Buying crypto used to feel like navigating a maze blindfolded. But ACH pay crypto is changing that-it’s faster, cheaper, and way less intimidating than the old wire transfer days.

At Web3 Enabler, we’ve watched thousands of people get stuck at the payment stage. The good news? ACH transactions are about to become your new best friend for getting into crypto without the headache.

What Makes ACH Different for Crypto Buyers

Automated Clearing House stands for ACH, and it’s the plumbing that moves money between American bank accounts electronically. Unlike wire transfers, which route through a different system entirely, ACH batches transactions together and processes them in scheduled windows throughout the day. This batching is exactly why ACH costs less than wires-financial institutions spend less effort when they bundle thousands of transactions at once. You’ll typically see ACH deposits cost nothing on platforms like Kraken, which offers free ACH deposits for US customers, while wire transfers charge anywhere from $15 to $50 depending on your bank and the receiving institution.

The tradeoff is timing. ACH transactions can take up to 48 hours to settle because of those scheduled processing windows, whereas wire transfers can clear in hours. If you can wait a few days, ACH saves you real money with zero fees on the deposit side.

Why Crypto Platforms Now Prefer ACH Over Wires

Exchanges have started pushing ACH hard because it reduces their operational costs dramatically. Fewer failed transactions, lower compliance overhead, and cheaper settlement fees all trickle down to better rates for you. Platforms like CEX.IO publish transparent deposit limits for each method, so you can plan exactly how much you move via ACH each month. The speed concern is overblown for most buyers anyway-your purchased crypto becomes available for trading instantly even though the bank settlement takes a few days. The real advantage emerges when you dollar-cost average or make regular purchases. Instead of paying wire fees repeatedly, you link your bank account once and make multiple ACH buys for zero deposit charges. Kraken’s maker-taker fee model actually lowers trading fees as your monthly volume increases, so frequent ACH buyers benefit twice. This shift toward ACH reflects a broader market reality: crypto adoption grows when friction disappears, and nothing removes friction like low cost crypto payments and straightforward bank connections.

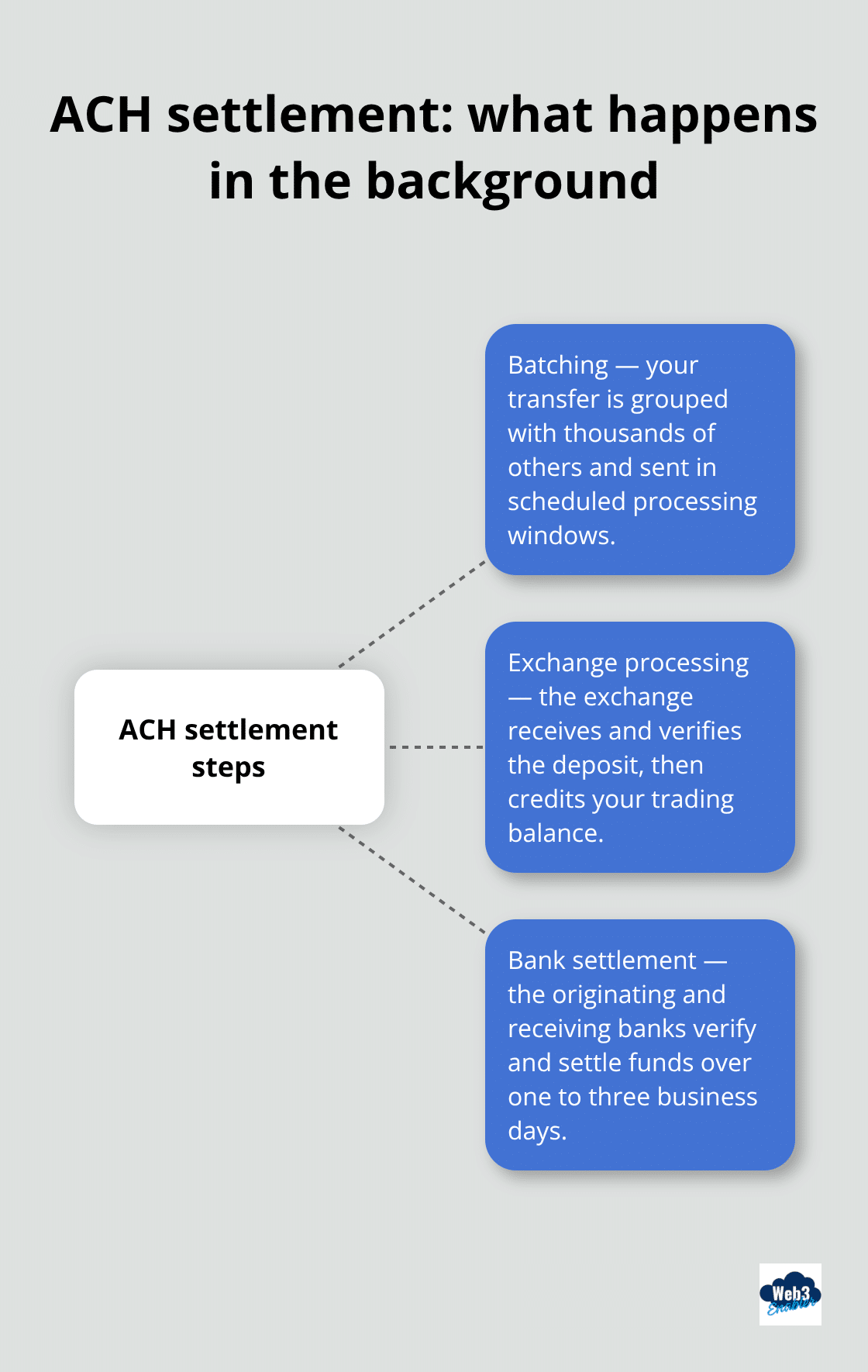

What Happens During Those Three Business Days

ACH doesn’t move money instantly, and that matters for your timeline. The network batches your transaction with thousands of others and processes them in scheduled windows throughout the day.

Your bank receives the batch, verifies the details, and then settles the funds. Each step takes time, which is why regulators and financial institutions built in those settlement windows. Some platforms move transactions from pending to processed within an hour, but funds may still take additional time to appear in your bank account depending on your specific banking institution. The key insight: your crypto arrives for trading right away, but your bank’s actual settlement happens later. This separation confuses many new buyers, so understanding it upfront prevents frustration.

Planning Around ACH Limits and Timing

Most platforms set ACH purchase limits for unverified users (typically around $1,000) and higher limits once you complete full verification. CEX.IO publishes these limits clearly, so you know exactly what you can move each month. If you need to buy more than your limit allows, you either wait for the next month’s window or complete full account verification to unlock higher amounts. Verification itself takes under two minutes on most platforms, which accelerates your ability to use ACH for larger purchases. The timing aspect matters too-if you initiate an ACH transfer on a Friday afternoon, it won’t process until Monday at the earliest, and settlement could stretch into Wednesday or Thursday. Plan your purchases with this rhythm in mind, especially if you’re trying to catch a specific price point.

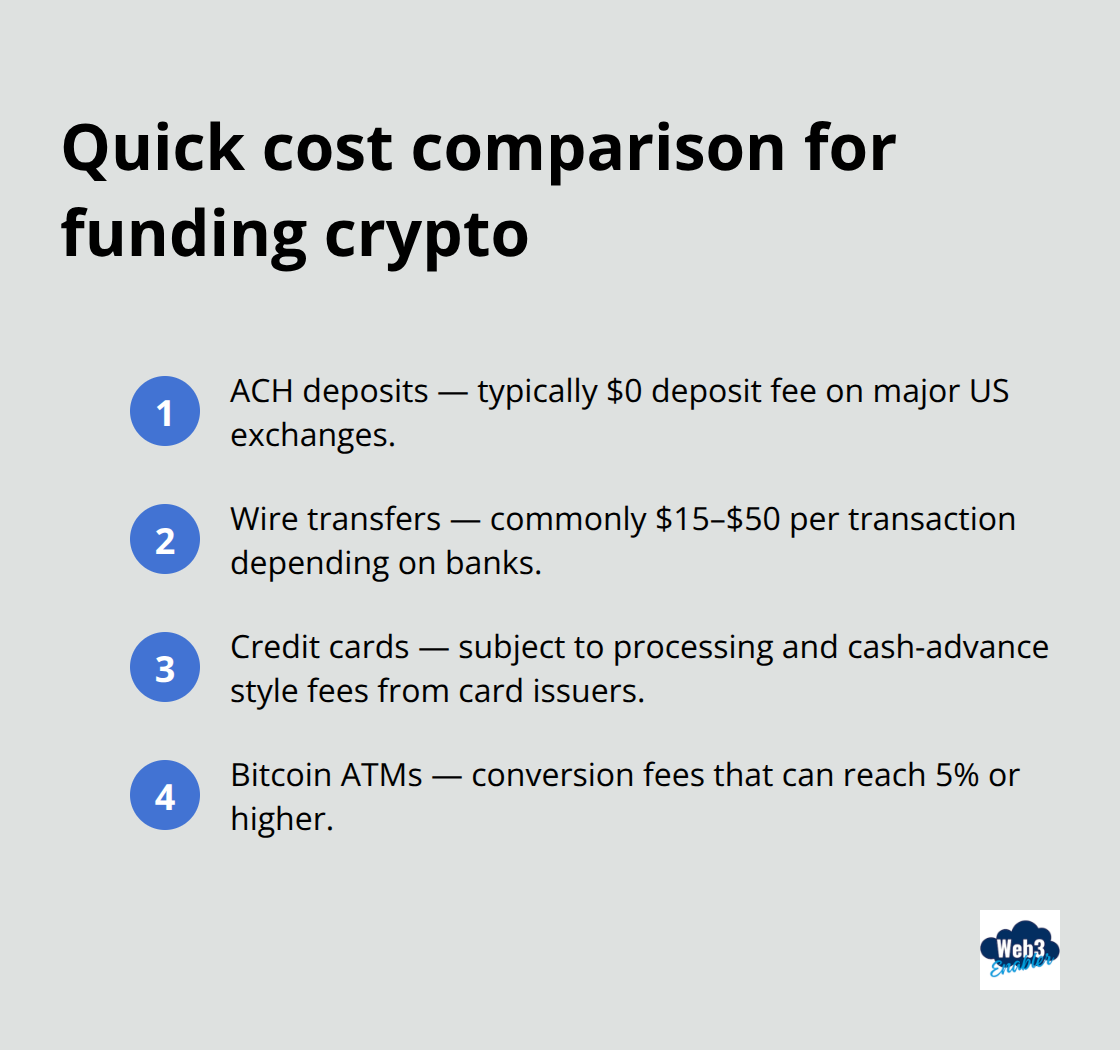

The Real Cost Comparison: ACH Versus Everything Else

Wire transfers cost $15 to $50 per transaction. Credit card purchases add processing fees plus cash-advance-style charges from your card issuer. Bitcoin ATMs charge conversion fees that can reach 5% or higher. ACH? Zero deposit fees on most platforms.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. The math becomes obvious when you make multiple purchases throughout the year. Someone who buys crypto monthly saves hundreds in fees by switching to ACH instead of wires or cards. CEX.IO supports multiple bank-transfer routes (SWIFT, SEPA, Faster Payments), and each has its own fee structure, but ACH remains the cheapest option for US customers. This cost advantage is why ACH adoption has accelerated so dramatically-it’s not flashy, but it works, and it saves real money.

Now that you understand how ACH actually works and why platforms love it, the next step is figuring out which platform fits your needs and how to set up your first transaction without tripping over common mistakes.

Getting Started with Your First ACH Purchase

Picking the right platform matters more than most people think, and the difference between a smooth first purchase and a frustrating one often comes down to which exchange you choose. Kraken stands out for US customers because it offers free ACH deposits paired with a maker-taker fee model that actually rewards you for trading more. CEX.IO takes a different approach by publishing exact deposit limits upfront for each funding method, so you know precisely how much you can move each month without surprises. OKX caters to verified US residents in eligible states and handles ACH through a secure Plaid partnership, meaning your bank connection stays encrypted throughout the process. The honest truth: all three work fine, but Kraken wins if you plan to make regular purchases because the fee structure improves as your volume grows.

Verification Happens Fast

Your verification completes instantly on most platforms, taking under two minutes to finish. This speed immediately unlocks higher ACH limits beyond the standard $1,000 threshold for unverified users. You move from account creation to your first purchase in roughly fifteen minutes, which explains why ACH adoption has exploded among people who previously avoided crypto because traditional payment methods felt too complicated or expensive.

Linking Your Bank Account Correctly

Matching the name on your exchange account to the name on your linked bank account exactly is non-negotiable-mismatches kill transactions faster than you’d expect. After that, you navigate to the buy section, select your cryptocurrency (Bitcoin, Ethereum, stablecoins like USDC), punch in your desired USD amount, choose Bank transfer as your payment method, and select your linked bank from the dropdown. The platform shows you a preview with exact pricing and fees before you confirm, so no hidden surprises appear after you’ve already committed.

Understanding the Settlement Timeline

Your purchased crypto becomes available for trading immediately, even though your bank’s actual settlement continues in the background for up to three business days. This separation confuses newcomers constantly, so understanding it prevents panic when your bank account hasn’t moved yet but your exchange balance shows your crypto. Some platforms temporarily restrict withdrawals during the settlement period, so plan accordingly if you’re thinking about moving your holdings to a hardware wallet right away.

Now that you’ve set up your account and executed your first purchase, the real challenge emerges: avoiding the mistakes that trip up most new ACH buyers.

Where ACH Buyers Go Wrong

Settlement Timing Confuses Everyone

Most ACH mistakes stem from misunderstanding the 1-3 business days settlement window, and this confusion costs real money when people panic-sell or miss price movements they thought they’d captured. The settlement timeline works like this: your bank processes the ACH request in batches throughout the day, your exchange receives the batch within 24 hours, and then your bank actually moves the funds over the next one to three business days. Your crypto shows up for trading immediately, but your bank account won’t reflect the outgoing transfer for several days. This separation between when crypto arrives and when your bank settles the transaction confuses nearly everyone on their first purchase.

If you initiate an ACH transfer on Friday afternoon, nothing happens until Monday morning at the earliest, and settlement often stretches to Wednesday or Thursday. Most people initiate a purchase, see their crypto arrive for trading, then panic when their bank account hasn’t moved yet and assume something went wrong. Nothing went wrong-the system is working exactly as designed, and your bank will eventually settle the transaction. Plan your ACH purchases with this rhythm in mind, especially if you’re trying to catch a specific price point. Waiting for settlement means you can’t time the market precisely, so dollar-cost averaging becomes a smarter strategy than trying to buy the exact dip.

Hidden Fees and Limits Destroy Your Budget

Hidden fees and limits destroy ACH budgets faster than people expect, and most platforms bury these details in settings menus instead of displaying them upfront. CEX.IO actually publishes deposit limits for each funding method directly on their platform, which makes planning straightforward, but most exchanges force you to click through multiple screens to find this information. Unverified accounts typically max out at $1,000 per purchase, but verification takes under two minutes and unlocks higher limits immediately.

The real trap isn’t the limits themselves but the spreads platforms charge on top of ACH deposits. Some exchanges quote you a price that includes their spread, so the actual cost per Bitcoin or Ethereum exceeds what you see on the live market data. Compare the price you’re quoted against the real-time market price on CoinGecko or another independent source before confirming any purchase. ACH itself carries zero deposit fees on platforms like Kraken, but some exchanges charge withdrawal fees that can reach 1 percent or higher depending on the asset and destination wallet. Stablecoins like USDC typically cost less to withdraw than Bitcoin, so moving smaller amounts out frequently gets expensive.

Security Requires Your Active Participation

Security should dominate your ACH strategy more than most people realize, and linking your bank account to any exchange creates a direct connection that malicious actors target constantly. Enable two-factor authentication on your exchange account immediately, and use an authenticator app like Google Authenticator instead of SMS-based 2FA, which can be intercepted. Never use the same password across multiple exchanges or services, and a password manager like Bitwarden or 1Password makes managing unique passwords painless.

When you withdraw your purchased crypto to a hardware wallet like Trezor, verify the withdrawal address character-by-character before confirming the transaction. Malware can alter clipboard contents, so copying and pasting an address without verification has cost people thousands in lost funds. Your bank account name must match your exchange account name exactly, and any mismatch kills the ACH transaction, but scammers exploit this verification requirement by creating accounts under your name and attempting transfers to drain your linked bank account. If you see ACH transactions you didn’t initiate, contact your bank and the exchange immediately. Most platforms have fraud protections and PCI-DSS certification (which means they meet strict payment security standards), but your personal security matters more than the platform’s security infrastructure.

Final Thoughts

ACH pay crypto has fundamentally shifted how regular people access digital assets without the friction that plagued earlier buyers. Wire transfers demanded patience and cash, credit cards added hidden charges, and Bitcoin ATMs charged conversion fees that made small purchases pointless. ACH removes these barriers by offering zero deposit fees, straightforward bank connections, and settlement timelines that work for anyone willing to plan ahead.

Your first ACH purchase teaches you more than any article can. You’ll experience the settlement timeline firsthand, understand why verification matters, and recognize how much money you save compared to traditional payment methods. The mistakes we covered aren’t theoretical-they happen to real buyers every day, but knowing about them in advance means you’ll avoid the panic and frustration that derails newcomers.

If you’re building a business around blockchain technology rather than speculating on price movements, the landscape looks different. We at Web3 Enabler help companies integrate blockchain into their existing infrastructure through Salesforce-native solutions that handle payments, compliance, and automation without the speculation angle. Visit Web3 Enabler to see what’s possible when you connect existing systems with blockchain infrastructure.