Buying property across borders has always been expensive and slow. Crypto real estate transactions are changing that, especially in Africa and MENA where traditional banking creates friction.

We at Web3 Enabler have seen firsthand how stablecoins and blockchain settlement cut weeks off closings and eliminate unnecessary intermediaries. This guide covers everything you need to know about the legal requirements, practical steps, and real deals happening right now.

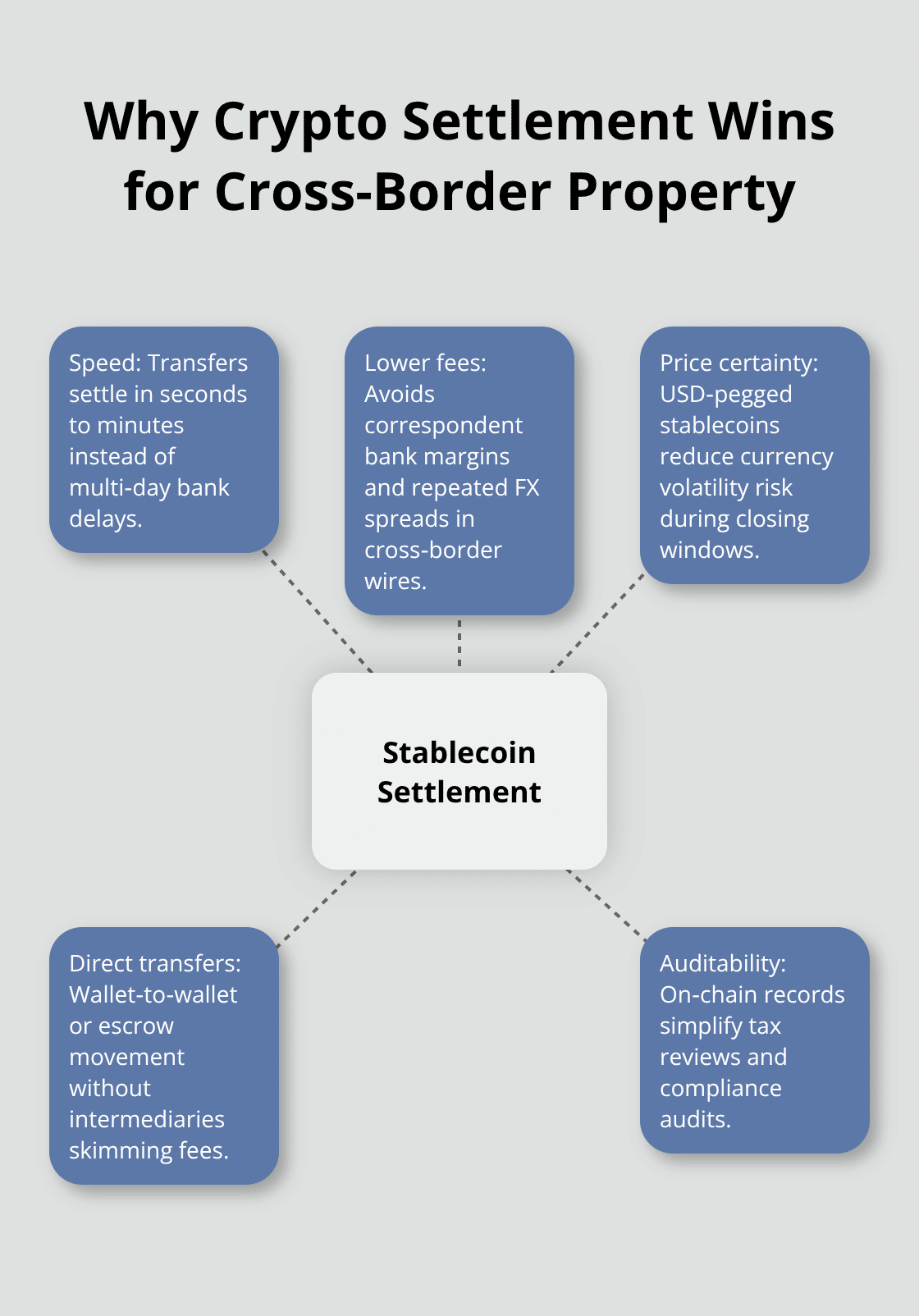

Why Crypto Settlement Beats Traditional Banking for Cross-Border Property

Stablecoin settlement fundamentally changes the economics of international real estate. Traditional banking forces you through multiple currency conversions, correspondent bank fees, and delays that stretch closings from weeks to months. A cross-border wire transfer through SWIFT costs between 15 and 50 USD per transaction, but the real damage comes from time. Nigeria experiences cross-border payment delays of 3 to 7 days on average, while stablecoin transfers settle in seconds to minutes. Global stablecoin activity reached 27.6 trillion USD in 2024, with transfers exceeding combined volumes of Visa and Mastercard-institutional players now trust this infrastructure. For property purchases in Africa and MENA, speed matters because price volatility works against you during lengthy settlement windows. When you lock in a property price and then wait a week for funds to arrive, currency fluctuations or market shifts erode your position. Stablecoins pegged to the USD eliminate that risk entirely.

Cost Reduction in Real Estate Transactions

International property deals using crypto cost dramatically less than traditional methods. In optimized corridors, stablecoin transfers cut cross-border remittance costs to under 3 percent, compared to the 8.37 percent average for African remittances. A real-world pilot in Cameroon showed merchants reducing fees from approximately 20 percent to 5.3 percent when they switched to stablecoins. For a property deal worth 500,000 USD, traditional banking costs you 40,000 to 50,000 USD in cumulative fees and currency conversion spreads, while stablecoin settlement costs 5,000 to 10,000 USD. Yellow Card’s 2024 partnership with Xoom now enables residents in the US, UK, EU, and Canada to send stablecoins directly to Cameroon, Ivory Coast, and Senegal, with users increasingly preferring USDT over Bitcoin due to its stability. Faster settlement creates additional value because you access properties sooner and can begin generating rental income weeks earlier than traditional transactions allow.

Direct Settlement Without Intermediary Friction

Stablecoin transactions eliminate correspondent banks, currency brokers, and remittance services that traditionally extract margins at each step. When you send USDC on the Polygon blockchain, the transaction moves directly from your wallet to the seller’s or escrow provider’s wallet, with no intermediaries skimming fees along the way. Flutterwave’s May 2025 pilot using USDC on Polygon enabled merchants to process cross-border payments with instant settlements and lower fees, proving that blockchain infrastructure now supports real-world commerce. For property transactions, this matters because escrow services hold stablecoins on-chain while legal documentation receives verification, then release funds automatically when conditions are met through smart contracts. The seller receives payment confirmation within minutes rather than waiting for bank clearance, reducing the risk of deal collapse due to payment uncertainty. Due’s settlement solution uses regulated stablecoins across 90 plus countries with SOC 2 compliance, demonstrating that enterprise-grade infrastructure exists for these transactions. The direct transfer model also simplifies accounting because every transaction records immutably on the blockchain, making it trivial for tax authorities and auditors to verify the source and destination of funds.

Why Stablecoin Reserves Matter for Property Deals

The stability of your settlement currency depends entirely on the issuer’s reserves. USDC maintains transparent, independently audited reserves backed by cash or short-term U.S. Treasuries. The U.S. Commodity Futures Trading Commission fined Tether 41 million USD in 2021 for misleading reserve claims, highlighting why you should verify reserve transparency before committing large property funds. When you lock in a 500,000 USD property purchase, you need absolute certainty that your stablecoin maintains its peg. Prefer issuers compliant with regulatory standards like the EU’s MiCAR and the U.S. GENIUS Act, which influence how stablecoins can settle large cross-border payments and real estate purchases. Proof of Reserve verification adds another layer of confidence that your settlement currency won’t collapse mid-transaction.

Blockchain Records Create Audit Trails for Compliance

Every stablecoin transaction creates an immutable record on the blockchain that tax authorities and compliance officers can verify instantly. This transparency actually simplifies your AML obligations because you can prove the source and destination of every fund movement without relying on bank statements or intermediary confirmations. When you work with escrow services that hold stablecoins on-chain, the entire transaction history becomes auditable in real time. Smart contracts can automatically log when funds move from your wallet to escrow, when legal conditions are satisfied, and when the seller receives final payment-creating a complete compliance trail that traditional banking requires weeks to reconstruct. This audit capability becomes especially valuable in jurisdictions like the UAE, where AML registration is mandatory for real estate transactions under Federal Decree Law No. 20 of 2018, with penalties up to AED 5,000,000 for non-compliance. The blockchain record satisfies regulatory requirements while eliminating the paperwork burden that slows traditional deals.

Now that you understand how stablecoin settlement reduces costs and accelerates closings, the next critical step involves navigating the legal framework that governs these transactions across Africa and MENA.

Legal Requirements for Crypto Real Estate Purchases in Africa and MENA

AML and KYC Compliance Across Jurisdictions

Buying property across borders with stablecoins requires you to navigate AML and KYC regulations that vary significantly by jurisdiction. In the UAE, AML registration is mandatory for real estate transactions under Federal Decree Law No. 20 of 2018. The process starts with SACM pre-registration through the goAML portal managed by the UAE Financial Intelligence Unit, then progresses to full goAML registration that yields a unique registration number for ongoing reporting. You must appoint a dedicated AML Compliance Officer who is a UAE resident with Emirates ID and a residence visa. Documents including your trade license, ownership structure, and compliance officer credentials upload as a single PDF to SACM, which issues a username and secret key within 1 to 3 business days. Google Authenticator 2FA requires immediate configuration using the secret key.

Nigeria’s 2025 Investment and Securities Act placed virtual assets under SEC oversight, creating regulatory clarity for stablecoin transactions and real estate purchases. The country experiences over 30 billion USD in stablecoin flows annually, making it a leading African market for crypto property deals.

Identity Verification and Intermediary Selection

When you purchase property abroad, your intermediary or escrow provider must verify your identity through Emirates ID OCR, passport scanning, and trade license extraction using compliant verification tools like those offered through the Signzy MENA API marketplace, which consolidates UAE-specific verification into a single platform with automatic regulatory mapping across 180 plus countries. Licensed intermediaries like Schindler’s Digital Assets in South Africa hold CASP licensing and implement strict KYC diligence before converting your crypto to local currency and routing funds to the conveyancer’s trust account. The conveyancer then processes the sale as a standard cash deal through the deeds office, satisfying all legal requirements without directly handling cryptocurrency. Work exclusively with intermediaries that demonstrate transparent compliance processes and regulatory alignment in your target jurisdiction.

Title Verification and Legal Due Diligence

Title verification demands a completely different approach than traditional banking because blockchain records and legal deeds operate on separate systems. The Dubai Land Department requires final title registration in AED, meaning you cannot complete property ownership through stablecoins alone-you must have reliable on and off-ramp capabilities to convert stablecoins to local currency before closing. Smart contracts are legally recognized in the UAE under DIFC and VARA guidelines, enabling automated escrow and ownership transfers when properly coded, but only when paired with traditional legal documentation that satisfies Dubai Land Department requirements. Your lawyer must confirm that title searches, lien checks, and ownership verification are complete and clear before you convert stablecoins to local currency. This sequencing prevents you from holding currency conversion risk while legal due diligence continues.

Stablecoin Selection and Price Lock-In Strategy

For volatile assets like Bitcoin, use a price lock-in window of hours to days to mitigate market swings, while stablecoins like USDT offer greater flexibility due to their stability. USDT maintains transparent reserves and benefits from broad adoption across settlement platforms, making it a reliable choice for property transactions. USDC, backed by Coinbase and Circle, provides another option with independently audited reserves and regulatory credibility. The choice between stablecoins depends on your intermediary’s integration capabilities and your comfort with the issuer’s reserve structure. Coordinate on-ramp timing precisely with legal documentation-convert stablecoins to local currency only after your lawyer confirms that all title and ownership verification is complete and clear.

With the legal framework and compliance requirements now clear, the practical execution of your property purchase requires careful coordination of on-ramp solutions, escrow mechanics, and settlement timing to protect both parties and satisfy regulatory obligations.

Executing Your Property Purchase with Stablecoins

Timing Stablecoin Conversion to Protect Against Risk

Converting stablecoins to local currency at exactly the right moment separates successful property deals from transactions that collapse due to timing misalignment. The fundamental rule is simple: do not convert stablecoins to fiat until your lawyer confirms that title verification, lien searches, and ownership documentation are completely clear. This sequencing prevents you from holding currency conversion risk while legal due diligence continues in the background.

When you work with intermediaries like Schindler’s Digital Assets in South Africa, the process follows a rigid structure that protects both buyer and seller. Your stablecoins transfer to the intermediary’s regulated wallet while legal documentation moves through verification in parallel. Once your lawyer signs off on title clarity, the intermediary converts stablecoins to local currency and deposits funds into the conveyancer’s trust account within hours. The conveyancer then processes the sale as a standard cash transaction through the deeds office, satisfying all legal requirements without the seller ever touching cryptocurrency.

For UAE property purchases, timing becomes even more critical because the Dubai Land Department requires final title registration in AED. Your on-ramp provider must have reliable AED conversion capability and settlement speed of under 24 hours to avoid price volatility between your stablecoin conversion decision and actual title registration. Flutterwave’s May 2025 USDC integration on Polygon demonstrated that instant settlement infrastructure now exists for these transactions, but only if you work with platforms designed specifically for property settlement rather than generic payment processors.

Smart Contracts and Escrow Mechanics

Escrow services built for blockchain transactions protect both parties by holding stablecoins in smart contract accounts that release funds automatically when predetermined conditions are satisfied. Smart contracts legally recognized under DIFC and VARA guidelines in the UAE enable automated escrow and ownership transfers when properly coded, but this only works if your escrow provider has integrated title verification APIs that connect directly to property registries. Current platforms export compliant reports for regulatory review rather than syncing directly with Dubai Land Department systems, meaning your escrow smart contract cannot fully automate based on title registry confirmation alone.

Your escrow agreement must specify that funds remain locked until your lawyer manually verifies title clearance and provides written authorization to the smart contract administrator. This hybrid approach combines blockchain certainty with legal verification, eliminating the scenario where stablecoins release before title issues surface. Real property deals in the UAE using this structure include DAMAC’s asset-tokenization partnerships and Binghatti’s crypto-enabled sales, where escrow holds USDT or USDC while legal teams complete due diligence.

AML Compliance and Intermediary Selection

For cross-border deals, Binance Pay enables property payments directly, but only after both parties execute AML compliance through regulated intermediaries. Your AML obligations require that you document the source of your stablecoins through KYC verification, sanctions screening against PEP databases, and adverse media checks before funds move into escrow. Legal teams must verify that stablecoin issuers are properly licensed and compliant with applicable regulations.

Signzy’s MENA API marketplace consolidates these verification tools with automatic regulatory mapping across 180 plus countries, reducing compliance complexity and accelerating the screening process. The US Department of Justice seized 225 million USD in USDT linked to fraud operations, underscoring that weak KYC practices create legal exposure for all parties.

Work exclusively with intermediaries that implement real-time screening against sanctions lists and operate under SOC 2 compliance standards to minimize this risk.

Final Thoughts

Crypto real estate transactions in Africa and MENA eliminate the friction that has made cross-border property purchases expensive and slow. Stablecoins settle in minutes instead of weeks, reduce costs from 8 percent to under 3 percent, and create immutable audit trails that satisfy regulatory requirements without the paperwork burden of traditional banking. You gain access to property markets faster, lock in prices without currency volatility risk, and generate rental income weeks earlier than conventional deals allow.

The legal framework supporting these transactions has matured significantly. The UAE’s VARA licensing, Nigeria’s 2025 regulatory clarity, and South Africa’s CASP framework now provide clear pathways for compliant crypto property purchases. Smart contracts legally recognized under DIFC guidelines automate escrow mechanics while your lawyer verifies title clearance in parallel. AML registration, KYC verification, and sanctions screening have become standardized processes that intermediaries like Schindler’s Digital Assets and platforms using Signzy’s MENA API consolidate into single workflows.

Execution requires discipline around timing and intermediary selection. Convert stablecoins to local currency only after title verification is complete, work exclusively with regulated intermediaries that implement robust KYC and maintain SOC 2 compliance, and coordinate on-ramp and off-ramp solutions with your legal team to prevent currency conversion risk from derailing deals. Global stablecoin activity reached 27.6 trillion USD in 2024, Nigeria alone processes over 30 billion USD in stablecoin flows annually, and real developers like DAMAC and Binghatti are tokenizing properties and accepting crypto payments today-as blockchain infrastructure matures and regulatory frameworks solidify, crypto real estate will shift from emerging opportunity to standard practice across Africa and MENA. Web3 Enabler connects blockchain transactions directly to your Salesforce environment, enabling faster and cheaper payments that settle in seconds.

Crypto Real Estate FAQs

Can I legally buy real estate abroad using crypto or stablecoins in Africa and MENA?

It depends on the country and the transaction structure. In many cases, the purchase is treated as a standard cash deal in local currency, and crypto or stablecoins are used as the funding rail through a compliant intermediary that handles conversion, reporting, and documentation.

Do property registries accept stablecoins directly?

Most land departments and registries still require final settlement and title registration in local fiat currency. Stablecoins typically fund the transaction, then convert to local currency before closing and registration.

How does an escrow process work with stablecoins?

Stablecoins can be held in escrow by a regulated intermediary or an escrow arrangement that documents when funds are received, held, and released. Release is usually tied to legal milestones like title verification, signed closing documents, and confirmation from the conveyancer or attorney handling the transfer.

When should I convert stablecoins to local currency during a property purchase?

A common best practice is to wait until legal due diligence is complete, including title checks, lien searches, and seller verification. Converting too early can expose you to timing issues if the deal stalls or if additional documentation is required.

What documents do I need to prove the source of funds for a crypto-funded property deal?

Expect to provide identity verification, proof of address, and source-of-funds documentation. This often includes exchange statements, transaction hashes, wallet ownership evidence, and documentation tying the funds to legitimate income or business activity.

Which stablecoins are typically used for cross-border real estate purchases?

USDC and USDT are commonly used because they are widely supported by exchanges and payment partners. The right choice is usually the one your intermediary can settle reliably in your target country with clear fees, strong liquidity, and compliant reporting.

How do I protect against price changes or timing risk during closing?

Use a clear timing plan with your legal team and intermediary, and avoid funding the transaction with volatile assets unless you have a defined conversion window. Many buyers use stablecoins specifically to reduce exposure to sudden price swings during settlement.

Do I need a crypto wallet to buy property using stablecoins?

Sometimes. Some buyers fund escrow from their own wallet, while others pay through a regulated platform that abstracts wallet management. The exact setup depends on the intermediary, the corridor, and the compliance requirements.

How do taxes work on crypto real estate purchases?

Tax treatment varies by country and by your residency. Some jurisdictions treat crypto conversion as a taxable event, even if the proceeds are used immediately for a property purchase. It’s best to confirm reporting and tax obligations with a qualified tax advisor in both your home country and the property’s jurisdiction.

What’s the biggest risk in crypto-funded real estate deals?

The biggest risks are usually compliance gaps, weak intermediaries, and poor coordination between legal due diligence and funding. Using regulated partners, maintaining clean documentation, and aligning the escrow and conversion timeline with the closing process reduces these risks significantly.