Sending money across borders shouldn’t feel like navigating a maze blindfolded. Yet traditional banking makes international transfers expensive, slow, and frustratingly complex.

Cross border payments crypto solutions are changing this game completely. We at Web3 Enabler see businesses ditching old-school wire transfers for blockchain-based alternatives that actually work.

The shift isn’t coming – it’s already here.

Why Traditional Cross-Border Payments Cost Too Much

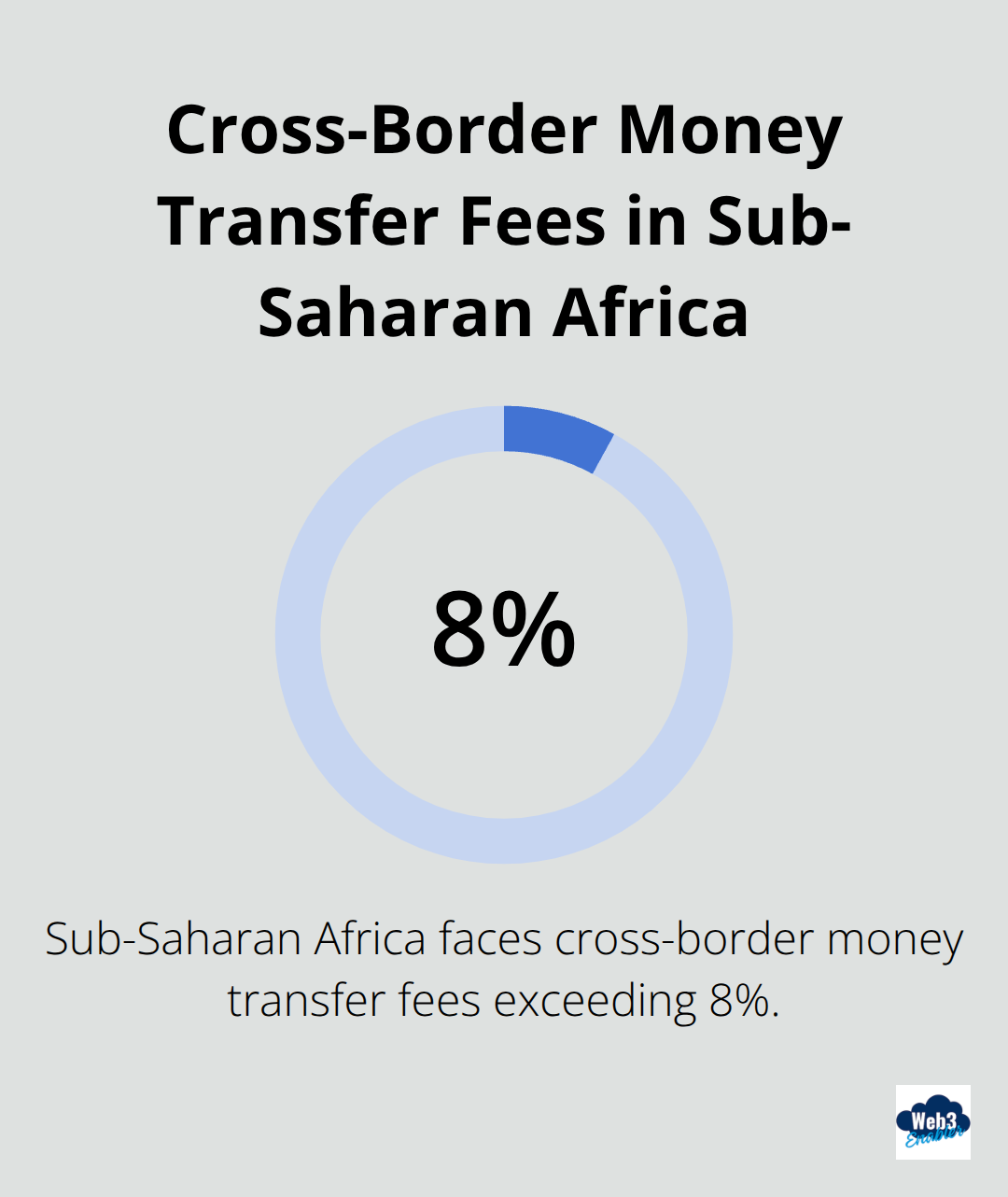

Banking executives love to talk about innovation, but their cross-border payment systems still operate like it’s 1995. The average global cost of sending money abroad creates significant barriers to financial inclusion, with Sub-Saharan Africa facing fees that exceed 8%. That’s not a service charge – that’s highway robbery with a three-piece suit.

The Fee Multiplication Game

Traditional banks don’t just charge you once. They layer fees like a wedding cake nobody asked for. You’ll pay origination fees, intermediary bank charges, correspondent banking fees, and foreign exchange spreads that add another 3-4% to your transfer. J.P. Morgan processes over $10 trillion daily across 60 million transactions and achieves a 99.3% straight-through processing rate, yet smaller businesses still face these compound costs that easily reach 10% of the transfer amount.

Settlement Speed That Makes Glaciers Look Fast

Wire transfers take 1-5 business days to settle internationally. In 2024, that’s not processing time – that’s procrastination with paperwork. Your money sits in correspondent banking limbo while banks earn interest on funds that should already be in your recipient’s account. Meanwhile, your business cash flow suffers, and time-sensitive payments become expensive emergencies that require premium express services (which double the already inflated fees).

Compliance Theater Performance

Banks have turned regulatory compliance into an elaborate performance where everyone knows their lines but nobody gets to the point. KYC procedures require documentation that would make the IRS jealous, and each intermediary bank adds its own compliance requirements. The result? Transfers get flagged, delayed, or rejected for reasons that range from legitimate security concerns to algorithmic paranoia about transaction patterns that don’t fit their outdated risk models.

These traditional payment rails weren’t built for today’s global economy – they were patched together from decades-old infrastructure that banks refuse to modernize. Fortunately, crypto offers a completely different approach that eliminates these systemic problems entirely.

How Crypto Fixes Cross-Border Payment Problems

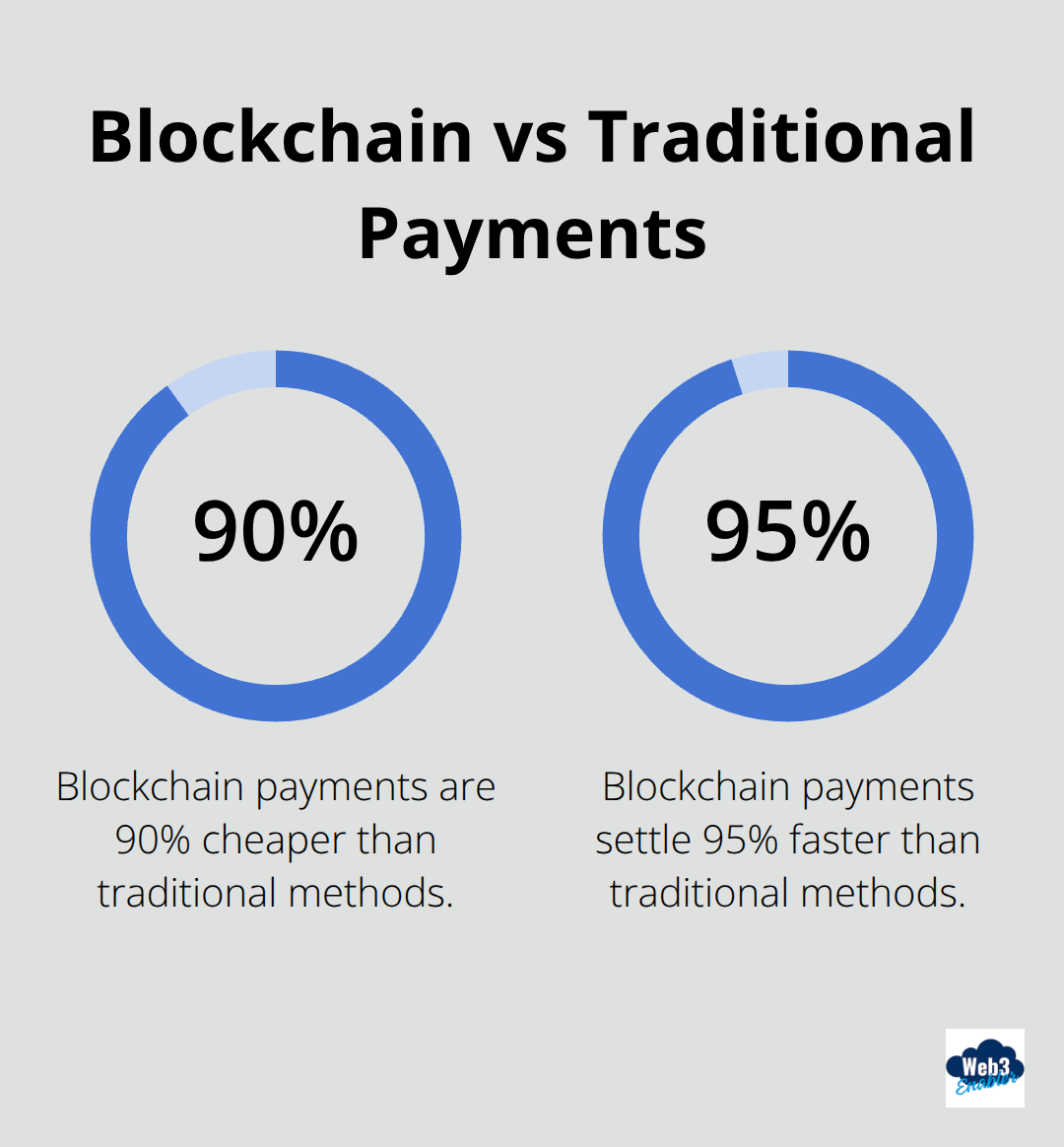

Crypto payments operate on fundamentally different rails that eliminate traditional banking bottlenecks entirely. Blockchain payments are 90% cheaper and settle 95% faster than traditional methods, while stablecoins like USDC have reached $250 billion in circulation volume over just 18 months according to recent market data. The Lightning Network processes transactions with superior technical capabilities versus Visa’s theoretical limit of 65,000, which demonstrates advantages that translate into real business benefits.

Transparent Fees Without Hidden Surprises

Blockchain networks display exact transaction costs upfront before you commit. No correspondent bank fees, no surprise foreign exchange spreads, and no intermediary charges that mysteriously appear on your statement weeks later. Platforms like NOWPayments support over 300 cryptocurrencies with transparent fee structures, while traditional banks layer multiple charges that can exceed 10% of your transfer amount when all costs combine.

Settlement Speed That Actually Works

Crypto transactions settle in seconds or minutes, not business days. Blockchain networks operate continuously without bank holidays, weekend closures, or time zone restrictions that delay traditional transfers. This 24/7 availability means your Friday afternoon payment reaches recipients immediately instead of sitting in correspondent bank limbo until the following Tuesday (improving cash flow management for businesses that operate across multiple time zones).

Programmable Compliance Features

Smart contracts automate compliance requirements directly into payment protocols, which reduces manual oversight while maintaining regulatory standards. Blockchain’s immutable transaction records provide superior audit trails compared to traditional systems where documentation gets scattered across multiple intermediaries. This transparency helps businesses meet regulatory requirements while reducing the administrative burden that makes traditional cross-border payments so cumbersome and expensive.

These technical advantages translate into real-world applications that businesses across industries are already implementing to overcome cross-border payment challenges and transform their international payment operations.

How Businesses Actually Use Crypto Payments

Stablecoins Replace Wire Transfers for Global Commerce

Companies like Nubank in Brazil, Mexico, and Colombia reported users held ten times more USDC stablecoin by late 2024, with new digital-asset customers making up 30% of total holdings. The Lemon platform reached over $137 million in USDC holdings, which marked 21% growth within a year according to 2025 data. These numbers reflect businesses that moved away from traditional banks for international transactions because stablecoins eliminate foreign exchange spreads that typically add 3-4% to cross-border payments.

Fintechs like Remitly adopted stablecoins specifically for faster, lower-cost remittances in Africa and Latin America where traditional banks charge fees that exceed reasonable business costs. Major companies including PayPal and Visa now incorporate cryptocurrencies into their platforms, which indicates a trend toward hybrid financial ecosystems that combine traditional services with crypto efficiency.

Remittances Get Cheaper and Faster

Wealthy migrants benefit most from DeFi platforms because they avoid multiple banks for large transfers, which saves on fees and foreign exchange spreads that compound across traditional correspondent networks. Stablecoins serve as accessible digital wallets that allow transactions before people establish traditional bank accounts (particularly helpful for migrants in countries like South Africa and Italy where local KYC compliance creates barriers).

Higher costs of traditional remittances directly correlate with increased usage of Bitcoin and stablecoins for cross-border flows according to a May 2025 Bank for International Settlements Working Paper. The regulatory frameworks implemented in Bahrain and the UAE for stablecoin issuance enhance transaction safety while they maintain the cost advantages that make crypto remittances attractive for regular use.

Blockchain Creates Superior Audit Trails

Companies that use blockchain report substantial reductions in invoice disputes, with Walmart Canada decreasing disputes from 70% to just 1% through smart contracts that automate payment verification. Blockchain provides a single, shared, tamper-proof record for transactions that enhances data reliability compared to traditional systems where documentation gets scattered across multiple intermediaries.

This transparency helps businesses meet regulatory requirements while it reduces administrative burden. The immutable transaction records provide superior audit trails that financial institutions can access instantly rather than request documentation from correspondent banks (which may take weeks to provide complete transaction histories). Financial institutions face an average cost of over $6 million per data breach, but blockchain’s decentralized model achieves near-zero chargebacks due to immutable transaction records.

Final Thoughts

The shift to cross-border payments crypto solutions isn’t a distant possibility – it happens right now. McKinsey predicts stablecoin usage will reach $2 trillion by 2028, while nine out of ten firms already explore blockchain payments. Traditional banks can keep patching their 1995-era systems, but businesses that want competitive advantages move to blockchain rails today.

Early adopters gain immediate cost savings of 90% on transaction fees, settlement times measured in minutes instead of days, and 24/7 operational access that eliminates bank hour restrictions. Companies that use blockchain report substantial efficiency improvements, with some reducing invoice disputes by 99% through automated verification systems. The technical infrastructure already exists and works at scale (while regulatory frameworks develop rapidly in major markets).

The only question is whether your business will lead this transformation or scramble to catch up later. We at Web3 Enabler help businesses integrate blockchain payments directly into their existing Salesforce infrastructure through 100% native solutions available on the AppExchange. Our tools support stablecoin payments, global transfers, and compliance automation without requiring crypto expertise or separate systems.