B2B crypto payments are reshaping how companies handle vendor transactions across borders. Traditional banking infrastructure still dominates corporate payments, but it’s built on outdated systems that create friction, delay settlements, and drain budgets through hidden fees.

At Web3 Enabler, we’ve seen firsthand how blockchain-based solutions eliminate these bottlenecks. This post explores how crypto payments accelerate vendor transactions, reduce costs, and integrate seamlessly into existing business operations.

Why Traditional B2B Payments Still Drain Corporate Budgets

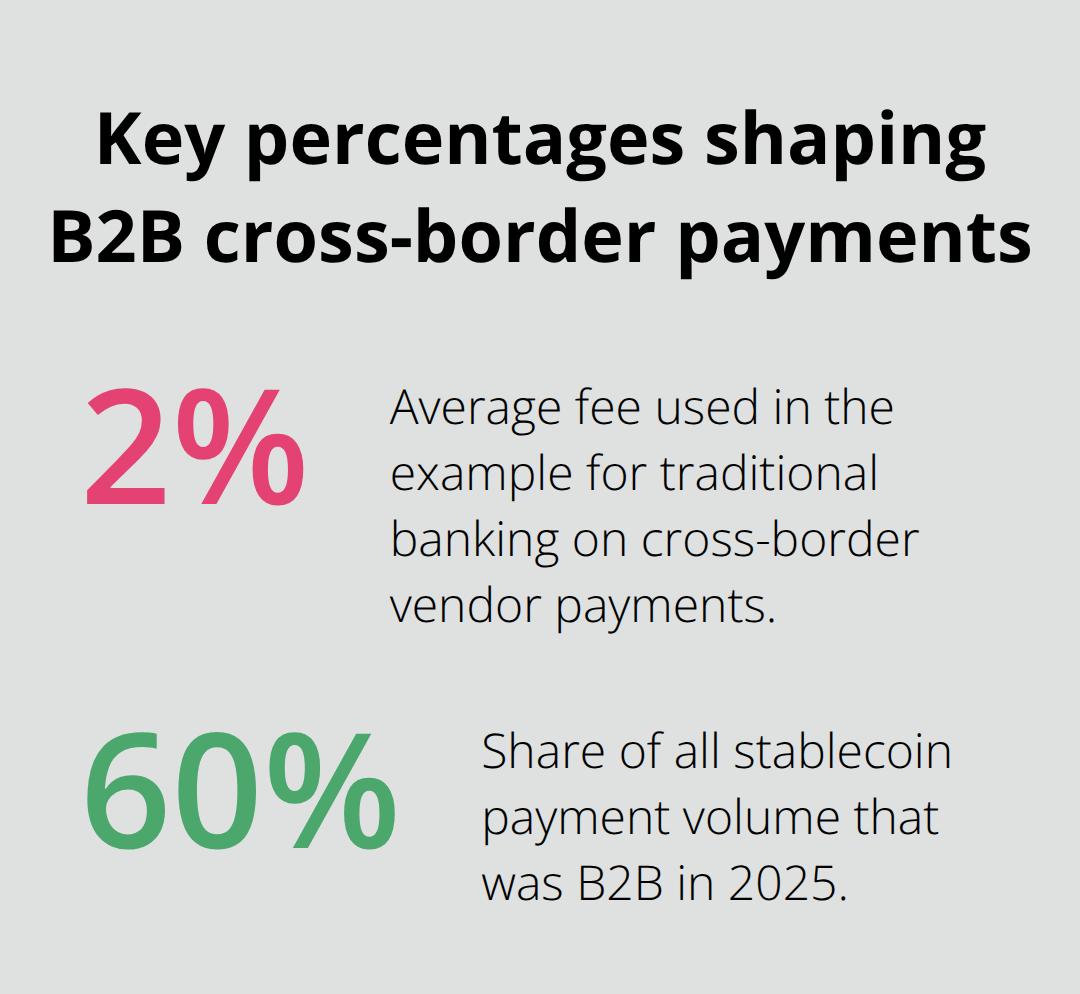

Corporate payments move through a maze of intermediaries, each taking a cut. A wire transfer to a supplier in Kenya or the Philippines involves correspondent banks, local clearing houses, and currency conversion spreads that stack up quickly. The World Bank reports that average remittance fees sit around 6.49%, but B2B cross-border payments often exceed this, especially for smaller transactions under $10,000. A company paying ten contractors across five countries each month faces fees that compound throughout the year. Wire transfers typically settle in 1–5 business days, meaning cash tied up in transit represents working capital that could fund operations or growth. For a mid-market company processing $5 million in annual vendor payments, even a 2% fee difference translates to $100,000 in unnecessary costs. Hidden charges emerge during currency conversion, where banks apply undisclosed spreads on top of the interbank rate, sometimes 1–3% higher than the actual market price.

The Real Cost of Delayed Settlement

Settlement delays create a cascading problem for treasury teams. When a payment leaves on Monday but settles Thursday, the supplier hasn’t received funds, yet the sending company’s cash is already debited. This gap forces businesses to maintain larger working capital reserves and complicates reconciliation across multiple accounting systems. Companies operating in Africa and Southeast Asia face even longer delays due to limited banking infrastructure. In high-volume corridors like Nigeria or the Philippines, traditional rails can take 5–7 business days for cross-border payments to clear. Settlement on blockchain networks ranges from 10 minutes to 2 hours depending on the chain-a massive improvement over banking timelines. For treasury operations managing payroll, supplier invoices, and contractor payments, near-instant settlement means better cash visibility and reduced operational overhead.

Why Blockchain Offers a Different Path

Stablecoins eliminate the intermediary problem that traditional banking creates. A payment on blockchain settles directly between sender and receiver without correspondent banks or clearing houses taking cuts along the way. This direct settlement path reduces conversion spreads and removes hidden fees that accumulate in multi-bank flows. Companies that shift vendor payments to stablecoin rails report settlement times measured in minutes rather than days, which transforms how they manage cash flow and supplier relationships. The cost structure changes fundamentally: instead of layered FX charges and processing fees, businesses pay only a network fee plus a defined conversion spread (typically under 1% for established providers). For global businesses processing high-volume vendor transactions, this cost difference directly boosts margins and profitability.

How Crypto Payments Work for Vendors

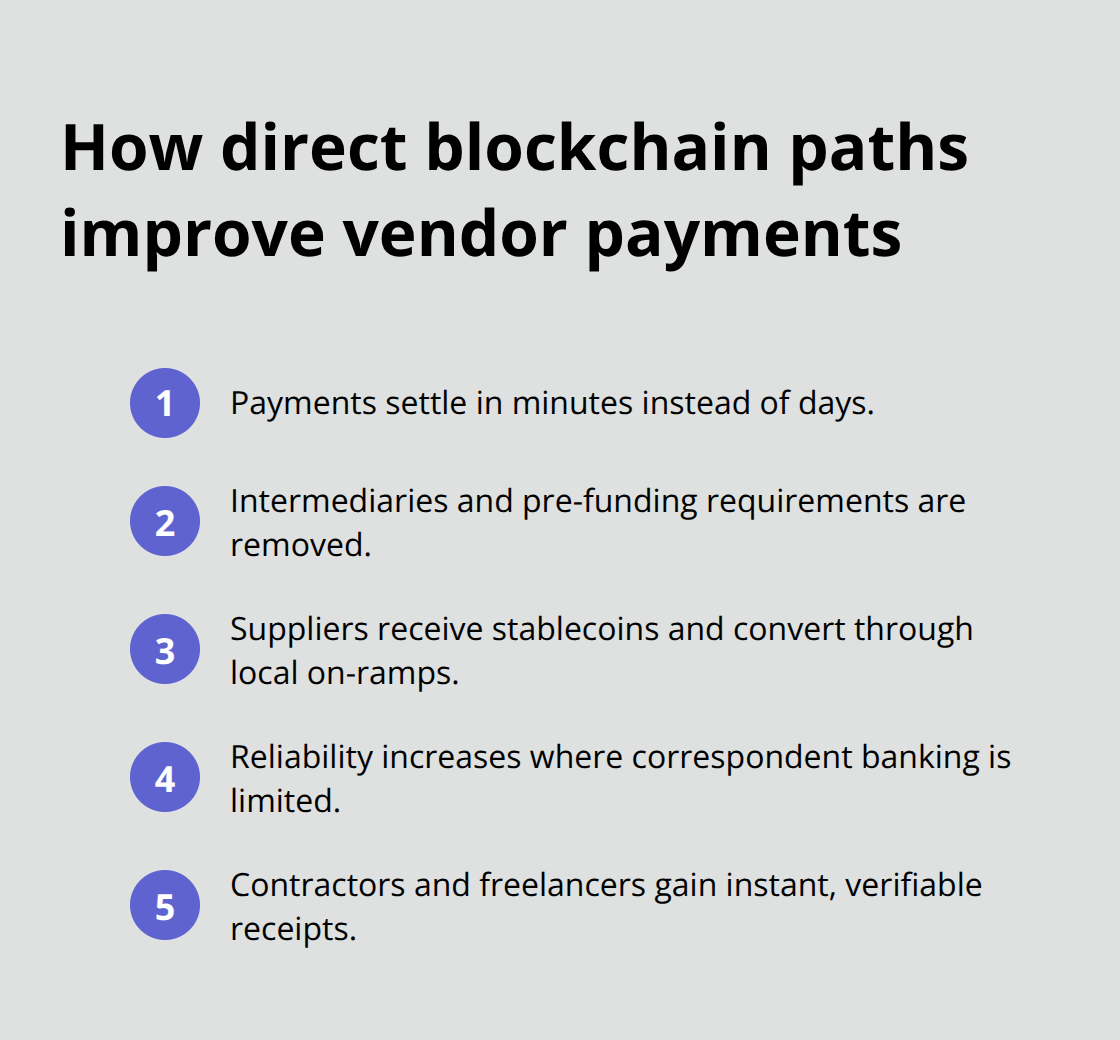

Stablecoin-based vendor payments operate on a fundamentally different architecture than traditional banking. When a company pays a supplier using blockchain rails, the transaction settles on-chain in minutes, eliminating the multi-day clearing cycle that characterizes wire transfers. Settlement on public blockchains ranges from 10 minutes to 2 hours depending on the network, compared to the 1–5 business day standard for traditional cross-border payments. This speed transforms treasury operations: teams gain immediate visibility into payment status, suppliers receive funds faster and reinvest sooner, and reconciliation becomes straightforward because blockchain records are immutable and transparent. For companies processing payroll or invoices across multiple countries, near-instant settlement reduces the working capital buffer required to cover in-flight payments. A mid-market firm paying contractors in Nigeria, Kenya, or the Philippines no longer needs to front cash for 5–7 days while traditional rails clear. Instead, funds arrive within hours, improving cash flow predictability and reducing the operational complexity of tracking payments across legacy banking systems.

The Fee Model Shifts Dramatically on Blockchain

The cost structure for stablecoin payments differs radically from traditional banking. Instead of correspondent bank charges, local clearing fees, currency conversion spreads, and processing costs stacked on one another, businesses pay only a network fee plus a defined conversion spread, typically under 1% for established providers. This transparency matters: a company calculates the exact cost of paying a $50,000 invoice to a supplier before execution, rather than discovering hidden charges days later during reconciliation. For high-volume corridors, the savings compound quickly. A business processing $5 million annually in cross-border vendor payments at an average fee of 2% through traditional banking saves $50,000 yearly when switching to stablecoin rails at under 1%. Larger organizations moving $50 million or more in annual supplier payments see savings in the hundreds of thousands. Integration with existing corporate infrastructure streamlines this process, connecting blockchain transactions directly to your business systems and eliminating manual reconciliation that adds invisible costs to traditional payment workflows.

Direct Paths Between Sender and Receiver Eliminate Intermediaries

Blockchain payments remove the intermediaries that traditionally stand between sender and receiver. A company paying a supplier in a developing market no longer routes payments through multiple correspondent banks or arranges pre-funding across jurisdictions. The supplier receives stablecoins directly into a wallet, then converts to local currency if needed through local fiat on-ramps. This direct path proves particularly valuable in Africa and Southeast Asia, where correspondent banking relationships are limited and pre-funding requirements force companies to lock capital across multiple regions.

Suppliers gain agency: they choose when and where to convert stablecoins to local currency rather than waiting for funds to arrive through channels outside their control. For contractor and freelancer payments, this matters significantly. A developer in the Philippines or a content creator in Nigeria receives payment instantly, verifies receipt on-chain, and avoids the delays and uncertainty of traditional remittance services. Companies integrating stablecoin payments into their vendor management systems report faster invoice approval cycles and improved supplier satisfaction because payment certainty increases.

Settlement Speed Reshapes Working Capital Management

The operational impact of faster settlement extends beyond individual transactions. Treasury teams managing multiple payment streams across regions gain real-time visibility into fund movements, reducing the reconciliation work that consumes hours each week in traditional banking environments. When payments settle in hours rather than days, companies maintain smaller cash reserves dedicated to in-flight transactions, freeing capital for operations or growth investments. Suppliers in emerging markets benefit equally: faster payment receipt means they can meet their own obligations sooner, strengthening their cash positions and reducing their reliance on expensive short-term financing. This efficiency cascades through supply chains, particularly in regions where working capital constraints limit supplier capacity. A manufacturing company paying component suppliers across West Africa experiences fewer payment disputes and smoother operations when settlement occurs within hours rather than weeks. The predictability of blockchain settlement also simplifies financial forecasting, allowing treasury teams to model cash positions with greater accuracy and confidence.

Vendor Relationships Strengthen Through Payment Certainty

Direct blockchain settlement creates a foundation for stronger vendor relationships. Suppliers receive transparent, immutable proof of payment on-chain, eliminating disputes about whether funds were sent or when they will arrive. This certainty matters especially in markets where banking infrastructure is unreliable or where suppliers have experienced payment delays from international partners. A vendor in Nigeria or Kenya can verify payment receipt independently without relying on bank notifications or intermediary confirmations. Companies that adopt stablecoin payments for vendor transactions report improved supplier engagement and faster response times to orders because vendors trust that payment will arrive as promised. For global companies managing hundreds of suppliers across multiple regions, this trust translates into better terms, faster fulfillment, and reduced friction in procurement cycles. The next section examines how companies structure their implementation to capture these benefits while managing compliance and operational integration.

Where Stablecoins Deliver the Biggest Impact

Global companies face three payment bottlenecks that stablecoins address directly: suppliers scattered across regions with weak banking infrastructure, contractors and freelancers operating in markets where traditional remittances are expensive, and treasury teams managing cash positions across multiple currencies and time zones. McKinsey and Artemis Analytics data shows that B2B stablecoin payments reached $226 billion in 2025, representing about 60% of all stablecoin payment volume with year-over-year growth of approximately 733%. This growth reflects real operational wins, not speculation.

Manufacturing and Regional Supplier Networks

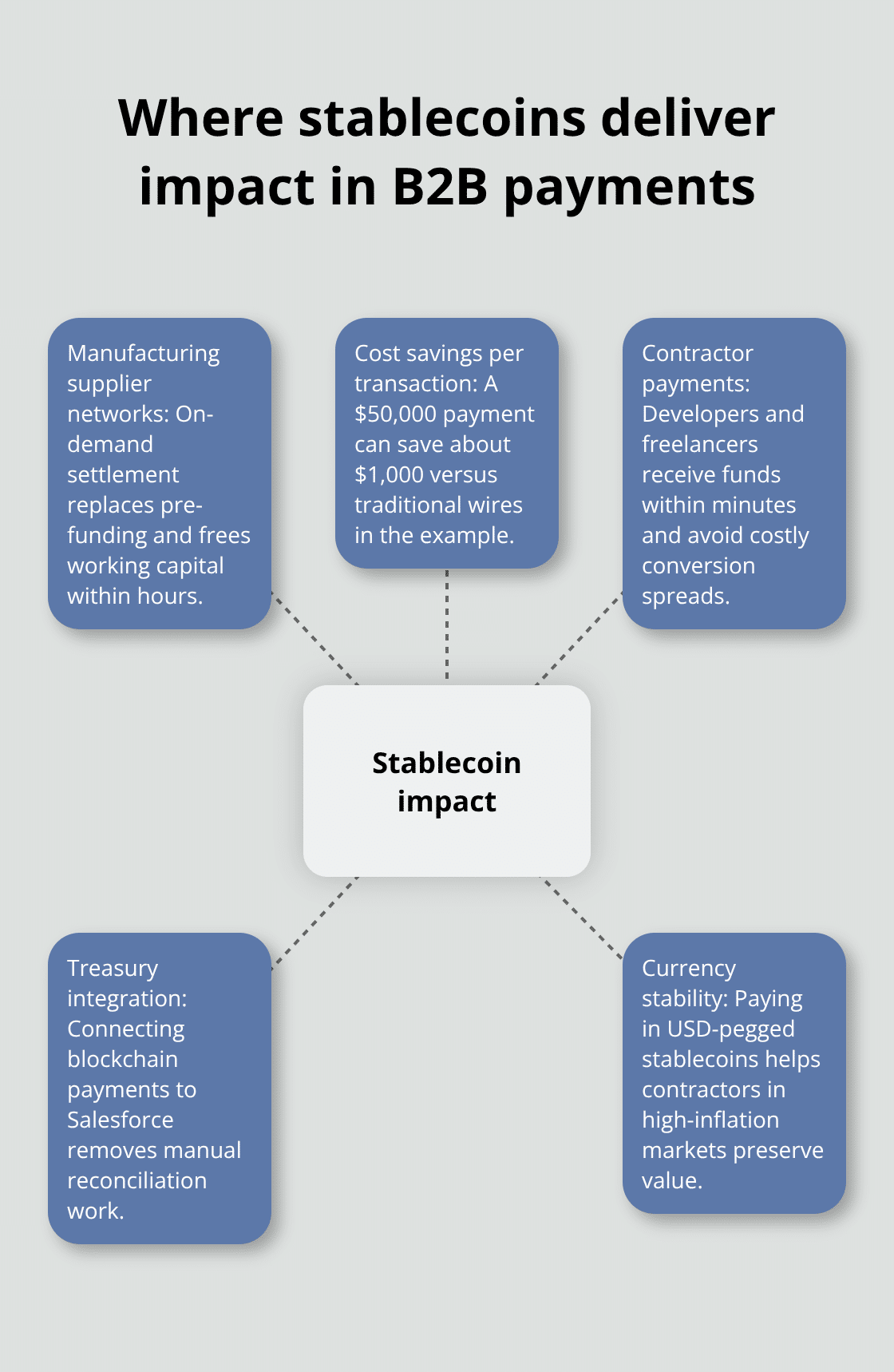

A manufacturing company paying component suppliers across West Africa eliminates the need to pre-fund accounts in multiple jurisdictions, a practice that forces businesses to lock capital in regions where banking relationships are limited. Instead of maintaining reserves in Kenya, Nigeria, and Ghana to cover supplier payments, the company executes transactions on-demand, converting stablecoins to local currency at the point of settlement. This shift reduces working capital tied up in cross-border transit from weeks to hours. For a company processing $10 million annually in regional supplier payments, faster settlement alone frees $200,000 to $500,000 in operational capital.

The mathematics favor stablecoin rails decisively: traditional cross-border B2B payments cost between 1.5% and 3% depending on corridor and amount, while stablecoin providers charge under 1% in network fees and conversion spreads combined. A $50,000 payment to a supplier costs $1,500 via traditional wire but under $500 using stablecoin rails, saving $1,000 per transaction. Over a year, a company processing 100 such transactions saves $100,000 in direct payment costs.

Contractor and Freelancer Compensation

Contractor and freelancer payments expose the inefficiency of traditional remittance services most clearly. A software developer in the Philippines working for a US agency currently waits 3 to 5 business days for wire transfer funds to arrive, and depending on the receiving bank, may face conversion spreads of 2% to 4%. With stablecoins, payment settles within minutes; the developer receives USDC or USDT directly into a wallet, then converts to Philippine pesos through local on-ramps like Coins.ph, which launched the regulated PHPC peso-backed stablecoin in 2025. This direct path eliminates intermediaries and reduces the total cost of the transaction.

Treasury Operations and Integrated Systems

For treasury teams managing payroll and invoicing across multiple countries, stablecoin integration into business systems creates visibility that traditional banking cannot match. Web3 Enabler connects blockchain transactions directly to Salesforce, allowing treasury teams to track contractor payments, supplier invoices, and currency conversions within their existing platform. This integration eliminates the manual reconciliation work that adds hidden overhead to traditional payment workflows. A finance team no longer spends hours cross-referencing bank statements with accounting records; blockchain settlement provides transparent, immutable proof of payment that reconciles automatically.

Currency Stability in Volatile Markets

For companies operating in high-inflation economies like Nigeria or Argentina, stablecoins serve an additional function: currency hedges that protect payment value during transit. A contractor in Lagos receiving payment in USDC maintains purchasing power independent of Nigerian naira volatility, removing the risk that currency fluctuations will reduce real compensation. This stability matters particularly for long-term vendor relationships where price certainty enables better planning on both sides (supplier confidence increases, payment disputes decrease, and operational friction diminishes across the supply chain).

Final Thoughts

B2B crypto payments transform how companies manage vendor transactions, contractor compensation, and treasury operations across borders. Settlement occurs in hours instead of days, costs drop below 1% instead of 2–3%, and transparent on-chain records eliminate reconciliation overhead that consumes finance teams’ time. For global organizations processing millions in annual supplier payments, these improvements free working capital, reduce operational complexity, and build vendor relationships on payment certainty rather than banking delays.

Implementation requires identifying high-volume payment corridors where cost savings compound fastest, then piloting stablecoin rails with a subset of suppliers before scaling across your vendor base. Compliance matters: your provider must maintain proper licensing, conduct AML/KYC screening, and disclose liquidity sources and fiat banking partners clearly. Integration with existing systems determines whether adoption succeeds or stalls-manual workarounds add hidden costs that offset the efficiency gains blockchain settlement provides.

Western Union, MoneyGram, PayPal, and Stripe have all integrated stablecoin infrastructure into their payment systems because the efficiency gains prove undeniable. Financial leaders now face a strategic choice: whether your organization leads or follows as B2B crypto payments reshape corporate finance. Web3 Enabler connects blockchain transactions directly to Salesforce, allowing your treasury team to track payments, manage invoices, and handle contractor compensation within the platform you already use.