International wire transfers can take days and cost hundreds of dollars. Banks charge steep fees while emerging markets face limited access to global payment networks.

International wire transfers can take days and cost hundreds of dollars. Banks charge steep fees while emerging markets face limited access to global payment networks.

Cross-border crypto payments offer a faster, cheaper alternative. At Web3 Enabler, we’ve seen businesses cut transfer times from days to minutes and reduce costs by up to 90% using stablecoins and blockchain infrastructure.

Why Traditional Cross-Border Payments Remain Expensive and Slow

Wire transfers dominate international business payments, yet they consistently underperform on speed and cost. A standard SWIFT transfer takes three to five business days and charges between $15 and $50 per transaction, with some banks imposing hidden fees that push costs above $100. For businesses sending multiple payments weekly, these delays create cash flow friction and hidden compliance overhead.

Geographic Barriers and Intermediary Costs

Emerging markets face even steeper barriers. Countries in Sub-Saharan Africa, Southeast Asia, and Latin America often lack direct banking corridors, forcing payments through multiple intermediaries that compound fees and add days to settlement. Each intermediary extracts a fee, and each routing decision introduces delay. A payment from the US to Nigeria might pass through four or five correspondent banks before reaching its destination, with each bank taking a cut.

Fragmented Compliance Requirements Across Regions

Compliance frameworks add another layer of complexity. Regulators across jurisdictions enforce different Travel Rule requirements, with the US enforcing a $3,000 threshold under the Bank Secrecy Act, while the EU’s Transfer of Funds Regulation (effective December 2024) requires sender and beneficiary data for every crypto transfer regardless of amount. The UK’s Financial Conduct Authority has enforced Travel Rule obligations since September 2023, and Singapore’s Monetary Authority requires sender and receiver data for every transfer. These fragmented rules mean businesses must navigate conflicting requirements when moving money internationally, often requiring separate compliance programs for different regions.

The Cost Multiplier for SMEs and Recurring Payments

Small and medium enterprises feel these inefficiencies acutely. A business paying 50 contractors across ten countries faces not just transaction fees but also currency conversion spreads that typically involve visible charges and hidden FX markups. Over a year, a company sending $100,000 monthly in cross-border payments loses significant amounts to conversion costs alone, before accounting for wire fees. Payroll processing compounds the problem-many businesses still batch process employee payments weekly or monthly because daily transfers would be prohibitively expensive.

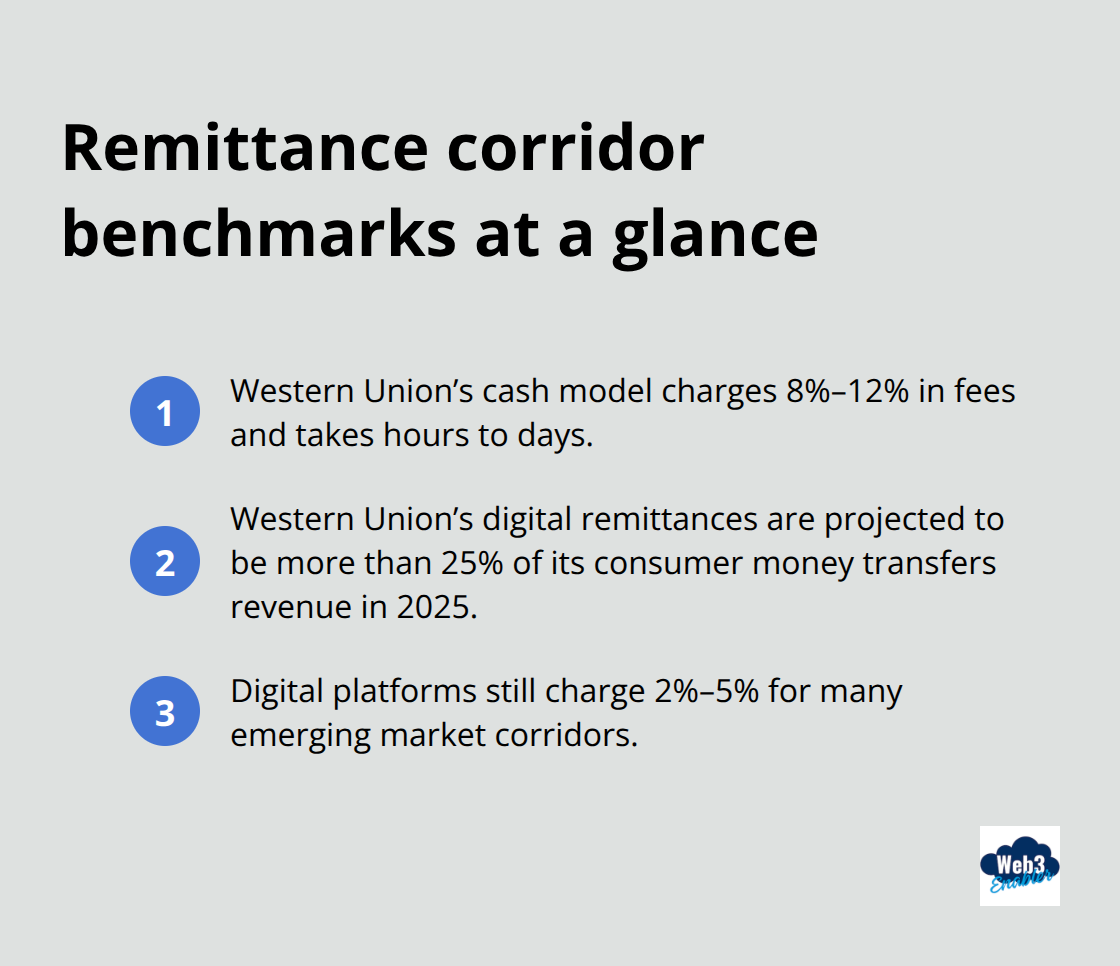

Remittance Corridors Reveal the Worst Outcomes

Remittance corridors reveal the worst outcomes. Western Union’s traditional cash-based model charges 8% to 12% in fees and takes hours to days, making it economically unfeasible for smaller transfers. Digital alternatives have improved this, with Western Union’s digital remittances projected to account for more than 25% of its consumer money transfers revenue in 2025, but even digital platforms charge 2% to 5% for emerging market corridors.

Tokenized infrastructure and stablecoins address these constraints directly. They remove intermediaries, compress settlement windows from days to minutes, and cut fees to under 1% for high-volume corridors. The regulatory clarity provided by the GENIUS Act (signed into law on July 18, 2025) has enabled major cross-border players like Corpay, dLocal, MoneyGram, and Rapyd to move beyond pilot phases and deploy stablecoin solutions into production. This shift signals that the cost and speed advantages are now operationally achievable for businesses at scale, and understanding how these solutions actually work becomes essential for any organization evaluating its payment infrastructure.

How Stablecoins and Blockchain Speed Up International Transfers

Stablecoins solve the volatility problem that makes ordinary cryptocurrencies impractical for business payments. A stablecoin like USDC or USDT maintains a fixed value pegged to the US dollar, eliminating the price swings that would turn a $10,000 payment into $9,500 or $10,500 by the time it settles. This stability makes stablecoins viable for payroll, vendor invoices, and remittances where predictable amounts matter. The mechanics are straightforward: a sender transfers stablecoins from their wallet to a recipient’s wallet on the blockchain, and the transaction settles in minutes rather than days. No intermediary banks, no currency conversion delays, no hidden fees extracted at each step. For a business paying contractors in five countries, this means moving money in a single transaction type rather than managing five separate wire transfer corridors with five different fee structures and five different settlement windows.

Why Settlement Speed Matters for Cash Flow

Blockchain settlement in international payments happens in minutes because transactions are validated and recorded on a distributed ledger without waiting for correspondent banks to clear funds. A SWIFT transfer from the US to Singapore takes three to five business days because the payment must pass through multiple banking intermediaries, each with their own processing windows and cutoff times. A stablecoin transfer across the same corridor completes in under five minutes. For a business with weekly payroll cycles across multiple countries, this speed advantage compounds. Payroll processed on Friday via stablecoin reaches employees’ accounts the same day or Monday morning, while traditional wires might not settle until Wednesday or Thursday. The practical impact is immediate: employees in emerging markets can access funds faster, reducing friction and improving retention.

Settlement times for traditional rails vary dramatically by corridor and method. ACH transfers in the US take one to three business days and cost under $1 per transaction. SEPA transfers in the Eurozone settle in one business day and cost virtually nothing. SWIFT transfers to emerging markets take five to seven business days and cost $15 to $100 depending on the destination and banks involved. On-chain stablecoin transfers settle in seconds or minutes and often cost cents to a few dollars, even for meaningful sums, making them economically superior for high-frequency, cross-border payments.

Fee Structure Reveals Where Crypto Cuts Costs

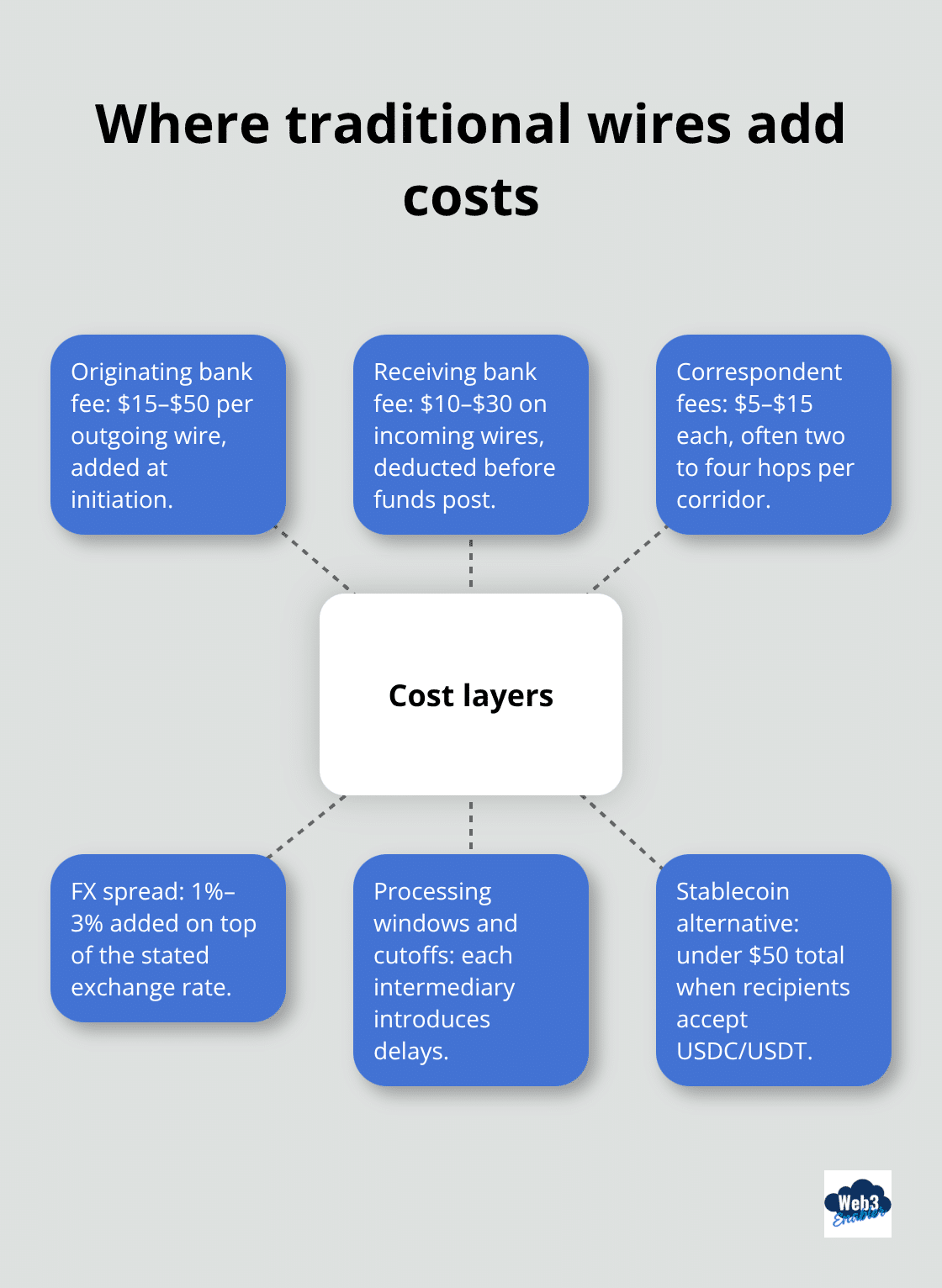

A traditional wire transfer incurs multiple layers of fees that compound across corridors. The originating bank charges an outgoing wire fee of $15 to $50. The receiving bank charges an incoming wire fee of $10 to $30. Correspondent banks extract fees for routing and processing, typically $5 to $15 each, with major corridors involving two to four correspondent banks.

Currency conversion spreads add another 1% to 3% on top of the stated exchange rate. A $50,000 payment from the US to Brazil via SWIFT might incur $200 in explicit fees plus $500 to $1,500 in hidden conversion spreads, totaling $700 to $1,700 in costs. The same payment via stablecoin costs under $50 in blockchain transaction fees and conversion costs combined, assuming the recipient accepts USDC or USDT directly.

If conversion to local currency is required, a stablecoin-to-fiat rail adds another 0.5% to 1%, bringing total costs to under $300. That gap compounds rapidly. A business sending $100,000 monthly across ten corridors saves $8,400 to $17,000 annually by switching from wires to stablecoin rails. For SMEs operating on thin margins, that saving is material. Larger enterprises moving millions monthly see six-figure annual savings.

Regulatory Clarity Enables Production Deployments

The GENIUS Act’s passage in July 2025 removed regulatory uncertainty around stablecoin use in US cross-border payments. This clarity allowed major players like Corpay, dLocal, MoneyGram, and Rapyd to move beyond pilot phases and deploy stablecoin solutions into production. Businesses can now evaluate stablecoin infrastructure as a standard payment option rather than an experimental technology, with vendor options expanding and pricing becoming competitive. The shift from exploratory interest to concrete product deployments signals that the cost and speed advantages are operationally achievable at scale.

Understanding how these solutions integrate with existing business systems becomes essential for any organization evaluating its payment infrastructure. The next section examines real-world applications and shows how businesses across different industries are capturing these benefits.

How Businesses Actually Use Stablecoins for International Payments

Payroll Acceleration Across Emerging Markets

Payroll departments at multinational companies face a recurring problem: employees in emerging markets wait days for salary deposits while finance teams juggle multiple wire corridors with conflicting cutoff times. A software company with developers in Nigeria, Philippines, and Mexico processes payroll on Friday but doesn’t see funds settle until the following Wednesday or Thursday through traditional banking. Switching to stablecoin rails compresses this timeline dramatically. Payments initiated Friday morning settle the same day, with employees accessing funds within hours rather than days.

The cost advantage proves equally compelling. Traditional wires to these corridors average $40 to $80 per employee plus currency conversion spreads of 1% to 3%. A company paying 50 contractors across these countries spends roughly $2,000 to $4,000 monthly in explicit fees alone, plus another $1,500 to $4,500 in hidden conversion costs. Stablecoin transfers cost under $50 total and eliminate conversion spreads if recipients accept USDC or USDT directly. For annual payroll cycles, this translates to $18,000 to $102,000 in savings.

Vendor Payments and Supply Chain Visibility

Vendors and suppliers benefit similarly from stablecoin infrastructure. A manufacturer ordering components from suppliers across Southeast Asia typically waits three to five business days for payment confirmation, creating working capital uncertainty. Stablecoin transfers settle in seconds, giving suppliers immediate confirmation and improving cash flow visibility across the supply chain. This speed advantage reduces friction in procurement cycles and strengthens supplier relationships by eliminating payment delays.

Remittance Corridors and Worker Transfers

Remittance flows show even starker improvements. Traditional remittance platforms charge 8% to 12% for emerging market corridors, making small transfers economically unfeasible. Digital-first platforms like Remitly report that their digital remittance revenue shares exceed 60%, with stablecoin-based alternatives like MoneyGram’s offering in Colombia pushing fees below 2%. For a migrant worker sending $500 monthly to family, this difference means $480 to $540 annually stays in the recipient’s pocket rather than disappearing into fees.

Integration with Existing Business Systems

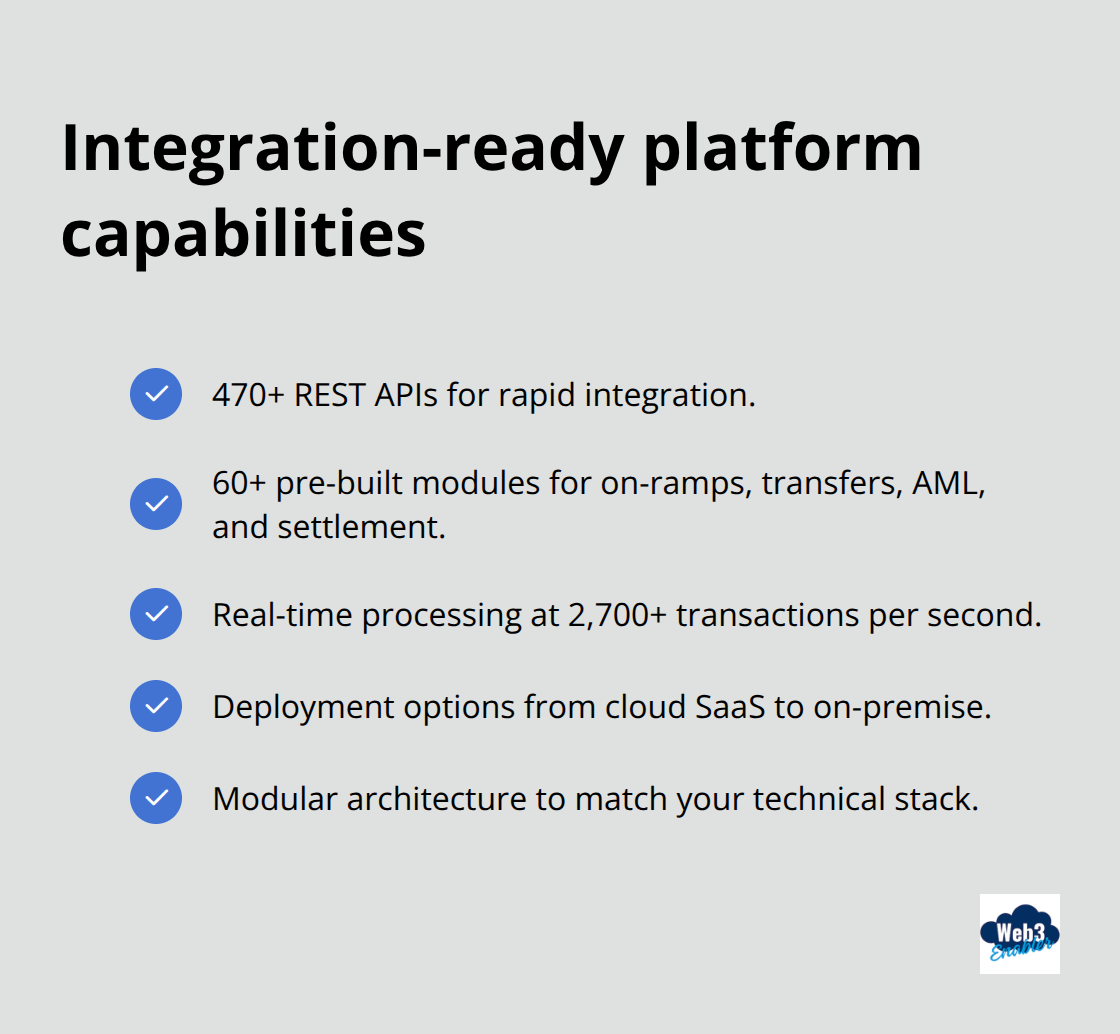

Integration with existing business systems determines whether these benefits translate into operational reality. Stablecoin infrastructure requires banking integrations, compliance controls, and ledger connections that sound complex but are increasingly standardized. White-label platforms like SDK.finance offer modular components with 470+ REST APIs and 60+ pre-built modules covering fiat on-ramps, stablecoin transfers, AML screening, and settlement. These platforms support real-time processing at 2,700+ transactions per second and offer deployment options ranging from cloud SaaS to on-premise infrastructure, allowing companies to match their technical architecture.

The compliance layer is non-negotiable. Travel Rule obligations vary by jurisdiction, with the US enforcing a $3,000 threshold, the EU applying zero thresholds as of December 2024, and Singapore requiring data for every transfer. A pragmatic approach involves designing compliance programs around the strictest requirements to avoid gaps across regions. Robust audit trails, standardized data-sharing protocols, and strong encryption become operational necessities rather than optional controls. Companies moving from traditional wires to stablecoins should implement Travel Rule data retention for five to ten years, matching BSA requirements and EU/UK practice.

Vendor Selection and Implementation Strategy

Evaluate stablecoin infrastructure against your current wire corridor costs and settlement timelines. Calculate annual savings by comparing explicit fees, conversion spreads, and operational overhead across your highest-volume corridors. If annual cross-border volume exceeds $1 million, stablecoin rails typically pay for themselves within months. For lower volumes, the operational simplification alone justifies the switch.

Platforms offering compliance-ready infrastructure with pre-integrated banking partners and modular architecture reduce implementation time from 12-24 months to 3-6 months. Request certifications like PCI DSS Level 1 and ISO 27001:2022, confirmation of banking partnerships, and transparent fee structures before committing. Web3 Enabler, as a Salesforce ISV partner, provides 100% Salesforce Native blockchain solutions that connect stablecoin payments directly with your existing corporate infrastructure, enabling faster implementation for organizations already using Salesforce.

Final Thoughts

Cross-border crypto payments deliver three concrete advantages that traditional banking cannot match: speed measured in minutes rather than days, costs reduced by 80% to 90% on high-volume corridors, and access to payment rails that work regardless of geographic location or banking infrastructure. Stablecoins eliminate volatility while blockchain settlement removes intermediaries entirely. The GENIUS Act’s passage in July 2025 transformed this from experimental technology into operational reality, with major players like Corpay, dLocal, MoneyGram, and Rapyd now running production stablecoin solutions.

Calculate your current cross-border costs by adding explicit wire fees, conversion spreads, and operational overhead across your highest-volume corridors. If annual volume exceeds $1 million, stablecoin infrastructure typically pays for itself within months. Evaluate vendors against your compliance requirements, focusing on Travel Rule capabilities, banking partnerships, and certifications like PCI DSS Level 1 before piloting a single corridor with moderate volume.

Web3 Enabler provides a direct path forward for organizations already using Salesforce through 100% Salesforce Native blockchain solutions that connect stablecoin payments directly with your existing corporate infrastructure. Our platform supports payments, compliance, and automation while backed by trusted partners including Circle, Ripple, and Cardano Catalyst. Stablecoin adoption will accelerate through 2026 as regulatory frameworks mature and more businesses recognize the operational and financial advantages of cross-border crypto payments.