Your payment system is probably costing you more than it should. Traditional banking rails move at a snail’s pace and charge fees that add up fast.

USDC payments workflow changes that equation entirely. We at Web3 Enabler have seen businesses cut settlement times from days to minutes and slash transaction costs dramatically. This isn’t theoretical-it’s happening right now.

Why USDC Actually Works for Business Payments

Banking Schedules Belong in a Museum

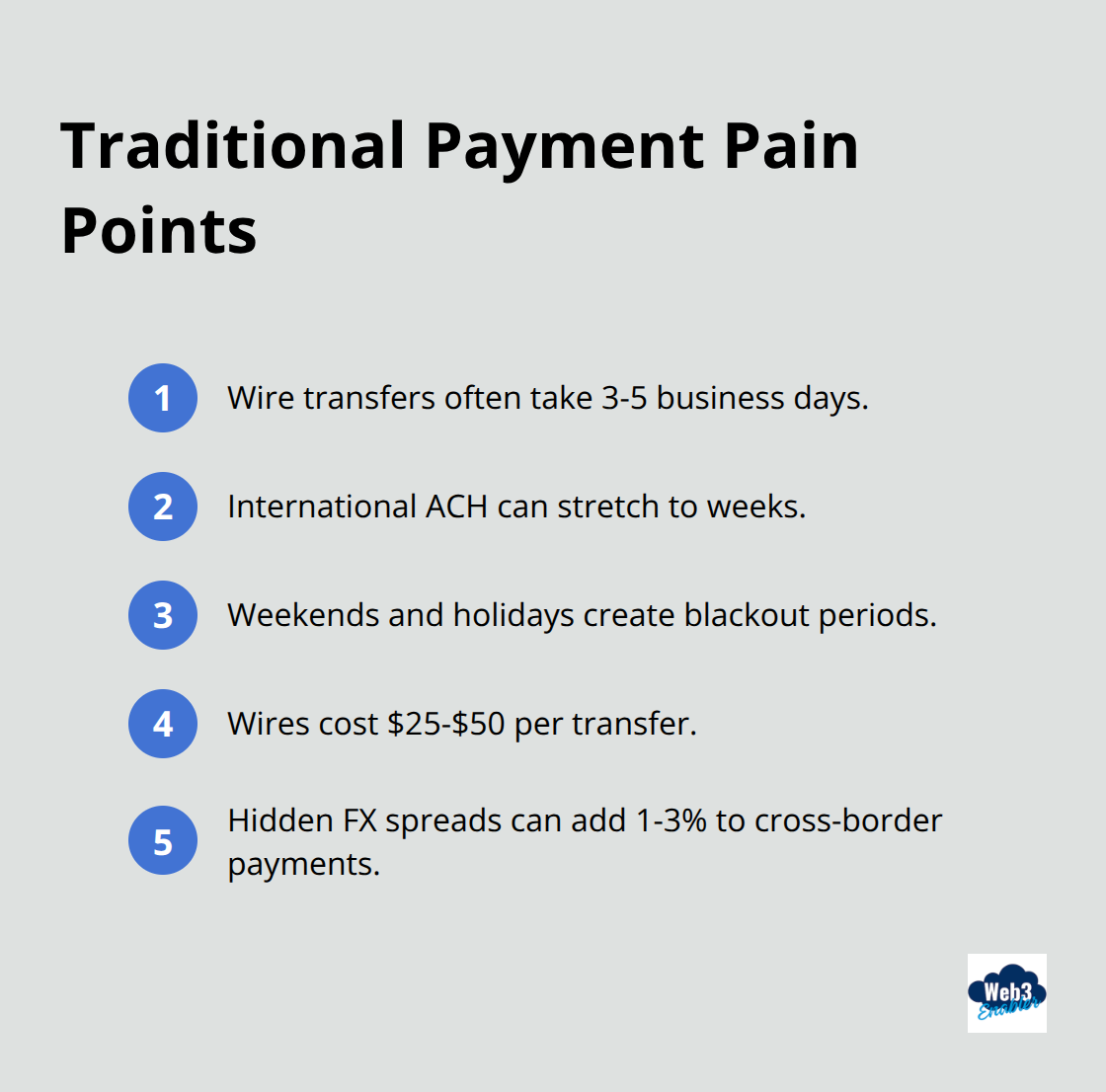

Traditional payment systems operate on banking schedules that haven’t changed much since the 1970s. Wire transfers take 3-5 business days. International ACH payments stretch across weeks. Weekends and holidays create blackout periods where your money just sits idle.

Meanwhile, you pay $25-$50 per wire transfer, plus hidden FX spreads that can eat 1-3% of cross-border transactions. About 708 million people globally own cryptocurrency, yet most businesses still funnel payments through antiquated rails that treat 2 PM Friday and 2 AM Monday as completely different universes.

USDC Moves on Blockchain Time

USDC changes this equation because it moves on blockchain time, not banking time. Settlement happens in minutes, not days. A payment sent at 11 PM on a Sunday night arrives in the recipient’s wallet before Monday morning coffee. Transaction costs drop dramatically-stablecoin transfers cost a fraction of traditional wire fees, with all-in costs under 1% compared to roughly 5–11% for traditional wires, and there’s no FX spread because USDC maintains a 1:1 parity with USD.

Compress Your Cash Conversion Cycles

When you run global payroll or handle cross-border vendor payments, minute-level settlements compress your cash conversion cycles and reduce working capital strain. Currency conversion friction disappears entirely when both parties use USDC, or when you use what’s called a stablecoin sandwich flow-converting local currency to USDC in the middle, then back to local currency at the destination. This approach balances speed with local accounting requirements without forcing everyone onto blockchain at once.

Always-On Settlement Improves Liquidity

For businesses with treasury teams managing liquidity across regions, USDC enables what we’d call always-on settlement: your money moves 24/7 without waiting for banking windows. This improves cash flow visibility and reduces the idle capital sitting in transit accounts. The result is a payment system that actually works around your business schedule, not against it-which means your next chapter involves figuring out how to integrate this capability into your existing tech stack.

USDC Payments Actually Move Through Your Systems

How the Mechanics Work (Spoiler: It’s Refreshingly Simple)

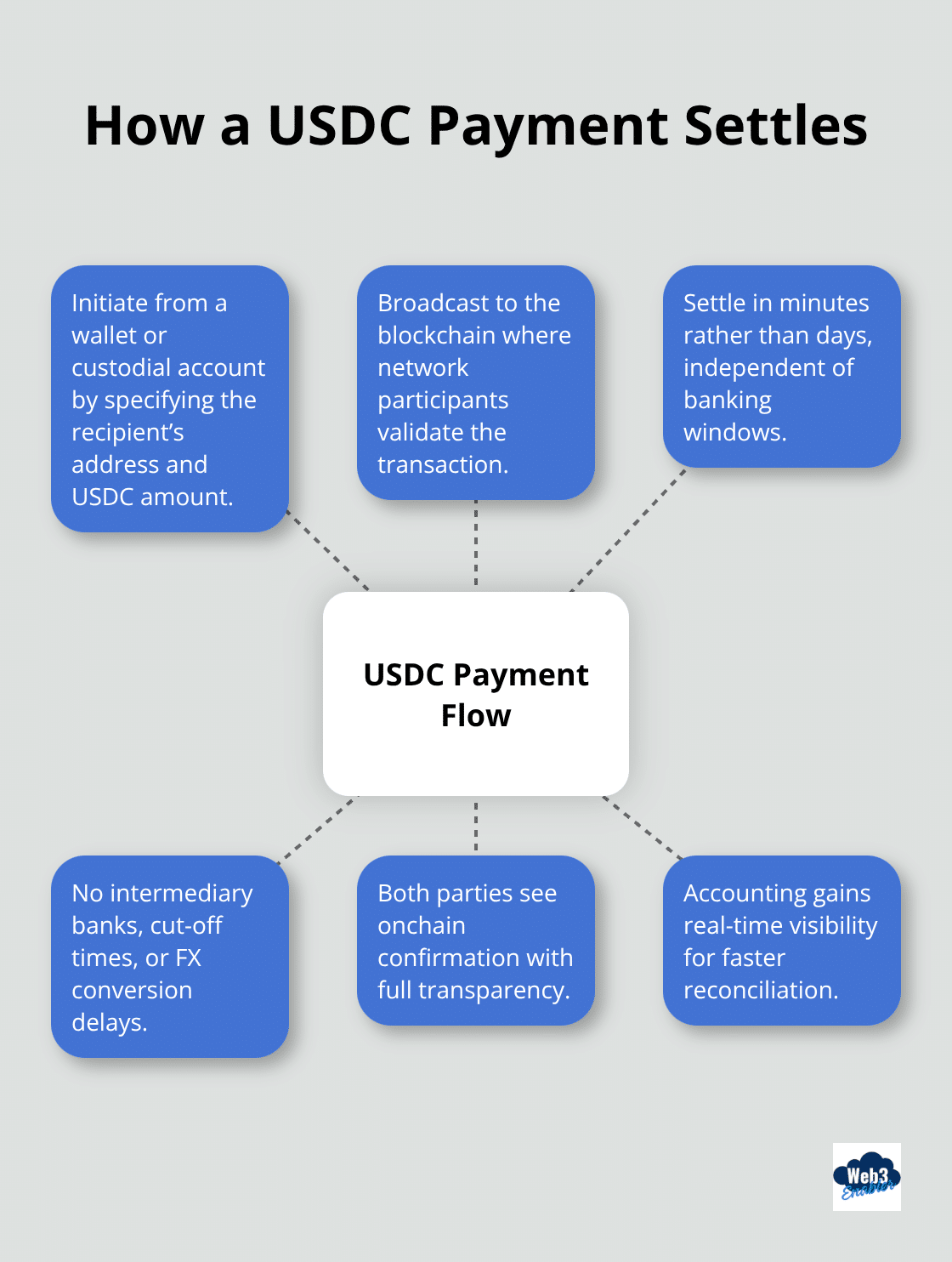

A sender initiates a transaction from their wallet or custodial account, specifying the recipient’s wallet address and the USDC amount. The payment broadcasts to the blockchain network, gets validated by network participants, and settles within minutes. No intermediary banks, no cut-off times, no FX conversion delays.

Both parties see the transaction confirmed on the blockchain with full transparency. This end-to-end onchain settlement gives your accounting team real-time visibility instead of waiting for a bank to confirm receipt three days later. For businesses handling high transaction volumes, this matters enormously. A company processing 100 international vendor payments monthly saves roughly $2,500 to $5,000 in wire fees alone, plus eliminates the working capital drag from multi-day settlement windows.

Integration Sits Alongside Your Current Stack

Most businesses assume adopting USDC means replacing their existing payment infrastructure. It doesn’t. USDC integrations sit alongside your current systems. If you use Salesforce for CRM and financial tracking, native Salesforce integration maps USDC transactions directly into your records without custom middleware. Merchants accepting USDC can use payment links, embedded checkout flows, or API-driven invoicing depending on their tech maturity. Payroll teams can fund payments via USD bank transfers or crypto wallets holding USDC, then let workers choose their payout currency each cycle from 90+ fiat options or stablecoins. The key is choosing an integration model that matches your operational complexity. A small ecommerce store needs a different setup than a multinational company managing payroll across 50 countries. WalletConnect Pay offers an end-to-end solution for merchants accepting crypto from any wallet, behaving like a familiar payment method within existing PSP stacks. For larger enterprises, custodial wallet models with role-based permissions, approval workflows, and audit logs align better with compliance requirements.

Real Adoption Accelerates Across Industries

Stablecoin transaction volumes now reach trillions annually, with USDC and USDT dominating adoption across wallets, exchanges, and payment processors. About 17% of websites now accept crypto payments via wallets, while stablecoins comprise roughly two-thirds of wallet transaction volume. Companies have processed payroll across 190+ markets using stablecoin rails, proving this works at scale beyond theory. Gaming platforms, digital goods marketplaces, and subscription services increasingly offer USDC as a checkout option because conversion rates improve when customers pay with their preferred wallet. Cross-border remittance corridors benefit most dramatically: workers receiving payments in USDC can withdraw to local currency immediately or hold stablecoins in high-inflation regions, giving them optionality that traditional banking never provided. The compliance infrastructure has matured too. KYC, sanctions screening, address allow-listing, and dual approvals now function as standard controls within wallet-based payment workflows, making institutional adoption feasible without sacrificing security. This foundation sets the stage for the next critical piece: actually building these payment solutions into your tech stack and managing the compliance side properly.

How to Build USDC Into Your Systems Without Breaking Existing Workflows

Integrating USDC into your payment stack sounds intimidating until you realize most businesses don’t need to rip out their current infrastructure. Salesforce users have a direct advantage here. Web3 Enabler’s Salesforce native blockchain solutions available on the Salesforce AppExchange mean USDC transactions map directly into your CRM, financial records, and reporting dashboards without custom middleware or API wrestling matches. Your finance team sees payment data flow into Salesforce automatically, which eliminates manual reconciliation and reduces the error rate that plagues traditional payment imports. For companies already using Salesforce, this matters because your existing workflows stay intact while you layer in USDC capability alongside them. Setup typically takes weeks rather than months because you extend systems instead of replacing them. Compliance integrations sit within Salesforce too, so KYC workflows, sanctions screening, and approval hierarchies become part of your standard business process rather than bolted-on afterthoughts.

Non-Salesforce shops have other paths. Merchants can use WalletConnect Pay, which integrates into existing PSP stacks and behaves like a familiar payment method without requiring merchants to hold crypto on their balance sheet. Payroll teams can connect to Rise, which supports 190+ markets and lets workers choose their withdrawal currency from 90+ fiat options or stablecoins each cycle, with funding happening via USD bank transfers or crypto wallets holding USDC. The key decision isn’t whether to integrate USDC-it’s choosing the right integration model for your operational complexity.

Compliance Controls Must Come First, Not Last

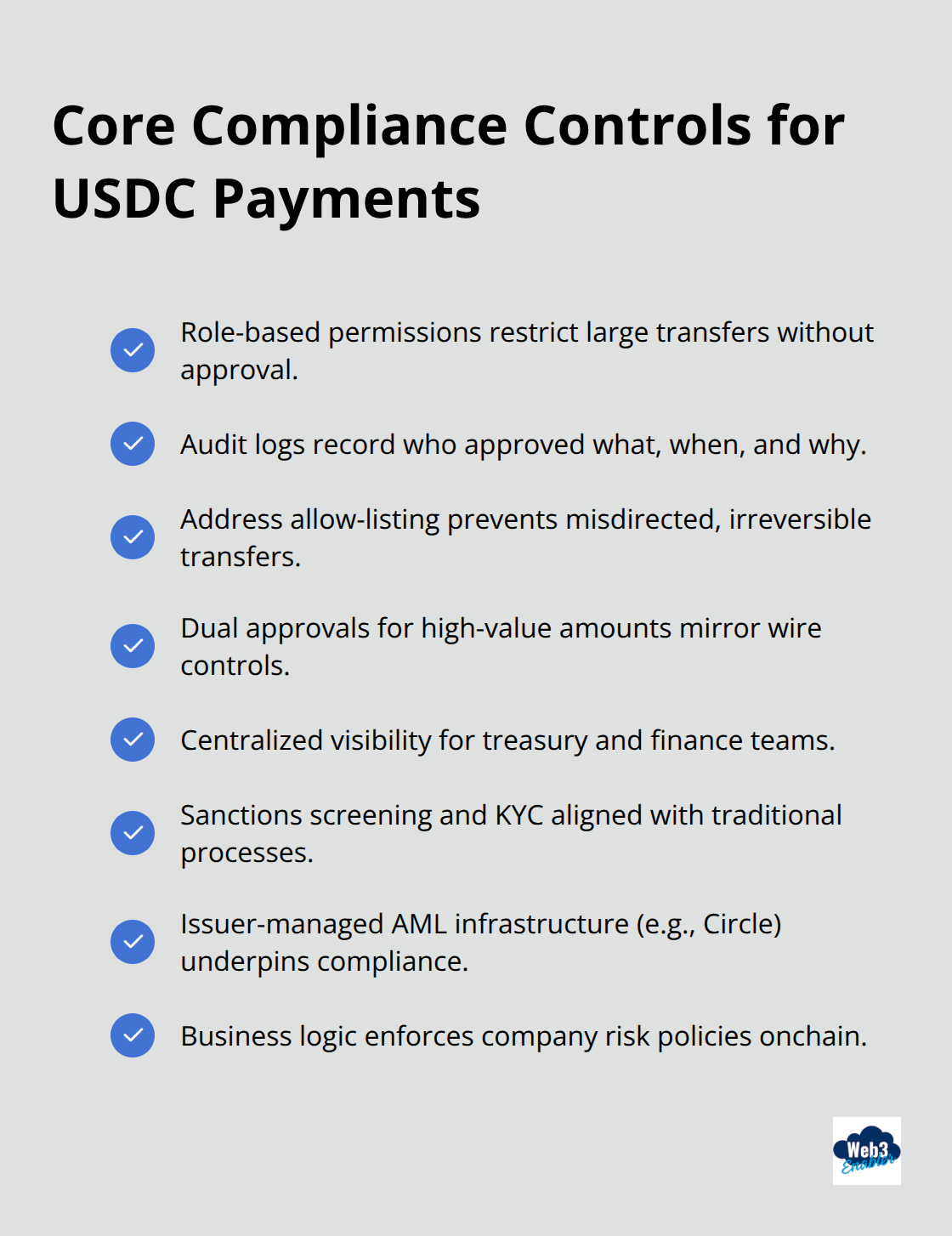

Many businesses treat compliance as a post-launch problem. That’s backward. Your USDC payment architecture should include compliance controls from day one because wallet-based payments require different guardrails than traditional banking. Role-based permissions prevent a single person from moving large amounts without approval. Audit logs create permanent records of who authorized what, when, and why, which regulators expect to see. Address allow-listing stops accidental payments to wrong wallet addresses, which blockchain transactions cannot reverse. Dual approval workflows for amounts above certain thresholds mirror what your finance team already does for wire transfers, just executed faster.

Your treasury team sees approvals and audit trails in the same place they manage other financial data. For enterprises handling high transaction volumes, this integration prevents the compliance drift that happens when payment controls live scattered across multiple platforms. Sanctions screening and KYC requirements work the same way they do for traditional payments, just executed onchain. Circle and other regulated stablecoin issuers handle the underlying compliance infrastructure, meaning you don’t need to build AML systems from scratch. Your job is implementing the business logic that enforces your company’s risk policies.

Start With a Single Use Case, Then Expand

Companies that succeed with USDC don’t try to transform their entire payment infrastructure overnight. They pick one concrete use case: payroll to contractors in a specific region, vendor payments to a particular supplier, or merchant settlements in a single market. This approach lets you learn the operational reality without betting your entire payment system on it. Once you’ve proven the model works operationally and your team understands the workflows, expanding to other use cases becomes straightforward because you’ve already solved the integration, compliance, and reconciliation challenges. Your technology partners matter enormously here. Web3 Enabler’s custom implementations help businesses map their specific workflows onto Salesforce-native USDC infrastructure, so you’re not starting from a blank slate. Ripple and Circle partnerships provide the payment rails and stablecoin infrastructure that actually move money, not theoretical demonstrations of blockchain capability. Your choice of partners directly impacts implementation speed and whether you can actually settle payments or just process them in a sandbox environment.

Final Thoughts

USDC payments represent a genuine business upgrade, not a speculative detour into crypto. You’ve seen how minute-level settlement compresses cash cycles, how stablecoin transfers cost a fraction of traditional wires, and how compliance controls integrate directly into your existing systems. The USDC payments workflow operates across payroll, vendor payments, merchant settlements, and treasury management at companies processing real volume across real markets.

Implementation succeeds when you choose partners who understand your business infrastructure, not just blockchain technology. We at Web3 Enabler specialize in connecting stablecoin payments with Salesforce environments, meaning your finance team sees USDC transactions flow directly into the systems they already use daily. Our Salesforce Native blockchain solutions available on the Salesforce AppExchange eliminate the custom middleware and API wrestling that derails most blockchain projects.

Your next step depends on where you sit operationally. If you run Salesforce, contact Web3 Enabler to explore how native blockchain integration maps USDC transactions into your existing workflows. If you manage payroll across borders, test stablecoin funding with a single contractor cohort in one region before expanding globally. The businesses winning with USDC payments aren’t waiting for perfect regulatory clarity or theoretical cost savings-they move money faster, cut fees, and improve cash flow visibility right now.