![Ensuring Regulatory Compliance in Crypto Transactions [Guide]](https://web3enabler.com/wp-content/uploads/emplibot/crypto-compliance-hero-1758197377.jpeg)

Crypto compliance isn’t just a buzzword anymore – it’s the difference between thriving and getting shut down by regulators. The wild west days of crypto are officially over.

We at Web3 Enabler see businesses scrambling to figure out which rules apply to them. The regulatory maze gets more complex every month, with new requirements popping up faster than meme coins.

This guide cuts through the confusion and shows you exactly what you need to know.

Who Sets the Rules for Crypto Business?

The Securities and Exchange Commission controls most crypto trading rules in the United States, while FinCEN handles money laundering prevention requirements. The Commodity Futures Trading Commission oversees crypto derivatives, which creates a three-way regulatory split that confuses even experienced compliance teams. The GENIUS Act amends existing federal financial law to clarify that the terms “security” and “commodity” do not include the payment stablecoins of a PPSI.

The Big Three Regulators You Cannot Ignore

The SEC treats most cryptocurrencies as securities and demands registration and disclosure requirements that mirror traditional stock offerings. FinCEN requires crypto businesses to implement Bank Secrecy Act compliance, which includes suspicious activity reports for transactions over $10,000. The CFTC focuses on Bitcoin and Ethereum as commodities and applies derivatives rules to futures and options trades. Each agency operates independently, which creates compliance gaps that cost businesses millions in penalties.

Why Crypto Rules Differ from Traditional Finance

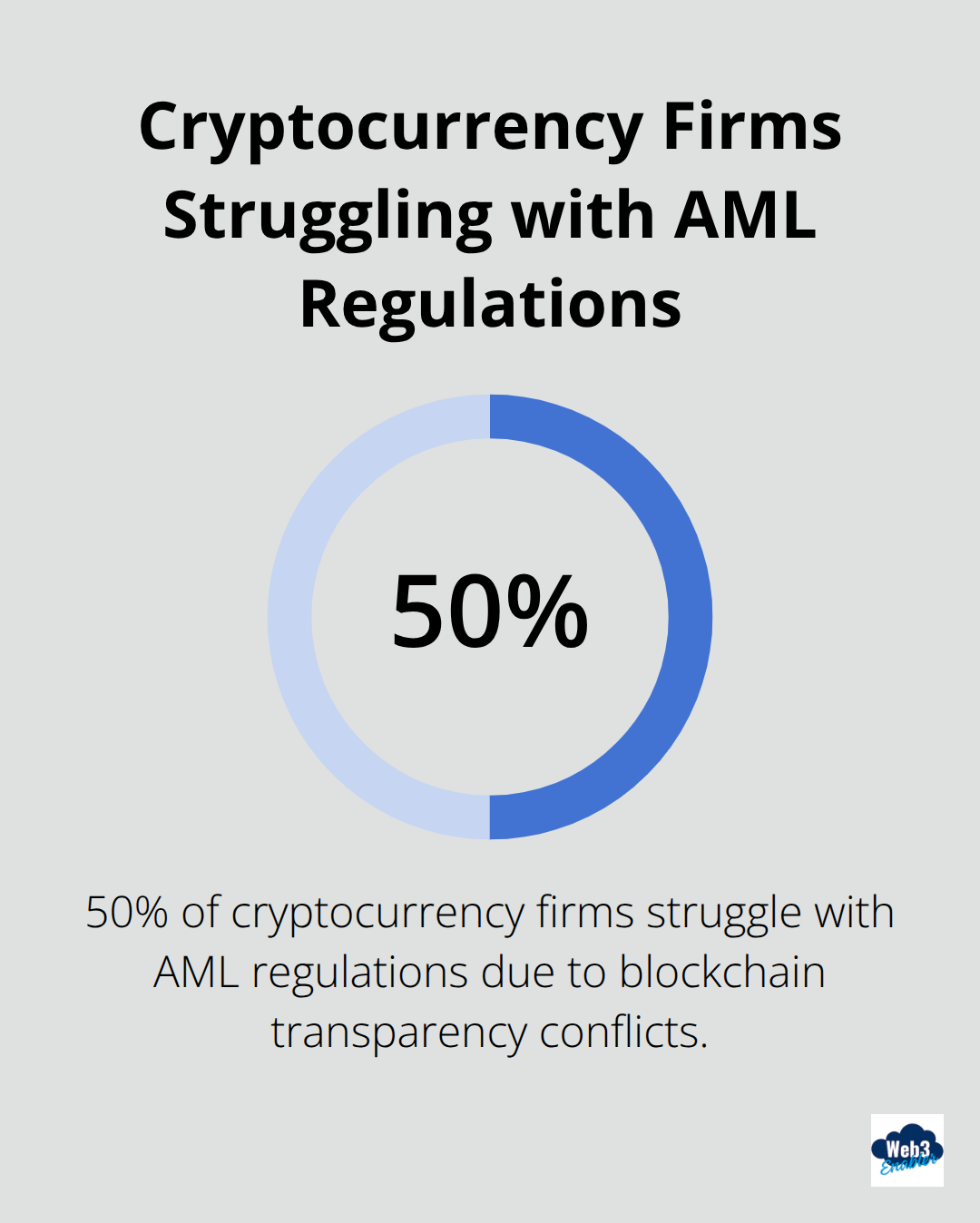

Traditional banks follow decades-old regulations that were written for centralized institutions with clear geographic boundaries. Crypto operates across borders instantly, which makes jurisdiction selection a real compliance nightmare. The Financial Action Task Force reports that 50% of cryptocurrency firms struggle with AML regulations because blockchain transparency conflicts with privacy expectations.

Banks rely on correspondent relationships for international transfers, while crypto transactions settle directly on public ledgers without intermediaries. This fundamental difference forces regulators to rewrite compliance playbooks from scratch.

State vs Federal Jurisdiction Wars

New York’s BitLicense and California’s Digital Finance Assets Law show how states create their own crypto rules (often stricter than federal requirements). Companies face a patchwork of state regulations that can contradict federal guidance. Some states welcome crypto businesses with open arms, while others treat them like radioactive waste.

The compliance burden multiplies when you operate across state lines, and legal teams spend more time on regulatory mapping than actual business strategy.

What Compliance Steps Actually Matter?

Crypto businesses must implement identity verification systems that capture government-issued photo IDs, proof of address documents, and beneficial ownership information for corporate accounts. The Financial Action Task Force provides a comprehensive framework to help countries fight financial crimes and promote financial transparency, while ongoing monitoring must flag transactions that exceed $3,000 in daily volume. Most compliance failures occur because businesses rely on basic KYC software that cannot handle the complexity of crypto transaction patterns.

Customer Verification That Actually Works

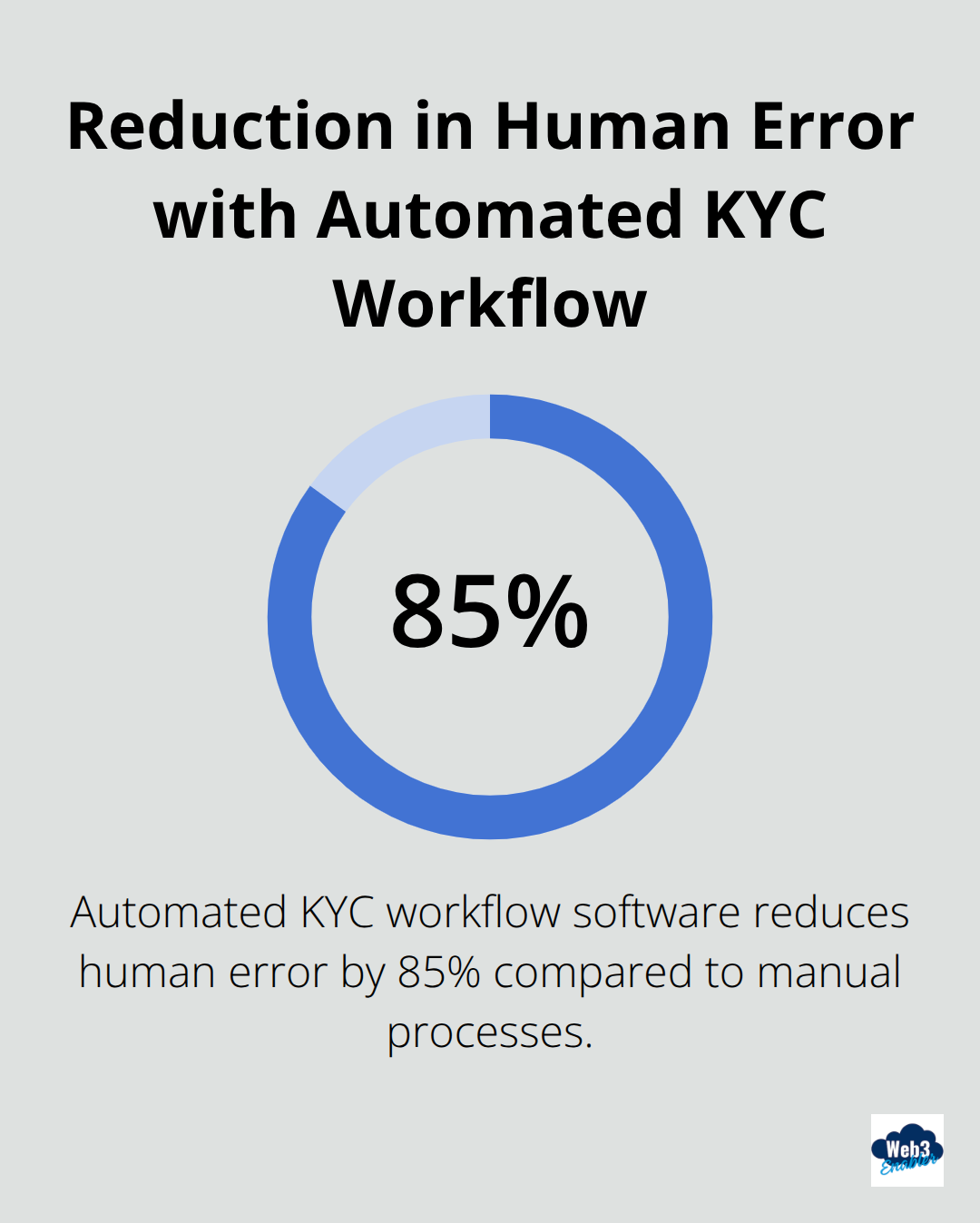

Automated KYC workflow software reduces human error by 85% compared to manual verification processes (according to recent industry studies). Your verification system must cross-reference customer data against OFAC sanctions lists, politically exposed persons databases, and adverse media screening tools in real-time. Companies should implement continuous sanctions screening rather than one-time checks, because regulatory lists update daily and missing a sanctioned entity costs an average of $2.8 million in penalties.

Document scanning technology with facial recognition capabilities prevents identity fraud, while blockchain analytics tools track the source of funds to identify high-risk transactions before they hit your platform. The most effective systems combine multiple verification layers to catch sophisticated fraud attempts.

Transaction Monitoring Without the Headaches

Real-time transaction monitoring systems must generate suspicious activity reports for cash transactions over $10,000, but crypto businesses need lower thresholds because digital assets move faster than traditional bank transfers. Your monitoring system should flag structuring patterns, rapid-fire transactions, and connections to known criminal wallets automatically.

The most effective compliance teams use blockchain intelligence platforms that provide transaction histories and risk scores for every wallet address. These tools help identify money laundering schemes that span multiple exchanges and mixing services (which traditional banking systems cannot track). Smart monitoring catches patterns that human analysts miss, especially when criminals split large transactions across multiple wallets.

Record Keeping That Survives Audits

The SEC plans to expand recordkeeping regulations to include cryptocurrency firms, which means your documentation standards need to match traditional financial institutions. Rule 17a-3 requires broker-dealers to maintain specific records related to business operations, and this will now include crypto-related transactions. Rule 17a-4 mandates the preservation of books and records with quick access for eDiscovery purposes.

Companies must capture and archive all business communication channels, because 39% of firms have already started this practice due to increased scrutiny. Your compliance technology stack needs automated tools that handle the complexity of blockchain transactions while meeting traditional audit requirements.

Which Compliance Tools Actually Work?

TRM Labs dominates blockchain analytics with transaction monitoring that processes transactions across 300+ cryptocurrencies. Their platform identifies sanctions violations within seconds and provides detailed risk scores for wallet addresses that traditional compliance software cannot match. Chainalysis offers similar capabilities but focuses more on law enforcement partnerships, while Elliptic specializes in DeFi protocol tracking that catches complex money laundering schemes.

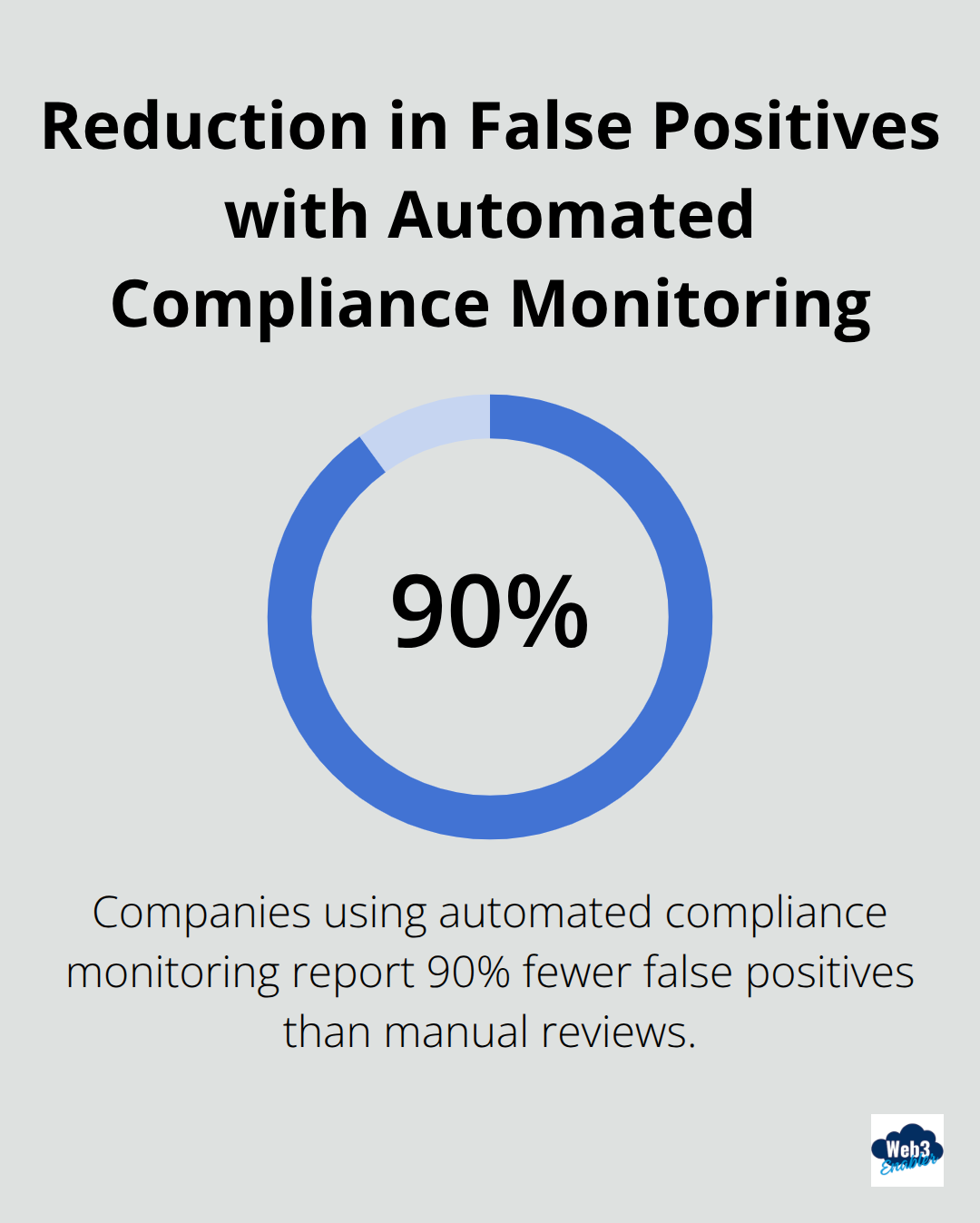

Companies that use automated compliance monitoring report 90% fewer false positives compared to manual review processes (according to recent industry surveys). Your compliance stack needs real-time screening that connects blockchain intelligence with traditional sanctions databases, because criminals exploit the gap between crypto and fiat monitoring systems.

Automated Systems That Stop Problems Before They Start

Compliance automation platforms like ComplyAdvantage and Refinitiv World-Check integrate directly with crypto exchanges through APIs that flag high-risk transactions instantly. These systems cross-reference customer data against 400+ sanctions lists and adverse media sources automatically, which eliminates the manual screening bottlenecks that slow down customer onboarding.

The most effective setups combine multiple data sources because no single provider catches every risk pattern. Smart compliance teams use webhook notifications that trigger immediate account freezes when suspicious activity occurs, rather than wait for daily batch reports that miss time-sensitive violations.

Integration Strategies That Actually Work

Your existing CRM and accounting systems need direct connections to compliance tools through standardized APIs that sync customer data and transaction histories automatically. Salesforce-native solutions eliminate data silos that create compliance gaps, while custom integrations often fail during regulatory audits because they lack proper documentation trails.

The best compliance architectures use middleware platforms that translate blockchain data into formats that traditional business systems understand. This approach reduces implementation time from months to weeks while it maintains audit readiness (which saves both time and money during regulatory reviews).

Final Thoughts

Crypto compliance requires three essential elements: robust KYC verification systems, real-time transaction monitoring, and comprehensive record keeping that survives regulatory audits. The SEC, FinCEN, and CFTC each impose different requirements that create compliance complexity, but automated tools from providers like TRM Labs and Chainalysis reduce false positives by 90% while they catch violations that manual processes miss. Proactive compliance management protects your business from the $2.8 million average penalty for sanctions violations while it builds investor confidence that drives market growth.

Companies that implement comprehensive compliance frameworks before regulators knock on their door avoid the scramble that shuts down unprepared competitors. The regulatory landscape will only get stricter as the GENIUS Act takes effect in 2027 and the SEC expands recordkeeping requirements to crypto firms. Smart businesses already prepare their compliance infrastructure to handle these changes (rather than wait for enforcement actions to force their hand).

Web3 Enabler provides Salesforce-native blockchain solutions that connect compliance tools with existing business systems. This approach makes regulatory readiness achievable without the need to rebuild your entire tech stack. We help businesses navigate crypto compliance requirements while they maintain operational efficiency.