and consumer protection laws, but Bitcoin’s immutable ledger means businesses must implement additional security measures and accept higher operational risks. Central bank digital currencies enable governments to implement anti-money laundering controls automatically, whereas cryptocurrency businesses face complex compliance requirements and potential regulatory penalties for inadequate systems (this creates significant operational overhead for companies entering the crypto space).

Final Thoughts

The difference between digital currency and cryptocurrency comes down to control, speed, and risk tolerance. Digital currencies offer government backing, instant reversibility, and regulatory compliance but sacrifice the freedom that makes crypto appealing. Cryptocurrencies provide decentralization and global accessibility while they demand higher technical expertise and accept permanent transaction risks.

Future financial systems will likely accommodate both approaches. Central bank digital currencies will dominate regulated business payments and government transactions, while cryptocurrencies will serve cross-border commerce and decentralized applications. The coexistence creates opportunities for businesses that understand when to use each option (and when to avoid the wrong choice entirely).

Your choice depends on specific business needs. Companies that require regulatory compliance, transaction reversibility, and predictable costs should consider digital currencies. We at Web3 Enabler help businesses navigate this landscape through Salesforce-native blockchain solutions that connect traditional corporate infrastructure with modern payment technologies.