Cross-border stablecoin payments are reshaping how businesses move money internationally. Traditional wire transfers take days and cost thousands in fees, while blockchain-based alternatives settle in minutes for a fraction of the price.

We at Web3 Enabler have built this guide to help you understand the infrastructure, compare real costs, and find the right payment solution for your corridors.

Stablecoin Payment Infrastructure for Cross-Border Transactions

ERC-20, TRC-20, and Layer-2 Solutions

Stablecoin infrastructure runs on different blockchain networks, each with distinct trade-offs in speed, cost, and compatibility. The three most practical options for cross-border payments are ERC-20 on Ethereum, TRC-20 on Tron, and Layer-2 solutions like Arbitrum and Polygon.

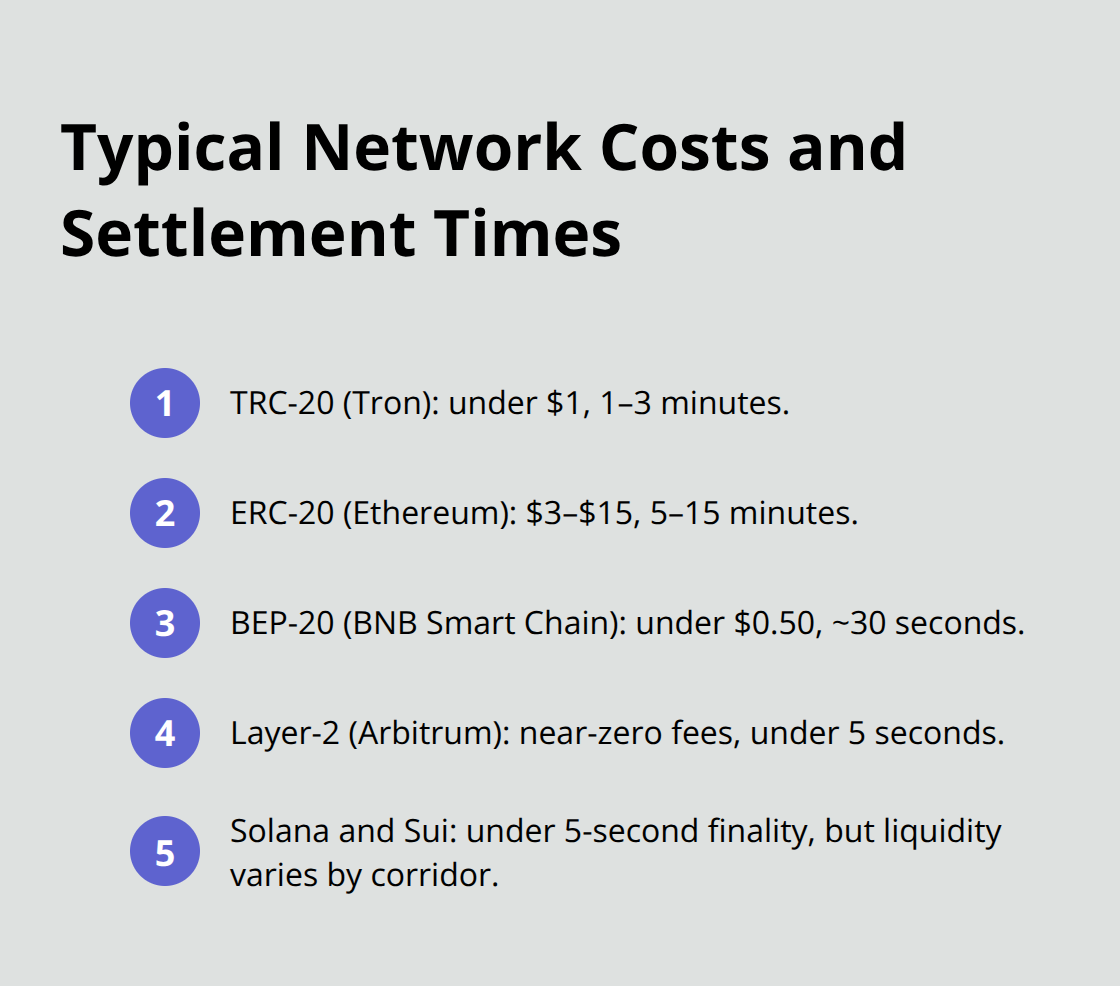

ERC-20 USDT dominates decentralized finance because most protocols like Uniswap and Aave operate on Ethereum. Typical fees range from $3 to $15 during network congestion, and settlement takes 5 to 15 minutes. TRC-20 USDT on Tron uses Delegated Proof of Stake consensus and costs around $1 or less per transfer with settlement in 1 to 3 minutes, making it ideal for exchange deposits and peer-to-peer transfers.

BEP-20 USDT on BNB Smart Chain splits the difference with fees typically under $0.50 and 30-second settlement times. For high-volume corridors, Solana and Sui offer sub-5-second finality, but liquidity remains concentrated on larger networks. Layer-2 solutions like Arbitrum deliver ERC-20 compatibility with sub-5-second finality and negligible fees, making them increasingly attractive for treasury operations.

Selecting the Right Network for Your Corridors

Your choice depends entirely on where your counterparties hold accounts and which networks your payment gateway supports. If you move money between exchanges or conduct remittances, TRC-20 and BEP-20 minimize costs dramatically. If you need DeFi access or custody solutions, ERC-20 remains necessary despite higher fees.

Network mismatches create real problems-sending BEP-20 USDT to an ERC-20 address renders funds inaccessible without a bridge or exchange conversion. Address prefixes help identify networks: 0x… indicates ERC-20, BEP-20, or Polygon, while T… indicates TRC-20. Always verify recipient compatibility before moving significant amounts.

Custody Architecture and Settlement Flows

Custodial wallets hold your private keys through a service provider, offering simplicity and insurance but requiring you to trust that provider’s security and solvency. Non-custodial wallets give you direct control through hardware wallets or self-managed hot wallets, eliminating counterparty risk but shifting security responsibility to you.

For cross-border payments, custodial solutions from institutional providers are standard because they integrate with compliance systems, enable Travel Rule reporting, and provide insurance against theft. Non-custodial flows work only when both parties control their own wallets and manage key rotation without operational friction. Most businesses start custodial for simplicity, then transition portions of their treasury to non-custodial models as their team gains experience.

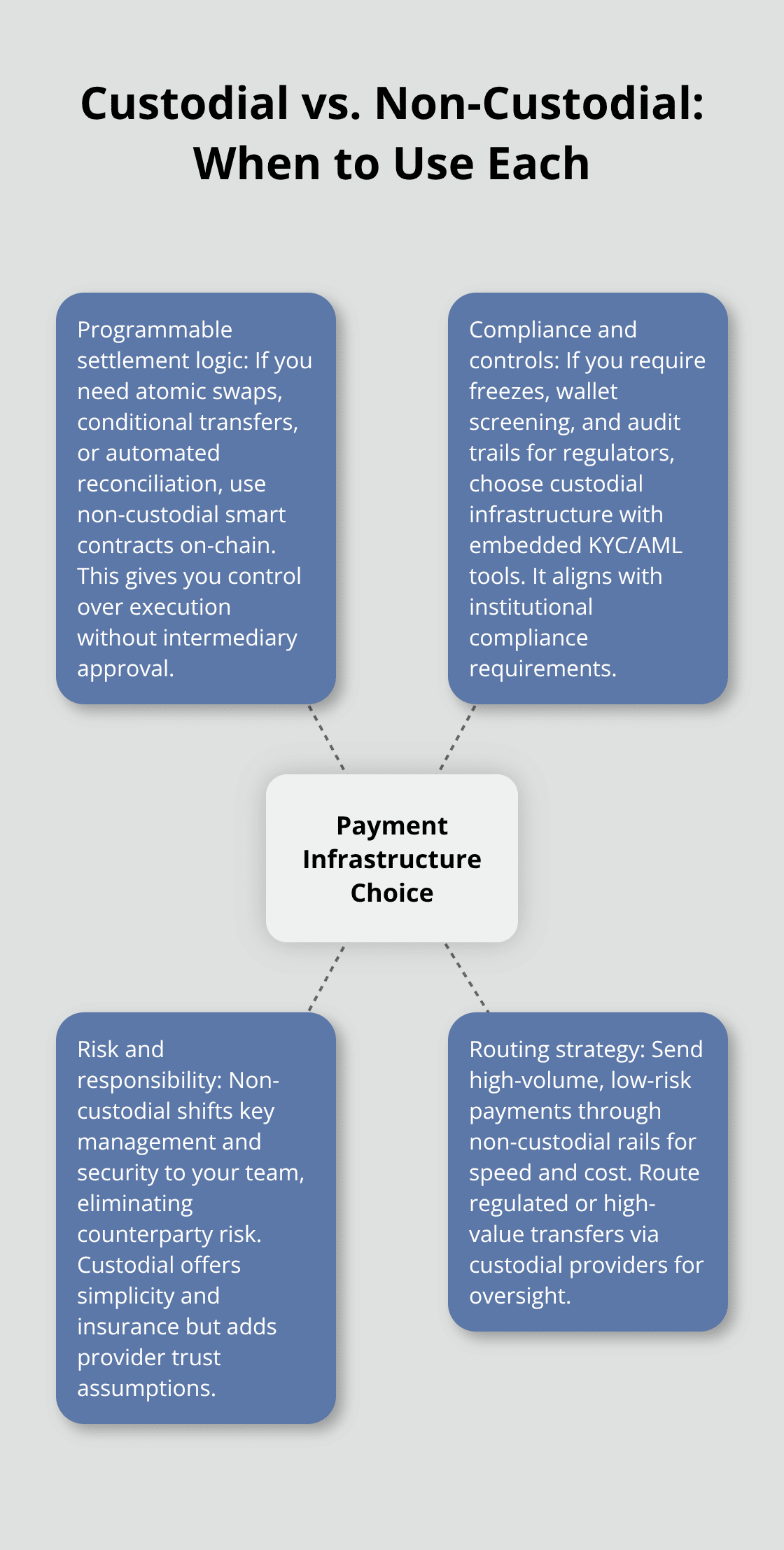

When to Use Custodial versus Non-Custodial Infrastructure

The critical decision is whether your payment flow requires programmable settlement logic. If you need atomic swaps, conditional transfers, or automated reconciliation, you must use non-custodial smart contracts on-chain. If you need compliance freezes, wallet screening, and audit trails for regulators, custodial infrastructure with embedded KYC/AML tools is essential.

Visa’s settlement pilots use custodial infrastructure integrated with their existing acquiring bank relationships, illustrating how institutional-grade payments require custody layers that traditional finance already demands. Your payment gateway provider should support both models so you can route different transaction types appropriately-high-volume, low-risk transfers through non-custodial channels and regulated or high-value payments through custodial infrastructure.

Understanding these infrastructure choices positions you to evaluate liquidity providers and compare their capabilities across your specific corridors.

What Do Cross-Border Payments Actually Cost?

Transaction Fees Across Blockchain Networks

Stablecoin transfers cost dramatically less than traditional banking, but the savings depend entirely on which blockchain you use and what you’re comparing against. A TRC-20 USDT transfer costs under $1 and settles in 1 to 3 minutes, while an ERC-20 transfer on Ethereum ranges from $3 to $15 during normal network conditions. BEP-20 on BNB Smart Chain typically costs under $0.50 with 30-second finality. Layer-2 solutions like Arbitrum deliver near-zero fees with sub-5-second settlement.

These aren’t theoretical numbers-blockchain explorers let you verify live network costs right now.

A traditional wire transfer can exceed $50 per transaction, takes 2 to 5 business days for international corridors, and often requires pre-funding at correspondent banks that tie up your capital. The World Bank estimates cross-border payment costs in many corridors are substantial, driven by multiple intermediaries, FX conversion spreads, and reserve requirements.

Real Savings on High-Volume Corridors

A $10,000 wire transfer between the US and Nigeria through traditional banking costs roughly $600 to $1,500 when you factor in bank fees, FX margins, and delays. The same transfer via TRC-20 USDT costs under $1 and settles within minutes. For high-volume corridors, the compounding effect becomes substantial-moving $1 million monthly between exchanges or subsidiaries saves $25,000 to $50,000 annually just in transaction fees, before accounting for faster capital deployment.

Hidden Costs in Traditional Banking Infrastructure

The hidden costs in traditional banking extend far beyond the wire fee itself. Your treasury team spends hours reconciling transfers across multiple bank statements, gateway reports, and correspondent bank confirmations because settlement happens in batches with no real-time visibility. You maintain reserve balances at multiple banks to ensure liquidity, capital that generates minimal returns while sitting idle. Pre-funding requirements force you to move money days before you need it, locking up working capital. FX spreads on cross-border transfers often run 1 to 3 percent above spot rates, and you gain no visibility into what rate you’re actually receiving.

Operational Efficiency with Stablecoin Infrastructure

Stablecoin infrastructure eliminates most of these costs. A single shared ledger gives you instant, permanent transaction records with full traceability. Settlement finality means your counterparty receives funds immediately, with no three-day wait for correspondent bank confirmations. No pre-funding requirements mean capital stays productive until the moment you need to move it. For businesses conducting regular cross-border payments-international contractor payroll, supplier settlements, marketplace payouts-the operational savings often exceed the transaction fee savings.

Visa’s settlement pilots achieved annualized volumes in the billions by routing cross-border payments through stablecoin rails integrated with their existing acquiring bank relationships, demonstrating that institutional-grade payment processors are already capturing these efficiencies. Your payment gateway provider should quantify your specific savings by mapping your current corridors, transaction volumes, and banking costs against stablecoin alternatives on the networks where your counterparties already operate. This analysis reveals where stablecoin infrastructure creates the most value for your specific payment flows and which networks your team should prioritize for implementation.

Regional Corridors and Provider Comparison

Africa and the Middle East: Where Stablecoins Solve Real Problems

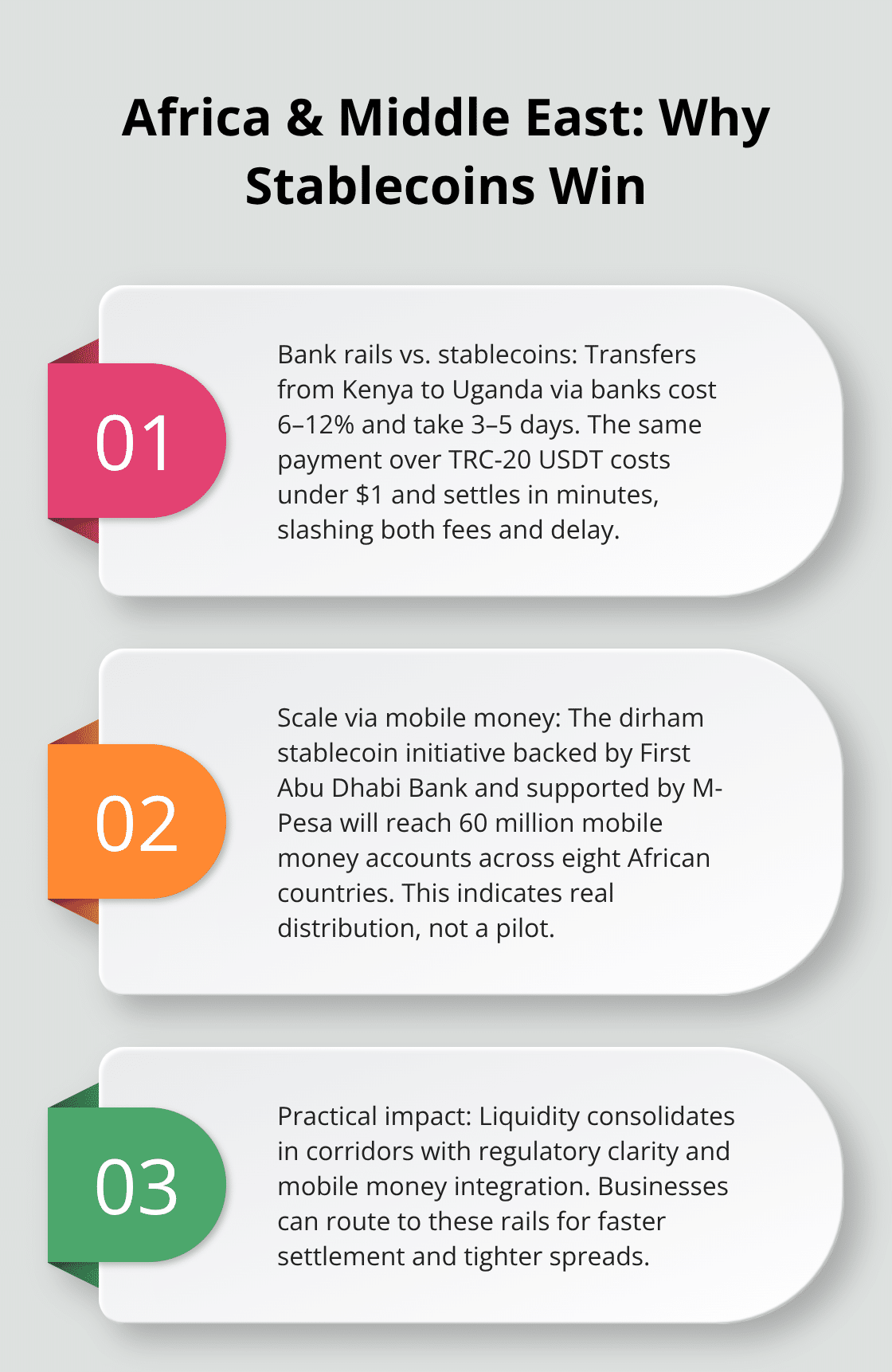

Africa and the Middle East represent the highest-value corridors for stablecoin infrastructure because traditional banking costs and settlement delays create the most friction. A cross-border payment from Kenya to Uganda through banks costs 6 to 12 percent in fees and takes 3 to 5 days, while the same transfer via TRC-20 USDT costs under $1 and settles in minutes. The dirham stablecoin initiative backed by First Abu Dhabi Bank and supported by M-Pesa will move digital settlement across 60 million mobile money accounts in eight African countries, signaling that regional institutions now recognize stablecoins as infrastructure, not speculation. This matters for your business because it means liquidity consolidates around specific corridors where regulatory clarity exists and mobile money networks can integrate blockchain rails directly.

Liquidity Concentration Determines Your Network Choice

Liquidity concentration determines whether stablecoin infrastructure works for your specific corridors. USDT dominates globally with over $33 trillion in on-chain volume during 2025, but regional liquidity varies dramatically. In East Africa, TRC-20 USDT trades actively on exchanges like MEXC and Binance with tight spreads because remittance volumes are high and counterparties already hold Tron wallets for speed and cost. In West Africa, BEP-20 USDT on BNB Smart Chain offers better liquidity than TRC-20 because regional exchanges prefer BSC infrastructure. In the Middle East, both ERC-20 and TRC-20 liquidity remain strong, but ERC-20 dominates for institutional treasury operations because custody providers and compliance platforms integrate Ethereum more deeply.

Mapping Your Counterparties and Preferred Networks

The practical step is to map your specific counterparty locations and their preferred exchanges, then verify which stablecoin versions trade with the tightest spreads on those platforms. If you move $100,000 monthly to three different countries and each corridor has different preferred networks, your payment gateway should support all three so you route each transfer to minimize slippage and settlement time. Providers maintain liquidity across multiple networks rather than forcing all customers onto a single rail. Your provider should offer similar flexibility, with clear reporting on which networks carry the deepest liquidity for each of your corridors so you can optimize routing without manual intervention.

Testing and Scaling Your Stablecoin Corridors

Test with a small transfer first, verify settlement finality and conversion rates on your preferred network, then scale volume once you confirm the corridor performs as expected. This approach reduces exposure to network mismatches or unexpected slippage while your team gains confidence in the infrastructure. Each region’s liquidity profile shifts as adoption accelerates, so quarterly reviews of your corridor performance help you identify when to shift volume between networks or add new payment routes as liquidity deepens.

Final Thoughts

Stablecoin infrastructure delivers three concrete advantages that traditional banking cannot match: settlement in minutes instead of days, transaction costs under $1 instead of $50 to $1,500, and permanent transaction records on a shared ledger that eliminate reconciliation delays. For businesses moving money across borders regularly, these advantages compound into meaningful operational savings and faster capital deployment. Your specific corridors and counterparty locations determine which network-TRC-20 on Tron, ERC-20 on Ethereum, or Layer-2 solutions like Arbitrum-minimizes costs and settlement time for each transfer.

Implementation starts with a pilot on your highest-volume corridor where you test a small transfer to verify settlement finality and conversion rates, then scale volume once your team confirms the cross-border stablecoin infrastructure performs as expected. This approach reduces risk while your organization gains confidence in blockchain-based payments. Your payment gateway should support routing across multiple networks so you optimize each corridor independently rather than forcing all transfers onto a single rail.

Web3 Enabler connects blockchain infrastructure directly to your existing Salesforce environment, letting you manage international contractor payments, supplier settlements, and digital asset tracking without building separate systems. Our platform handles the complexity of multi-network routing and compliance integration so your team focuses on business operations rather than blockchain mechanics.