Your business is bleeding money through outdated payment methods. Cash gets lost, checks take forever, and your customers are already shopping elsewhere because you won’t accept their preferred payment options.

Your business is bleeding money through outdated payment methods. Cash gets lost, checks take forever, and your customers are already shopping elsewhere because you won’t accept their preferred payment options.

The importance of digital payments isn’t some future trend-it’s happening right now. At Web3 Enabler, we’ve watched businesses transform their operations by ditching legacy systems, and the results speak for themselves: faster transactions, happier customers, and actual visibility into what’s happening with your money.

Why Businesses Are Ditching Legacy Payment Systems

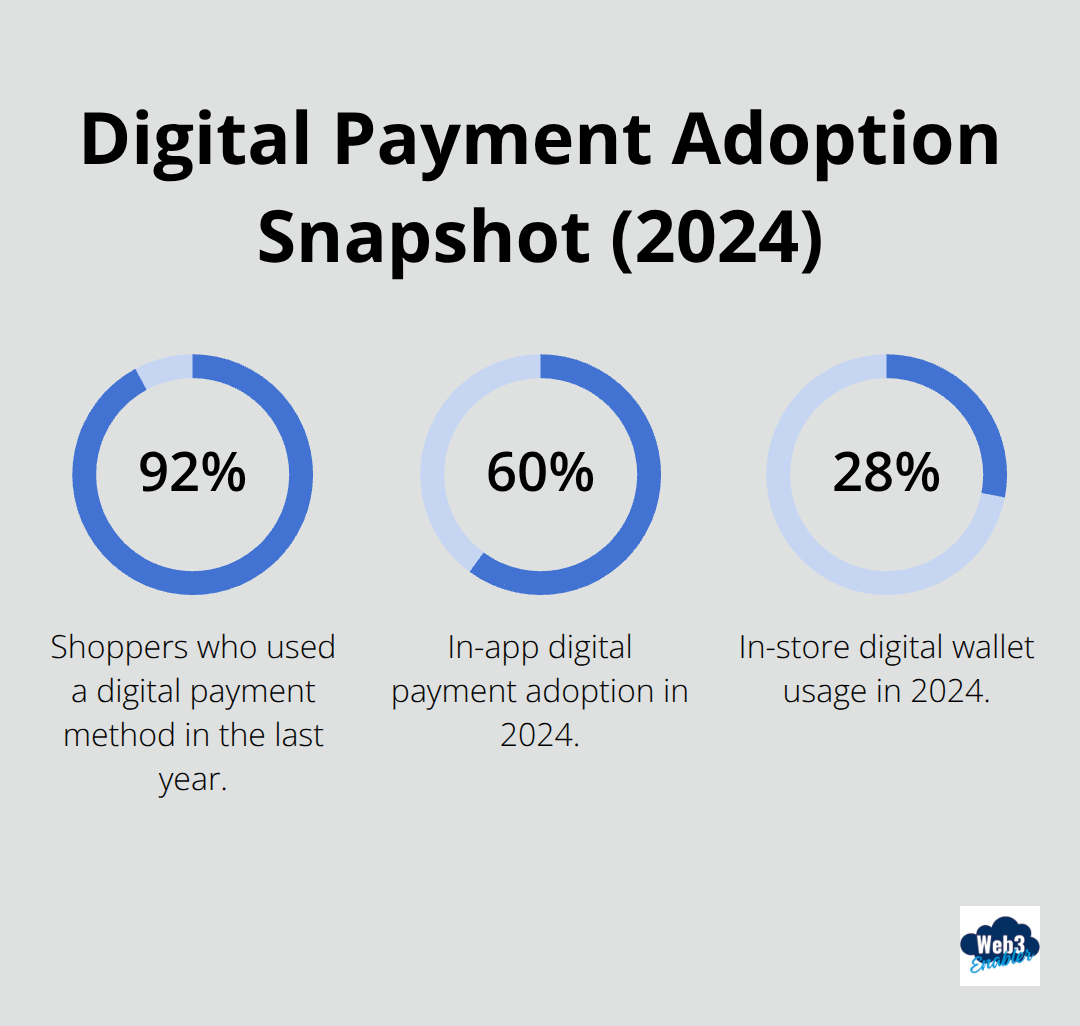

Your competitors aren’t waiting around for checks to clear. According to McKinsey research from 2024, 92% of shoppers used a digital payment method in the last year, and that number keeps climbing. Businesses that still rely heavily on cash and checks are essentially running against the current.

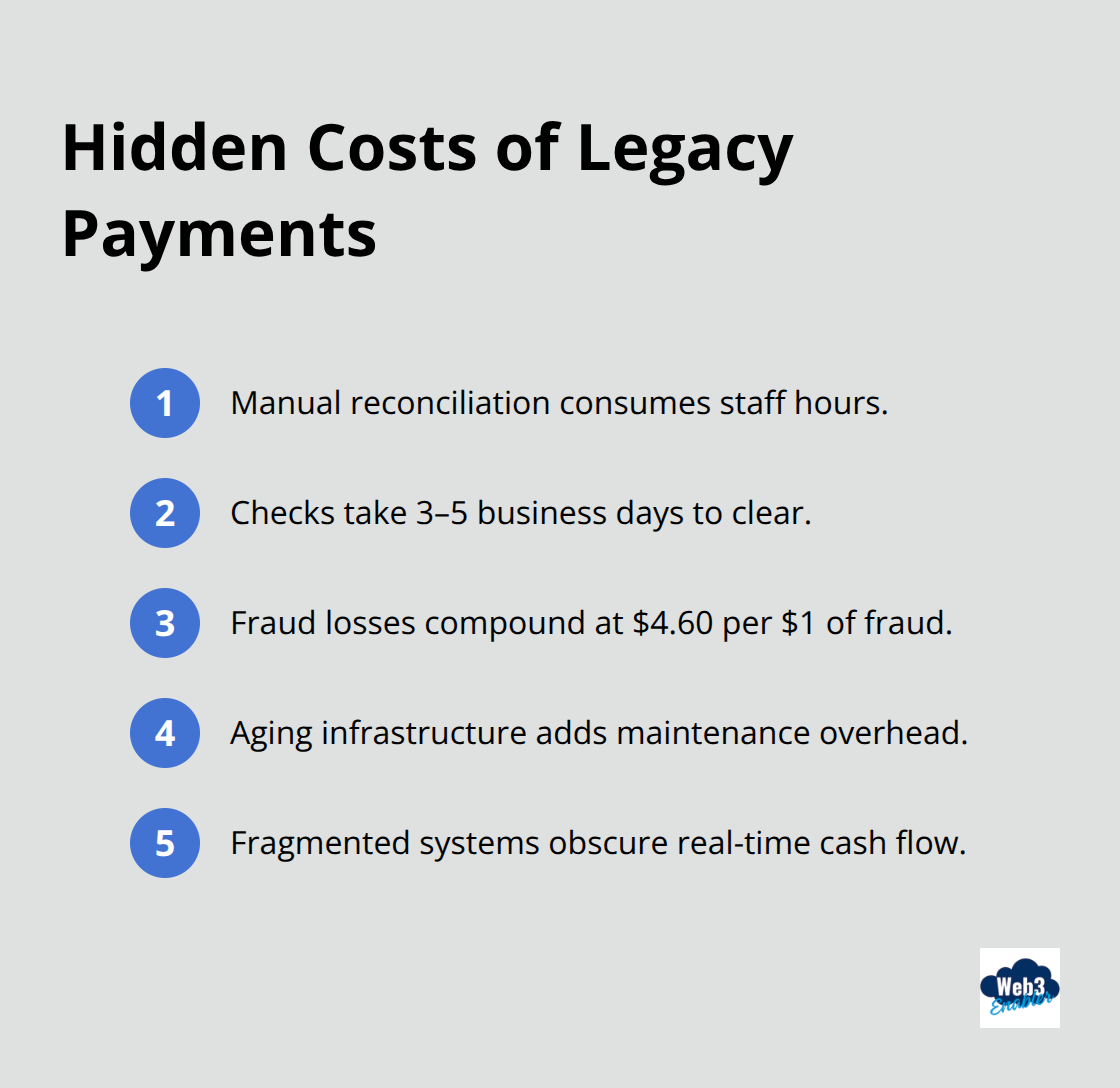

The speed difference alone is brutal: while a check takes 3-5 business days to clear, digital payments settle in seconds or minutes. For cash-heavy operations, you lose time and visibility into your cash flow, tying up working capital that could fund growth. Companies processing high transaction volumes have discovered that switching to digital payments frees up staff from manual reconciliation work, reduces human error, and dramatically cuts the cost per transaction. When JDS Industries moved to an integrated digital payment platform, they achieved 10% cost savings and 50% faster payment processing. That’s not theoretical-that’s money back in your pocket.

The Contactless Revolution Is Already Here

Your customers have already made the choice for you. In-store digital wallet usage has grown significantly, and in-app payments reached about 60% adoption. If your business doesn’t accept mobile wallets like Apple Pay and Google Pay, you watch customers abandon their carts and head to competitors who do. The shift goes beyond convenience-contactless payments reduce friction at checkout, lower fraud risk through tokenization, and speed up transaction processing. Global payment networks have made this infrastructure accessible even to small businesses through standard payment processors. The real advantage goes to businesses that accept multiple digital payment methods (customer preferences vary by region, age group, and purchase context). Offering flexibility isn’t nice-to-have anymore; it’s the baseline expectation that separates thriving businesses from struggling ones.

What Happens When You Ignore Digital Payment Trends

Sticking with legacy systems costs more than you think. Your staff spends hours reconciling transactions manually, your customers experience checkout friction that drives them elsewhere, and your cash flow remains opaque until days after transactions complete. Meanwhile, businesses that embraced digital payments already moved ahead-they process transactions faster, reduce operational overhead, and gain real-time visibility into their finances. The competitive gap widens every quarter. Those hidden costs of legacy systems (processing delays, manual labor, lost sales) add up quickly, which is exactly why the next section reveals what you’re actually paying to stay stuck in the past.

What Legacy Payment Systems Actually Cost You

The Hidden Price of Manual Processes

Every day your business operates on outdated payment infrastructure, you hemorrhage money in ways that don’t show up on a single line item. Your staff spends hours manually reconciling transactions across different systems because nothing talks to each other. A typical merchant loses about 4.60 dollars for every dollar of fraud that occurs, and legacy systems lack the real-time fraud detection that modern digital payment platforms provide.

Meanwhile, checks take 3-5 business days to clear while your competitors who switched to digital payments access funds in minutes.

That delay directly impacts working capital-cash you could use to pay suppliers faster, invest in inventory, or fund operations sits trapped in the clearing pipeline. Processing fees on legacy systems compound the problem. Credit card processors charge standard rates, but add in manual reconciliation labor, check printing costs, and the overhead of maintaining outdated infrastructure, and your actual cost per transaction balloons. JDS Industries discovered this firsthand and cut their costs by 10% simply consolidating onto an integrated digital payment platform. That’s not optimization theater; that’s legitimate money recaptured from inefficiency.

Security Vulnerabilities That Drain Your Bottom Line

Legacy systems create a second financial drain that most businesses underestimate. Global online payment fraud losses reached 44 to 48 billion USD in 2024, and projections suggest losses could exceed 100 billion USD by 2029. Many legacy systems lack tokenization, which replaces sensitive payment data with secure tokens, making them attractive targets for criminals. Two-factor authentication and machine-learning-based fraud detection were the most effective defenses in 2024, yet most legacy infrastructure doesn’t support either.

Your visibility into cash flow remains broken until transactions fully settle, meaning you can’t make informed decisions about inventory, payroll, or growth investments in real time. Modern digital payment systems provide instant transaction visibility, fraud scoring, and settlement confirmation. The businesses that moved forward already have cash flow transparency that legacy operators can only dream about. That information gap isn’t just inconvenient-it costs you competitive advantage every single day, which is exactly why forward-thinking companies are already exploring how digital payments can transform their operations and unlock new growth opportunities.

How Digital Payments Multiply Your Revenue Streams

Real-Time Settlement Transforms Your Cash Flow

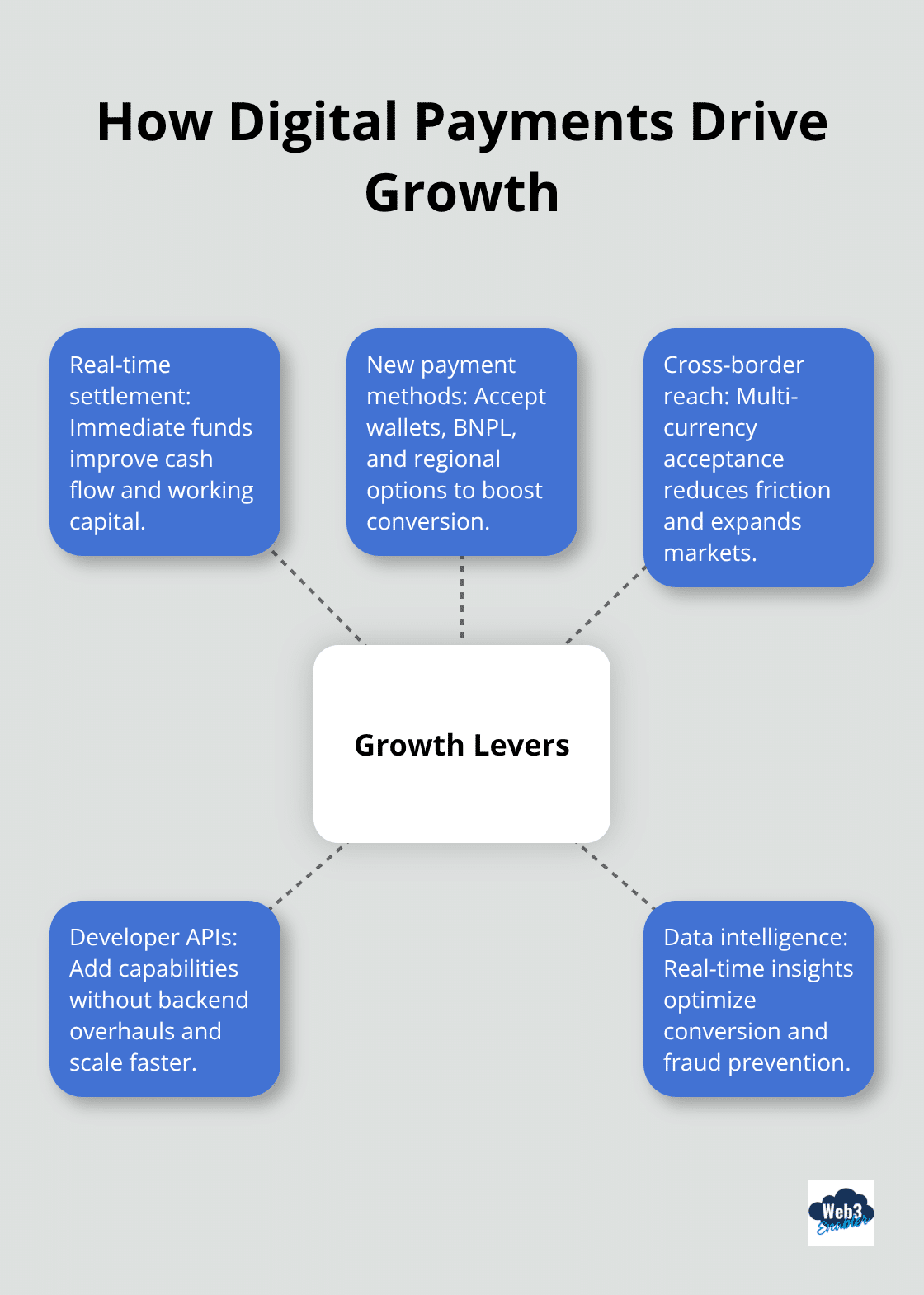

The moment you accept digital payments, your business stops leaving money on the table. Real-time settlement means capital hits your account immediately rather than days, fundamentally changing how you manage cash flow and working capital. Cargill and JPMorgan Payments demonstrated this advantage in Brazil’s agricultural sector, where real-time payments reduced funding delays and credit risk for suppliers and farmers. When you access capital faster, you can pay suppliers on better terms, invest in inventory immediately, or fund growth initiatives without waiting for traditional clearing cycles.

Small businesses operating on thin margins discover that faster settlement alone improves their ability to weather seasonal fluctuations or unexpected expenses. Medium-sized companies use the freed-up capital to negotiate better vendor pricing or expand operations without external financing. Large enterprises leverage real-time payment visibility to optimize working capital across global operations, reducing the cash required to run the business.

New Markets Open When You Accept What Customers Want

Expanding into new markets becomes dramatically simpler when you accept the payment methods customers in those regions actually use. McKinsey research shows in-app digital payments reached 60% adoption, while in-store digital wallet usage climbed to 28% in 2024. A retailer accepting only credit cards misses customers who prefer mobile wallets, buy-now-pay-later services like Affirm or Klarna, or regional payment methods.

Cross-border payment friction disappears when you work with platforms that handle multiple currencies and payment types seamlessly. Shopify merchants integrating services like Coinbase Commerce instantly reach customers paying with stablecoins or cryptocurrencies, opening entirely new customer segments. Developer portals and payment APIs enable merchants to add new payment acceptance capabilities without overhauling backend systems.

Data Transforms Payment Processing Into Strategic Intelligence

The data advantage compounds this opportunity significantly. Modern digital payment systems capture transaction patterns, customer preferences, and regional trends in real time. You see which payment methods drive the highest conversion rates, which customer segments prefer installment payments, and where geographic expansion opportunities exist.

This intelligence transforms payment data from a compliance checkbox into a competitive asset. Merchants using machine-learning-based fraud detection not only prevent 2024’s most common fraud types, but also identify legitimate high-value customers that rule-based systems would incorrectly flag. That distinction separates merchants who block fraud from those who block revenue.

Final Thoughts

The importance of digital payments isn’t debatable anymore-your competitors switched years ago, your customers expect it, and the financial case crushes any argument for staying put. Businesses clinging to legacy systems actively choose to pay more, move slower, and hand market share to rivals who embraced digital payment infrastructure. The gap between early adopters and laggards widens every quarter as real-time settlement, fraud prevention, and payment data intelligence compound into genuine competitive advantages.

Starting your digital payment journey doesn’t require tearing apart your entire operation. Modern payment platforms integrate seamlessly with existing systems, so you accept new payment methods, gain real-time cash flow visibility, and reduce fraud risk without massive disruption. The businesses winning right now aren’t the ones waiting for perfect conditions-they’re the ones who recognized that digital payments solve real problems: faster cash flow, lower operational costs, and access to customers and markets that legacy systems keep locked away.

We at Web3 Enabler help businesses connect blockchain technology with their existing infrastructure, making it simple to accept stablecoin payments and send global payments faster. Whether you’re processing your first digital payment or optimizing a global payment network, the time to act is now-the competitive advantage belongs to businesses that move first.

Frequently Asked Questions: Why Digital Payments Are Important

Why are digital payments important for businesses today?

Digital payments are important because they reduce checkout friction, improve cash flow visibility, and meet modern customer expectations. When customers can pay how they prefer (card, wallet, bank transfer, or other digital methods), businesses typically see smoother conversions, faster settlement, and less manual back-office work.

What counts as a digital payment?

A digital payment is any electronic method of paying without physical cash or paper checks. Common examples include credit and debit cards, ACH and bank transfers, mobile wallets (Apple Pay and Google Pay), QR payments, buy now pay later options, and blockchain-based payments such as stablecoins.

How do digital payments improve cash flow and settlement speed?

Digital payments can settle faster than legacy methods like checks and many cross-border wires. Faster settlement means you confirm funds sooner, ship sooner, recognize revenue sooner, and make decisions based on real-time or near-real-time payment status rather than waiting days for clearing.

How do digital payments reduce operational costs?

Digital payments reduce costs by minimizing manual processes like check handling, bank portal chasing, and spreadsheet reconciliation. Modern payment systems also centralize reporting, automate receipts and transaction records, and reduce the time teams spend on payment exceptions and status updates.

Do digital payments help prevent fraud and chargebacks?

Yes. Many modern digital payment methods include security features such as tokenization, encryption, and risk checks that are harder to achieve with cash and checks. While no system eliminates fraud entirely, digital payment platforms can improve detection and reduce exposure by providing richer transaction data and faster anomaly visibility.

Why do customers prefer contactless and mobile wallet payments?

Customers prefer contactless and mobile wallets because they are fast, convenient, and reduce checkout friction. They also feel safer for many shoppers because they do not require handing over a card or entering payment details repeatedly, especially on mobile devices.

How do digital payments support international sales and cross-border commerce?

Digital payments make it easier to sell globally by supporting multiple payment methods, currencies, and regions. When customers can use familiar digital payment options, businesses can reduce payment drop-off and improve confirmation speed, which matters for international fulfillment, billing, and customer experience.

How do stablecoins fit into digital payments?

Stablecoins are digital currencies designed to track the value of a fiat currency, which makes them useful for payments where businesses want blockchain settlement benefits without the volatility of traditional cryptocurrencies. For some companies, stablecoins can improve cross-border payment speed, reduce operational friction, and provide clearer payment tracking.

What is the easiest way to start accepting digital payments?

Start by reviewing how customers want to pay, then enable the top methods you are missing (often mobile wallets and modern bank transfer options). Next, unify reporting so finance teams can track payments in one workflow. If you sell internationally, consider adding options that reduce cross-border friction, including stablecoin rails where appropriate.

How can Web3 Enabler help with modern digital payments?

Web3 Enabler helps businesses connect blockchain payment capabilities to existing workflows so teams can accept stablecoin payments and improve cross-border payment operations without adding unnecessary complexity. The goal is to keep payment visibility, auditability, and reporting aligned with the systems your teams already use.