African businesses lose billions annually to remittance fees and slow cross-border payments. A fiat onramp in Africa changes this by converting local currency directly into stablecoins, cutting costs and settlement times dramatically.

We at Web3 Enabler have seen firsthand how this shift transforms payment flows for merchants across the continent. This guide walks you through the providers, compliance steps, and technical setup you need to start accepting international payments in stablecoins today.

Why African Businesses Hemorrhage Money on Cross-Border Payments

Traditional remittance corridors drain African businesses through multiple layers of inefficiency. A manufacturer in Lagos sending payment to a supplier in Kenya pays 5–7% in fees through conventional banking, then waits 3–5 business days for settlement. A software company in Nairobi invoicing international clients faces similar delays plus currency conversion losses. These costs compound across dozens of transactions monthly, directly cutting into margins that could fund growth or hiring. Stablecoins bypass this entirely.

A business accepting USDT or USDC receives funds in minutes, not days, with fees typically under 1%, and settles directly into local currency without intermediaries skimming at each step. Nigeria ranks second globally in crypto adoption according to the Chainalysis 2024 Global Crypto Adoption Index, reflecting how aggressively businesses there are already moving toward digital rails to escape the traditional banking trap.

The Banking Gap That Stablecoins Fill

Formal banking infrastructure in Africa remains fragmented and expensive. Many businesses operate in markets where international wire transfers cost $30–50 per transaction, require advance notice, and fail unpredictably. Smaller merchants and startups often cannot access correspondent banking at all, leaving them unable to receive payments from overseas clients. Stablecoins eliminate this requirement. A business needs only a digital wallet and an internet connection to receive international payments instantly. Yellow Card, Africa’s largest licensed stablecoin on- and off-ramp, now operates across 20 countries with over 1.7 million retail customers, demonstrating how rapidly this infrastructure is scaling. For a Ugandan e-commerce platform or a Ghanaian logistics firm, this means accessing global payment flows without applying to banks that may reject them outright. Settlement into local currency happens through local payment rails-bank transfers, mobile money, instant peer-to-peer payments-that businesses already use daily, removing the friction of unfamiliar systems.

Why Merchants Are Moving Fast

Cross-border payment demand in Africa is accelerating because businesses face no other viable option for speed and cost. Flutterwave plans a pilot enabling USDC-based cross-border transactions on the Polygon blockchain, signaling how major African fintechs recognize stablecoins as the only practical infrastructure for merchant settlements. A gaming platform accepting payments from players across five countries cannot wait days for clearing and cannot absorb 5–7% fees per transaction. Stablecoins compress both timelines and costs to negligible levels. Breet’s API, launched in Nigeria, lets businesses receive stablecoins and settle instantly without managing crypto operations themselves-the wallet generation, monitoring, and settlement happen behind the scenes. This removes the technical barrier that previously locked out non-crypto-native merchants. A marketplace with international vendors no longer relies on slow cross-border banking rails; it accepts dollar-denominated payments and settles them in minutes, whether the vendor wants stablecoins or local currency. This shift is not theoretical-it is happening now across West Africa as businesses competing globally cannot afford the drag of traditional payment infrastructure.

What Comes Next

The providers and compliance frameworks that enable this shift vary significantly across regions and use cases. Understanding which onramp provider fits your business model, how to integrate their systems, and what regulatory steps you must complete determines whether you capture these savings or remain trapped in expensive traditional flows.

Fiat-to-Crypto Onramp Providers and Solutions Available in Africa

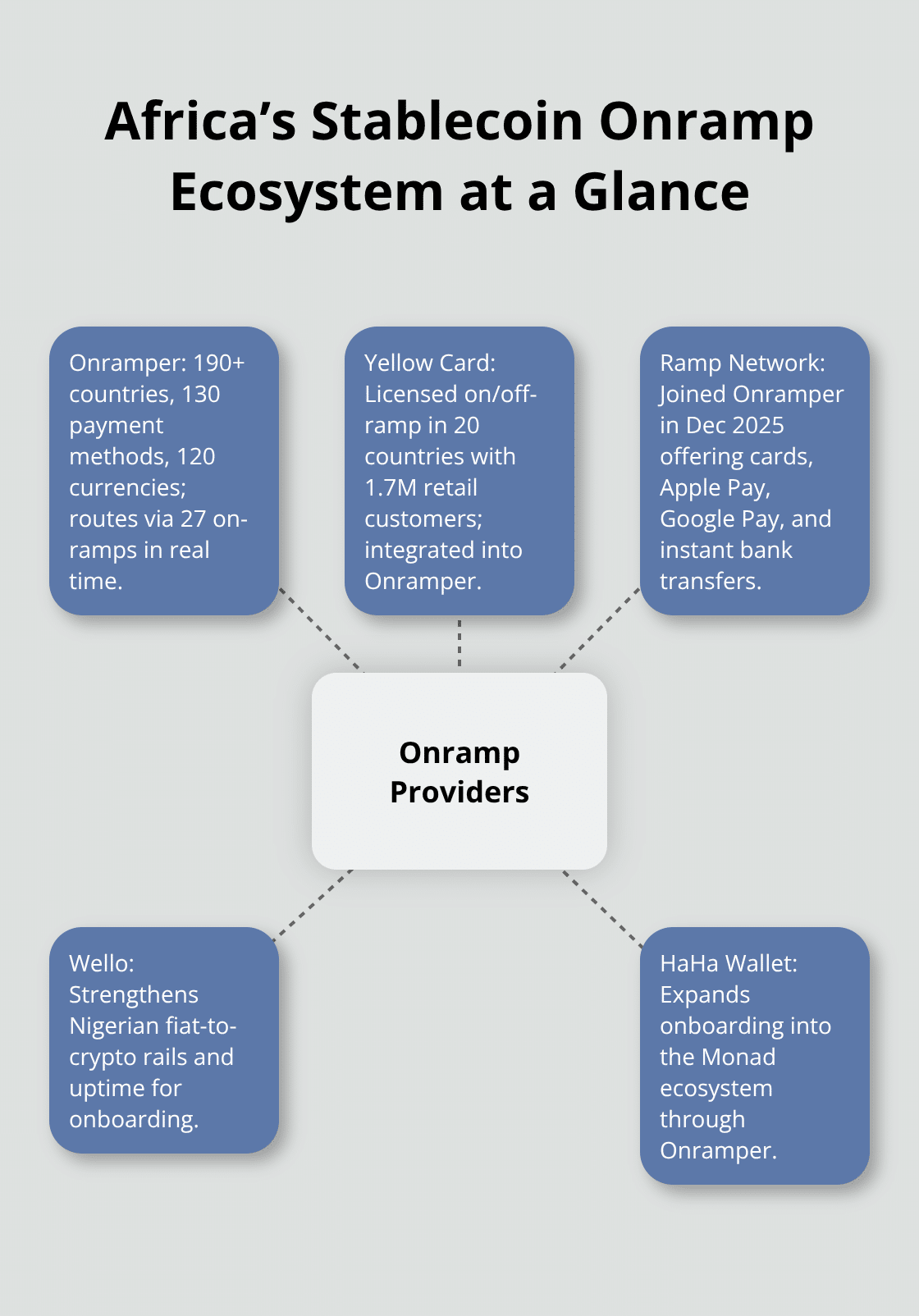

Onramper’s Network Dominates African Payment Routes

Onramper operates the largest network for African fiat-to-crypto conversions, covering 190+ countries with 130 local payment methods across 120 currencies. The platform routes transactions through 27 on-ramps in real time, selecting the best conversion rates automatically to maximize the crypto you receive and minimize failed transactions. For businesses in Nigeria, Kenya, Uganda, and Ghana, this matters because local payment rails vary dramatically by country. Onramper’s smart routing engine handles this complexity behind the scenes, meaning a Lagos merchant receives competitive pricing whether paying via bank transfer, mobile money, or instant peer-to-peer rails.

Yellow Card and Regional Partners Strengthen Local Access

Yellow Card, Africa’s largest licensed stablecoin on- and off-ramp, integrates directly into Onramper’s network and operates across 20 countries with 1.7 million retail customers. Through Yellow Card’s rails, businesses access USDT, USDC, and PYUSD using local currency in their own market. Ramp Network joined Onramper’s ecosystem in December 2025, adding fast, compliant payment flows via cards, Apple Pay, Google Pay, and instant bank transfers. The integration rolls out automatically to existing Onramper partners without requiring setup changes, meaning merchants gain access to additional payment methods instantly. Wello strengthened Nigerian payment rails when it joined Onramper in December 2025, improving coverage and uptime specifically for fiat-to-crypto onboarding in West Africa’s largest crypto market.

HaHa Wallet expanded Onramper’s ecosystem in December 2025 to broaden onboarding into the Monad ecosystem, giving merchants 130+ local payment methods across 190+ countries to receive crypto from international clients.

Integration and Compliance Made Simple

Integration happens through Onramper’s widget, which requires only eight lines of code to embed into your platform. Merchants avoid managing multiple provider relationships; instead, one integration connects you to all 27 on-ramps and their local payment methods. Compliance requirements vary by country, but Onramper handles AML and KYC checks across its network, meaning you do not repeat identity verification for each provider. Settlement timeframes depend on the payment method and provider, but most conversions complete within minutes to hours rather than the 3–5 business days traditional banking requires.

Breet’s Direct API for High-Volume Nigerian Merchants

Breet offers an alternative approach for Nigerian businesses specifically, providing an API that lets you accept stablecoins directly and settle instantly without managing crypto operations yourself. Breet generates wallet addresses, monitors transactions, and handles settlement in stablecoins or local currency, with confirmations delivered via webhooks. Pricing follows a usage-based model with percentage fees per incoming transaction, custom terms for larger volumes. PIL, a B2B spend-management platform, integrated Breet to fund virtual cards with stablecoins, demonstrating how this infrastructure works at scale for businesses beyond simple payment acceptance.

Selecting Your Provider Based on Business Needs

The choice between Onramper’s aggregated approach and Breet’s API depends on your volume and technical capability. High-volume merchants benefit from Breet’s direct integration and custom pricing. Merchants preferring simplicity and broad geographic reach choose Onramper’s widget and automatic provider selection. Your next step involves evaluating which provider aligns with your transaction volume, the countries where you receive payments, and whether you want to settle in stablecoins or local currency-decisions that shape your technical setup and ongoing operational costs.

How to Pick Your Stablecoin and Set Up Payments

USDT and USDC Lead African Payment Flows

USDT and USDC dominate African payment flows because they offer the deepest liquidity and widest acceptance across exchanges and merchants. USDT trades on virtually every platform in Africa and settles faster than alternatives. USDC, backed by Circle and regulated in the U.S., appeals to merchants prioritizing regulatory clarity. PYUSD, PayPal’s stablecoin, offers an alternative for businesses already embedded in PayPal’s ecosystem, though adoption across Africa remains limited compared to USDT and USDC.

Your choice depends on three factors: where your international clients send payments, which stablecoin your settlement provider accepts, and whether you plan to hold the asset or convert immediately to local currency. If you receive payments from multiple countries, USDT wins because nearly every African merchant and exchange accepts it without friction. If you settle into local currency instantly, the choice matters less since your provider handles the conversion.

Pricing and Rate Selection Across Providers

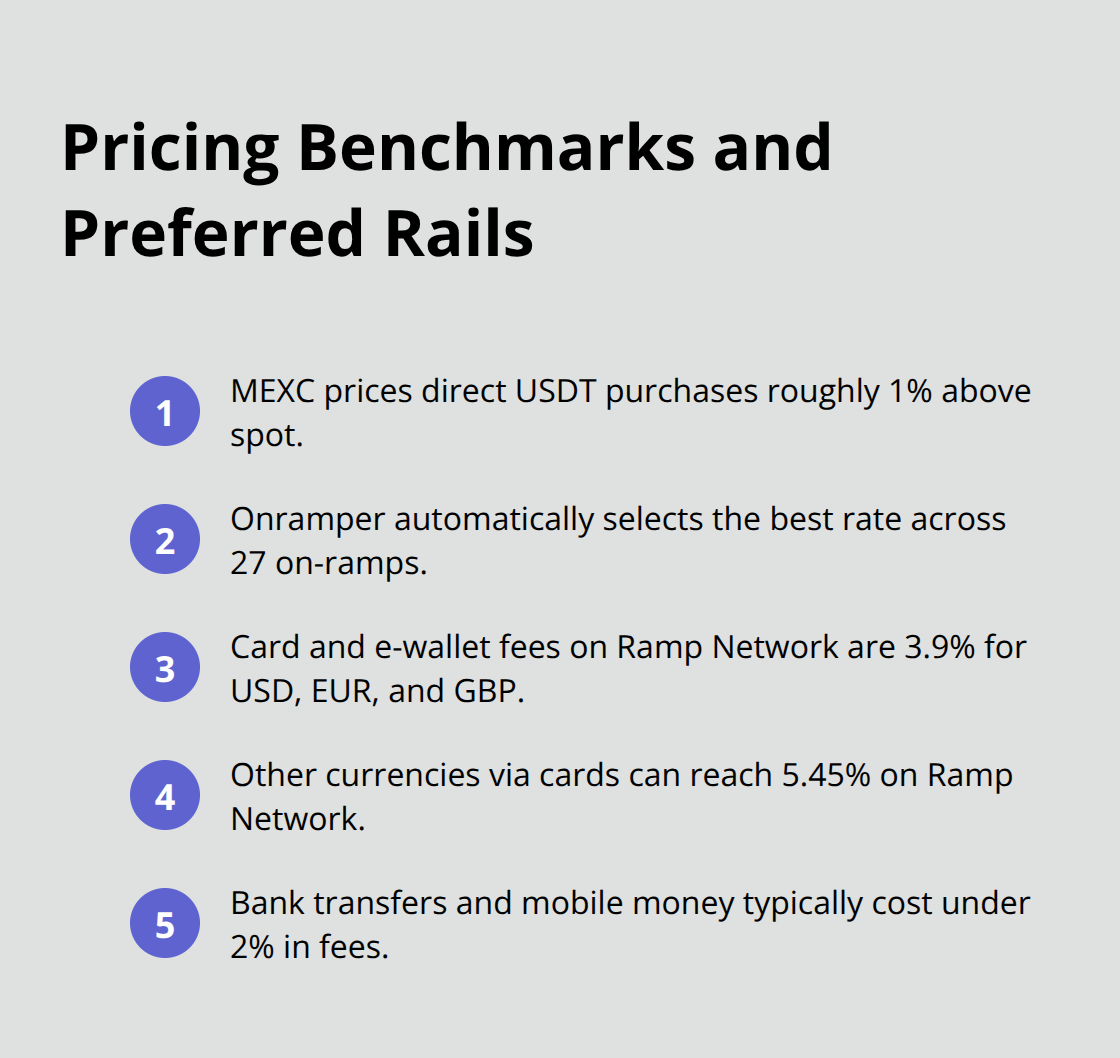

MEXC, a major exchange used across Africa, prices direct fiat purchases of USDT at roughly 1% above the spot price, making it competitive for high-volume conversions. Onramper’s smart routing automatically selects the best rate across 27 on-ramps, removing the need to manually compare pricing across providers.

For Nigerian businesses specifically, Breet’s API accepts both USDT and USDC and settles into local currency or stablecoins based on your preference, with fees structured as a percentage of each incoming transaction and custom pricing available for volume over 50,000 USDC monthly. Card and e-wallet payments carry higher fees universally-expect 3.9% on Ramp Network for USD, EUR, or GBP, rising to 5.45% for other currencies. Bank transfers and mobile money consistently offer the lowest fees, typically under 2%, making them the preferred method for high-volume merchants who can plan payment collection around these rails.

Integration Approaches: Widget vs. Direct API

The integration choice determines your operational load. Onramper’s widget embeds in eight lines of code and requires no backend work-your platform immediately connects to all 27 on-ramps and their payment methods without managing multiple provider relationships. Breet’s API demands more technical setup but gives you direct control over wallet generation, transaction monitoring, and settlement logic, making it preferable for platforms processing over 10,000 transactions monthly where custom pricing and direct integration justify the engineering effort.

Most conversions through Onramper complete within minutes to a few hours depending on the payment method; bank transfers typically settle fastest at 5–30 minutes, while some mobile money rails take 1–2 hours due to local network processing. Breet delivers confirmations via webhooks, letting your platform automate settlement flows immediately without polling external systems.

Settlement Strategy: Stablecoins or Local Currency

Settle in stablecoins if you hold reserves in USD or operate across multiple countries where local currency conversion would trigger losses. Settle in local currency immediately if you need to pay local staff, suppliers, or cover operational costs in naira, cedis, or shillings. Yellow Card’s integration with Onramper handles both settlement types across 20 African countries, meaning your choice can be made transaction-by-transaction rather than locked in at setup.

For a Lagos e-commerce platform receiving payments from buyers across five African countries, settling USDC into NGN through Yellow Card’s local rails costs roughly 1% and completes within hours, compared to the 5–7% and 3–5 business days traditional banking requires. Onramper’s embedded fees range from under 1% for bank transfers in major corridors to 3–5% for card payments depending on the on-ramp provider handling that specific route.

Final Thoughts

Fiat onramps in Africa eliminate the cost and delay that constrained business growth across the continent for decades. A merchant accepting USDT or USDC through Onramper or Breet receives international payments in minutes instead of days, pays under 1% in fees instead of 5–7%, and settles directly into local currency without intermediaries extracting value at each step. This structural change rewires how African businesses connect to global payment flows and transforms competitive advantage overnight.

The practical advantage compounds across your operation as a gaming platform accepting stablecoins from players across five countries eliminates payout delays that previously frustrated users and cut retention, while a marketplace with international vendors stops relying on slow cross-border banking and settles dollar-denominated payments instantly. A software company invoicing clients overseas no longer absorbs currency conversion losses or waits for clearing, and these savings accumulate monthly to fund expansion, hiring, or reinvestment that traditional payment infrastructure made impossible. The shift toward stablecoin payments across West Africa accelerates because businesses competing globally cannot afford the drag of traditional infrastructure-Flutterwave pilots USDC on Polygon, Yellow Card serves 1.7 million customers across 20 countries, and Breet processes stablecoin settlements for platforms like PIL at scale.

We at Web3 Enabler recognize that blockchain integration extends beyond payment acceptance into your entire business infrastructure, and our platform connects blockchain transactions directly to Salesforce to enable you to manage digital assets, track investment returns, and handle international contractor payments within your existing corporate systems. The future of African commerce runs on stablecoins and digital rails, and the question is not whether your business adopts them, but how quickly you move.