The Clarity for Payment Stablecoins Act just dropped, and it’s about to shake up how businesses handle digital payments. This isn’t just another regulatory snooze-fest – it’s the roadmap that could finally make stablecoins mainstream.

The Clarity for Payment Stablecoins Act just dropped, and it’s about to shake up how businesses handle digital payments. This isn’t just another regulatory snooze-fest – it’s the roadmap that could finally make stablecoins mainstream.

We at Web3 Enabler are breaking down what this actually means for your business. Spoiler alert: some companies are about to get very happy, while others might need new game plans.

What the Clarity for Payment Stablecoins Act Actually Says

The Clarity for Payment Stablecoins Act creates two distinct paths for stablecoin issuers: Federal Qualified Payment Stablecoin Issuers and State Qualified Payment Stablecoin Issuers. Banks and their subsidiaries can apply directly to federal regulators, while non-bank entities must navigate state-level oversight first. This dual framework means companies like Circle and PayPal will face different compliance hurdles depending on their chosen route. The catch? Non-financial companies need approval from the Stablecoin Certification Review Committee before they can even think about issuing stablecoins.

Reserve Requirements That Pack a Punch

Every stablecoin must maintain one-to-one backing with U.S. dollars, but here’s where it gets spicy: the act allows Treasury securities and high-quality bank deposits as reserve assets. Monthly attestations and annual audits become mandatory, which means no more mystery backing like we’ve seen with some providers. The act specifically prohibits paying interest on stablecoins, effectively killing yield-bearing products that banks have been lobbying against for months.

Compliance Costs Hit Hard

Companies planning stablecoin strategies need to budget for significant compliance costs just for basic regulatory requirements. The current system forces fintechs to either partner with chartered banks or obtain multiple state money transmitter licenses across 49 states and the District of Columbia. This new framework promises to streamline operations (though at a price), potentially eliminating the need for redundant state licenses once companies achieve federal qualification.

Federal Oversight Reshapes the Market

The Treasury Department gains authority to determine whether foreign stablecoin regulations meet U.S. standards, creating a potential barrier for international providers. State regulators retain consumer protection powers, but federal preemption applies to core operational requirements. Implementation kicks in by January 2027, giving current market leaders like Tether and USD Coin time to restructure their operations.

The regulatory landscape shift sets the stage for massive changes in how businesses approach digital payments and cross-border transactions.

How This Act Changes the Stablecoin Game for Businesses

New Compliance Requirements Hit Finance Teams

The compliance burden shifts dramatically for companies that want to use stablecoins. Previously, businesses could work with any stablecoin provider without concern about regulatory status. Now companies must verify their chosen stablecoin meets federal or state qualification standards before they integrate it into payment systems. Finance teams need new due diligence processes to check issuer compliance status, reserve assets, and audit reports monthly. The act eliminates regulatory uncertainty that kept many enterprises on the sidelines, but it also creates new operational requirements that smaller businesses might struggle to manage.

Payment Processing Transforms Speed and Cost

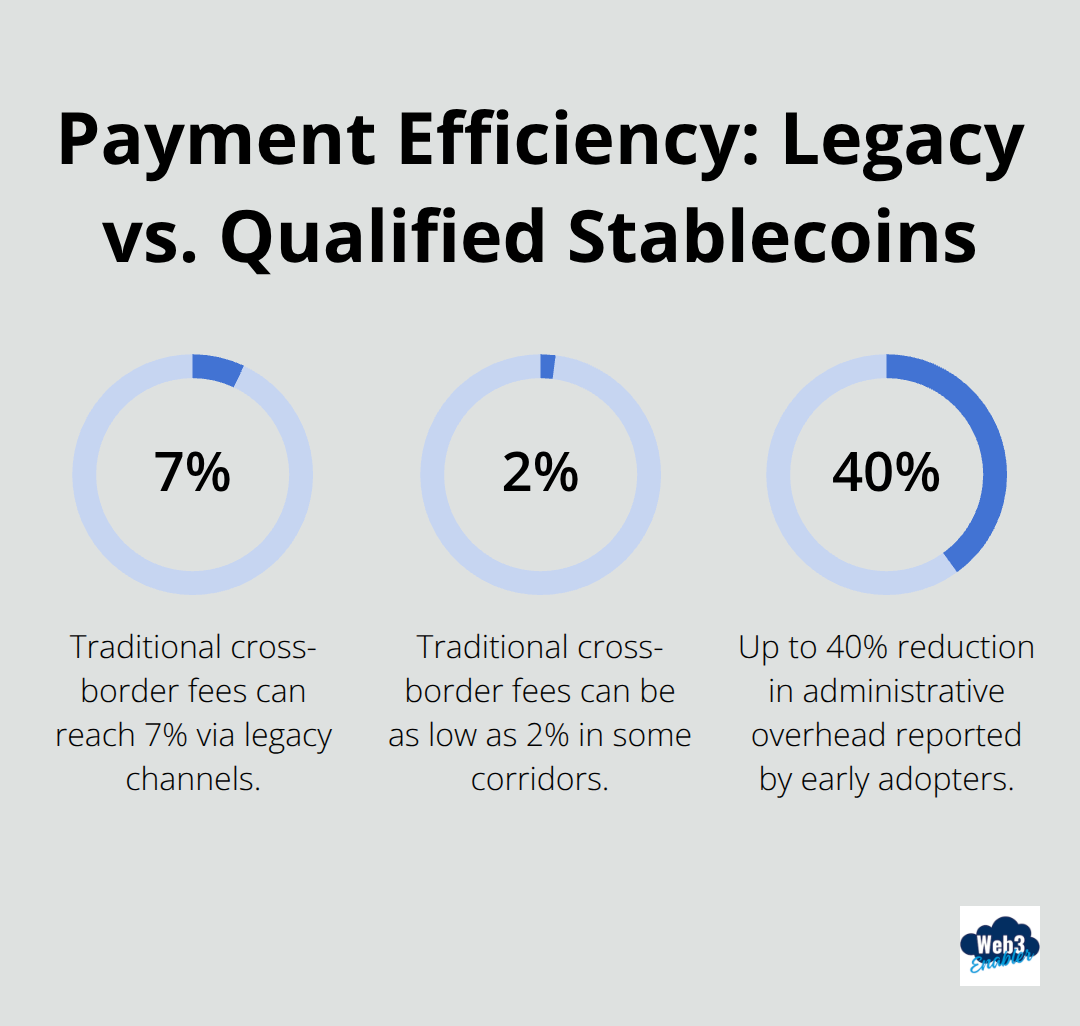

Cross-border transactions stand to benefit most from these new rules. Companies that send international payments currently face 3-7 day settlement times and fees that range from 2-7% through traditional channels. Qualified stablecoins operate 24/7 with settlement times under 60 seconds and transaction costs below 1%. Manufacturing companies with global supply chains can now pay suppliers instantly without currency conversion delays.

The programmable nature of compliant stablecoins also enables automated payment triggers based on delivery confirmations or contract milestones (which reduces administrative overhead by up to 40% according to early adopters).

Enterprise Adoption Accelerates Across Industries

Large corporations like Apple, Google, and Meta already explore stablecoin integration strategies ahead of the 2027 implementation deadline. The regulatory clarity removes legal risk that previously prevented Fortune 500 companies from experimenting with blockchain payments. Companies can now budget for stablecoin infrastructure with confidence that the regulatory framework won’t change overnight. Treasury departments gain access to dollar-backed digital assets that maintain value stability while they offer superior transaction speed and cost efficiency compared to traditional wire transfers.

But not every player in this new landscape will thrive equally. Some stablecoin providers are positioned to dominate (while others face serious challenges ahead).

Winners and Losers Under the New Stablecoin Rules

Circle and PayPal Lead the Charge

Circle dominates the regulated stablecoin market with USDC already maintaining transparent reserves and monthly attestations that align with the new requirements. Their partnerships with major financial institutions and existing compliance infrastructure give them a massive head start over competitors who scramble to meet federal standards. PayPal’s PYUSD faces a tougher path since they need to restructure their current backing mechanisms, but their existing payment network with 435 million active users creates an instant distribution advantage. Tether faces the biggest challenge despite controlling over 50% of the current stablecoin market – their opaque reserve practices and offshore structure directly conflict with the act’s transparency requirements.

Traditional Payment Giants Feel the Heat

Visa and Mastercard see their cross-border payment monopoly under serious threat as qualified stablecoins eliminate the need for their settlement networks entirely. Companies that currently pay high fees in international transfers through traditional processors can cut costs significantly with compliant stablecoins. Western Union and MoneyGram face existential pressure as their remittance business model becomes obsolete when workers can send money home instantly at near-zero cost. Banks gain new opportunities to issue their own stablecoins and capture payment flow directly (potentially bypassing card networks altogether). The shift creates winners and losers across different jurisdictions among financial institutions that embrace stablecoin infrastructure while it threatens payment processors that rely on slow, expensive legacy systems.

Enterprise Adoption Accelerates with Regulatory Clarity

Fortune 500 companies can finally integrate stablecoin payments without legal uncertainty, which creates massive opportunities for blockchain infrastructure providers. Manufacturing giants like Boeing and Caterpillar can streamline supplier payments across dozens of countries without currency conversion delays or excessive fees. The retail sector stands to benefit most as companies like Walmart and Amazon explore stablecoin integration for faster customer refunds and supplier settlements (with 24/7 availability that traditional banking cannot match).

Financial services firms gain competitive advantages through instant settlement capabilities that eliminate the delays of traditional banking hours.

Final Thoughts

The Clarity for Payment Stablecoins Act represents the most significant regulatory development for digital payments since the creation of the Federal Reserve. January 2027 will transform the business payment landscape where qualified stablecoins become legitimate alternatives to traditional banks. Companies that act now gain competitive advantages through reduced transaction costs, faster settlement times, and 24/7 payment capabilities.

The regulatory framework eliminates legal uncertainty that previously prevented enterprise adoption while it creates clear compliance pathways for businesses ready to modernize their payment systems. Smart organizations should begin evaluation of stablecoin integration strategies immediately rather than wait for full implementation. The compliance requirements demand careful planning, but the operational benefits justify the investment for companies that handle significant payment volumes or international transactions.

Web3 Enabler provides blockchain solutions that help businesses navigate this transition seamlessly within existing corporate infrastructure. Our platform enables stablecoin payment acceptance and global transfers with trusted technology partners. The stablecoin revolution starts now (and companies that embrace these changes will lead their industries while others scramble to catch up).