African and Middle Eastern businesses face real friction when moving money across borders. Traditional banking channels are slow, expensive, and often unreliable for B2B transactions.

B2B stablecoin payments offer a direct alternative. They cut settlement times from days to minutes and reduce costs by up to 80% compared to wire transfers. At Web3 Enabler, we’ve seen growing momentum in these regions as companies discover faster ways to pay suppliers, contractors, and manage working capital.

This guide covers the platforms, use cases, and implementation steps that matter most for your business.

Why These Markets Need Stablecoin Payments Now

The Real Cost of Traditional Cross-Border Payments

African and Middle Eastern businesses hemorrhage money every day through correspondent banking delays and FX markups. A supplier payment from Lagos to Dubai takes 5–7 business days through traditional wire transfers, during which funds sit frozen and exchange rates shift constantly. The cost compounds quickly: a USD 50,000 supplier invoice can lose USD 2,400 to bank fees and unfavorable spreads. Mordor Intelligence reports that FX markups on exotic corridors average 4.8%, with bid-ask spreads reaching 300 basis points in frontier markets where liquidity fragments across dozens of small banks. Treasury teams in these regions have no choice but to overfund accounts weeks in advance, tying up working capital that could fund growth instead.

De-risking pressures make the problem worse. The World Bank reported that 127 African bank relationships were terminated in 2024–2025 alone, forcing remittances through expensive hubs like UAE and South Africa and adding days to settlement. This squeeze hits small and mid-sized exporters hardest-they lack the banking relationships that larger corporations maintain, so they pay premium rates on every transaction.

How Stablecoins Eliminate Friction

Stablecoins collapse this friction into seconds. A USDC transfer settles in under a minute, 24/7, with transparent on-chain costs under 0.1%. No intermediaries. No prefunding. No waiting for correspondent banks to process batches. With Web3 Enabler’s Salesforce integration, businesses can initiate supplier payments directly from their existing CRM, with transactions settling instantly on the blockchain while data flows back into accounting records automatically.

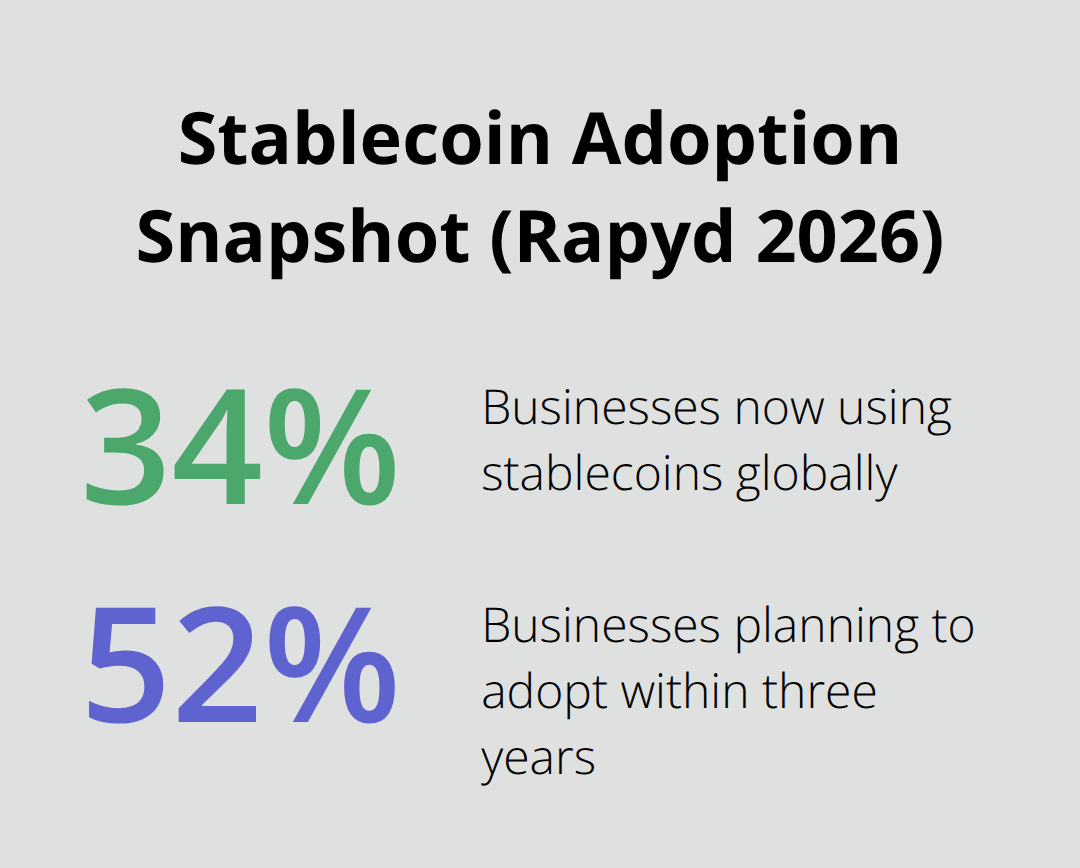

Adoption is accelerating globally. Rapyd’s 2026 State of Stablecoins report shows that 34% of businesses now use stablecoins, with 52% planning adoption within three years. In the Gulf specifically, capital has surged into fintech infrastructure-investment hit USD 7.5 billion with 58% flowing to fintech companies, according to Wamda Research. McKinsey projects 35% annual fintech revenue growth across MENA through 2028, nearly triple the global average.

Regional Momentum and Regulatory Support

Regulatory sandboxes across 11 Gulf jurisdictions now let companies test stablecoin rails under supervision, offering predictability in cross-border financial planning. Saudi Arabia’s engagement is strongest: 50% of small businesses under USD 500k annual revenue already use digital wallets for cross-border payments, and 14% of Saudi consumers have made at least one cross-border transaction. Real-time settlement via stablecoins directly addresses the region’s pain-supplier payments that once took a week now settle instantly, and working capital that was locked in float becomes available for operations.

This shift from experimental pilots to operational infrastructure means treasury teams across Africa and the Middle East can now move beyond traditional banking constraints. The next section examines the specific B2B workflows where stablecoins deliver the biggest impact.

Key Use Cases for B2B Stablecoin Payments

Supplier Payments and Invoice Settlement

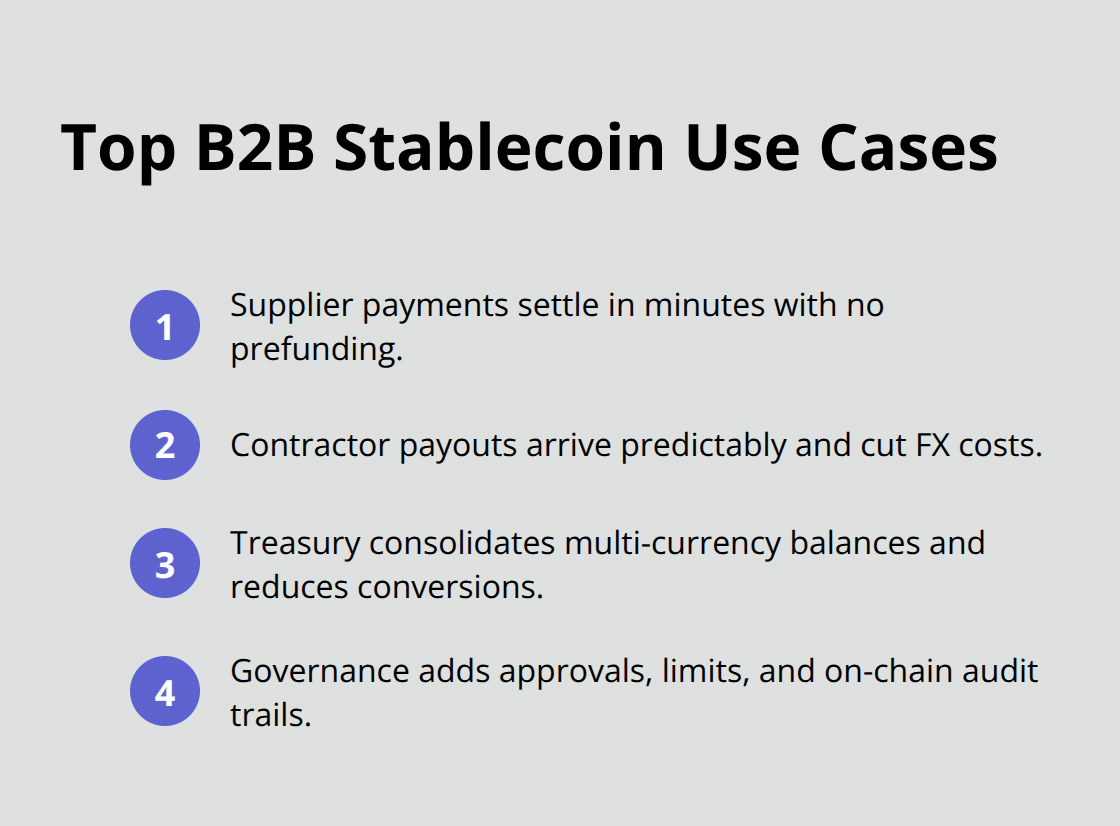

Supplier payments represent the largest immediate opportunity for stablecoin adoption in African and Middle Eastern businesses. A manufacturer in Cairo paying a component supplier in Lagos no longer waits five business days for wire settlement. With stablecoins, the payment settles in minutes, and the supplier receives funds immediately in their local wallet. Invoice-to-cash cycles compress significantly, which demonstrates the operational advantage for businesses managing hundreds of monthly supplier invoices. This speed eliminates the need to overfund accounts or negotiate extended payment terms to compensate for float. USDC-based settlement via platforms like NymCard and Visa now enables 24/7 settlement with zero prefunding, meaning capital stays in operations instead of frozen in transit. The cost advantage proves equally stark-a USD 50,000 supplier invoice costs roughly USD 1,500 in bank fees and FX spreads through traditional channels but under USD 50 through stablecoin rails.

International Contractor and Freelancer Payouts

International contractor and freelancer payouts follow the same efficiency pattern but address different pain points. A marketing agency in Lagos paying web developers across five countries faces currency conversion fees on each transaction, manual invoice tracking across spreadsheets, and delayed payments that damage contractor relationships. Stablecoin payouts eliminate these friction points entirely.

Contractors receive payments in USDC within minutes, then convert locally at their chosen exchange, avoiding the FX markup that traditional remittance channels extract. This approach transforms how teams manage global talent-payments arrive predictably, contractors maintain stronger relationships with agencies, and finance teams reduce administrative overhead significantly.

Treasury Management and Working Capital Optimization

Treasury management improves measurably when businesses adopt multi-currency stablecoin accounts. Instead of holding separate balances in five bank accounts across different jurisdictions, teams consolidate USD, EUR, and regional currencies in a single wallet, execute FX conversions only when operationally necessary, and reduce conversion frequency from daily to weekly or monthly. This approach cuts FX costs significantly in high-volatility corridors. For working capital optimization specifically, companies that shift portions of their cross-border payments to stablecoin rails free up working capital from float. Small businesses in Saudi Arabia are already capturing this benefit-digital wallets for cross-border payments signal that the infrastructure and user behavior are moving faster than many executives realize.

Governance and Compliance Foundations

The mechanics require clear governance to turn stablecoin payments from experimental pilots into repeatable, compliant operational processes. Establish beneficiary controls, transaction approval workflows, FX exposure limits, and audit trails that track both fiat and on-chain activity. Finance teams need systems that connect blockchain transactions to existing corporate infrastructure-this integration ensures that stablecoin payments flow seamlessly into accounting records and treasury dashboards without manual reconciliation. The next section examines the platforms and integration approaches that make this governance practical and scalable.

Leading Platforms and Solutions for B2B Stablecoin Payments

Platform Categories and Core Strengths

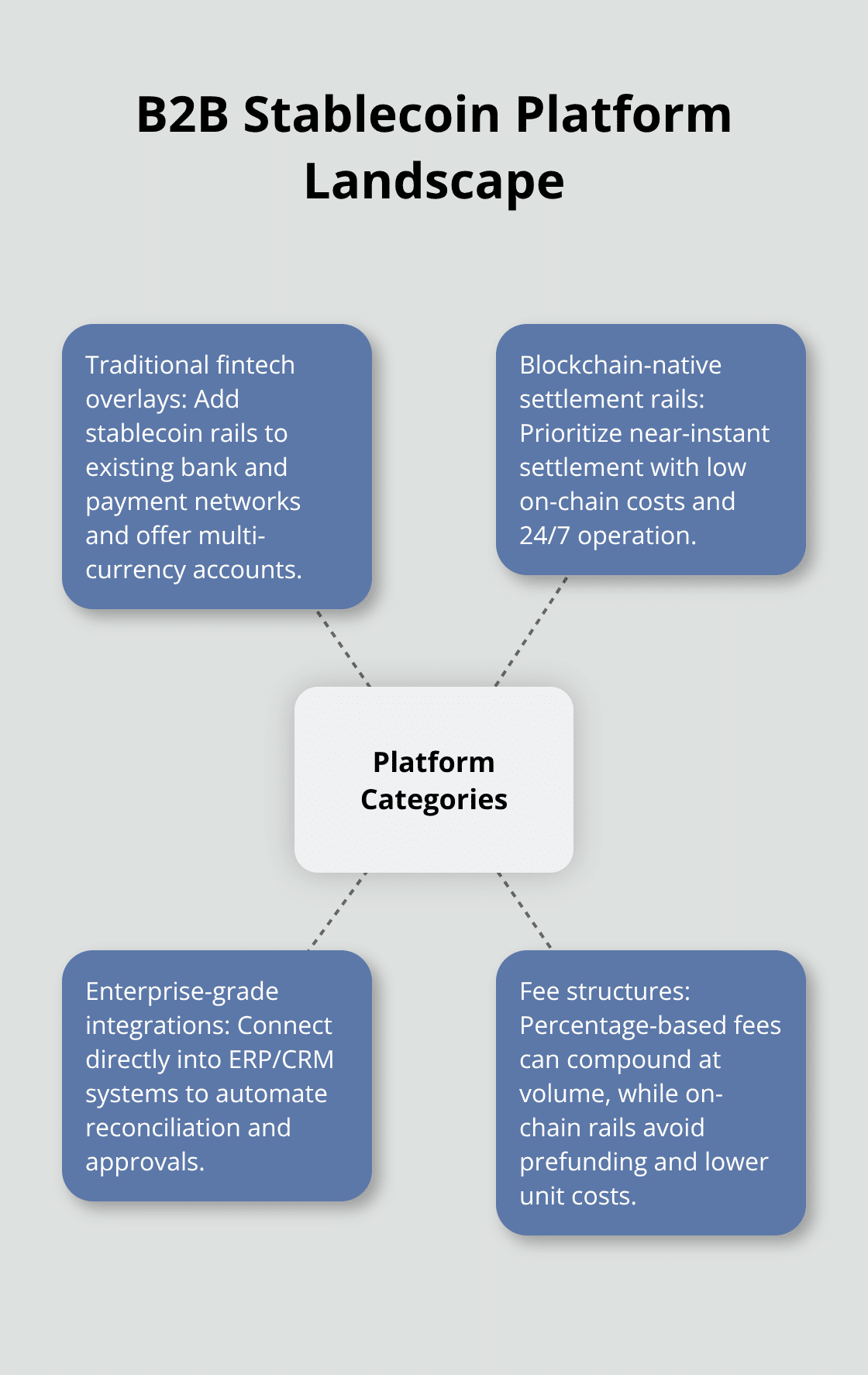

The market has fragmented into three distinct categories: traditional fintech overlays that add stablecoin rails to existing payment infrastructure, blockchain-native platforms that prioritize settlement speed, and enterprise-grade solutions that integrate directly into your existing systems. Rapyd stands out in the first category, offering stablecoin solutions alongside multi-currency business accounts and cross-border payment infrastructure across regulated jurisdictions in the US, EU, UK, and Singapore. The platform targets B2B payments, eCommerce, and marketplaces, with 72% of surveyed businesses citing faster payments and settlement as the primary benefit and 62% highlighting easier cross-border transactions.

However, Rapyd charges transaction fees that typically range from 1-2% depending on corridor and volume, which compounds quickly for high-frequency supplier payments.

NymCard and Visa’s USDC settlement partnership launched live in the Gulf and represents the second approach: USDC transfers settle in under one minute with near-zero on-chain costs under 0.1%, and the 24/7 settlement eliminates the prefunding trap that traditional banking imposes. For African and Middle Eastern businesses specifically, this matters enormously because you can pay suppliers in real time without locking capital in float.

Integration with Your Existing Systems

Integration with your existing ERP and accounting systems separates viable platforms from expensive experiments. Most traditional fintech platforms offer API access to accounting software like QuickBooks or NetSuite, but the integration requires custom development and manual invoice mapping to blockchain transactions. This approach works for companies with dedicated development teams but creates maintenance headaches as your transaction volume scales.

Web3 Enabler connects blockchain transactions directly to your Salesforce environment without requiring separate systems or manual reconciliation. Transactions settle in seconds while data flows automatically into your CRM and connected accounting systems in real time, eliminating the administrative overhead that most stablecoin platforms force onto finance teams. You can manage international contractor payments and track settlement status all within Salesforce, transforming how your team handles cross-border operations.

Compliance Frameworks and Regulatory Pathways

Governance and compliance separate experimental pilots from repeatable operational processes. Establish clear approval workflows tied to invoice amounts and beneficiary categories before selecting any platform. The World Bank reports that 127 African bank relationships terminated in 2024-2025, forcing businesses toward alternative rails, which makes regulatory clarity non-negotiable.

Gulf regulatory sandboxes across 11 jurisdictions now provide supervised environments to test stablecoin payments with clear licensing pathways, and McKinsey projects 35% annual fintech revenue growth across MENA through 2028, indicating that regulators actively support this transition. Your compliance framework needs to map AML/KYC requirements by destination country, assign clear ownership for sanctions screening, establish transaction approval limits tied to risk profiles, and maintain audit trails that regulators can access. Platforms operating under FinCEN, FCA, or MAS licenses provide stronger compliance foundations than unregulated alternatives, though network partners can deliver compliant services in less-regulated jurisdictions.

Cost Comparison and Fee Structures

Cost comparison reveals that stablecoins are increasingly recognised for real-world utility in B2B payments, but fee structures vary dramatically. NymCard and Visa’s USDC rails charge minimal transaction fees with no prefunding requirements, while Rapyd’s broader infrastructure requires percentage-based fees that compound across monthly transaction volumes.

For a business executing 200 supplier payments monthly at an average USD 25,000 per transaction, traditional wire transfers cost roughly USD 60,000 annually in bank fees and FX spreads. Stablecoin platforms through Rapyd cost approximately USD 12,000-15,000, and USDC settlement via NymCard costs under USD 2,000. This calculation assumes 2% average fees for Rapyd and 0.1% for USDC settlement, so your actual costs depend on transaction size and corridor selection.

Final Thoughts

B2B stablecoin payments eliminate the operational friction that has constrained African and Middle Eastern businesses for decades. Your supplier payments settle in minutes instead of days, your working capital stays in operations instead of frozen in transit, and your finance team stops hemorrhaging money to bank fees and unfavorable FX spreads. Rapyd reports that 34% of businesses now use stablecoins operationally, with 52% planning adoption within three years, while McKinsey projects 35% annual fintech revenue growth across MENA through 2028.

Start your pilot with a single high-volume payment corridor where the operational pain cuts deepest. If your business executes 50+ monthly supplier payments to a single country, that corridor becomes your test case-map your current costs precisely, then execute 10–20 stablecoin transactions through your chosen platform and measure the actual time and cost difference. Track settlement time from initiation to beneficiary confirmation, total cost per transaction including all fees and FX conversion, and reconciliation time from blockchain settlement to accounting record completion.

Web3 Enabler connects blockchain transactions directly to your Salesforce environment, eliminating the manual reconciliation that makes most stablecoin pilots expensive to operate. Your finance team manages international contractor payments and tracks settlement status within Salesforce, transforming how your organization handles cross-border operations without requiring separate systems or custom development. The infrastructure exists, the regulatory pathways are clear, and the only remaining question is whether your business moves first or watches competitors capture the efficiency gains that B2B stablecoin payments deliver.