The digital payments industry is growing fast, and employers are actively seeking professionals who can prove their expertise. A digital payments certification demonstrates your competence to employers and clients, setting you apart in a competitive job market.

At Web3 Enabler, we’ve seen firsthand how certification holders advance their careers and command higher salaries. This guide walks you through the certification options, exam preparation strategies, and the real benefits waiting for you on the other side.

Why Digital Payments Certification Matters

The Job Market Demands Certified Professionals

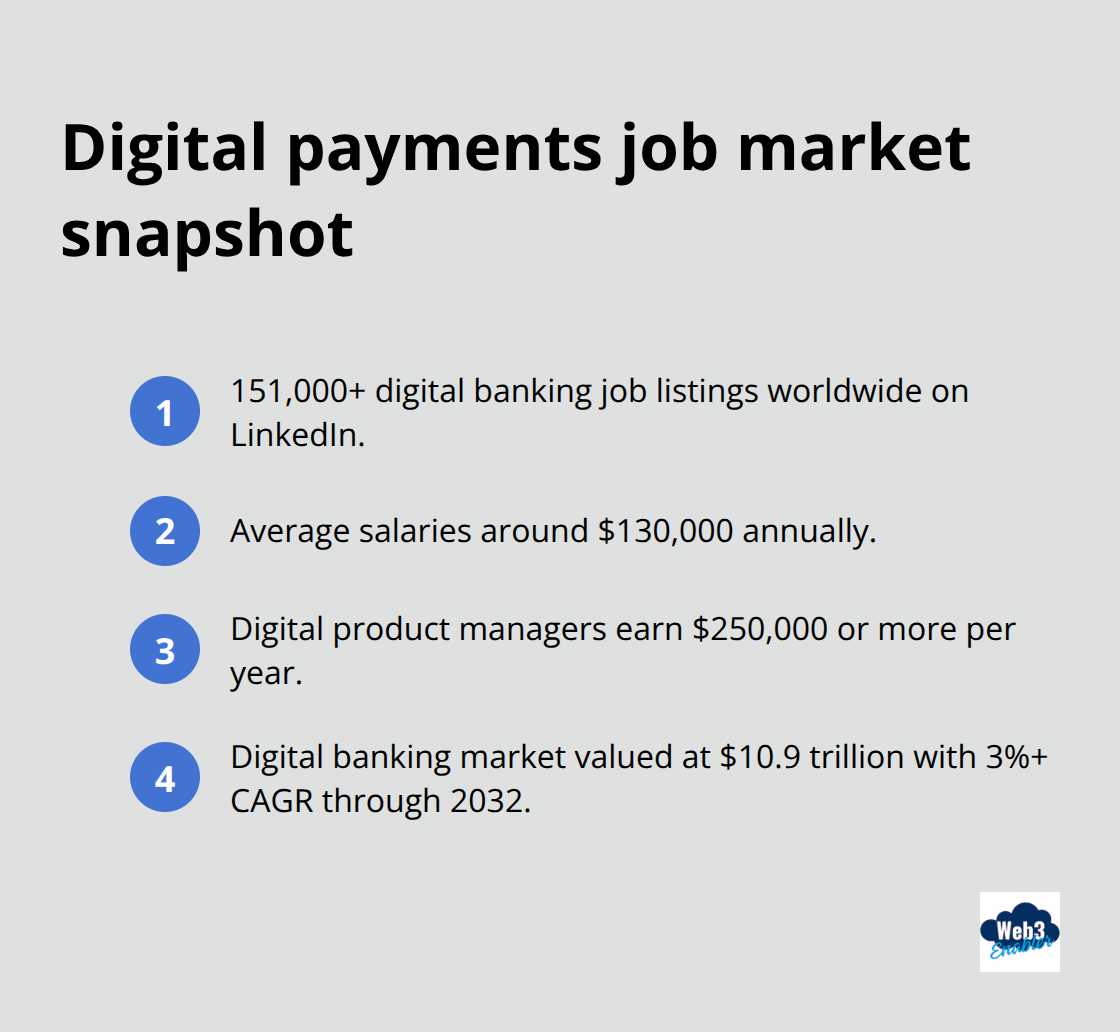

The job market for digital payments professionals expands faster than qualified candidates fill roles. LinkedIn data shows over 151,000 digital banking job listings worldwide, with average salaries around $130,000 annually and digital product managers earning $250,000 or more per year.

The digital banking market was valued at $10.9 trillion in 2023 and is estimated to grow at a CAGR of over 3% between 2024 and 2032, creating genuine demand for professionals who understand how payments actually work. Without certification, you compete against candidates who prove their competence on day one. With it, you position yourself as someone who understands the full stack-from onboarding flows to card management, settlement, and compliance frameworks like PSD2 and KYC requirements. Employers hire based on demonstrated expertise, not potential.

Certification Proves Real Competence

Certification accelerates your path to higher-paying roles because it signals you studied real payment architecture, not just theory. The four-layer digital banking architecture and seven key customer journeys aren’t abstract concepts-they determine whether a payment system succeeds or fails. When you understand digital onboarding, account opening, card lifecycle, and API-driven ecosystems (the core components of modern payment platforms), you contribute immediately to projects that matter. Companies moving away from branch-based banking toward mobile-first payment experiences need people who already learned what works.

Why Certification Matters Now

The difference between a certified professional and an uncertified one often comes down to months of accelerated learning compressed into a structured program. That efficiency translates directly into salary negotiations and advancement timelines. In a field where branch networks decline and digital channels dominate everything, certification represents the fastest way to become genuinely valuable. Your next step involves understanding which certification options actually align with your career goals and current experience level.

Which Digital Payments Certification Should You Choose

Comparing Program Structure and Format

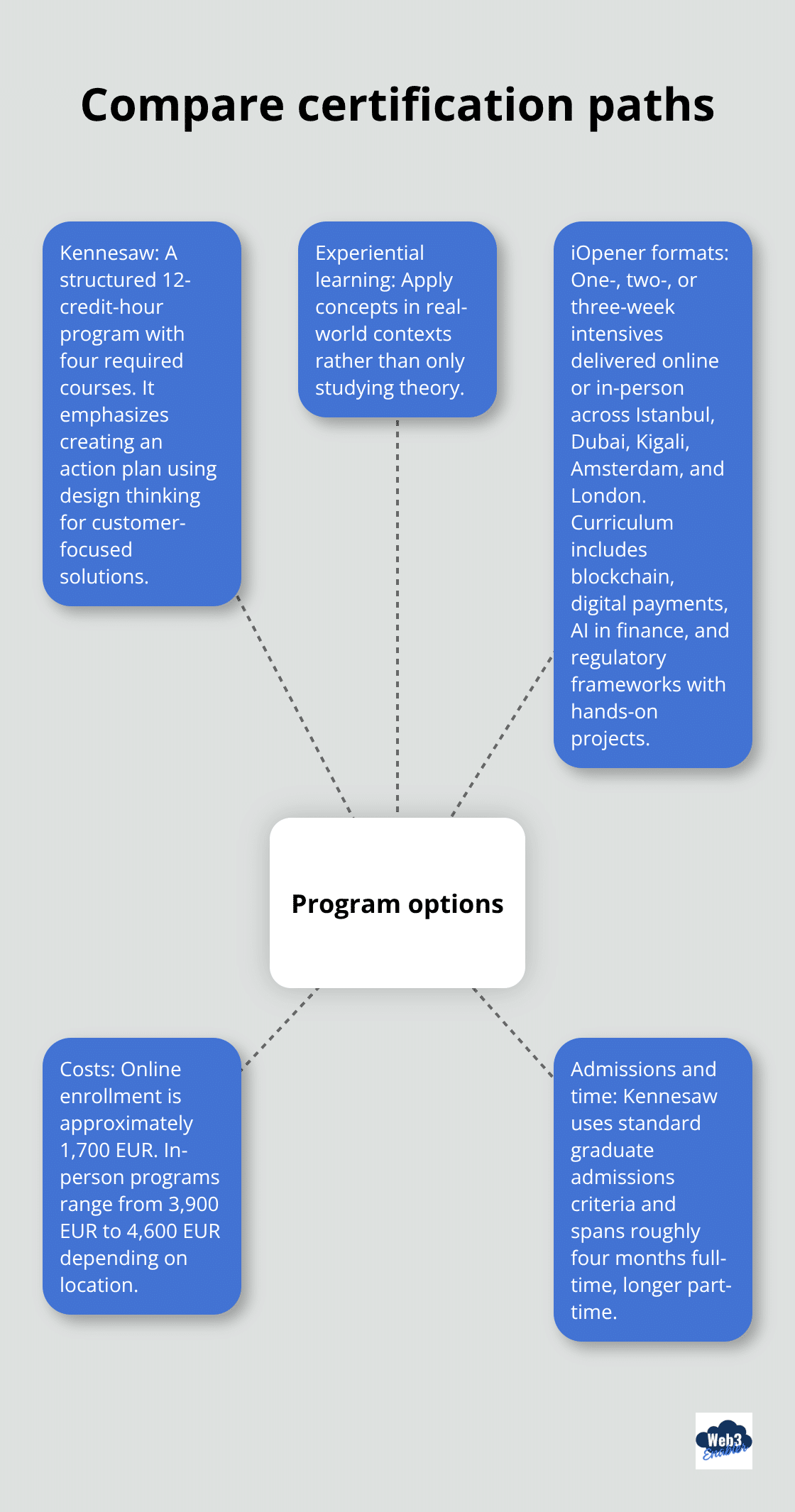

The market offers several legitimate digital payments certifications, but they differ significantly in depth, cost, and industry recognition. The Financial Technology Certificate from Kennesaw State University’s Michael J. Coles College of Business stands out as a structured 12-credit-hour program composed of four required courses: Payments Processing in FinTech, FinTech Payments Security and Assurance, Emerging FinTech Payments Technologies, and Experiential Learning in FinTech Payments. This program explicitly teaches you how to create an action plan for digital payments innovation within an organization, using design thinking to develop customer-focused solutions. The experiential learning component means you apply concepts in real-world contexts rather than just studying theory.

iOpener Training Center offers the Mastering Digital Finance & FinTech course with a Digital payments certification available in flexible formats: one-, two-, or three-week intensives delivered online or in-person across Istanbul, Dubai, Kigali, Amsterdam, and London. Their curriculum covers blockchain, digital payments, AI in finance, and regulatory frameworks with hands-on projects like designing a digital payment solution. Online enrollment costs approximately 1,700 EUR while in-person programs range from 3,900 EUR to 4,600 EUR depending on location.

Entry Requirements and Time Investment

Admissions to Kennesaw’s program require only meeting the university’s standard graduate admission criteria, so no specialized prerequisites block entry. The total time investment spans roughly four months at full-time pace, though part-time enrollment extends this timeline. iOpener’s intensive formats compress essential knowledge into weeks, making them ideal for professionals who need rapid upskilling and prefer concentrated learning over semester-long study.

Matching Your Learning Style to the Right Program

The real decision hinges on your timeline and learning style. If you work full-time and want depth without rushing, Kennesaw’s certificate program delivers structured knowledge of payment architecture, security protocols, and compliance frameworks over several months. If you have limited time or want to test your interest before committing heavily, iOpener’s intensive formats work better for your situation.

Neither program requires prior payments experience, though both assume comfort with financial concepts. Kennesaw graduates complete a capstone action plan that demonstrates practical capability, while iOpener participants earn certification through project work and final presentations. Banks have invested over one trillion dollars in digital banking recently, meaning employers actively hire people who finish these programs.

Cost Considerations and Value

The cost difference matters significantly. Kennesaw’s program costs substantially less than most in-person iOpener sessions, though exact pricing depends on your location and whether you attend part-time or full-time. The investment you make should align with your career timeline and financial situation.

What to Look for in Any Program

Whichever path you select, verify that the program covers the four layers of digital banking architecture, the seven key customer journeys (onboarding, account management, card issuance), and practical topics like API security, card lifecycle management, and KYC processes. Programs lacking hands-on labs or real-world projects leave you unprepared for actual job responsibilities. Your next step involves understanding how to prepare effectively once you’ve selected your certification program.

How to Actually Prepare for Your Certification Exam

Map Your Program’s Content First

Certification exams test whether you can apply payment concepts to real business problems, not memorize definitions. The programs at Kennesaw and iOpener structure their assessments around practical scenarios: designing payment flows, identifying security gaps, and solving compliance challenges. This means your study approach should mirror actual job work rather than traditional test cramming.

Start by mapping what each program explicitly covers. Kennesaw’s four courses address payments processing, security, emerging technologies, and real-world application, so your materials should include their course syllabi, assigned readings on PSD2 and KYC frameworks, and case studies showing how banks implement digital onboarding. iOpener’s curriculum emphasizes hands-on projects designing payment solutions and analyzing cross-border payment workflows, so you need materials that show actual implementation steps, not theoretical concepts.

Build Your Foundation Before Practice Tests

The best study approach involves working through sample scenarios before touching practice questions. Spend your first two weeks understanding the four-layer digital banking architecture and the seven key customer journeys (onboarding, account management, card issuance, payments, settlement, dispute resolution, and analytics). This foundation prevents you from memorizing disconnected facts.

Next, work through any sample projects your program provides. If Kennesaw requires a capstone action plan, study examples of real organizational payment strategies. If iOpener includes design projects, complete them under timed conditions to simulate actual exam pressure.

Use Practice Materials That Match Your Program

Practice tests matter, but only if they match your program’s assessment format. Generic payment industry quizzes waste time because they test breadth over depth. Instead, use practice materials directly from your chosen program or vetted third-party sources aligned with their curriculum.

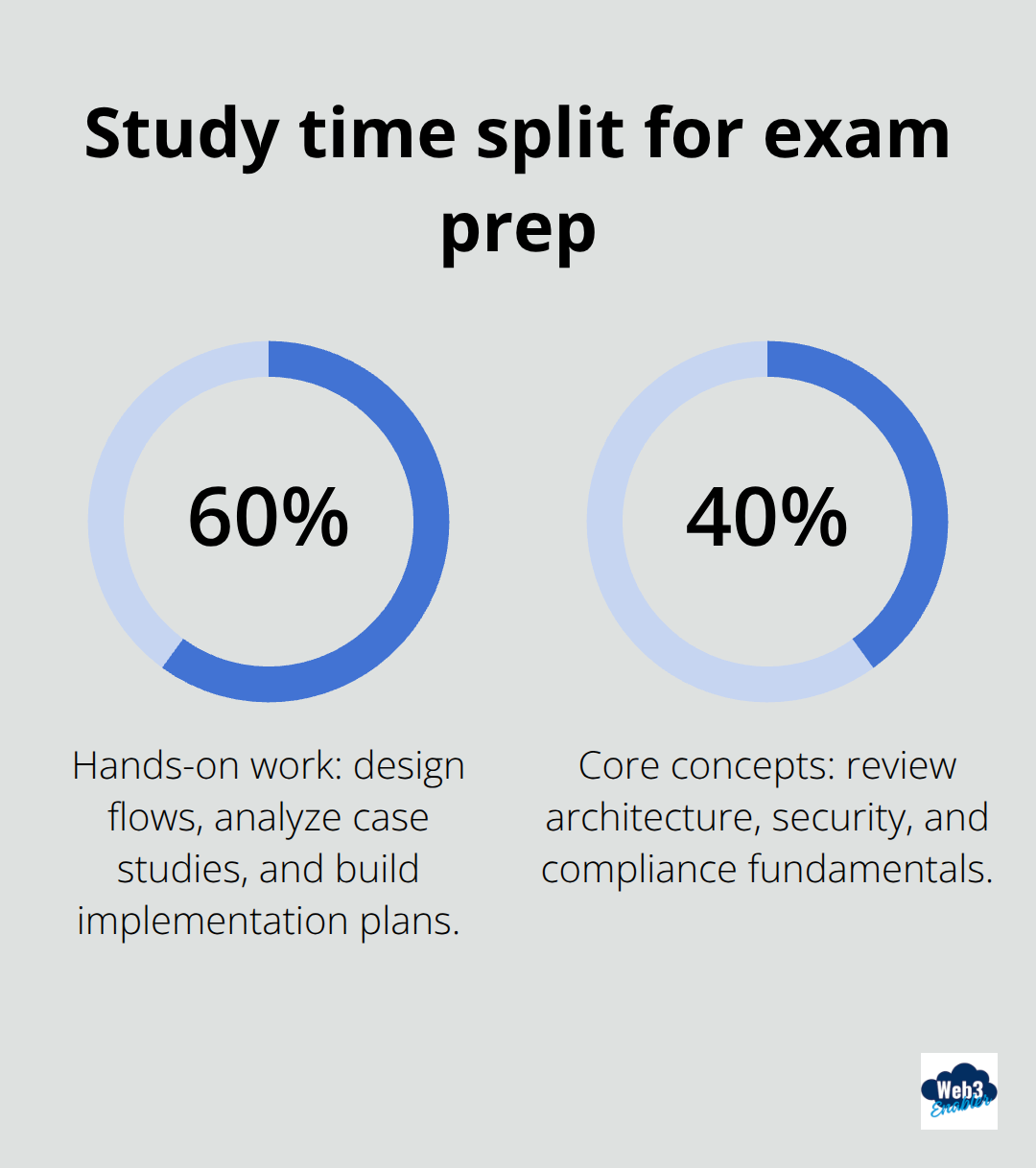

Allocate roughly 60% of study time to hands-on work (designing flows, analyzing case studies, building implementation plans) and 40% to reviewing core concepts. Most professionals underestimate how much time payment security and compliance topics require. PSD2 Strong Customer Authentication, KYC processes, and anti-money laundering frameworks appear throughout both programs because they determine whether payment systems actually work in regulated markets. Dedicate specific study blocks to these areas rather than treating them as secondary topics.

Schedule Study Sessions Around Your Reality

Schedule study sessions around your work calendar realistically. If you work full-time, Kennesaw’s semester-long program fits better than iOpener’s intensive format because you can study 10-15 hours weekly spread across four months rather than attempting 40+ hours weekly during a compressed timeline. Whatever your timeline, consistency beats intensity.

Three focused study hours daily outperform weekend cramming sessions because your brain consolidates payment architecture concepts more effectively through spaced repetition. Track which topics give you trouble and revisit them multiple times rather than moving forward hoping understanding improves.

Final Thoughts

Your digital payments certification represents a concrete investment in your career at a moment when the industry genuinely needs qualified professionals. The 151,000 digital banking job listings worldwide and the trillion-dollar investment banks have made in digital infrastructure mean employers actively hire people who complete these programs. After obtaining your certification, update your resume and LinkedIn profile to highlight specific competencies: payment processing, security frameworks, API integration, and regulatory compliance.

Within your first month post-certification, apply to roles that explicitly mention digital payments, payment platform development, or FinTech implementation. Entry-level certified professionals typically move into payment operations, compliance, or technical implementation roles within six months. Mid-career advancement leads to payment strategy, product management, or architecture positions where your understanding of the four-layer digital banking architecture directly influences business decisions.

The professionals earning $250,000 annually as digital product managers built expertise through structured learning, real-world application, and continuous skill development. We at Web3 Enabler work with organizations implementing blockchain-based payment solutions, and we consistently see that certified professionals advance faster because they understand both traditional payment systems and emerging technologies. If you want to explore how blockchain and stablecoins integrate with existing payment infrastructure, Web3 Enabler provides Salesforce-native solutions for businesses ready to modernize their payment capabilities.