Cross-border payments are undergoing a fundamental shift. Stablecoins, blockchain infrastructure, and regulatory frameworks are converging to reshape how enterprises move money globally.

At Web3 Enabler, we’re watching these cross-border payments trends accelerate adoption among institutions that can’t afford to wait. The competitive advantage belongs to those who act now.

Stablecoins Are Now Moving Real Money Globally

Stablecoin transaction volume reached significant levels in 2024, and that number tells you everything about institutional adoption. This isn’t theoretical anymore. Major players like Corpay, dLocal, MoneyGram, and Rapyd have already integrated stablecoins into their treasury operations to cut costs and speed up settlements. The regulatory framework that enterprises were waiting for arrived with recent legislation, and institutions moved from pilots directly into production. Stablecoins still represent less than 1% of total cross-border payment volume, but the growth trajectory is undeniable. Global stablecoin circulation reached approximately 307 billion dollars as of November 2025, with annual growth exceeding 50%.

What Makes Stablecoins Cheaper Than Wire Transfers

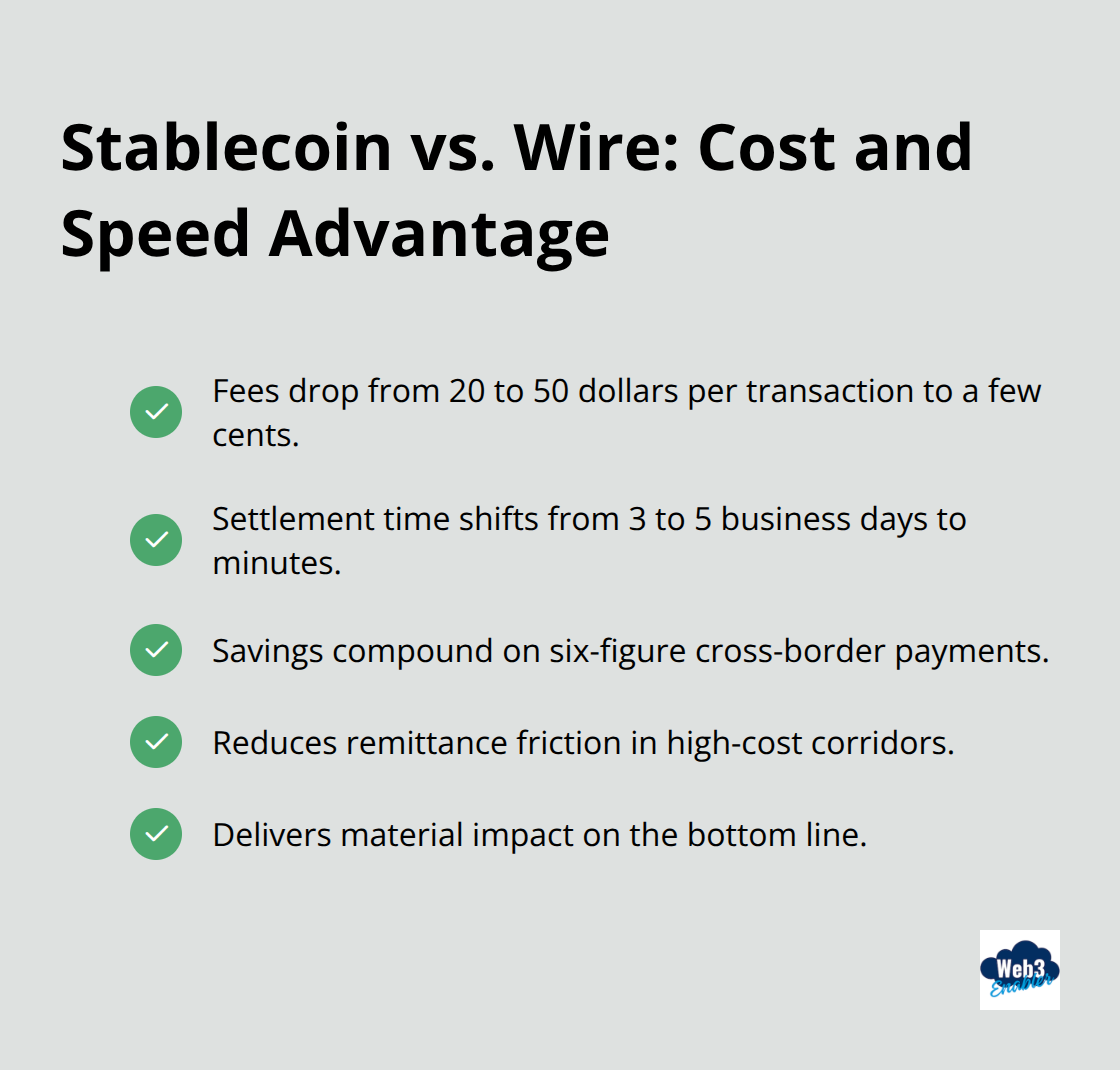

Traditional wire transfers charge 20 to 50 dollars per transaction and take 3 to 5 business days to settle. Stablecoin transfers cost a few cents regardless of sender or recipient location and clear in minutes. MoneyGram launched a stablecoin-based app in Colombia specifically to demonstrate this advantage in remittance corridors where speed and cost matter most.

For a business sending 100,000 dollars to a vendor across borders, the difference between a 40-dollar wire fee and a few-cent blockchain settlement cost compounds quickly. That’s not marginal savings-that’s material impact on your bottom line. Over the course of a year, a mid-market company processing dozens of cross-border payments can reclaim tens of thousands of dollars through stablecoin settlements.

How Real-Time Settlement Changes Your Cash Flow

Wire transfers create liquidity gaps. Your money leaves your account but doesn’t arrive for days, creating uncertainty about when funds actually clear. Stablecoin transactions settle on-chain within minutes, giving you immediate visibility into whether the payment landed. This matters enormously for treasury operations. You know exactly when cash becomes available on the other side, which means you can optimize working capital management instead of building buffer reserves to account for settlement delays. Visa tested USDC in settlements, and PayPal uses PYUSD for the same reason. These aren’t experiments anymore-they’re live operations. For enterprises managing global payments across multiple currencies and time zones, this shift from batch processing to instant settlement removes friction that has existed in cross-border finance for decades.

Why Institutions Can’t Ignore This Shift

The institutions moving fastest understand that stablecoin adoption isn’t about being trendy. It’s about reclaiming operational efficiency and cash flow that traditional rails waste. Settlement speed translates directly to better working capital management. Cost reduction flows straight to profitability. Real-time visibility into on-chain transactions eliminates reconciliation delays that plague treasury teams. As more financial institutions integrate blockchain infrastructure into their operations, the competitive gap widens between those who act now and those who wait. The next chapter explores how blockchain infrastructure itself is replacing legacy systems that have dominated cross-border payments for decades.

Why Blockchain Infrastructure Matters More Than You Think

SWIFT processes roughly 42 million messages daily, yet the system itself doesn’t move money-it only relays instructions. Banks then settle through correspondent networks that add days to transactions and layer on fees at each hop. Blockchain infrastructure eliminates intermediaries entirely. When you send a stablecoin across borders, the transaction settles on-chain with cryptographic certainty in minutes, and everyone involved sees the same immutable record.

Tokenized Deposits Replace Legacy Settlement Networks

Citi, JPMorgan, and HSBC now offer live tokenized deposit services, moving normal bank deposits via blockchain for the same speed and efficiency stablecoins provide. These aren’t experimental pilots anymore. Tokenized deposits back settlements with actual bank reserves rather than separate crypto collateral, which means institutions get blockchain’s speed advantage without the complexity of managing separate asset classes. JPMorgan’s tokenized deposit trials demonstrated settlement times measured in minutes rather than days, and the audit trail remains complete.

On-Chain Visibility Transforms Reconciliation

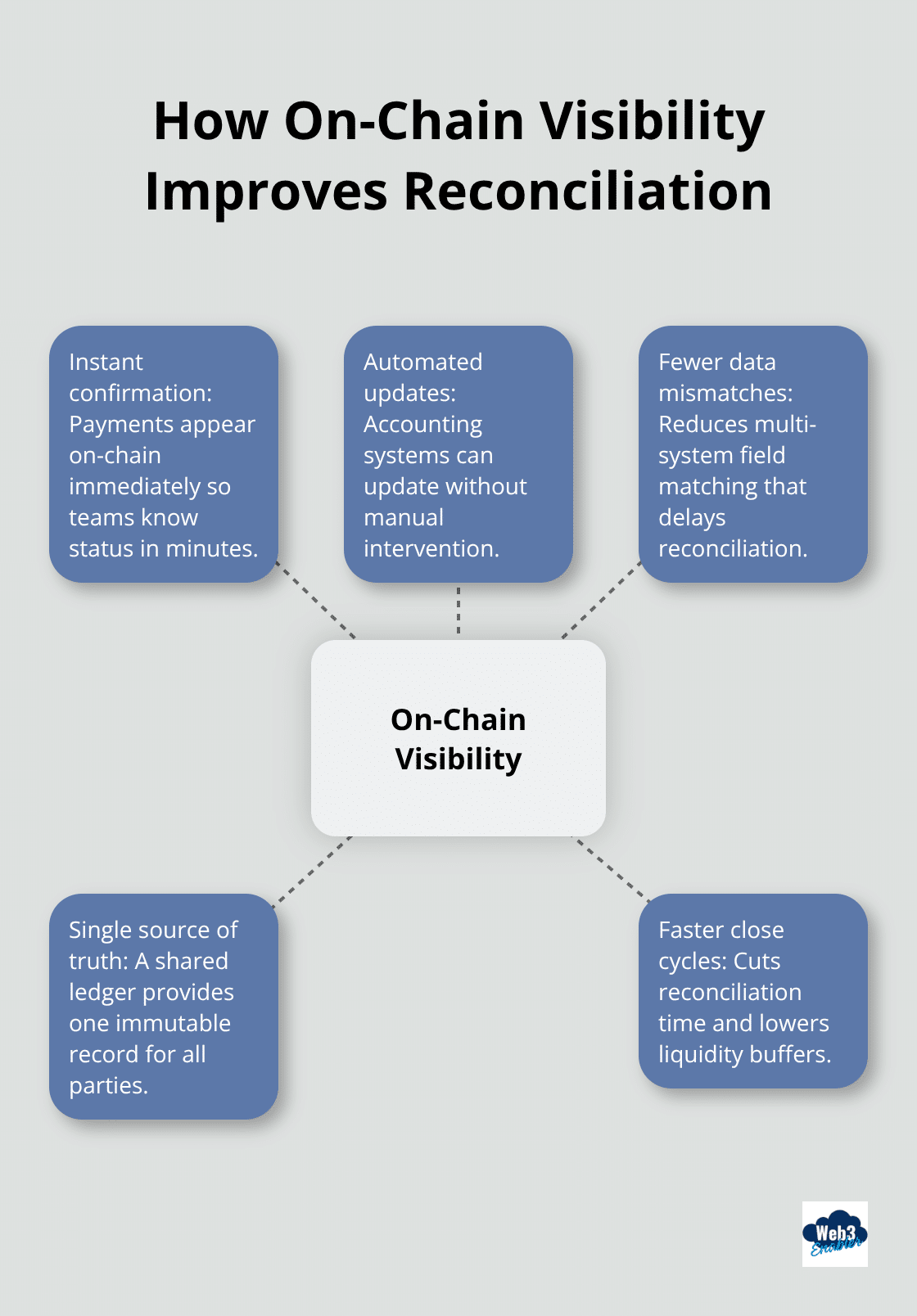

For treasury teams, this shift matters because on-chain visibility transforms reconciliation from a manual, error-prone process into an automated one. Your payment shows up on-chain, confirmation arrives instantly, and your accounting system updates without human intervention. Traditional wire transfers require matching dozens of fields across multiple systems-correspondent bank confirmations, nostro account updates, currency conversion records. One mismatch delays the entire reconciliation.

Blockchain removes that friction.

Real-time visibility into on-chain transactions means treasury teams know exactly when liquidity arrives, eliminating the buffer reserves that companies maintain to account for settlement uncertainty. A mid-market business holding 500,000 dollars in excess reserves to cover the float on outstanding cross-border payments can reclaim that capital for operations or investment.

Institutions Move From Pilots to Production

The institutional movement away from legacy networks isn’t gradual-it’s accelerating because the operational advantages compound. When MoneyGram launched its stablecoin-based remittance app in Colombia, it wasn’t testing a concept. The company was solving a real problem: customers needed money faster, and traditional corridors couldn’t deliver. Blockchain infrastructure handles that demand at a fraction of the cost.

Regulatory frameworks in major markets now provide the certainty institutions needed to move from pilots to production. The GENIUS Act, passed in the US in July 2025, created a regulatory pathway for stablecoins in cross-border payments that removed the ambiguity holding back enterprise adoption. When regulatory clarity arrives, institutions don’t wait-they move.

The Competitive Advantage Belongs to Early Movers

Over the next year, expect to see more financial institutions integrate blockchain infrastructure into their core treasury operations, not as an alternative to traditional rails but as the primary settlement mechanism for specific corridors and payment types. Organizations that treat blockchain infrastructure as a core capability rather than an experimental side project will pull ahead of competitors still relying on correspondent networks. This shift in how enterprises settle payments globally sets the stage for the regulatory frameworks that are now making institutional adoption not just possible, but inevitable.

Regulatory Frameworks Are Making Enterprise Adoption Non-Negotiable

The GENIUS Act, passed in July 2025, fundamentally changed how enterprises approach cross-border payments. This legislation created a US regulatory framework that explicitly permits stablecoins in cross-border settlements, removing the ambiguity that kept most institutions in pilot mode for years. When regulatory clarity arrives at this scale, institutions move forward immediately. Financial services teams that spent 2023 and 2024 seeking legal certainty now have it, and the shift from experimental projects to production deployments is already visible.

Institutions Launch Live Services, Not Pilots

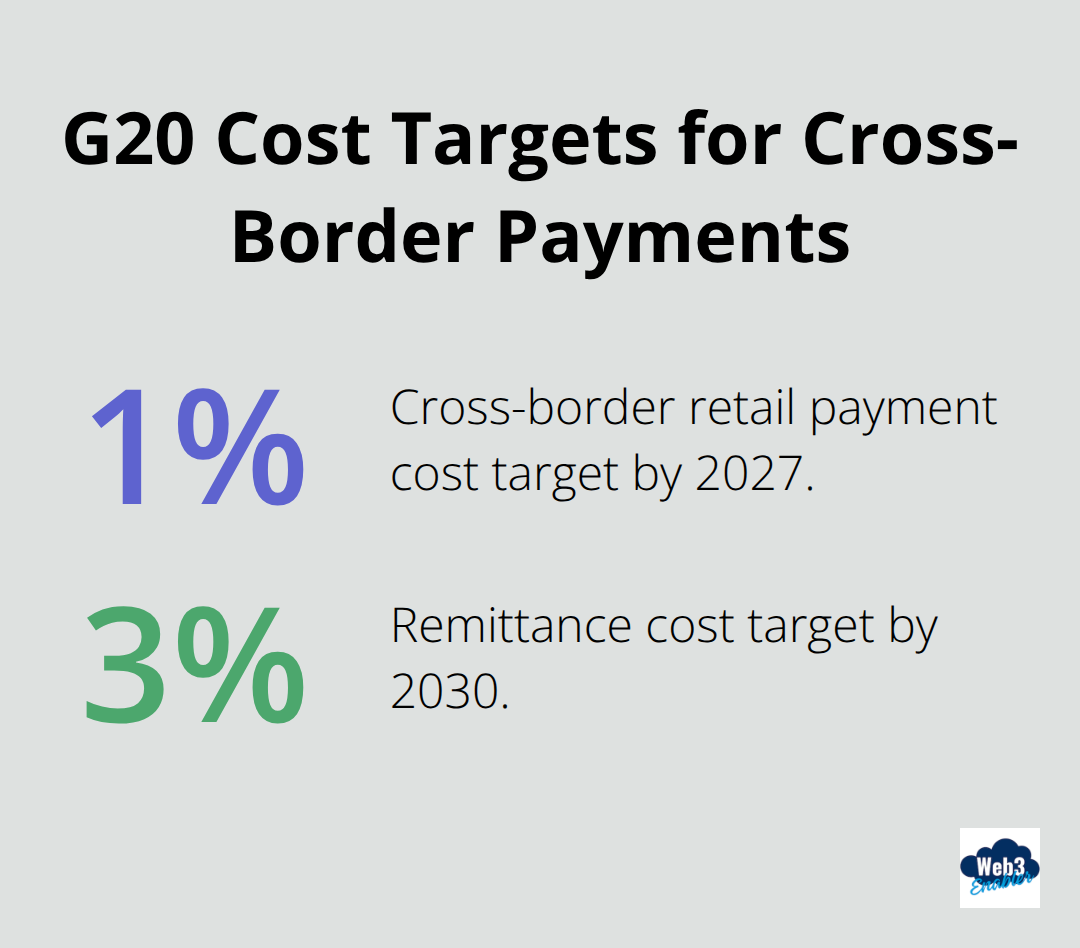

Citi, JPMorgan, and HSBC launched live tokenized deposit services as operational reality, not as proofs of concept. These institutions understand that compliance frameworks are now mature enough to support institutional-grade cross-border payment infrastructure. The G20 has set explicit targets to reduce cross-border retail payment costs to 1% by 2027 and remittance costs to 3% by 2030, which means regulatory bodies worldwide actively push institutions toward faster, cheaper settlement mechanisms.

Compliance Happens in Real Time, Not as a Bottleneck

Compliance integration is no longer an afterthought-blockchain-based payment platforms now include automated sanctions screening, AML checks, and KYC verification that run in parallel with transaction processing. Traditional compliance workflows add days to settlements and create operational bottlenecks. When compliance happens on-chain in real time, transactions move at blockchain speed without regulatory compromise.

Competitive Pressure Accelerates Production Deployments

Financial institutions move from pilots to production because competitive pressure has become real. MoneyGram’s stablecoin app in Colombia was a competitive response to customer demand for faster remittances, not a test case. Remitly and Wise have already demonstrated that digital-first remittance models outperform traditional retail channels, and Western Union expects digital remittances to account for over a quarter of its consumer money transfers revenue in 2025. A proposed 1% US tax on cash-based remittances will accelerate this shift further.

Treasury Teams Gain Months of Operational Advantage

For treasury teams at multinational enterprises, the calculation is straightforward: institutions that integrate blockchain-based settlement now gain months of operational advantage over competitors still waiting for perfect regulatory certainty. That advantage compounds through faster cash cycles, reduced operational costs, and improved working capital management. Organizations that build blockchain payment capabilities into their core treasury operations today will have production-grade experience managing on-chain settlements, compliance workflows, and reconciliation automation before competitors even begin their pilots. A mid-market business processing dozens of cross-border payments annually can reclaim tens of thousands of dollars through stablecoin settlements while competitors remain in evaluation mode.

Regulatory Clarity Removes the Last Barrier

The institutions moving fastest understand that regulatory clarity removes the last barrier to capturing operational advantage that blockchain infrastructure delivers. Organizations that treat blockchain-based settlement as a core capability rather than an experimental side project will pull ahead of competitors still relying on correspondent networks.

Final Thoughts

Cross-border payments trends converge around three operational realities: stablecoins move billions in live transactions, blockchain infrastructure replaces legacy settlement networks, and regulatory frameworks now permit institutional adoption at scale. Organizations that integrate blockchain-based settlement into their core operations today gain months of operational experience before competitors finish their evaluation phases. That head start compounds through faster cash cycles, reduced settlement costs, and improved working capital visibility.

Treasury teams managing dozens of cross-border payments annually reclaim tens of thousands of dollars while gaining real-time visibility into on-chain transactions that traditional wire transfers never provided. Fragmented tools create operational friction-compliance teams work separately from treasury teams, payment data remains disconnected from accounting systems, and on-chain visibility stays isolated from core business processes. We at Web3 Enabler built the only native blockchain platform available on Salesforce AppExchange, enabling financial institutions and enterprises to accept and send stablecoin payments directly within their existing workflows.

Our platform streamlines global settlements and provides real-time visibility into on-chain transactions for faster reconciliation and enhanced liquidity management-all without leaving your CRM. Organizations that treat blockchain-based settlement as a core capability rather than an experimental project pull ahead of competitors still relying on correspondent networks. Move forward with Web3 Enabler and lead the transition instead of following competitors who acted first.